MNI US MARKETS ANALYSIS - GBP Hits New High, USD Selling Phase

Highlights:

- Treasuries consolidate late Thursday bounce, US-EU trade in focus on report Trump is pushing for lower levies from Brussels

- CNH rally adds to broad strength in APAC FX across the week

- GBP hits new multi-year high on solid retail sales

US TSYS: Consolidation Of Bounce From Yesterday’s Long End Lows

- Treasuries are little changed on net, consolidating a bounce off yesterday’s long-end lows after 30Y yields fleetingly cleared 5.15%.

- Cash Tsys see an early close today (1400ET) and are closed Monday for Memorial Day. Futures see a full session today before an early close Monday (1300ET).

- The FT overnight reported that President Trump is pushing the EU to cut tariffs or face extra duties, with USTR Greer preparing to tell EU counterpart that the recent “explanatory note” falls short of US expectations.

- Japan PM Ishiba and US President Trump spoke via phone ahead of further trade talks between the two countries.

- Cash yields are between 0-1bp lower on the day.

- 30Y yields trade at 5.031% (-0.8bp), off yesterday’s 5.1501% (2023 high 5.1764%, before that last higher 2007). 5s30s trades at 94bps after yesterday’s fresh ytd highs with a breach of 100bps.

- TYM5 trades at 109-30 (+ 03+) off an earlier high of 110-03+, firmly within the week’s range.

- It has lifted a little closer to a key near-term resistance level at 110-21+ (May 16 high) but a key support also remains exposed, with 109-13 (May 22 low) above the key 109-08 (Apr 11 low).

- TY volumes are boosted by the ongoing roll, estimated at now a little over 40% complete.

- Data: New home sales Apr (1000ET), KC Fed services May (1100ET)

- Fedspeak: Goolsbee (0830ET), Musalem & Schmid (0935ET), Cook (1200ET) – see STIR bullet

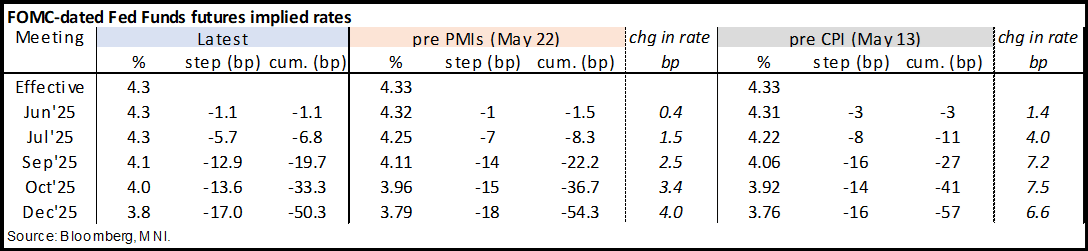

STIR: Circa 50bp Of Fed Cuts For 2025; Dove vs Hawks Ahead

- Fed Funds implied rates for 2025 meetings keep to narrow ranges seen since after the US-China trade de-escalation on May 12, close to the most hawkish they’ve been since February.

- The US Supreme Court yesterday ruled that the Fed is a "uniquely structured, quasi-private entity" and its decision allowing removal of officials at other agencies won't apply to the Fed.

- Cumulative cuts from 4.33% effective: 1bp Jun, 7bp Jul, 19.5bp Sep, 33.5bp Oct and 50.5bp Dec.

- The SOFR implied terminal yield is 1.5bp lower on the day at 3.35% (SFRZ6), at the low end of that two-week range.

- Today sees Fedspeak from current year voters at both ends of the hawk-dove spectrum.

- 0830ET - Goolsbee (’25 voter, dove) on CNBC. He last spoke on May 14, seeing underlying hard data suggesting a still solid economy, which whilst of note for one of the most dovish members of the FOMC was less surprising having told the NY Times earlier that week that "'If we could get the dust out of the air, it would make sense to think that rates would be going down […] But the bar for action has to be high when there's so much uncertainty.' He also talked on data lags and the extra importance of listening to people in real time.

- 0935ET – Musalem & Schmid (’25 voters, hawks) in fireside chat – Q&A only. Musalem on May 20 reiterated that overall he agrees with the "wait-and-see" approach adopted by the Fed amid heightened tariff-related uncertainty. Depending on how tariffs and their impacts play out, he appeared to suggest he could support either an easing bias; a "balanced" approach, or holding rates indefinitely. Schmid last spoke on Apr 17, simply noting that the US economy is still in good shape but noted a lot of nervousness around the flow of agricultural goods (being the Kansas City Fed president).

- 1200ET – Gov. Cook (voter) on financial stability – text only.

STIR: Positions Added In Front End Of SOFR Strip On Thursday

The lack of net change in SFRH5 & M5 during Thursday ‘s flattening of the SOFR strip makes it very difficult to provide any real inference when it comes to net positioning swings in the very front end.

