MNI US MARKETS ANALYSIS - No Bounce for USD Index

Highlights:

- USD Index consolidates at lower levels, falling wedge in play

- French, Spanish inflation data creeps ahead of expectations

- PCE, Michigan sentiment data in focus

US TSYS: Paring Gains Ahead PCE Prices, UofM Sentiment & Inflation Data

- Taking cues from EGBs - Treasuries are currently trading modestly weaker, low end of narrow overnight range as rates retreat from late Thursday's near 2-month highs (TYU5 112-03). Decent volumes with the Sep'25 10Y contract just over 300k.

- Tsy Sep'25 10Y contract currently trades -5.5 at 111-27, initial technical support at 111-11+/110-25+ (Low Jun 25 / 50-day EMA). Key resistance above at 112-23 (High May 1). Curves mildly flatter: 2s10s -.121 at 51.707, 5s30s -1.243 at 99.060.

- Relative calm on the geopolitical front with Israel/Iran ceasefire holding, market focus on today's data with PCE prices kicking off at 0830ET, final U of M sentiment and inflation at 1000ET.

- NY Fed Williams starts off today's Fed speaker schedule at 0730ET - shouldn't be market moving as he chairs a closed press session at the Bank for International Settlements. Cleveland Fed Hammack & Boston's Cook will participate at a Fed listens event at 0915ET (no text, Q&A).

- Short week next week - Friday closed for Independence Day holiday - which brings the June employment data forward to Thursday - sharing the session with weekly jobless claims and factory orders and ISM services data.

SOFR: Long Setting Dominated In Futures On Thursday

OI data points to a mix of net long setting and short cover through most of the SOFR blues on Thursday, with the former dominating.

- The only exception to that theme came via net short setting in SFRM5, as the strip twist flattened.

- Data and speculation surrounding Fed Chair Powell’s successor provided support in early NY trade, before a bid further out the curve underpinned into the close.

| 26-Jun-25 | 25-Jun-25 | Daily OI Change |

| Daily OI Change In Packs |

SFRM5 | 1,289,435 | 1,272,599 | +16,836 | Whites | +32,484 |

SFRU5 | 1,131,772 | 1,139,253 | -7,481 | Reds | +52,684 |

SFRZ5 | 1,274,813 | 1,244,080 | +30,733 | Greens | +17,453 |

SFRH6 | 984,028 | 991,632 | -7,604 | Blues | +1,201 |

SFRM6 | 866,774 | 850,359 | +16,415 |

|

|

SFRU6 | 828,120 | 819,441 | +8,679 |

|

|

SFRZ6 | 946,686 | 923,299 | +23,387 |

|

|

SFRH7 | 703,848 | 699,645 | +4,203 |

|

|

SFRM7 | 645,409 | 637,336 | +8,073 |

|

|

SFRU7 | 456,232 | 451,223 | +5,009 |

|

|

SFRZ7 | 408,819 | 407,349 | +1,470 |

|

|

SFRH8 | 303,714 | 300,813 | +2,901 |

|

|

SFRM8 | 231,041 | 234,705 | -3,664 |

|

|

SFRU8 | 202,032 | 199,719 | +2,313 |

|

|

SFRZ8 | 179,177 | 176,235 | +2,942 |

|

|

SFRH9 | 140,746 | 141,136 | -390 |

|

|

US TSY FUTURES: Long Setting At The Fore Again On Thursday

OI data points to meaningful net long setting in curve-wide terms during Thursday’s rally, with the only exception to that theme coming via modest net short cover in US futures.

- TY futures accounted for ~$5.4mn DV01 of the ~$13.4mn DV01 in fresh net longs added across the curve on the day.

- 3/4 sessions of the week have seen relatively meaningful net long setting.

| 26-Jun-25 | 25-Jun-25 | Daily OI Change | OI DV01 Equivalent Change ($) |

TU | 4,253,603 | 4,184,107 | +69,496 | +2,690,467 |

FV | 7,121,394 | 7,081,149 | +40,245 | +1,756,149 |

TY | 5,019,882 | 4,939,441 | +80,441 | +5,368,787 |

UXY | 2,404,819 | 2,378,961 | +25,858 | +2,279,631 |

US | 1,760,130 | 1,760,976 | -846 | -106,900 |

WN | 1,887,275 | 1,879,641 | +7,634 | +1,392,661 |

|

| Total | +222,828 | +13,380,794 |

EUROPE ISSUANCE UPDATE:

Belgium Issuance Update

Belgium Increases OLO Funding Target for 2025 by E5.0bln:

- Belgium's gross borrowing requirements have increased by E7.83bln to E52.52bln "on the back of higher net financing requirements (+ 8.0 billion euro) whose increase is, amongst others, due to rising defence spending."

