MNI US MARKETS ANALYSIS - JPY Weakness Exceeding Expectations

Highlights:

- JPY slippage extends, exceeding sell-side estimates

- French politics sees dose of optimism, Lecornu set to speak later today

- Shutdown continues, Fed minutes in focus

US TSYS: Lagging EGB Gains, 10Y Supply and FOMC Minutes Headline Docket

- Treasuries have extended yesterday’s gains, underperforming a stronger rally in EGBs on cautious political optimism with Italy and France leading gains.

- Today’s US docket is likely headlined by 10Y supply after a strong auction last month (yields are currently almost 7bps higher than last month’s high yield) as well as the FOMC minutes.

- Any sign of government shutdown progress will also be watched with Polymarket currently showing 74% chance of it ending Oct 15 or later.

- Cash yields are 0.2bp (2s) to 2.4bp (30s) lower on the day.

- The bull flattening sees 2s10s at 54.4b (-1.7bp), off yesterday’s almost month-long high of 58.2bp for back more firmly within recent ranges.

- TYZ5 trades at 112-25 (+03+) just off an earlier high of 112-25+, clearing yesterday’s 112-24 as it moves a little closer to resistance at 113-00 (Sep 24 high). Volumes are again very subdued at just 180k.

- Prior weakness was considered corrective, having yesterday probed support at 112-12+ (50-day EMA), with the trend structure remaining bullish.

- Data: Weekly MBA mortgage data (0700ET), Federal budget balance Sep (1400ET)

- Fedspeak: FOMC minutes (1400ET) plus Musalem (0920ET), Barr (0930ET), Goolsbee (1000ET & 1915ET), Kashkari (1515ET & 1630ET), Barr (1745ET) – see STIR bullet

- Coupon issuance: US Tsy $39B 10Y Note auction re-open - 91282CNT4 (1300ET). Last month’s auction was strong as it stopped through by 1.4bps and saw bid-to-cover rise from 2.35 to 2.65.

- Bill issuance: US Tsy $69B 17W bill auction (1130ET)

- Politics: Trump participates in roundtable on ANTIFA (1500ET)

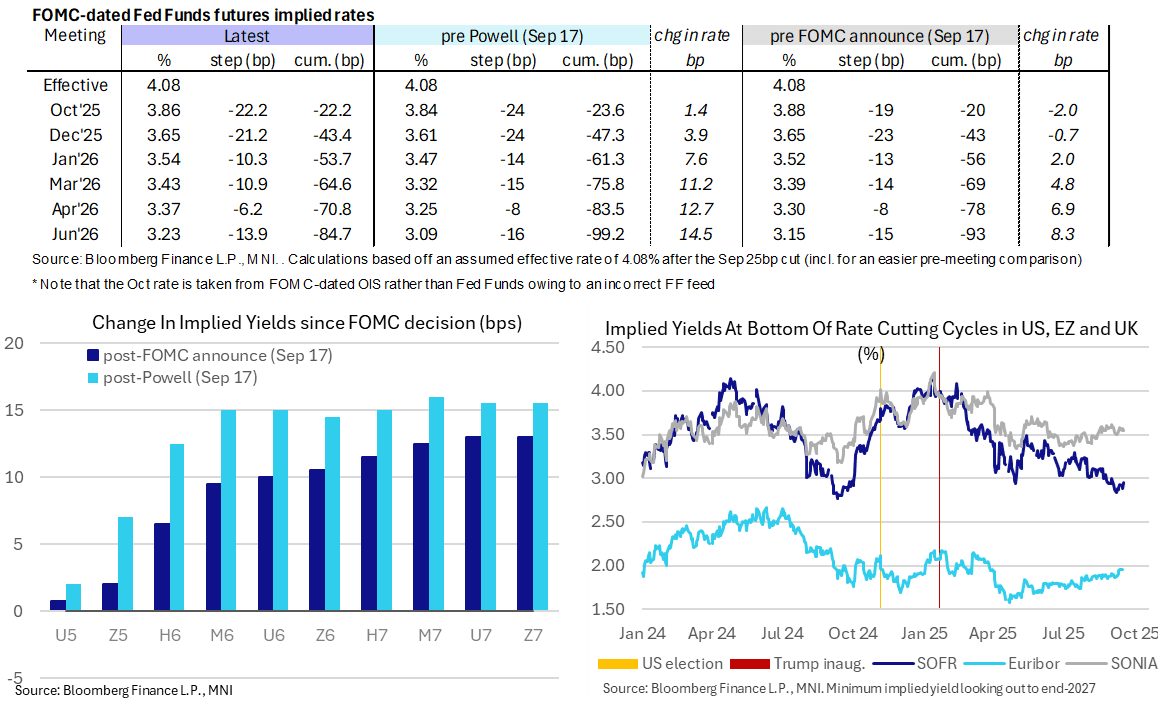

STIR: Fed Rates Little Changed, FOMC Minutes Likely More Notable Than Fedspeak

- Fed Funds implied rates are 0.5bp higher overnight for most near-term meetings, holding within yesterday’s range.

