OPTIONS: Expiries for Jun27 NY cut 1000ET (Source DTCC)

- EUR/USD: $1.1400(E1.3bln), $1.1415-25(E1.1bln), $1.1500(E531mln), $1.1550-55(E525mln), $1.1600(E1.1bln)

- USD/JPY: Y144.50($581mln)

- AUD/USD: $0.6550-70(A$800mln)

- USD/CAD: C$1.3630-50($1.3bln), C$1.3740-50($730mln)

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

GERMAN DATA: Mixed Signals In Latest Labour Market Data

Latest German labour market data was mixed - employment continues its stabilization but unemployment ticked up considerably, with the employment agency looking for further layoffs. The IFO employment barometer remains contractionary but is on 10-month highs.

- Unemployment rose noticeably more than expected, by the quickest pace since July 2022 (34k vs 12k cons, 6k Apr) on a seasonally-adjusted basis. The unemployment rate meanwhile remained at 6.3% for the third consecutive month, as expected.

- The expected number of employees impacted by 'Kurzarbeit' (which has to be reported in advance by companies and can be interpreted as an early indicator for future use of state benefits) was little changed in May at around 46k.

- New vacancies reversed their April jump in May, printing at 114k, the lowest since the pandemic. Overall vacancies continue their longer-term downtrend in place since 2022.

- Employment was unchanged in April, meanwhile (lined out in previous bullet).

- Recall the IFO employment index jumped to 95.2 in May, a 10-month high - IFO sees a slower pace of job cuts ahead, especially in industry (manufacturing employment decreased 0.64% Q/Q, worst rate since Q2'20).

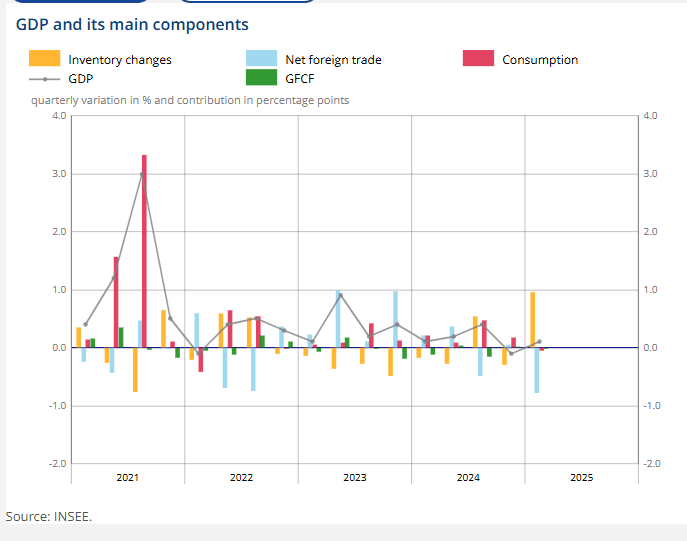

FRANCE DATA: Sharp Downward Revision To Q1 Export Growth

French Q1 GDP confirmed flash estimates at 0.1% Q/Q, but this masked substantial revisions in the net trade breakdown. Export growth was -1.8% Q/Q, revised from a -0.7% flash print. Import growth was revised up a tenth to 0.5% Q/. With fewer products sold on the export market than implied by the flash release, the contribution of net inventories to the quarterly GDP reading was revised up 0.5pp to 1.0 points.

- Household consumption growth was revised down to -0.2% Q/Q from 0.0% in the flash, but this was offset by a two tenth upward revision to gross fixed capital investment to 0.0% Q/Q. Weakness in consumption growth appears to have continued into Q2, with April consumer spending at 0.3% M/M (vs 0.8% cons).

- Government consumption growth was 0.2% Q/Q, up from 0.1% in the flash.

- The savings rate inched up to 18.8% (vs 18.5% prior), while total hours worked declined 0.4% Q/Q (vs -0.2% prior).

EGB OPTIONS: Schatz Put Ladder

DUQ5 107.40/107.30/106.90 broken put ladder -0.5 (receive) in 7k.