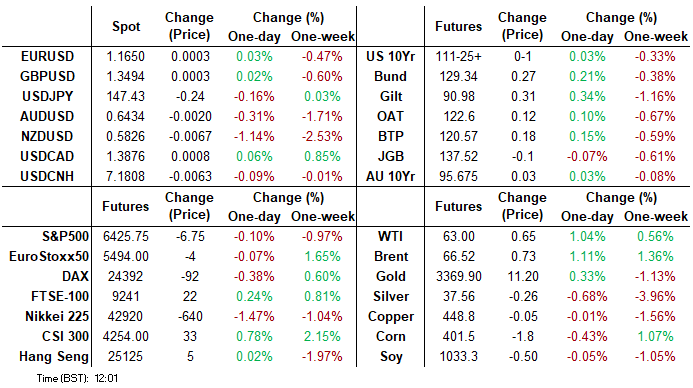

MNI US MARKETS ANALYSIS - GBP/NZD Nears 10y High on CPI, RBNZ

Highlights:

- NZD slips as RBNZ opt for dovish rates track

- UK CPI tops expectations, but implications for BoE policy may be limited

- Fed minutes eyed for any suggestions others could have joined Bowman, Waller in dissenting

US TSYS: Bull Flatter In Thin Trading, 20Y Auction & FOMC Minutes Ahead

- Treasuries have firmed since ~0400ET with little by way of meaningful headlines, more than reversing weakness in Asia hours to leave them bull flatter on the day.

- Cash yields are 0-2bp lower on the day, fading the 4-5bp declines in UK yields (the hawkish impact from firmer CPI was short-lived) but with Treasuries exhibiting a slightly more pronounced flattening.

- It sees 5s30s at 107.5bps vs recent ytd steeps of ~109.5bps.

- TYU5 trades at 111-26 (+01+) on particularly thin cumulative volumes approaching 190k.

- Monday’s low of 11-13+ came close to support at 111-11 (50-day EMA) but the outlook remains bullish with resistance seen at a bull trigger of 112-15+ (Aug 5 high).

- The flattening suggests little concern about today’s 20y auction. Last month’s sale was solid, trading through by 1.5bps and with the bid-to-cover rising to 2.79 from 2.68 the month prior.

- Data: MBA mortgage applications (1200ET)

- Fedspeak: Waller (1100ET), FOMC Minutes (1400ET), Bostic (1500ET) – see STIR bullet

- Coupon issuance: US Tsy $16B 20Y Bond auction - 912810UN6 (1300ET)

- Bill issuance: US Tsy $65B 17W bill auction (1130ET)

- Politics: Trump participates in Swearing-In Ceremony for US Ambassador to EU (1600ET)

