MNI US MARKETS ANALYSIS - Lighter Volumes into CAD Jobs Data

Highlights:

- Treasury, FX volumes thin; GBP remains firmer on dwindling BoE rate cut prospects

- September Fed rate cut now locked in, with Miran set to join FOMC

- Canadian unemployment rate seen rising back to post-COVID high

US TSYS: Particularly Thin Volumes Ahead of Fedspeak and Trump Deliberations

- Treasuries are little changed overnight although the front end is mildly lower having reversed a rally seen on Trump yesterday choosing CEA’s Miran for a temporary Fed Governor position.

- Today sees focus on a hawkish Musalem at 1020ET before continued attention on Trump ahead with his pick for new BLS commissioner still outstanding amongst other matters.

- This BLS pick will come ahead of next week’s CPI report, clearly not having a direct impact on the report but it will still hang over its release. For recent context from the MNI Policy Team, see MNI INTERVIEW: Ex-Chief Says BLS Can Withstand Trump Pressure (Aug 2) and MNI INTERVIEW: Mounting BLS Pressure Harmful For Data- Groshen (Aug 5).

- Cash yields are 1bp higher (2s) to near unchanged (7s onwards).

- TYU5 trades at 112-02+ (-00+) on particularly low cumulative volumes of 155k.

- It’s been in a range of 111-26+ to 112-15+ this week, consolidating the shunt higher on Friday’s nonfarm payrolls and less so ISM manufacturing reports. Resistance is seen at that 112-15+ after which lies 112-23 (May 1 high) whilst support is seen at 110-19+ (Jul 24 low).

- Data: None scheduled

- Fedspeak: Musalem at 1020ET – see STIR bullet

- Politics: President Trump signs Executive Orders (1200ET) and deliver remarks (1600ET).

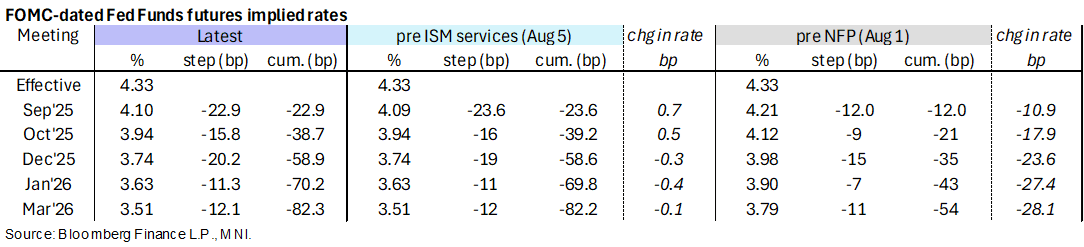

STIR: September Fed Cut Still Seen Locked In, Hawkish Musalem On The Docket

- Fed Funds implied rates are up to 2bp higher having reversed the decline seen yesterday on President Trump choosing CEA’s Miran for the temporary Fed Governor role to January after Kugler’s resignation.

- It could be that Bloomberg reporting that existing Governor Waller is an emerging prime candidate amongst Trump’s advisers for the Fed Chair role continues to carry weight although that shouldn’t impact near-term meetings.

- Cumulative cuts from 4.33% effective: 23bp Sep, 38.5bp Oct, 59bp Dec, 70bp Jan and 82.5bp Dec.

- The SOFR implied terminal yield of 3.07% (SFRH7) is unchanged on the day, implying circa five cuts from current levels.

- See MNI’s “Board-Bound Miran Has Signaled He'd Support Rate Cuts” from 1633ET yesterday for more color on the temporary position.

- JPM yesterday pulled forward the start of four consecutive cuts to September from December on the back of the news.

- St Louis Fed’s Musalem (’25 voter, hawk) is the sole scheduled event on the regular calendar, speaking on banking and credit at 1020ET (text + Q&A). He’ll be arguably the most hawkish FOMC member to have spoken since Friday’s NFP report – likely one of the seven dots who pencilled in no cut this year – and any mon pol comments will be watched accordingly.

- Expect further remarks from Trump however, with his pick for new BLS Commissioner still outstanding. He signs Executive Orders at 1200ET and is also set to deliver remarks at 1600ET.

