US TSYS: Lagging EGB Gains, 10Y Supply and FOMC Minutes Headline Docket

Oct-08 10:50

- Treasuries have extended yesterday’s gains, underperforming a stronger rally in EGBs on cautious political optimism with Italy and France leading gains.

- Today’s US docket is likely headlined by 10Y supply after a strong auction last month (yields are currently almost 7bps higher than last month’s high yield) as well as the FOMC minutes.

- Any sign of government shutdown progress will also be watched with Polymarket currently showing 74% chance of it ending Oct 15 or later.

- Cash yields are 0.2bp (2s) to 2.4bp (30s) lower on the day.

- The bull flattening sees 2s10s at 54.4b (-1.7bp), off yesterday’s almost month-long high of 58.2bp for back more firmly within recent ranges.

- TYZ5 trades at 112-25 (+03+) just off an earlier high of 112-25+, clearing yesterday’s 112-24 as it moves a little closer to resistance at 113-00 (Sep 24 high). Volumes are again very subdued at just 180k.

- Prior weakness was considered corrective, having yesterday probed support at 112-12+ (50-day EMA), with the trend structure remaining bullish.

- Data: Weekly MBA mortgage data (0700ET), Federal budget balance Sep (1400ET)

- Fedspeak: FOMC minutes (1400ET) plus Musalem (0920ET), Barr (0930ET), Goolsbee (1000ET & 1915ET), Kashkari (1515ET & 1630ET), Barr (1745ET) – see STIR bullet

- Coupon issuance: US Tsy $39B 10Y Note auction re-open - 91282CNT4 (1300ET). Last month’s auction was strong as it stopped through by 1.4bps and saw bid-to-cover rise from 2.35 to 2.65.

- Bill issuance: US Tsy $69B 17W bill auction (1130ET)

- Politics: Trump participates in roundtable on ANTIFA (1500ET)

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

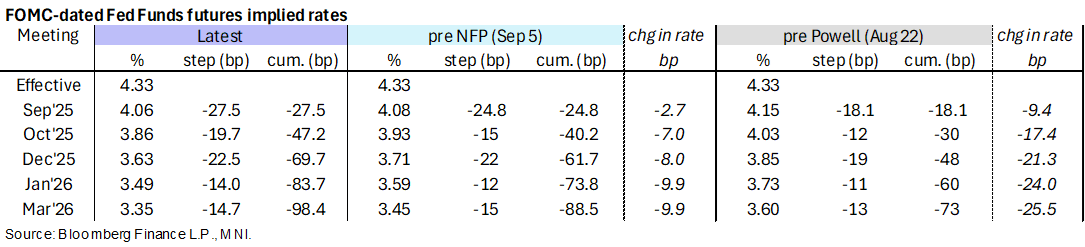

STIR: Payrolls Rally Broadly Consolidated With Tue-Thu Data Eyed

Sep-08 10:43

- Fed Funds implied rates are little changed since Friday’s close, holding what was only a modest paring of the rally on a soft payrolls report at the time.

- It sees close to three consecutive cuts priced to year-end, with only limited odds of a 50bp cut next week (~10%).

- Cumulative cuts from 4.33% effective: 27.5bp Sep, 47bp Oct, 69.5bp Dec, 83.5bp Jan and 98.5bp Mar.

- The SOFR implied terminal yield of 2.86% (SFRH7) is 1bp lower from Friday as it sits a little off 150bp of cuts ahead from current levels. The yield is only 2.5bp lower than levels just prior to the NFP release after rates rallied into the release.

- It’s a quieter start to the week before preliminary payrolls benchmark revisions, PPI and CPI over Tue-Thu. The Fed is now in media blackout ahead of the FOMC meeting on Sep 16-17.

LOOK AHEAD: Monday Data Calendar: NY Fed Inflation Exp, Consumer Credit

Sep-08 10:41

- US Data/Speaker Calendar (prior, estimate)

- 09/08 1100 NY Fed 1-Yr Inflation Expectations (3.09%, --)

- 09/08 1130 US Tsy $82B 13W & $73B 26W bill auctions

- 09/08 1500 Consumer Credit $7.371B, $10.2B)

- Source: Bloomberg Finance L.P. / MNI

FRANCE: Result of No-confidence Vote Not Expected Till 1900CET At The Earliest

Sep-08 10:40

Local and political media outlets report that the result of the French no-confidence vote is not expected to be known until 1900CET (1800BST) at the earliest.

- PM Bayrou in theory has an unlimited amount of time to deliver his general policy address at 1400BST/1500CET.

- Following this address, speakers from each parliamentary group (eleven in total) will provide remarks. Speaking times depend on the number of seats each group holds in the National Assembly. From Le Figaro:

- Ensenble Group: 35 mins

- RN, DR and MODEM (Bayrou's party): 15 mins

- Other groups (fewer than 35 deputies): 10 mins:

- Speaker for non-registered deputies: 5 mins

- Following these speeches, Bayrou will then be able to speak again before votes begin.

- Le Parisien highlights that "The debates surrounding his previous general policy statement, on January 14, lasted approximately five hours, without a vote"