- Cumulative cuts from 4.08% effective: 22bp Oct, 43.5bp Dec, 53.5bp Jan, 64.5bp Mar, 71bp Apr and 85bp June.

- SOFR futures also see small moves on the day: H6 with marginal losses (-0.005) otherwise small gains beyond including +0.015 through blues and yellows.

- The SOFR implied terminal yield of 3.045% (SFRH7, -0.5bp) is also within recent ranges, eyeing a little more than 100bp of cuts ahead.

- Today’s Fedspeak focus should be on the FOMC Minutes from the Sept 16-17 meeting. Last month’s meeting revealed a lack of conviction on the FOMC about the rate path forward in both the SEP and then Chair Powell’s press conference.

- The median voter marked down their end-2025 rate 25bps to 3.5-3.75% (i.e. two further cuts in addition to the 25bp cut last month) but 2 members look for 1 cut and 6 members don’t expect another cut this year (and 1 would have preferred not to have cut at all last month).

- Other scheduled Fedspeak looks unlikely to materially add to monetary policy discussions. Nevertheless, for completeness:

- 0920ET – Musalem (’25 voter, hawk) welcoming remarks at community banking research conference

- 0930ET – Gov. Barr (voter) keynote at community banking research conference (text only)

- 1000ET – Goolsbee (’25) opening remarks at Chicago Payments Symposium

- 1515ET – Kashkari (’26) speaks at Center for Indian Country Development

- 1630ET – Kashkari (’26) hosts fireside chat with Senator Tina Smith

- 1745ET – Gov. Barr (voter) speaks on community development

- 1915ET – Goolsbee (’25) speaks at payments conference (text only)

UK FISCAL: Error in fiscal data benefits government; but another ONS data issue

- Note that correction in the data means that the tracking versus the OBR numbers YTD will only be GBP9.4bln (rather than the GBP11.4bln estimated when the data was released on 19 September). And it means that VAT is now tracking GBP1.5bln below the OBR's target versus GBP3.5bln below target in that release.

- This is of course good news for the government and will be fully incorporated in the next monthly release on 21 October (which will be the last release the OBR will incorporate into its forecasts for the Budget).

- But it is yet another error at the ONS - albeit this one was due to HMRC data that was sent to the ONS. An HMRC calculation error was also behind the VED issue that caused a correction to PPI recently.

- But this now means that we have had issues with PPI (which is due to begin publishing again soon), retail sales, GDP (from those two releases), CPI, public finance data and trade data over the past few months. This is on top of the quality issues with the LFS survey and the delays in launching the TLFS.