US TSY FUTURES: Net Short Setting Across The Curve On Thursday

OI data points to net short setting across the curve on Thursday, with just under $7mln of net DV01 exposure added and the most meaningful positioning swing coming in WN futures.

| 07-Aug-25 | 06-Aug-25 | Daily OI Change | OI DV01 Equivalent Change ($) |

TU | 4,576,349 | 4,575,795 | +554 | +20,236 |

FV | 7,052,353 | 7,047,359 | +4,994 | +212,973 |

TY | 5,141,404 | 5,108,686 | +32,718 | +2,159,096 |

UXY | 2,462,273 | 2,452,174 | +10,099 | +884,940 |

US | 1,775,235 | 1,767,652 | +7,583 | +1,062,131 |

WN | 1,998,805 | 1,984,670 | +14,135 | +2,583,826 |

|

| Total | +70,083 | +6,923,201 |

SOFR: Mix Of Net Short Setting & Long Cover Seen In Futures On Thursday

OI data points to net short setting dominating through the SOFR greens on Thursday (albeit with some pockets of net long cover seen), before net long cover moved to the fore in the blues.

| 07-Aug-25 | 06-Aug-25 | Daily OI Change |

| Daily OI Change In Packs |

SFRM5 | 1,218,240 | 1,225,424 | -7,184 | Whites | +16,474 |

SFRU5 | 1,274,769 | 1,292,092 | -17,323 | Reds | +17,991 |

SFRZ5 | 1,385,112 | 1,352,639 | +32,473 | Greens | +25,013 |

SFRH6 | 1,050,983 | 1,042,475 | +8,508 | Blues | -5,780 |

SFRM6 | 887,747 | 867,062 | +20,685 |

|

|

SFRU6 | 852,882 | 856,066 | -3,184 |

|

|

SFRZ6 | 959,163 | 951,417 | +7,746 |

|

|

SFRH7 | 719,055 | 726,311 | -7,256 |

|

|

SFRM7 | 797,311 | 780,952 | +16,359 |

|

|

SFRU7 | 578,484 | 576,331 | +2,153 |

|

|

SFRZ7 | 515,737 | 511,115 | +4,622 |

|

|

SFRH8 | 334,209 | 332,330 | +1,879 |

|

|

SFRM8 | 262,305 | 267,670 | -5,365 |

|

|

SFRU8 | 205,282 | 205,702 | -420 |

|

|

SFRZ8 | 216,791 | 216,888 | -97 |

|

|

SFRH9 | 152,754 | 152,652 | +102 |

|

|

US OUTLOOK/OPINION: JPM Bring Forward Next Fed Cut To Sep From Dec

JPMorgan refined their Fed rate view after Miran was named as Gov. Kugler’s temporary replacement, pulling forward the start of four consecutive cuts to September from December.

- “Last year, Miran penned an opinion piece arguing for hawkish monetary policy. We very much doubt that remains his view today.”

- “[…] in the off chance Miran is governor by the time of the next meeting, that could imply three dissents. That’s a lot of dissents. For Powell the risk management considerations at the next meeting may go beyond balancing employment and inflation risks, and we now see the path of least resistance is to pull forward the next 25bp cut to the September meeting.”

- “We continue to look for three like-sized cuts at the subsequent three meetings before pausing indefinitely.” [They previously saw a 25bp cut in Dec before 75bp of cuts early in 2026].

- “It's not unprecedented for the Fed to ease when stocks are at or near all-time highs. It’s rarer when stocks are at the highs and inflation is above target and inflecting higher. So, an ease next meeting isn't likely to be broadly welcomed by the Committee. At the last FOMC meeting, Powell framed the labor market risks in the context of the unemployment rate. Simplifying to that one dimension, a rate of 4.4% or higher could get a larger-sized cut at the next meeting, while a rate of 4.1% or lower could prompt a few dissents for a full employment, above-target inflation cut.”

UK: Reeves & Starmer To Prepare Ground For Tax Hikes In Budget-Guardian

The Guardian reported late on 7 August that, "The chancellor and prime minister will begin to prepare the ground for tax rises and reforms from September as part of a strategy to prepare the country for a difficult budget that could be held in November". The article claims that Chancellor of the Exchequer Rachel Reeves intends to stick to the Labour manifesto commitment of not raising income tax, VAT or employee National Insurance contributions and to her fiscal rules, but that former PM Gordon Brown's call for a levy on online gambling is set to be heeded.

- The article notes that, following the 5-4 second vote split decision by the BoE on 7 August, "the MPC warned tax-raising measures in the chancellor’s first autumn budget had contributed to the rekindling of inflationary pressures hitting shoppers in the pocket across the country." With food price inflation set to remain elevated, the gov't may prove wary of burdening businesses with further tax hikes that could push prices up further.

- With PM Sir Keir Starmer's centre-left Labour party trailing the right-wing populist Reform UK by double-digits in some opinion polling, the gov't finds itself in a difficult position. A recent report by the National Institute of Economic and Social Research outlined that “moderate but sustained” tax hikes would be required to eliminate a GBP41.2bln deficit and restore GBP10bln of fiscal headroom.

- With the tax burden as a percentage of GDP forecast to hit the highest level on record by 2027/28, it is unclear how the gov't will balance competing priorities, including public sector demands for higher wages, financial market concerns about the UK's fiscal trajectory and debt dynamics, and continued voter concerns about cost-of-living issues.