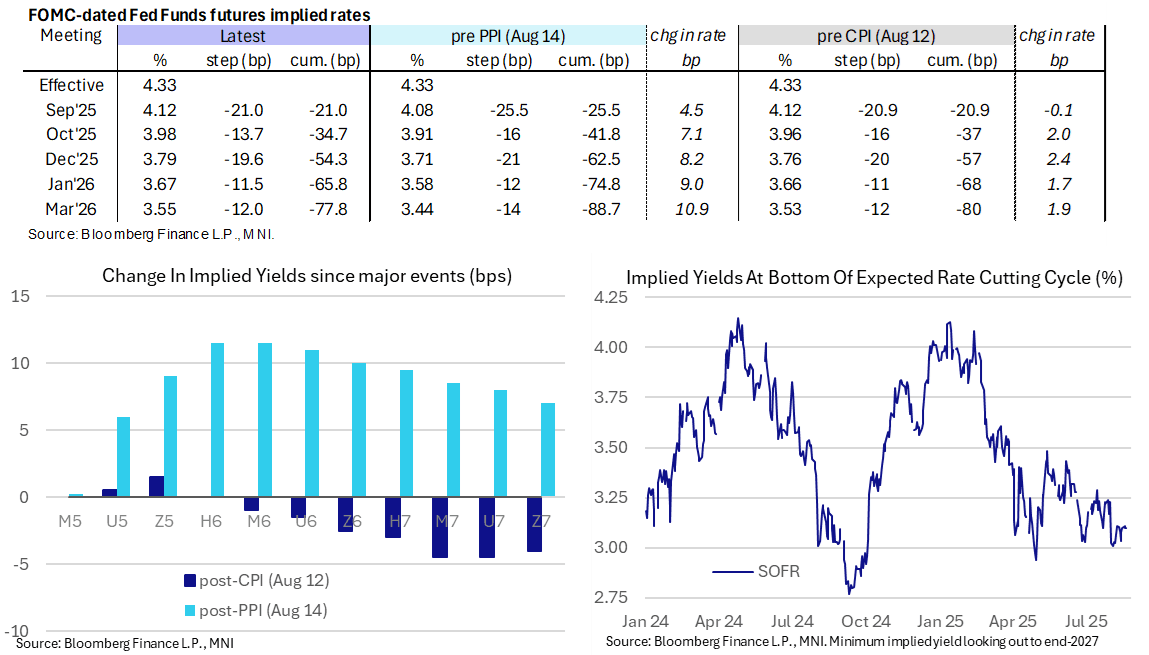

STIR: Fed Rates Treading Water, FOMC Minutes Later Today

- Fed Funds implied rates are little changed overnight as they keep to relatively narrow ranges seen so far this week.

- Whilst the FOMC minutes are released later today, the main data of the week comes tomorrow with jobless claims and flash PMIs before Powell’s Jackson Hole appearance on Friday.

- Cumulative cuts from 4.33% effective: 21bp Sep, 34.5bp Oct, 54.5bp Dec, 66bp Jan and 78bp Mar.

- The SOFR implied terminal yield of 3.10% (SFRH7, unch) also keeps to particularly narrow ranges, having closed the past three sessions between 3.10-3.11%. More broadly, it holds the +/-5bp of 125bp of cuts from current levels range seen since the Aug 1 payrolls report.

- Today’s Fedspeak:

- 1100ET – Fed Gov Waller (permanent voter, dove) speaks on payments at Blockchain Symposium (text + Q&A). If anything like Bowman’s appearance yesterday, expect a simple acknowledgement that his view remains the same (“the wait and see approach is overly cautious and, in my opinion, does not properly balance the risks to the outlook and could lead to policy falling behind the curve”) before moving onto areas that are less directly monetary policy relevant.

- 1400ET – FOMC minutes for the Jul 29-30 meeting, offering further color on the meeting that saw two dissenters with Bowman and Waller preferring to cut rates. This is firmly seen as secondary to Fed Chair Powell’s Jackson Hole speech at 1000ET on Friday.

- 1500ET – Bostic (non-voter) in conversation on economy (Q&A only). He said Aug 13 ““For the rest of this year, I still have one cut on my outlook… that also is predicated on the notion that labor markets stay solid. If they weaken considerably, that balance of risks starts to look differently and the appropriate path will look different as well.”

SOFR: Mix Of Long Setting & Short Cover In Futures On Tuesday

OI data points to a mix of net long setting and short cover as SOFR futures generally ticked higher on Tuesday. There wasn’t much in the way of meaningful positioning swings in individual contracts and wider packs.