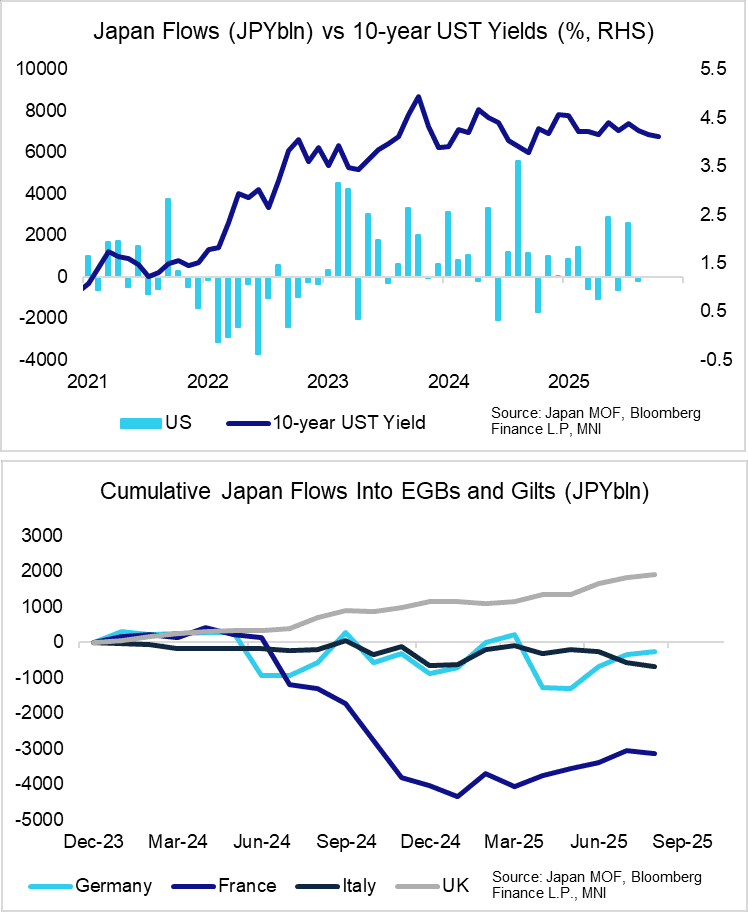

BONDS: Japanese Investors Net Sold OATs and BTPs In August

Japanese investors were net sellers of French and Italian bonds in August, according to balance of payments data released overnight. While there is no detail on the timing of flows in the data, it’s reasonable to assume that ex-French PM Bayrou’s no-confidence vote announcement on August 25th prompted a degree of selling in French paper.

- Investors net sold JPY67.7bln of French bonds in August, the first month of net sales since March. Year-to-date, net purchases have still totalled JPY917bln, but net flows since Macron’s snap legislative election announcement in Q2 2024 remain clearly negative.

- Investors sold JPY123bln if Italian bonds in August, the third consecutive month of net sales.

- Net purchases of German and UK bonds remained positive in Augst.

- Investors net sold JPY214bln of US Treasuries, but this followed a sizeable JPY2.59trln net inflow in July.

SOFR: Net Long Setting Dominated In Futures On Tuesday

OI data suggests that net long setting dominated in SOFR futures as contracts ticked higher on Tuesday. Only a couple of instances of net short cover were seen through the blues.

| 07-Oct-25 | 06-Oct-25 | Daily OI Change |

| Daily OI Change In Packs |

SFRU5 | 1,413,666 | 1,411,259 | +2,407 | Whites | +78,703 |

SFRZ5 | 1,510,843 | 1,481,053 | +29,790 | Reds | +38,972 |

SFRH6 | 1,200,513 | 1,161,483 | +39,030 | Greens | +9,276 |

SFRM6 | 1,031,353 | 1,023,877 | +7,476 | Blues | +11,217 |

SFRU6 | 998,775 | 989,448 | +9,327 |

|

|

SFRZ6 | 1,030,970 | 1,015,526 | +15,444 |

|

|

SFRH7 | 795,046 | 787,606 | +7,440 |

|

|

SFRM7 | 796,100 | 789,339 | +6,761 |

|

|

SFRU7 | 676,917 | 682,142 | -5,225 |

|

|

SFRZ7 | 748,863 | 744,503 | +4,360 |

|

|

SFRH8 | 431,018 | 429,083 | +1,935 |

|

|

SFRM8 | 365,049 | 356,843 | +8,206 |

|

|

SFRU8 | 298,173 | 299,116 | -943 |

|

|

SFRZ8 | 327,104 | 317,464 | +9,640 |

|

|

SFRH9 | 192,299 | 190,093 | +2,206 |

|

|

SFRM9 | 166,817 | 166,503 | +314 |

|

|

US TSY FUTURES: Mix Of Long Setting & Short Cover Seen Tuesday

OI data points to a mix of net long setting (TU, FV & WN) and short cover (TY, UXY & US) as Tsy futures ticked higher on Tuesday.

- The most meaningful positioning swing came via the short cover seen in TY futures (~$2.4mln DV01), with the curve-wide net bias also tilted towards net short cover.