The following from the press release:

- "The Belgian Debt Agency plans to issue 49.35 billion euro of long- and medium-term debt. It increased its OLO-funding target by 5.0 billion euro to 47.00 billion euro. As of Friday 27 June, 31.64 billion euro of OLOs have been issued, corresponding to 67.3% of the new target."

- "Short term debt is now expected to rise, in net terms, by 3.17 billion euro, as opposed to 0.34 billion euro mentioned in the original funding plan. The outstanding amount of Treasury Certificates is anticipated to increase by 3.98 billion euro over 2025."

MNI don't expect any additional Belgian auctions at this stage.

- There are still 5 conventional and 5 ORI operations scheduled for H2-25 and with just over E15bln left to issue and auction sizes having been over E3bln for conventional auctions and E0.5bln for ORIs it just means we won't see the usual reduction in auction sizes through H2.

Italy auction results

- Looks like a solid set of bid-to-covers for the 5-year lines (1.79x and 1.80x), but that's likely down to the smaller-than-usual E1.5bln auction sizes.

- The 2.95% Jul-30 BTP had averaged a 1.54x bid-to-cover ratio across four auctions since February, but for amounts issued between E3.00-E3.75bln.

- E1.5bln of the 2.95% Jul-30 BTP. Avg yield 2.68% (bid-to-cover 1.79x).

- E1.5bln of the 2.70% Oct-30 BTP. Avg yield 2.74% (bid-to-cover 1.80x).

- E3.5bln of the 3.60% Oct-35 BTP. Avg yield 3.48% (bid-to-cover 1.51x).

- E2bln of the 1.05% Apr-34 CCTeu. Avg yield 3.16% (bid-to-cover 1.56x).

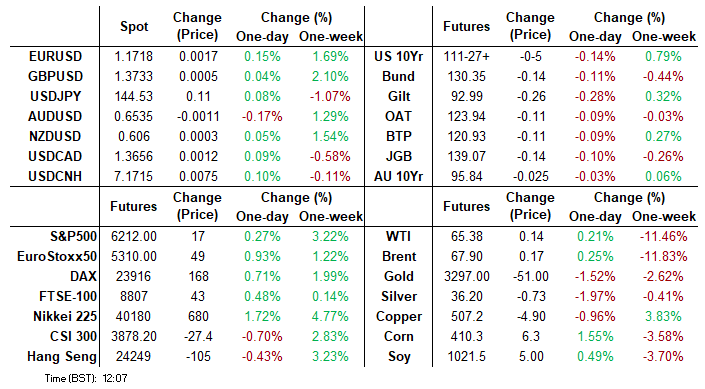

FOREX: USDCAD Consolidating Weekly Decline as US & Canada Data Awaited

- The sharp moves/reversals for both oil prices and the dollar this week have provided offsetting forces for the USDCAD exchange rate. However, the renewed greenback pessimism has taken its toll, leaving USDCAD around 0.6% below last Friday’s close.

- Monday’s spike to 1.3798 appears technically corrective, and the primary downtrend is bolstered by the 50-day EMA capping the topside for now. The pair has not been above this average since early April.

- We have US and Canada data today at 1330BST (0830ET), and a continuation lower for USDCAD would place initial attention on yesterday’s low of 1.3618. The US May PCE report should be impactful for clues on latest consumer momentum amidst strong income growth. Core PCE is seen around 0.15% M/M judging by unrounded estimates. In Canada, April GDP is expected to decline to 1.3% Y/y from 1.7% in the prior release.

- Overall, attention for USDCAD remains on key support and the bear trigger, which has been defined at 1.3540, the Jun 16 low. Clearance of this price point would resume the downtrend. Goldman Sachs have continued to argue that the macro fundamentals support a stronger Canadian dollar, and continue to expect USDCAD to grind lower to 1.34 in 6 months.