| 19-Aug-25 | 18-Aug-25 | Daily OI Change |

| Daily OI Change In Packs |

SFRM5 | 1,198,843 | 1,199,163 | -320 | Whites | -14,744 |

SFRU5 | 1,284,078 | 1,287,739 | -3,661 | Reds | -3,009 |

SFRZ5 | 1,418,700 | 1,424,297 | -5,597 | Greens | +5,013 |

SFRH6 | 1,036,778 | 1,041,944 | -5,166 | Blues | -9,790 |

SFRM6 | 933,170 | 927,706 | +5,464 |

|

|

SFRU6 | 895,297 | 892,416 | +2,881 |

|

|

SFRZ6 | 996,855 | 1,005,589 | -8,734 |

|

|

SFRH7 | 736,485 | 739,105 | -2,620 |

|

|

SFRM7 | 904,136 | 907,303 | -3,167 |

|

|

SFRU7 | 590,855 | 590,453 | +402 |

|

|

SFRZ7 | 599,716 | 596,896 | +2,820 |

|

|

SFRH8 | 354,290 | 349,332 | +4,958 |

|

|

SFRM8 | 275,193 | 273,561 | +1,632 |

|

|

SFRU8 | 207,518 | 205,338 | +2,180 |

|

|

SFRZ8 | 218,526 | 231,675 | -13,149 |

|

|

SFRH9 | 150,758 | 151,211 | -453 |

|

|

ISRAEL: 60k To Be Called Up For Gaza City Op That Could Start Within Weeks

The Israeli gov't is reported to be reviewing the prospective ceasefire deal put forward by Qatar and Egypt and agreed to by Hamas on 18 August. Initially, PM Benjamin Netanyahu was reported to have been 'dismissive' towards the prospect of a truce being reached. The Times of Israel, though, claims that "Two Israeli officials said Tuesday that Jerusalem is studying the hostage-ceasefire proposal accepted by Hamas, and that Netanyahu is expected to convene discussions about it soon. A response is expected in the coming two days, said a Palestinian source close to the talks."

- The 'Witkoff proposal' on which the current deal is based envisages a 60-day ceasefire in exchange for the release of half of the remaining living hostages. During the period, talks on a permanent truce would get underway. Gov't figures have forcefully claimed that a ceasefire is only possible with the release of all hostages.

- The gov't has also overnight approved plans to call up tens of thousands of military reservists for the full military encirclement and occupation of Gaza City and central Gaza. Letters will be sent out soon to 60,000 reservists to be called up on 2 September, with another 20,000 having their service extended. An estimated 100k reservists are expected to be drafted during the operation.

- A full military takeover of the Gaza Strip would likely be a months-long operation. It is unclear whether, once started, the gov't will be willing to halt, even if a favourable ceasefire deal is presented, given Netanyahu's stated intention to eliminate Hamas.

RUSSIA: TURKEY-Putin Holds Call Erdogan To Discuss Ukraine & Trump Meeting

Russian state media has confirmed a call between President Vladimir Putin and his Turkish counterpart, Recep Tayyip Erdogan. Tass reports that the two discussed Putin's meeting with US President Donald Trump, Turkey's role in previous Russia-Ukraine talks, and bilateral trade and investment. There has been speculation that it is one of the potential options for a prospective meeting between Putin and Ukrainian President Volodymyr Zelenskyy. However, Turkey's position as a member of the 'coalition of the willing' may complicate any such plans. Russia may view Turkey as too close to the Ukrainian 'camp', especially if it volunteers peacekeepers or air/sea patrols as part of a peace deal.

- As Politico reports, "Turkey — with its large army and Black Sea experience — could play a key role. But it's also politically messy — with Greece and Cyprus leery of allowing Ankara to access any EU funds for its military. "It’s too early to contemplate such a development,” Selim Yenel, a former Turkish ambassador to the EU, told POLITICO. And Ankara, he warned, would demand something in return. “As for the quid pro quo, it would still be difficult to overcome the EU’s obstacles on the funds for defense. I’m sure the EU will find a way to prevent Turkey from having any access.”

- Since his meeting with US President Donald Trump, Putin has engaged in something of a diplomatic flurry with BRICS partners, holding calls with Indian PM Narendra Modi, South African President Cyril Ramaphosa, and Brazilian President Luiz Inacio Lula da Silva.

EUROPE ISSUANCE UPDATE

Finland syndication: Final terms

- E4bln (MNI expected E3bln but noted upsizing to E4bln was possible) of the new 7-year Apr-32 RFGB. Books in excess of E33bln, spread set at MS + 29bp (guidance was MS + 31bps area)

ESM syndication: Mandate

- "Today ESM, the European Stability Mechanism has sent a Request for Proposal to a selection of banks from the EFSF/ESM Market Group with regards to an upcoming transaction, subject to market conditions."