| 07-Oct-25 | 06-Oct-25 | Daily OI Change | OI DV01 Equivalent Change ($) |

TU | 4,617,546 | 4,590,741 | +26,805 | +1,053,344 |

FV | 6,721,536 | 6,714,305 | +7,231 | +316,306 |

TY | 5,393,967 | 5,429,056 | -35,089 | -2,363,707 |

UXY | 2,460,836 | 2,462,153 | -1,317 | -119,098 |

US | 1,881,110 | 1,887,029 | -5,919 | -841,244 |

WN | 2,054,464 | 2,052,350 | +2,114 | +395,110 |

|

| Total | -6,175 | -1,559,289 |

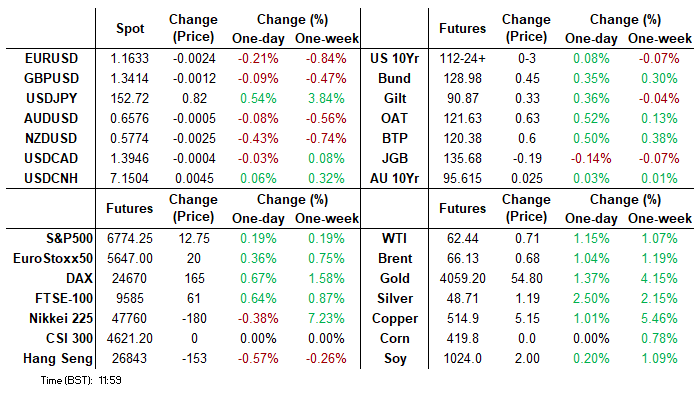

FOREX: JPY Slippage Extends, USD Rally Contained by Lower Long-End

- The greenback is higher against all others in G10 headed through to the NY crossover, however the further fade for the US 10y yield across the European morning has contained further strength. The RBNZ 50bps rate cut, further political uncertainty in Japan & France, and a tax collection revision in the UK have been the primary market drivers.

- NZDUSD hit the lowest levels since April and is eyeing a test of next support at 0.5728, the 61.8% retracement of the April/July range as the RBNZ stated “the Committee remains open to further reductions in the OCR” following their outsized cut to prop up the lacklustre domestic economy.

- Meanwhile, JPY weakness continues to run further than market expectations, boosting USDJPY for a fifth consecutive session to hit 152.89. Market moves follow the softer real wages data - which endorse Takaichi's preference for slower rate hikes, however government formation is still the active driver as coalition talks with Komeito continue, delaying the reconvening of the Diet. For USDJPY, this week’s gains reinforce current bullish trend conditions, with technical breaches paving the way for an extension towards 154.39, a Fibonacci retracement point. Initial support to watch lies at 150.92, the Aug 1 high.

- EURGBP meanwhile is edging to new daily lows, despite the tightening of the French-German bond yield spread and seeming optimism of PM Lecornu that a budget agreement can be reached in the near-term. This has pressed through the 50-dma of 0.8676, which had successfully provided intraday support on three occasions over the past month, putting attention on 0.8597, the Aug 14 low. The break lower here stems from the reduction in UK borrowing estimates following ONS VAT revisions this morning - adding to the view that the worst may be behind us for the longer-end of the UK Gilt market headed into November's Budget.

- Focus turns to the Fed meeting minutes, which should shed light on the FOMC's pre-shutdown thoughts on the US economy and policy into year-end. Speakers still due include ECB's Elderson, BoE's Pill and Fed's Musalem, Barr, Goolsbee & Kashkari.

EURGBP: Fading EURGBP Challenges Consensus View

EURGBP is edging to new daily lows, despite the tightening of the French-German bond yield spread and seeming optimism of PM Lecornu that a budget agreement can be reached in the near-term. This has pressed through the 50-dma of 0.8676, which had successfully provided intraday support on three occasions over the past month.

- The break lower here stems from the reduction in UK borrowing estimates following ONS VAT revisions this morning - adding to the view that the worst may be behind us for the longer-end of the UK Gilt market headed into November's Budget.

- The fade in EURGBP runs counter to the consensus view for further upside in the cross. Despite falling expectations for BoE easing for the rest of this year, most had seen EURGBP as the better expression for fiscal-tripped GBP weakness given US uncertainty and Fed easing, raising focus on any correction toward mid-Sept lows of 0.8633 and 0.8562, the 50% retracement for the May-Jul upleg.

- Meanwhile, EURUSD remains lower, but is comfortably off the daily lows headed into the NY crossover. French politics has aided the moderate bounce in spot, but it's the fade through yesterday's lows in US 10y yield that's the primary driver here - and has contained the mid-week USD rally.

OPTIONS: Expiries for Oct08 NY cut 1000ET (Source DTCC)

- EUR/USD: $1.1650(E698mln), $1.1700(E1.1bln), $1.1770-80(E1.2bln), $1.1800(E1.5bln), $1.1850-60(E1.0bln)

- USD/JPY: Y146.50($1.2bln), Y147.00($1.5bln), Y149.00($980mln), Y150.00($562mln), Y151.00($799mln)

EQUITIES: E-Mini Trend Condition Unchanged, Direction Remains Upward

- Eurostoxx 50 futures remain in a bull-mode condition. Last week’s gains resulted in a breach of key resistance at 5525.00, the Aug 22 high. The break confirms a resumption of the uptrend. The impulsive climb opens the 5700.00 handle next, with potential for a test of 5727.18 further out, a Fibonacci projection. Moving average studies are in a bull-mode position too, highlighting a dominant uptrend. Initial firm support is 5525.00, Aug 22 high.

