MNI US MARKETS ANALYSIS - Light Schedule Keeps Focus on Fed

Highlights:

- French political risk continues to pressure OAT-Bund spread, undermining EUR

- Light schedule should keep focus on speculation of Oval Office influence over the FOMC

- NVIDIA earnings after-market could prove market moving, with stock in range of all-time highs

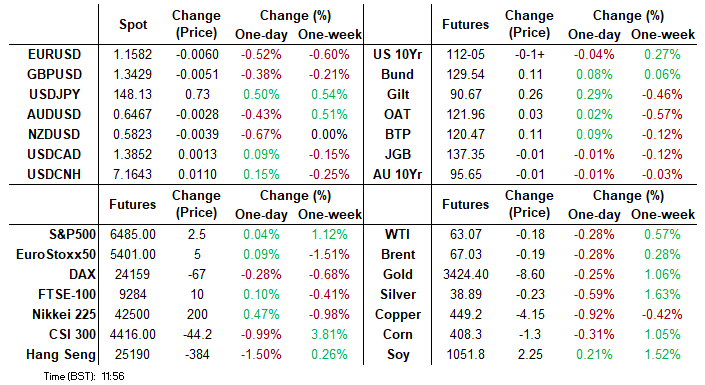

US TSYS: Steepening Consolidated, 5Y Auction Headlines A Light Docket

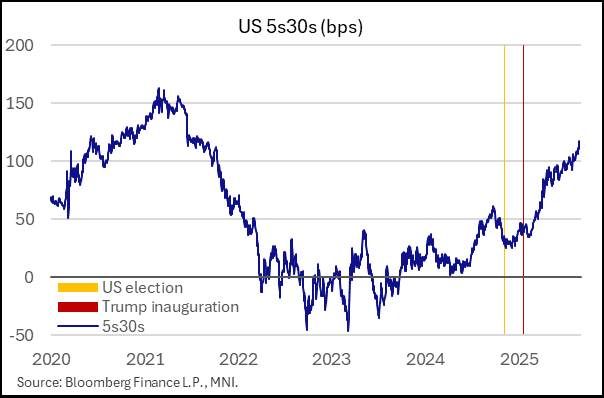

- Treasuries broadly consolidate yesterday’s steepening on challenges to Fed independence, which saw 5s30s at fresh highs since 2021.

- Today sees a light docket with focus on the 5Y auction. Yesterday’s 2Y was well-received, stopping through by 1.5bps and with the bid-to-cover rising to 2.69 from 2.62, whilst last month’s 5Y tailed by 1bp and the bid-to-cover fell to 2.31 from 2.36.

- Cash yields are 0.8bp higher (2s) to 0.1bp lower (30s) on the day.

- 2s10s at 61.1bps (+3.1bp) is mechanically steeper with yesterday’s new 2Y taking the benchmark. The earlier high of 62.0bp saw its steepest since Jul 16 (62.6bp, after PPI) and prior to that May.

- 5s30s at 117.6bp (-0.4bp) as it edges off yesterday’s fresh multi-year high of 118.1bps.

- TYZ5 trades at 112-05 (-02+), with the Z5 now the front month. Volumes are relatively subdued at 265k considering about half of this remains roll-related.

- Support is seen at 111-25 (20-day EMA) but the technical outlook remains bullish with resistance seen at the bull trigger of 112-15+ (Aug 5 high).

- Data: MBA mortgage applications (0700ET)

- Coupon issuance: US Tsy $28B 2Y FRN reopen - 91282CNQ0 (1130ET), $70B 5Y Note auction - 91282CNX5 (1300ET)

- Bill issuance: US Tsy $28B 17W bill auctions (1130ET)

- Politics: Nothing scheduled beyond regular in-town pool call time at 0900ET and Trump having lunch with VP Vance (1230ET)