- This likely means a transaction on Monday / Tuesday next week.

- We had flagged an ESM/EFSF transaction as likely in late August (although we thought EFSF was more likely).

German auction results

- Very weak Bund auction on the Aug-54 line with a 1.03x bid-to-cover and 0.79x bid-to-offer. The low price achieved at the auction was also lower than the pre-auction midprice.

- The 1.03x bid-to-cover is the lowest seen since 2018 in the German 30-year segment.

- The line was seeing some contained weakness in the minutes after the auction, bottoming out at 85.407 vs 85.560 right before the auction.

- The Aug-46 line fared better, with solid demand metrics and the low price achieved at the auction above the pre-auction mid.

- Bund futures came off the highs past the auction.

- E1bln (E747mln allotted) of the 2.50% Aug-46 Bund. Avg yield 3.18% (bid-to-offer 2.33x; bid-to-cover 3.13x).

- E1.5bln (E1.15bln allotted) of the 2.50% Aug-54 Bund. Avg yield 3.28% (bid-to-offer 0.79x; bid-to-cover 1.03x).

GBPUSD Struggles to Build on Post-CPI Rally

- GBP/USD remains below the earlier post-CPI high of 1.3509, with the pair failing to test earlier highs despite the edge lower in the USD Index at the NY crossover. Bucking the recent trend, GBP volumes have been far healthier relative to recent weeks, with cumulative activity close to 35% above average for this time of day.

- In currency options space, the spot moves have failed to elicit much notable GBP/USD flow, however EUR/GBP saw some sizeable trades consistent with short- and medium-term downside exposure via 0.8675 puts rolling off on Dec 17th (thereby capturing the lead-up to the December rate decision, but not the decision itself) and 0.8325 puts expiring in July '26.

- Consistent with today's market reaction, most see today's inflation print as posing short-term upside risks for GBP, but the broader impact should be limited for markets given the recent hawkish tilt in the MPC's voting patterns.

- HSBC write that the risk of poor jobs and GDP data slowing inflation more quickly helped limit the market reaction to today's CPI print, however the timing of the next rate cut remains in the balance and could support GBP near-term. They see US factors remaining the key driver for GBP/USD, but further BOE cuts into Q3 2026 should boost EUR/GBP, and see the Autumn Budget posing a risk to GBP over the coming months.

- MUFG see the details of today's CPI arguing against cutting rates further in the near-term. The BoE additionally will be concerned that higher inflation will feed through to inf2ation expectations adding to persistence risks. MUFG see long-run persistent inflation as being a negative development for GBP.

- ING warn against chasing the CPI rally in GBP, as the BoE is more concerned about food inflation, which hasn't changed much in today's release. As such, they doubt today's print will alter much of the BoE's current thinking. They see risk of GBP/USD sinking back to the 1.3470/80 area today.

FOREX: NZDUSD Prints Four-Month Lows Following Dovish RBNZ Cut

- The New Zealand dollar has been under significant pressure Wednesday, after the RBNZ committee voted to reduce the OCR by 25bps to 3.00%. There were two votes for a larger 50bp interest rate cut, representing the most fractious vote split in the MPC’s history. The dovish tilt saw NZGBs close 10-16bp richer, with OIS pricing down 14-23bp across future meetings, and 35bp of further easing priced by November.

- Kiwi weakness had been notable ahead of the decision, largely reflective of the weakness for the major equity benchmarks. NZDUSD recorded its first print below 0.5900 in two weeks, and the subsequent extension south has seen the pair trade down to a four-month low at 0.5815.

- Exponential moving average studies have moved into a bear-mode position and today’s move through the May lows bolsters the short-term bearish momentum. The 50% and 61.8% retracements of the April-July price swing are the next notable support levels, located at 0.5803 and 0.5728 respectively.

