MNI US MARKETS ANALYSIS - Meeting Details Not Exp. Until Close

Highlights:

- Trump/Putin meeting set to begin from 1500ET, no outcomes expected until well after the market close

- Treasury curve mildly steeper ahead of fresh data risk

- HKD continues to strengthen off the weak-side of the band, tighter liquidity eyed

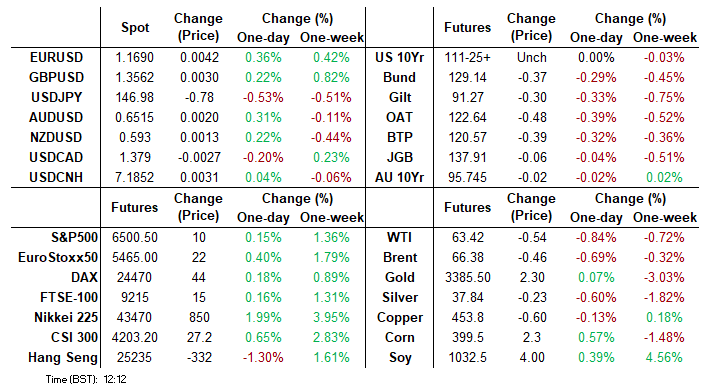

US TSYS: Mildly Twist Steeper Awaiting An Important Docket

- Treasuries have seen the front end keep to a narrow range overnight ahead of an important docket but the longer end biased lower by EGBs, which see more sizeable losses in a continuation of prior bear steepening trends rather than a fresh catalyst.

- Today sees important data releases including retail sales, import prices, industrial production and the U.Mich consumer survey, Chicago Fed’s Goolsbee offering his latest view after yesterday’s strong PPI report and then the Trump-Putin meeting at 1500ET.

- Cash yields are 0.5bp lower (2s and 3s) to 1bp higher (20s and 30s).

- 5s30s sits at 107.0bps as it starts to eye ytd highs of 108.5bps seen in the aftermath of the Aug 1 nonfarm payrolls report.

- TYU5 trades at 111-26 for near unchanged on the day, on subdued cumulative volumes of 225k ahead of an important docket.

- Yesterday’s pre-PPI high of 112-14 stopped just short of testing resistance at 112-15+ (Aug 5 high). The contract remains some way from support at 110-19+ (Jul 24 low) despite the pullback, although some may look at 111-19+ as a tentative level in puzzling trading after the initially dovish reaction to Tuesday’s CPI report.

- Data: Retail sales Jul (0830ET), Import prices Jul (0830ET), IP & Cap util Jul (0915ET), U.Mich consumer survey Aug prelim (1000ET), Business inventories Jun (1000ET), TIC Flows Jun (1600ET)

- Fedspeak: Goolsbee on CNBC (0830ET) – see STIR bullet

- Politics: President Trump departs the White House for Anchorage at 0645ET, with scope for subsequent headlines from the press travel pool, before the Trump-Putin meeting at 1500ET.