JAPAN: Ishiba Maintains Intention To Remain PM As LDP Critics Threaten Recall

The governing Liberal Democratic Party (LDP) has concluded a two-hour meeting of lawmakers from both houses of the National Diet. The formal reason for the assembly was to assess the fallout from the 20 July House of Councillors election, in which the LDP-Komeito governing coalition lost its majority in the upper chamber. However, the meeting was also a chance for LDP lawmakers to voice their displeasure with PM Shigeru Ishiba, whose critics blame for the party's poor performance.

- Ishiba apologised for the seat losses, but stated that he intends to remain as party president and prime minister. Opponents have called for his resignation. On 7 August, a group of conservative LDP lawmakers led by Councillor Shigeharu Aoyama presented Chief Cabinet Secretary Yoshimasa Hayashi with a letter formally calling for the PM to step down.

- Under LDP rules, there is no 'vote of no confidence' measure. Instead, a 'recall provision' exists. An early leadership election is called if half of sitting LDP lawmakers and half of the LDP's prefectural organisations formally submit a request. At present it appears this threshold has not been met.

- The latest polling shows former Minister of State for Economic Security Sanae Takaichi leading with 26% support, ahead of Minister of Agriculture, Forestry and Fisheries Shinjiro Koizumi on 22%. Ishiba, who would be allowed to run for the leadership again, trailed with just 8% support.

- Takaichi is seen as an advocate of the loose fiscal and monetary policy stance of the late Shinzo Abe, while Koizumi is viewed as closer to former PM Fumio Kishida, who also pursued increased gov't spending on defence and investment in industry via deficit spending.

FOREX: GBP Extends Post-BoE Strength; CAD Jobs Report the Data Highlight

- GBP has extended the spell of post-BoE decision strength. GBP/USD edged to a new recovery high overnight at 1.3453, signalling markets are still buying into the view that the split vote yesterday has restricted the room with which the BoE can cut rates later this year. For now, S/T momentum is still pointed higher, with the Jul 24 high of 1.3589 the next notable upside level.

- Canada's July jobs report is due Friday, and with markets expecting job gains to slow sharply to +10k from +83.1k previously, the unemployment rate is seen ticking moderately higher. Ahead of the print, USD/CAD is holding toward the lower-end of the weekly range, with yesterday's 1.3722 low and the 1.3692 50-dma the next notable downside levels.

- JPY is among the poorest performers on the day. Speculation continues to mount over the future of the LDP leadership. Speaking today, Ishiba noted he is not intending to change the cabinet lineup for now, but has vowed to stay on in his role despite party pressure to accelerate succession. Conviction in the weaker is low, however, with volumes holding below the average for this time of day.

- BoE's Pill and Fed's Musalem are the sole central bank speakers. Speculation remains over the possible make-up of the FOMC into 2026, with CEA head Miran set to step in for the remainder of Kugler's term, while reports earlier in the week suggested current FOMC member Waller was being pushed to take over from Powell next year. Any further reports or headlines here will be carefully watched by markets.

- Today also marks the supposed expiry of Trump's deadline by which Moscow must strike a ceasefire with Ukraine to avoid secondary tariffs. Presumably the week's developments and potential meeting with Putin as early as next week will prompt relief here, but further White House commentary on this topic will be carefully watched.

OPTIONS: Expiries for Aug08 NY cut 1000ET (Source DTCC)

- EUR/USD: $1.1500(E1.5bln), $1.1550(E614mln), $1.1600(1.1bln), $1.1650(E741mln), $1.1700(E1.3bln)

- USD/JPY: Y146.00($672mln), Y147.45-50($765mln)

- EUR/GBP: Gbp0.8675(E1.3bln), Gbp0.8700(E1.3bln)

- AUD/USD: $0.6500(A$4.4bln)

- USD/CAD: C$1.3750($851mln)

EQUITIES: Eurostoxx50 Futs Extending Bounce

- While the e-mini S&P faded into the Thursday close, the bulk of the bounce off the NFP low is holding firm, keeping the underlying uptrend intact for now. The index holds above support at the 20-day EMA, at 6336.50.

- The bounce off post-NFP lows in global equity indices persists, with the Eurostoxx 50 future recovering back above the 50-day EMA into the Thursday close.

COMMODITIES: WTI Futures Extend Spell of Weakness

- Gold continues to benefit from the soft NFP print on Friday and broad USD weakness across the week. This returns prices toward the top-end of the recent range and supports the view that short-term weakness is corrective.

- WTI futures trade poorly early Friday, having cracked the 50-day EMA and extended losses on the week. This keeps S/T momentum pointed lower. Support at the 50-day EMA has been cleared.

| Date | GMT/Local | Impact | Country | Event |

| 08/08/2025 | 1115/1215 | BOE Pill At National MPC Agency Briefing | ||

| 08/08/2025 | 1230/0830 | *** | Labour Force Survey | |

| 08/08/2025 | 1420/1020 | St. Louis Fed's Alberto Musalem | ||

| 08/08/2025 | 1700/1300 | ** | Baker Hughes Rig Count Overview - Weekly |