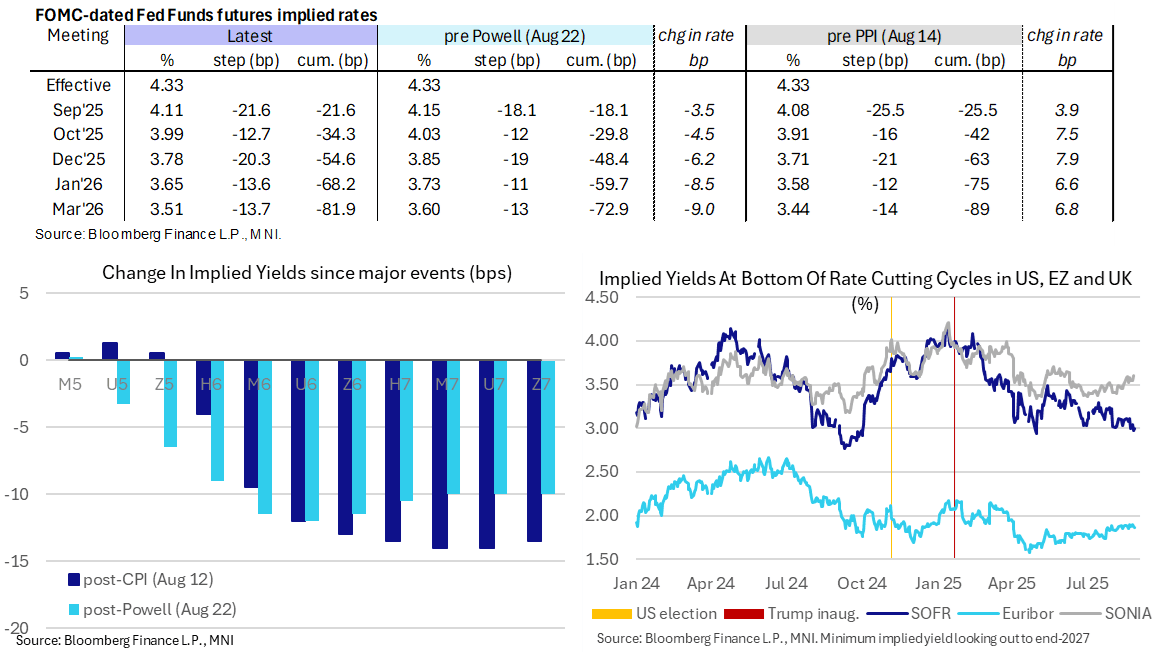

STIR: US Terminal Yields Hover Near Recent Lows On Fed Independence Fears

- Fed Funds implied rates hold most of yesterday’s decline attributed primarily to Fed independence concerns – see the 0551ET bullet for latest developments here.

- Cumulative cuts from 4.33% effective: 21.5bp Sep, 34.5bp Oct, 54.5bp Dec, 68bp Jan and 82bp Mar.

- SOFR implied yields are up to 2bp higher on the day in the reds, including the terminal yield of 2.995% for nearing 135bp of cuts from current levels.

- Yesterday’s close of 2.975% was a new lowest since late April having cleared the 3.01% on the Monday after the Aug 1 payrolls report.

- Further Trump-Fed headlines are likely to remain in the driving seat today with no major data releases or new Fed appearances scheduled. Data picks up Thu/Fri with Q2 GDP/Jul PCE reports.

FED: Latest Trump-Fed Deliberations

- Governor positions: Trump yesterday appeared to suggest in a cabinet meeting press conference that the administration could nominate Stephen Miran to "fired" Governor Cook's Board position (expiring in 2038), instead of ex-Gov Kugler's vacant spot (whose term ends in January before requiring renewal). Politico reports Miran’s nomination hearing is expected next week.

- Trump also made it clear he is looking to have a "majority" on the Fed Board "very shortly", with the aim to bring down interest rates.

- Two separate articles published in quick succession point to multiple angles being pursued by the Trump administration to exert more influence on the composition of the FOMC.

- The WSJ cited "people familiar with the matter" as saying President Trump wants to "move quickly to announce a nominee" to succeed Cook. One potential candidate is ex-World Bank President David Malpass.

- Regional Fed presidents: Echoing concerns by Brainard from earlier in the day, Bloomberg wrote that the Trump administration is "reviewing options for exerting more influence over the Federal Reserve's 12 regional banks that would potentially extend its reach beyond personnel appointments in Washington, according to people familiar with the matter." It’s ahead of the once-in-five-year exercise of authorizing reserve bank presidents in February.