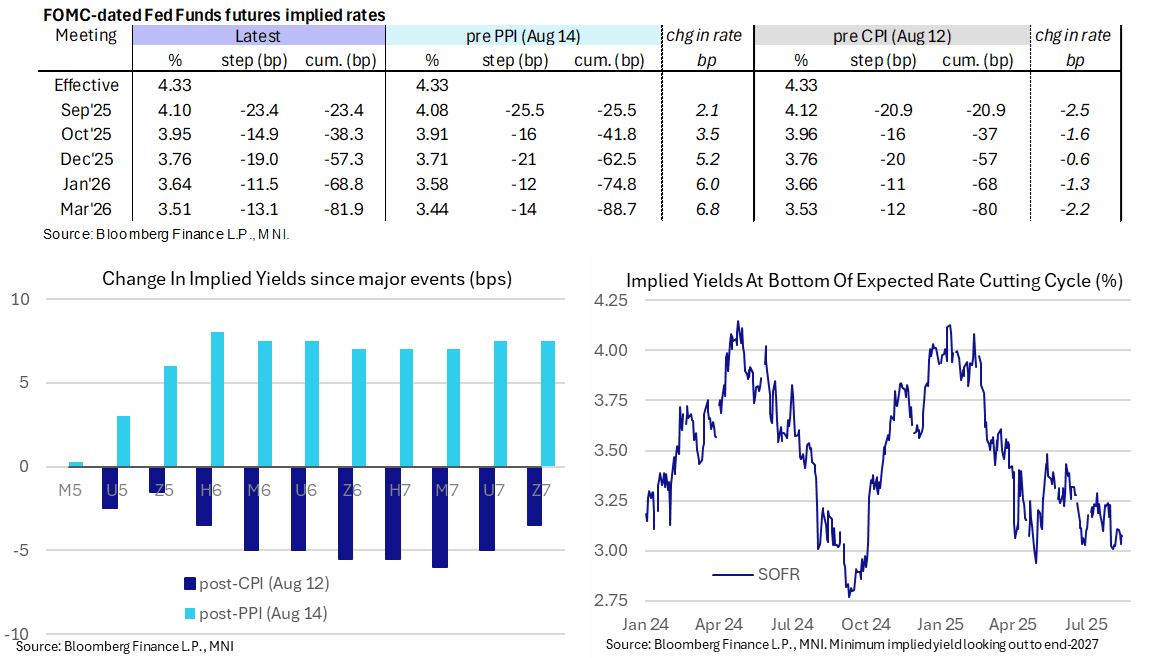

STIR: Fed Rates Holding Most Of PPI Shift, Retail Sales and More Ahead

- Fed Funds implied rates hold the bulk of their shift higher on yesterday’s far stronger than expected PPI report, although with the path for near-term meetings slightly below pre-CPI levels.

- Cumulative cuts from 4.33% effective: 23.5bp Sep, 38.5bp Oct, 57.5bp Dec, 69bp Jan and 82bp Mar.

- The SOFR implied terminal yield of 3.075% (SFRH7) is near unchanged on the day, hovering around five cuts from current levels.

- Data is likely to be in the driving seat for the bulk of today’s session, with retail sales, import prices, industrial production and the U.Mich consumer survey all due. Geopol remains in focus though ahead of the Trump-Putin meeting at 1500ET.

- Chicago Fed’s Goolsbee (’25 voter, dove) speaks on CNBC at 0830ET for a post-PPI update. He said following CPI that FOMC meetings in the fall are "going to be live" but, notably for one of the more dovish FOMC members, that he's "uneasy" about the idea that tariffs have only a one-off impact on prices and that he wants more surety that inflation won’t be persistent.

- Looking ahead to next week, Fed Chair Powell’s Jackson Hole speech has been formerly set for 1000ET on Friday (Aug 22) titled “Economic Outlook and Framework Review”.

- Marc Summerlin confirmed yesterday that he’s on a list of contenders for the next Fed Chair role. He noted he is close friends with Tsy Sec Bessent with the two having discussed monetary policy “weekly for probably 12 years”. Kalshi has Summerlin at just 3% odds though, with current Fed Governor Christopher Waller in the lead (30%) followed by Kevin Hassett (21%) and Kevin Warsh (14%).

US-RUSSIA: Trump-Putin Summit Schedule

The high-profile summit between US President Donald Trump and his Russian counterpart, Vladimir Putin, gets underway later today in Anchorage, Alaska. Trump is set to leave the White House at 06:45ET (11:45BST/12:45CET/19:45JST) and arrive at around 11:00 local time (15:00ET/20:00BST/21:00CET/04:00JST). He will then depart for Washington, D.C., at 17:45 local time (21:45ET/02:45BST/03:45CET/10:45JST), giving the two leaders just under seven hours together.

- The Kremlin has said that an initial tete-a-tete involving just Trump, Putin and their interpreters will get underway ~11:30 local time (15:30ET/20:30BST/21:30CET/04:30JST). This will be followed by talks involving the delegations from both sides, and then a "working breakfast".

- As noted on 14 August, the Russian delegation is a senior and sizeable one of five high-ranking ministers and officials (see 'US-RUSSIA: Kremlin: Putin-Trump Summit Starts 11:30 Local, Joint Presser After', 10:27BST). The Guardian reports that the US delegation is smaller, consisting of three senior officials: Secretary of State Marco Rubio, Secretary of Defense Pete Hegseth, and Middle East envoy Steve Witkoff. The Kremlin had previously talked up a 'five-to-five' summit.

- The Kremlin has talked up the prospect of a joint press conference after the summit, but earlier in the week, Trump raised the prospect that if the summit does not go to his liking, he may walk out without doing the presser with Putin. There is no set time for any presser yet.