- The trend condition in S&P E-Minis is unchanged and the direction remains up. Recent fresh cycle highs confirm a continuation of the uptrend and maintain the positive price sequence of higher highs and higher lows. Sights are on 6812.29, a Fibonacci projection. Initial support to watch is at the 20-day EMA, at 6700.59. It has recently been pierced, a clear break of it would signal scope for a deeper pullback.

COMMODITIES: Correction Off Recent Lows for WTI Futures Considered Corrective

- WTI futures have recovered from the most recent low print - a correction. A bearish theme remains intact. Last week’s sell-off resulted in a move through key support and the bear trigger at $60.85, the Aug 13 low. Clearance of this level strengthens the bear threat and paves the way for an extension towards $57.50, the May 30 low. Initial firm resistance has been defined at $66.42, the Sep 29 high. Clearance of this level would highlight a reversal.

- A bull cycle in Gold remains in play and this week’s breach of $40000.0 reinforces the uptrend. The move higher maintains the price sequence of higher highs and higher lows. Furthermore, momentum studies highlight a condition known as momentum drag - where momentum remains in overbought territory and moves sideways - a bullish signal. Sights are on $4074.54, a Fibonacci projection. Support to watch is $3775.3, 20-day EMA.

| Date | GMT/Local | Impact | Country | Event |

| 08/10/2025 | 1100/0700 | ** | MBA Weekly Applications Index | |

| 08/10/2025 | 1320/0920 | St. Louis Fed's Alberto Musalem | ||

| 08/10/2025 | 1330/0930 | Fed Governor Michael Barr | ||

| 08/10/2025 | 1430/1030 | ** | DOE Weekly Crude Oil Stocks | |

| 08/10/2025 | 1430/1030 | ** | US DOE Petroleum Supply | |

| 08/10/2025 | 1500/1600 | BOE Pill Speech at University of Birmingham | ||

| 08/10/2025 | 1600/1800 | ECB Lagarde Video Message at Werner Report Event | ||

| 08/10/2025 | 1700/1300 | ** | US Note 10 Year Treasury Auction Result | |

| 08/10/2025 | 1800/1400 | *** | FOMC Minutes | |

| 08/10/2025 | 1915/1515 | Minneapolis Fed's Neel Kashkari | ||

| 08/10/2025 | 2145/1745 | Fed Governor Michael Barr | ||

| 09/10/2025 | 0600/0800 | ** | Trade Balance | |

| 09/10/2025 | 0830/0930 | BOE Mann Keynote at Resolution Foundation Event | ||

| 09/10/2025 | 1145/0745 | BOC Sr Deputy Gov Rogers speaks in Toronto (time TBC) | ||

| 09/10/2025 | - | ECB Lagarde & Cipollone at Eurogroup Meeting | ||

| 09/10/2025 | 1230/0830 | *** | Jobless Claims | |

| 09/10/2025 | 1230/0830 | ** | WASDE Weekly Import/Export | |

| 09/10/2025 | 1230/0830 | Fed Chair Jerome Powell | ||

| 09/10/2025 | 1235/0835 | Fed's Miki Bowman | ||

| 09/10/2025 | 1245/0845 | Fed's Miki Bowman | ||

| 09/10/2025 | 1400/1000 | ** | Wholesale Trade | |

| 09/10/2025 | 1400/1000 | ** | Wholesale Trade | |

| 09/10/2025 | 1430/1030 | ** | Natural Gas Stocks | |

| 09/10/2025 | 1500/1700 | ECB Lane Round Table at Irish Investment Managers Event | ||

| 09/10/2025 | 1530/1130 | ** | US Bill 04 Week Treasury Auction Result | |

| 09/10/2025 | 1530/1130 | * | US Bill 08 Week Treasury Auction Result | |

| 09/10/2025 | 1600/1200 | *** | USDA Crop Estimates - WASDE | |

| 09/10/2025 | 1645/1245 | Fed Governor Michael Barr | ||

| 09/10/2025 | 1700/1300 | Minneapolis Fed's Neel Kashkari | ||

| 09/10/2025 | 1700/1300 | *** | US Treasury Auction Result for 30 Year Bond | |

| 09/10/2025 | 1945/1545 | Fed's Miki Bowman |