- MNI Exclusive: With Miran’s growing likelihood at being placed in a longer-term Governor position, the MNI policy team’s latest interview with him from yesterday carries even more weight. See MNI INTERVIEW: US Growth, Jobs Poised For Rebound – Miran (1345ET) followed by Transcript of MNI Interview with CEA Chair Stephen Miran (1557ET)

- Fed Statement: A Federal Reserve statement yesterday indicated that the Fed's position is that Board Governors can only be removed "for cause", and that while Cook " has indicated through her personal attorney that she will promptly challenge this action in court and seek a judicial decision that would confirm her ability to continue to fulfill her responsibilities", the Fed will "abide by any court decision". “Long tenures and removal protections for governors serve as a vital safeguard”.

EUROPE ISSUANCE UPDATE

ESM Syndication: Spread Set

- USD2bln WNG of the new 5-year Sep-30 ESM-Bond.

Spread set at SOFR MS+39 (SA 30/360) (guidance was SOFR+40 Area, IPT was MS+42 area, that was equiv. to CT5 + ~7.3bp), books in excess of $10.2bn excl. JLM interest

EFSF Syndication: RfP Sent

- "Today, EFSF, the European Financial Stability Facility, rated Aaa (Moody's) / AA- (Fitch) / AA- (S&P), has sent a Request for Proposal to a selection of

banks from the EFSF/ESM Market Group with regards to an upcoming transaction,

subject to market conditions." - The EFSF request for proposal means a transaction early next week is likely.

- We saw a good chance of an EFSF September transaction in our daily supply note.

- On size, E3bln could be expected (which would complete the EFSF's funding needs for 2025). There is a chance of a smaller E2bln transaction with a further E1bn sold later this year, but that seems a less likely option to us.

German auction results

- E4bln (E2.675bln allotted) of the 2.50% Nov-32 Bund. Avg yield 2.46% (bid-to-offer 0.79x; bid-to-cover 1.19x).

FRANCE: Gov't Spox-Macron Did Not Discuss Dissolving Parl't During Cabinet Meet

Gov't spox Sophie Primas says that President Emmanuel Macron, in a recently-concluded meeting with the Council of Minsiters, did not discuss the option of dissolving parliament should the Bayrou gov't be defeated in a confidence motion. As MNI noted earlier, recent polling shows a clear majority of respondents in favour of snap legislative elections if PM Francois Bayrou's gov't is ousted on 8 September (see 'FRANCE: Poll-63% Back Dissolving National Assembly & Snap Elections', 08:36BST)

- Primas said there was "there was no [discussion] of a post-September 8 scenario", that Macron offered his "total support" to Bayrou's "approach" in seeking parliamentary approval for spending plans.

- Spox says the gov't will "continue to push forward all of our projects, very important issues that were coming up at the start of the [parliamentary calendar] We must take back the reins of our destiny, (...) this is a strong message to the financial markets,"

- The cabinet also confirmed that municipal elections will take place on 15 and 22 March 2026. In the event that the Bayrou gov't somehow avoids defeat/Macron can put together another gov't, these will be the next major set of nationwide elections to take place in France.

FRANCE: Poll-63% Back Dissolving National Assembly & Snap Elections

The latest polling from Ifop (carried out on 26 Aug, after PM Francois Bayrou's announcement of a confidence vote in his gov't) found a large majority of respondents in favour of the dissolution of the National Assembly and snap legislative elections. In total, 63% of respondents favoured dissolution, with 33% "absolutely" in favour. This represents an increase in overall support for dissolution from 41% in June and 50% in July.

- Unsurprisingly, those in favour of dissolution are largely supporters of opposition parties. Among far-right Rassemblement National (National Rally, RN) supporters, 86% are in favour of snap elections, as are 75% of those who vote for the far-left La France Insoumise (France Unbowed, LFI). Only 36% of supporters of President Emmanuel Macron's centrist Rennaissance support snap elections.

- In terms of whether respondents believe President Macron will dissolve the National Assembly 49% say they think he will, 51% believe he will not. The proportion of those that think the president will call snap elections has increased from 30% in June and 34% in July.