SOFR: Net Short Setting Dominated In Futures Following PPI

OI data points to net short setting dominating in SOFR futures during the hawkish repricing that came in the wake of yesterday's PPI data, comfortably outweighing any pockets of net long cover through the blues.

| 14-Aug-25 | 13-Aug-25 | Daily OI Change |

| Daily OI Change In Packs |

SFRM5 | 1,200,338 | 1,197,179 | +3,159 | Whites | +25,352 |

SFRU5 | 1,330,689 | 1,337,336 | -6,647 | Reds | +36,903 |

SFRZ5 | 1,388,398 | 1,364,103 | +24,295 | Greens | +9,951 |

SFRH6 | 1,023,668 | 1,019,123 | +4,545 | Blues | +11,501 |

SFRM6 | 913,633 | 889,477 | +24,156 |

|

|

SFRU6 | 891,117 | 874,073 | +17,044 |

|

|

SFRZ6 | 1,001,320 | 1,020,537 | -19,217 |

|

|

SFRH7 | 757,874 | 742,954 | +14,920 |

|

|

SFRM7 | 917,732 | 921,532 | -3,800 |

|

|

SFRU7 | 590,126 | 587,080 | +3,046 |

|

|

SFRZ7 | 591,142 | 579,821 | +11,321 |

|

|

SFRH8 | 344,178 | 344,794 | -616 |

|

|

SFRM8 | 274,676 | 271,499 | +3,177 |

|

|

SFRU8 | 206,514 | 205,294 | +1,220 |

|

|

SFRZ8 | 234,591 | 231,188 | +3,403 |

|

|

SFRH9 | 156,274 | 152,573 | +3,701 |

|

|

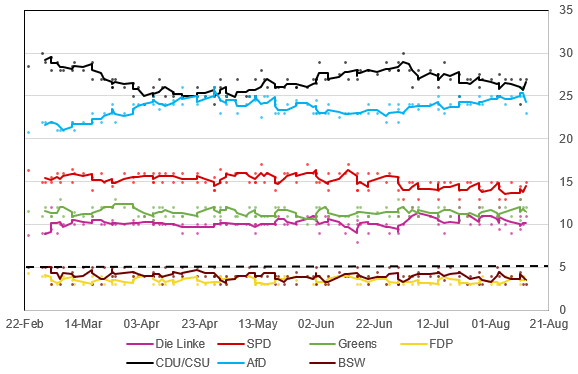

GERMANY: Merz's CDU Regains Top Spot After Shock AfD Lead Poll

Following a shock opinion poll from Forsa published earlier in the week, in which the far-right Alternative for Germany (AfD) recorded its joint-highest level of support on record, the trend has reverted to the norm, showing the AfD in second place behind Chancellor Friedrich Merz's centre-right Christian Democratic Union (CDU). All three polls posted after the Forsa poll had the CDU in first place, with the AfD in second and the junior coalition partner, the centre-left Social Democrats (SPD), third.

- The next federal election is not due until 2029, but that is not to say current polling and gov't support will not play a significant role in German policy making or affect gov't stability.

- Should the AfD develop a consistent polling lead over the CDU, it could lead to increased pressure on Merz from the conservative wing of the party to swing to the right to counter AfD gains. This trend has been seen in France and the UK, where both gov'ts have sought to talk tough on immigration to try and wrest control back from right-wing parties currently topping the polls.

- In contrast to both France and the UK, the German gov't comprises both the centre-right and centre-left. A hardline shift to the right by the CDU could damage (already tepid) relations with the SPD, risking policy paralysis or public acrimony. Both issues plagued the previous 'traffic light' coalition of Olaf Scholz and contributed to its early collapse.

Chart 1. Federal Election Opinion Polling, % and 3-Poll Moving Average

Source: Forsa, INSA, YouGov, Verian, FGW, Allensbach, Infratest dimap, pollytix, MNI

FOREX: USD/JPY Remains Weaker After Conclusion of Consolidation Phase

- The USD Index trades rangebound and inside the Thursday range after the PPI print yesterday helped prompt a minor recovery in the greenback. This keeps prices either side of the 50-dma which, notably, has begun to flatten out after maintaining a solid downtrend throughout 2025.

- JPY is the strongest currency in G10, extending the breakout and bearish conclusion of the consolidation phase in USD/JPY. Recent weakness puts the price through support drawn off the early August lows as well as 146.71, a key retracement. Price action this week marks a full reversal of the previously overbought condition, keeping the downside argument in focus.

- Anticipation ahead of the Putin-Trump meeting will likely continue to dominate sentiment, particularly after Putin's positivity in comments earlier this week helped support the e-mini S&P to a new record high.

- We noted yesterday the pressure building on USD/HKD, with price action not matching the pattern of HKMA intervention. That move extended overnight, and is still building at typing, putting spot down to new pullback lows of 7.8119 shortly after the European open. Overnight swap rates have surged further still Friday (hitting 1.7% at typing), well ahead of the 0.3% prevailing rate mid-week and should continue to support a recovery in HIBOR fixes ahead. Today's 1m HIBOR fixed higher by 41bps, hitting 1.45% for the highest fix since mid-May. It's these factors that should work against the HKD carry trade (selling HKD, buying USD), evident in the further tightening of the HKD forward discount today: down 975 points from as high as 1270 this month.