- In the crosses, AUDNZD has broken a number of daily highs just below the psychological 1.10 mark, rising to an intra-day high of 1.1069 and the highest level since early March. Further strength would place the focus back on key medium-term resistance between 1.1175/80.

- Following the upside surprise for UK inflation data, GBPNZD has surged 1.2%, briefly extending the bounce from the July lows to 4.25%. Price action for the cross has significantly narrowed the gap to the blowout highs from April this year, located around 2.3350. Downtrend resistance from the 2015 highs comes in just below this level.

FOREX: UK Inflation Favours GBP, But No Range Break Yet

- UK inflation data came in hotter-than-expected, with an outsized contribution from services inflation helping boost the headline print to 3.8%. This leaves the UK with one of the highest core rates of inflation in the G10, and while much of the pressure stemmed from seasonality (airfares in particular), it still relieves pressure on the MPC to lean further on this year's easing cycle. That said, market moves have been generally contained. Year-end SONIA pricing factored out around 1bps of BoE rate cuts (now at ~12bps), and pressured EUR/GBP to daily lows of 0.8609 as a result.

- NZD slips against all others in G10 on the RBNZ rate decision for August. The bank cut rates by 25bps, but more importantly triggered NZD sales by signalling deeper rate cut below neutral - pressing markets to price in a greater likelihood of 50bps of further cuts into year-end. NZD/USD made light work of the 0.5833 200-dma support in the initial reaction, having already cleared 0.5847. 0.5803 marks the next downside level: the 50% retracement for the rally off the April low.

- The USD Index has crept to a new weekly high at 98.441 despite the GBP rally. Prices continue to edge higher as markets appear to be adopting a more neutral position headed into Friday's Jackson Hole appearance from Chair Powell. Despite Trump's renewed criticism of Powell's approach to policy overnight (this time, Trump highlighted the issues for the housing market from high rates), there remains a risk that Powell pushes against the urgency of easing in September - any suggestion of which would work against the 21bps of cuts currently priced, and favour the dollar.

- Fed minutes due Wednesday will be carefully watched for the conversation around rates and, in particular, any clues as to whether further FOMC members came close to dissenting alongside Bowman and Waller at the most recent rate decision. While today's Fed release will be of importance, it's Powell's appearance at Jackson Hole on Friday that'll likely be of more market interest.

OPTIONS: Expiries for Aug20 NY cut 1000ET (Source DTCC)

- EUR/USD: $1.1550(E915mln), $1.1600(E854mln), $1.1660-75(E1.4bln)

- USD/JPY: Y147.25-35($982mln), Y148.00-10($1.5bln)

- USD/CAD: C$1.3800($1.1bln), C$1.3835-55($872mln)

- USD/CNY: Cny7.1050($500mln)

EQUITIES: Trend Set-Up in Eurostoxx 50 Futures Remains Bullish

- The trend set-up in Eurostoxx 50 futures remains bullish and the contract traded to a fresh short-term cycle high yesterday. The print above the May and July highs strengthens a bull theme and signals scope for a climb towards 5575.00, the Mar 3 high (cont) and key resistance. Moving average studies remain in a bull-mode position, highlighting an uptrend. Support to watch lies at 5355.64, the 50-day EMA.

- The dominant uptrend in S&P E-Minis remains intact and the latest shallow retracement is considered corrective. Moving average studies are in a bull-mode position, highlighting a clear uptrend. A resumption of gains would pave the way for a climb towards 6523.63, a Fibonacci projection. On the downside, supports to watch are; 6402.75, the 20-day EMA, and 6282.00, the 50-day EMA.

COMMODITIES: Bullish Theme in Gold Intact, Despite Recent Pullback

- WTI futures remain in a clear bear cycle and the contract continues to trade closer to its recent lows. A key support at $61.99, the Jun 30 low, has been breached, strengthening a bearish theme. A continuation lower would open $57.71, the May 30 low. Key short-term resistance has been defined at $69.36, the Jul 30 high. Clearance of this level would cancel a bear theme. Initial resistance to watch is $63.91, the 50-day EMA.