- Seventy-four per cent of respondents believe the defeat of Bayrou in the upcoming 8 Sep confidence vote would be a sign France is "ungovernable". A total of 68% believe if snap elections take place and once again there is no clear governable majority, Macron would have to resign as president, but only 50% believe that LFI leader Jean-Luc Melenchon was right to move to dismiss Macron.

- Data from Polymarket shows bettors assigning a 20% implied probability that fresh elections are called by 15 September, rising to 41% by year-end.

FOREX: EUR Softer as French, Dutch Political Risk Remains Key Driver

- Datapoints are few and far between Wednesday - and it's a similar case for both the central bank speaker schedule as well as Trump's official timetable, which may keep headline risk subdued throughout today. As a result, focus may remain on political machinations in Paris as the government look increasingly fragile. French bonds continue to trade sensitively and underperform broader European markets - highlighting the risks to the French economy (and thereby the EUR) from any decrease in fiscal credibility from the French government.

- While EURUSD weakness on Wednesday has primarily been driven by broader dollar dynamics, the French political situation will be adding weight. The latest polling from Ifop found a large majority of respondents in favour of the dissolution of the National Assembly and snap legislative elections. In total, 63% of respondents favoured dissolution. Data from Polymarket shows bettors assigning a 20% implied probability that fresh elections are called by 15 September, rising to 41% by year-end.

- Accordingly, the wider French-German 10y yield spread remains a solid proxy for European political risk, and is worth monitoring for intraday inflection points in the single currency.

- The USD Index is firmer within the recent range. Should prices close at current or higher levels today, it could mark the beginning of an upside correction, marking a break above the downtrendline drawn off the early August highs on the 15min candle chart.

- NZD is worse-off against all others in G10. NZD/USD is back below the 200-dma of 0.5832, but it's the 0.5800 that should provide firmer support on any further phases of weakness. Clearance here puts prices at the lowest since April, and another spell of soft equities could trigger a test. NVIDIA earnings are due after-market, and could have a sizeable impact on headline indices.

FOREX: EURUSD Weakness Extending Below 50-Day EMA Support

- Although EURUSD weakness on Wednesday has primarily been driven by broader dollar dynamics, the French political situation will be adding weight. The latest polling from Ifop found a large majority of respondents in favour of the dissolution of the National Assembly and snap legislative elections. In total, 63% of respondents favoured dissolution. Data from Polymarket shows bettors assigning a 20% implied probability that fresh elections are called by 15 September, rising to 41% by year-end.

- Latest price action has seen EURUSD extend below its 50-day EMA at 1.1600, with momentum building below last week’s lows of 1.1583 as short-term positions post-Powell are pressured. Noted pressure on European equities will be providing an additional Euro headwind.

- A clear break and close below the average would signal scope for a deeper retracement towards 1.1528 (Aug 05 low) initially, and potentially setup a move to key medium-term support at 1.1392, the Aug 1 low.

- Although moves for the likes of EURGBP and EURJPY have been more moderate, moves below the Aug 14 lows at 0.8597 and 170.97 would provide bearish impetus. For EURJPY, key support to watch lies at the 50-day EMA at 170.56, an average spot has not traded below since May 27.

OPTIONS: Expiries for Aug27 NY cut 1000ET (Source DTCC)

- EUR/USD: $1.1550-60(E1.8bln), $1.1620-30(E1.5bln), $1.1650(E2.1bln), $1.1665(E954mln), $1.1700-10(E1.5bln), $1.1750(E1.3bln), $1.1800(E2.0bln)

- USD/JPY: Y147.00($633mln), Y147.20-25($910mln), Y147.40-50($805mln), Y147.90-05($3.2bln)

- GBP/USD: $1.3350-60(Gbp1.8bln), $1.3484-85(Gbp672mln), $1.3515-25(Gbp903mln), $1.3570-75(Gbp1.1bln)

- AUD/USD: $0.6515-25(A$1.3bln), C$1.3915-25($840mln)

- USD/CAD: C$1.3680-90($1.2bln)

- USD/CNY: Cny7.1669($766mln)

EQUITIES: Dominant Uptrend in E-Mini S&P Intact, Contract Close to Recent Highs

- The trend set-up in Eurostoxx 50 futures is bullish and the pullback from the Aug 22 high is for now, considered corrective. Support to watch lies at 5374.47, the 50-day EMA. A clear break of this average would strengthen a short-term bearish threat and signal scope for a deeper retracement towards 5166.00, the Aug 1 low and a key support. Resistance to watch is 5522.00, the Aug 22 high. Clearance of this hurdle would resume the uptrend.