- Just ahead of today's close, Presidents Trump and Putin are set to meet in Alaska. The meeting is set to continue for an indeterminate period of time before, reportedly, the Presidents will hold a joint press conference (however Trump stated that a joint appearance would be contingent on results of the meeting itself). Any appearance is likely to be well after the market close, leaving any reaction to Monday trade.

HKD: Liquidity Tightening Further; Triggering More Carry Unwind

- We noted yesterday the pressure building on USD/HKD, with price action not matching the pattern of HKMA intervention. That move extended overnight, and is still building at typing, putting spot down to new pullback lows of 7.8119 shortly after the European open.

- Tighter local liquidity and the lagged effect of HKMA HKD buying remains the key driver here, but headlines such as: "*MAINLAND INVESTORS BUY $4.6B OF HK STOCKS ON FRIDAY, MOST EVER" - bbg will also provide a tailwind ahead.

- Overnight swap rates have surged further still Friday (hitting 1.7% at typing), well ahead of the 0.3% prevailing rate mid-week and should continue to support a recovery in HIBOR fixes ahead. Today's 1m HIBOR fixed higher by 41bps, hitting 1.45% for the highest fix since mid-May. It's these factors that should work against the HKD carry trade (selling HKD, buying USD), evident in the further tightening of the HKD forward discount today: down 975 points from as high as 1270 this month.

- Sell-side views are mixed ahead: HSBC write that HKD T/N points at -6 still provide attractive carry, which should keep USD/HKD supported near 7.85, but the now-low aggregate balance may mean HKD is more sensitive to equities and HKD demand ahead. Elsewhere Malayan Banking Berhad see it as a "matter of time" for USD/HKD to pull away from the upper bound, as markets search for the tipping point in the aggregate balance.

OPTIONS: Expiries for Aug15 NY cut 1000ET (Source DTCC)

- EUR/USD: $1.1590-10(E1.3bln), $1.1750(E1.2bln)

- USD/JPY: Y147.00($572mln)

- GBP/USD: $1.3500-20(Gbp630mln)

- AUD/USD: $0.6485-00(A$681mln), $0.6523(A$562mln)

- USD/CAD: C$1.3910($995mln)

- USD/CNY: Cny7.5000($1.7bln)

EQUITIES: New Highs for E-mini S&P

- This morning saw new record highs in the e-mini S&P, extending gains on the clearance of resistance through the 6477.31 mark. This cements the underlying uptrend, exposing projection levels into 6523.63 next.

- The bounce off post-NFP lows in global equity indices persists, with the Eurostoxx 50 future recovering back above the 50-day EMA. Markets look to build a base above this level, through which additional strength refocuses attention on 5486.00, the May 20 high and bull trigger.

COMMODITIES: Gold Prices Hold Above Weekly Low

- Gold prices are off the weekly low, however bounces appear shallow at these levels, keeping price within the mid-point of the recent range. The phase of weakness into the end of July supported the view that short-term pullbacks are corrective - for now.

- WTI futures traded poorly into the Wednesday close, extending losses on the clearance of the 50-day EMA and bear trigger. Markets have built on this S/T momentum lower, with support breaking at $62.77.

| Date | GMT/Local | Impact | Country | Event |

| 15/08/2025 | 1230/0830 | ** | Monthly Survey of Manufacturing | |

| 15/08/2025 | 1230/0830 | ** | Wholesale Trade | |

| 15/08/2025 | 1230/0830 | *** | Retail Sales | |

| 15/08/2025 | 1230/0830 | ** | Import/Export Price Index | |

| 15/08/2025 | 1230/0830 | ** | Empire State Manufacturing Survey | |

| 15/08/2025 | 1230/0830 | *** | Retail Sales | |

| 15/08/2025 | 1300/0900 | * | CREA Existing Home Sales | |

| 15/08/2025 | 1315/0915 | *** | Industrial Production | |

| 15/08/2025 | 1400/1000 | * | Business Inventories | |

| 15/08/2025 | 1400/1000 | *** | U. Mich. Survey of Consumers | |

| 15/08/2025 | 1400/1000 | ** | University of Michigan Surveys of Consumers Inflation Expectation | |

| 15/08/2025 | 1400/1000 | * | Business Inventories | |

| 15/08/2025 | 1700/1300 | ** | Baker Hughes Rig Count Overview - Weekly | |

| 15/08/2025 | 1700/1300 | ** | Baker Hughes Rig Count Overview - Weekly | |

| 15/08/2025 | 2000/1600 | ** | TICS |