- Despite the latest pullback, a bull cycle in Gold remains intact. Moving average studies are in a bull-mode position. The sideways trend that has been in place since the Apr peak appears to be a corrective phase - a pause in the uptrend. A resumption of gains would open $3439.0, the Aug 23 high. Key resistance and the bull trigger is at $3500.1, the Apr 22 low. On the downside, first support to watch lies at $3268.2, the Jul 30 low.

| Date | GMT/Local | Impact | Country | Event |

| 20/08/2025 | 1100/0700 | ** | MBA Weekly Applications Index | |

| 20/08/2025 | 1430/1030 | ** | DOE Weekly Crude Oil Stocks | |

| 20/08/2025 | 1430/1030 | ** | US DOE Petroleum Supply | |

| 20/08/2025 | 1500/1100 | Fed Governor Christopher Waller | ||

| 20/08/2025 | 1700/1300 | ** | US Treasury Auction Result for 20 Year Bond | |

| 20/08/2025 | 1800/1400 | FOMC Minutes | ||

| 20/08/2025 | 1900/1500 | Atlanta Fed's Raphael Bostic | ||

| 21/08/2025 | 2300/0900 | *** | Judo Bank Flash Australia PMI | |

| 21/08/2025 | 0030/0930 | ** | Jibun Bank Flash Japan PMI | |

| 21/08/2025 | 0600/0700 | *** | Public Sector Finances | |

| 21/08/2025 | 0600/0800 | ** | Norway GDP | |

| 21/08/2025 | 0715/0915 | ** | S&P Global Services PMI (p) | |

| 21/08/2025 | 0715/0915 | ** | S&P Global Manufacturing PMI (p) | |

| 21/08/2025 | 0730/0930 | ** | S&P Global Services PMI (p) | |

| 21/08/2025 | 0730/0930 | ** | S&P Global Manufacturing PMI (p) | |

| 21/08/2025 | 0800/1000 | ** | S&P Global Services PMI (p) | |

| 21/08/2025 | 0800/1000 | ** | S&P Global Manufacturing PMI (p) | |

| 21/08/2025 | 0800/1000 | ** | S&P Global Composite PMI (p) | |

| 21/08/2025 | 0830/0930 | *** | S&P Global Manufacturing PMI flash | |

| 21/08/2025 | 0830/0930 | *** | S&P Global Services PMI flash | |

| 21/08/2025 | 0830/0930 | *** | S&P Global Composite PMI flash | |

| 21/08/2025 | 0900/1100 | ** | Construction Production | |

| 21/08/2025 | 1000/1100 | ** | CBI Industrial Trends | |

| 21/08/2025 | 1130/0730 | Atlanta Fed's Raphael Bostic | ||

| 21/08/2025 | 1230/0830 | *** | Jobless Claims | |

| 21/08/2025 | 1230/0830 | ** | WASDE Weekly Import/Export | |

| 21/08/2025 | 1230/0830 | * | Industrial Product and Raw Material Price Index | |

| 21/08/2025 | 1230/0830 | ** | Philadelphia Fed Manufacturing Index | |

| 21/08/2025 | 1345/0945 | *** | S&P Global Manufacturing Index (Flash) | |

| 21/08/2025 | 1345/0945 | *** | S&P Global Services Index (flash) | |

| 21/08/2025 | 1400/1000 | *** | NAR existing home sales | |

| 21/08/2025 | 1400/1000 | * | Services Revenues | |

| 21/08/2025 | 1400/1600 | ** | Consumer Confidence Indicator (p) | |

| 21/08/2025 | 1430/1030 | ** | Natural Gas Stocks | |

| 21/08/2025 | 1530/1130 | ** | US Bill 04 Week Treasury Auction Result | |

| 21/08/2025 | 1530/1130 | * | US Bill 08 Week Treasury Auction Result | |

| 21/08/2025 | 1700/1300 | ** | US Treasury Auction Result for TIPS 30 Year Bond |