- The dominant uptrend in S&P E-Minis remains intact and the contract is trading at its recent highs. Moving average studies are in a bull-mode position, highlighting a clear uptrend and positive market sentiment. Attention is on 6508.75, the Aug 15 high and the bull trigger. Clearance of this level would confirm a resumption of the uptrend and open 6523.63, a Fibonacci projection. Support to watch lies at 6311.73, the 50-day EMA.

COMMODITIES: Medium-Term Trend Condition for Gold Remains Bullish

- A bear cycle in WTI futures remains intact and the latest round of short-term gains appear corrective - for now. A key support at $61.99, the Jun 30 low, has recently been breached, strengthening a bearish theme. A continuation lower would open $57.71, the May 30 low. Key short-term resistance has been defined at $69.36, the Jul 30 high. Clearance of this level would cancel a bear theme. Initial resistance to watch is $66.56, the Aug 4 high.

- Gold traded higher Tuesday. The medium-term trend condition remains bullish - MA studies are in a bull-mode position highlighting a dominant uptrend. The sideways direction that has been in place since the Apr peak appears to be a pause in the uptrend. A stronger resumption of gains would open $3439.0, the Aug 23 high. Key resistance and the bull trigger is at $3500.1, the Apr 22 low. First key support to watch is $3268.2, the Jul 30 low.

| Date | GMT/Local | Impact | Country | Event |

| 27/08/2025 | 1100/0700 | ** | MBA Weekly Applications Index | |

| 27/08/2025 | 1430/1030 | ** | DOE Weekly Crude Oil Stocks | |

| 27/08/2025 | 1430/1030 | ** | US DOE Petroleum Supply | |

| 27/08/2025 | 1530/1130 | ** | US Treasury Auction Result for 2 Year Floating Rate Note | |

| 27/08/2025 | 1700/1300 | * | US Treasury Auction Result for 5 Year Note | |

| 28/08/2025 | 0130/1130 | * | Private New Capex and Expected Expenditure | |

| 28/08/2025 | 0700/0900 | ** | Economic Tendency Indicator | |

| 28/08/2025 | 0700/0900 | *** | GDP | |

| 28/08/2025 | 0700/0900 | ** | KOF Economic Barometer | |

| 28/08/2025 | 0800/1000 | ** | M3 | |

| 28/08/2025 | 0800/1000 | ** | ISTAT Consumer Confidence | |

| 28/08/2025 | 0800/1000 | ** | ISTAT Business Confidence | |

| 28/08/2025 | 0900/1100 | * | Consumer Confidence, Industrial Sentiment | |

| 28/08/2025 | 1230/0830 | *** | Jobless Claims | |

| 28/08/2025 | 1230/0830 | ** | WASDE Weekly Import/Export | |

| 28/08/2025 | 1230/0830 | * | Current account | |

| 28/08/2025 | 1230/0830 | * | Payroll employment | |

| 28/08/2025 | 1230/0830 | *** | GDP / PCE Quarterly | |

| 28/08/2025 | 1400/1000 | ** | NAR Pending Home Sales | |

| 28/08/2025 | 1430/1030 | ** | Natural Gas Stocks | |

| 28/08/2025 | 1500/1100 | ** | Kansas City Fed Manufacturing Index | |

| 28/08/2025 | 1530/1130 | ** | US Bill 04 Week Treasury Auction Result | |

| 28/08/2025 | 1530/1130 | * | US Bill 08 Week Treasury Auction Result | |

| 28/08/2025 | 1700/1300 | ** | US Treasury Auction Result for 7 Year Note | |

| 28/08/2025 | 2200/1800 | Fed Governor Christopher Waller |