FOREX: USD Index Consolidates At Lower Levels

- Currency markets are more sanguine early Friday, but the lack of any reversal off lows for the USD Index provides another bearish signal as the price holds close to the cycle low of 96.997. This keeps the falling wedge pattern in play, with a firm break of the downtrendline drawn off the late 2024 lows still a possibility ahead of next week's payrolls print.

- This morning's SEK strength has taken a breather in the last 20 minutes, but EURSEK and USDSEK are nonetheless 0.7% below this morning's levels. There wasn't an obvious fundamental driver for the earlier selloff (this morning's Swedish PPI data was actually quite dovish), but yesterday's lows remain intact for both crosses.

- USDCAD has pulled back from its recent highs. The primary downtrend remains intact and short-term gains appear to have been corrective. Key support and the bear trigger has been defined at 1.3540, the Jun 16 low.

- Core PCE data will mark the highlight of the Friday calendar, with final University of Michigan confidence numbers set to follow. The central bank speaker slate is busier: ECB's Rehn & Cipollone speak, as well as Fed's Williams, Hammack & Cook

OPTIONS: Expiries for Jun27 NY cut 1000ET (Source DTCC)

- EUR/USD: $1.1400(E1.3bln), $1.1415-25(E1.1bln), $1.1500(E531mln), $1.1550-55(E525mln), $1.1600(E1.1bln)

- USD/JPY: Y144.50($581mln)

- AUD/USD: $0.6550-70(A$800mln)

- USD/CAD: C$1.3630-50($1.3bln), C$1.3740-50($730mln)

EQUITIES: E-Mini S&P Remains Above Bull Trigger, Trading at Cycle Highs

- The trend condition in Eurostoxx 50 futures remains bearish, however, the recovery from Monday’s low appears to be a potential reversal. The contract has traded through the 20- and 50-day EMAs. A clear break of both averages would strengthen a reversal theme and signal scope for a stronger recovery. This would open 5486.00, the May 20 high and bull trigger. On the downside, a breach of Monday’s 5194.00 low would reinstate a bearish theme.

- The trend condition in S&P E-Minis is unchanged, it remains bullish and this week’s fresh cycle highs reinforces current conditions. Short-term resistance and a bull trigger at 6128.75, the Jun 11 high, has been breached. The clear break confirms a resumption of the uptrend that started Apr 7. The 6200.00 handle has been cleared, this opens 6249.00, the Feb 21 high. Key support is at the 50-day EMA - at 5952.18. A clear break of it would signal a reversal.

COMMODITIES: Gold Below Two Important Short-Term Support Points

- WTI futures maintain a softer tone following the reversal from Monday’s high. Support to watch is at the 50-day EMA, at $64.55. It has been pierced, a clear break of it would signal scope for a deeper retracement. This would expose $58.87, the May 30 low. On the upside, initial resistance to watch is $71.20, the 50.0% retracement of the Jun 23 - 24 high-low range. Key resistance is at $78.40, the Jun 23 high.

- The trend condition in Gold remains bullish and the latest pullback is considered corrective - for now. Note that today’s move down has resulted in a test of two important short-term support points; $3290.9, the 50-day EMA, and 3294.8, a trendline drawn from the Dec 30 ‘24 low. A clear break of both support points would signal scope for a deeper correction - this would expose $3245.5. A reversal higher would refocus attention $3451.3, the Jun 16 high.

| Date | GMT/Local | Impact | Country | Event |

| 27/06/2025 | 1130/0730 | New York Fed's John Williams | ||

| 27/06/2025 | 1230/0830 | *** | Gross Domestic Product by Industry | |

| 27/06/2025 | 1230/0830 | *** | Personal Income and Consumption | |

| 27/06/2025 | 1230/0830 | *** | Gross Domestic Product by Industry | |

| 27/06/2025 | 1315/0915 | Cleveland Fed's Beth Hammack | ||

| 27/06/2025 | 1400/1000 | *** | U. Mich. Survey of Consumers | |

| 27/06/2025 | 1400/1000 | ** | University of Michigan Surveys of Consumers Inflation Expectation | |

| 27/06/2025 | 1500/1100 | Finance Dept monthly Fiscal Monitor (expected) | ||

| 27/06/2025 | 1700/1300 | ** | Baker Hughes Rig Count Overview - Weekly | |

| 27/06/2025 | 1700/1300 | ** | Baker Hughes Rig Count Overview - Weekly |