- What we can suggest is that just under ~130K of fresh positions were added across those contracts.

- A mix of net short setting and long cover was then seen through the remainder of the whites, net short cover then came to the fore in the reds and greens.

| 22-May-25 | 21-May-25 | Daily OI Change |

| Daily OI Change In Packs |

SFRH5 | 1,076,498 | 1,050,602 | +25,896 | Whites | +132,206 |

SFRM5 | 1,324,179 | 1,220,901 | +103,278 | Reds | -11,269 |

SFRU5 | 1,096,261 | 1,085,535 | +10,726 | Greens | -27,468 |

SFRZ5 | 1,071,137 | 1,078,831 | -7,694 | Blues | +950 |

SFRH6 | 763,461 | 762,008 | +1,453 |

|

|

SFRM6 | 721,150 | 734,516 | -13,366 |

|

|

SFRU6 | 758,414 | 742,521 | +15,893 |

|

|

SFRZ6 | 870,549 | 885,798 | -15,249 |

|

|

SFRH7 | 698,212 | 727,206 | -28,994 |

|

|

SFRM7 | 592,082 | 596,466 | -4,384 |

|

|

SFRU7 | 394,769 | 392,347 | +2,422 |

|

|

SFRZ7 | 412,927 | 409,439 | +3,488 |

|

|

SFRH8 | 271,642 | 267,599 | +4,043 |

|

|

SFRM8 | 199,241 | 197,420 | +1,821 |

|

|

SFRU8 | 153,039 | 156,621 | -3,582 |

|

|

SFRZ8 | 168,938 | 170,270 | -1,332 |

|

|

BONDS: Pullback From Session Highs After Benefitting From Long End JGB Rally

Bonds pull back from session highs after the bid that was tied to a late Tokyo rally in the Japanese long end falters.

- ECB negotiated wage data was a touch softer than the loose consensus from the sell-side reports that we read (+2.4% Y/Y vs. +2.5-2.7%).

- This, coupled with some weakness in equities, has allowed bonds to stabilise after the pullback from highs.

- Bund futures trade in the middle of their range at 130.05, key support at 129.13 untested, with resistance located at 130.75. The early May pullback in the contract appears corrective.

- German curve flatter, yields little changed to -2.5bp. 5s30s back to 95bp after registering a fresh cycle high at 99.2bp yesterday.

- Less dovish than usual comments from ECB’s Stournaras provided some modest weight to the front end of the curve/EUR STIRs early today.

- EGB spreads to Bunds little changed.

- Focus continues to fall on the 10-Year BTP/Bund spread, which hovers around 100bp, with moves below remaining limited at this stage. We have previously argued that sustained moves below 100bp likely require more meaningful progress in EU-U.S. trade talks. We also noted that positive action from Moody's at this evening’s scheduled rating review of Italy could also provide a catalyst for further narrowing.

- Gilt futures +20 or so at 90.65, sticking within the pre-existing weekly range.

- Yields +1.5bp to -2.5bp, front end weigh by strong UK retail sales data, while the long end benefits from cross-market inputs detailed above.

- Lower tier U.S. data and Fedspeak is due in NY hours, with little scheduled Eurozone/UK event risk evident during the remainder of the session.

CHINA: CNH Rally Fits APAC Theme, But PBOC Liquidity Preference Stabilises Fwds

USD/CNH spot has shown through the May lows on the latest phase of dollar weakness, meaning a close at current levels would be the lowest since November and the lowest of Trump's term so far. As was the case in early May, much of the intraday CNH gains being led by the run of stronger-leaning CNY fixes: this week's fix at 7.1903 USD/CNY midpoint was the lowest since early April and goes further in reversing the tariff-tripped CNY depreciation seen in early April.

- Trade optimism is partly responsible here, and fits theme of stronger APAC currencies (seen across KRW, TWD, HKD, IDR and others since April). While expectations for a wide-ranging settlement before the August 12th deadline (when the 90-day tariff delay expires) are scant, orderly markets suggest an underlying expectation we won't see a return of 145% (or higher) tariffs once that period expires.

- The scale of official intervention remains a key focus for the near-term trajectory. Notably, China's 50-year bond sale today saw yields rise for the first time in three years - mimicking the eventful US and Japanese 20y bond sales this week, however this lower demand at auction is more likely a preference for riskier assets given the far-ranging policy package last month, rather than the buyer's strikes evident elsewhere.

- This is also reflected in the PBOC's strong preference for liquidity support in the last few weeks - with heightened reverse repo activity pressuring local CNY rates and likely containing the extent of the break lower in USD/CNH Friday, and stabilising the front-end of the forward curve.

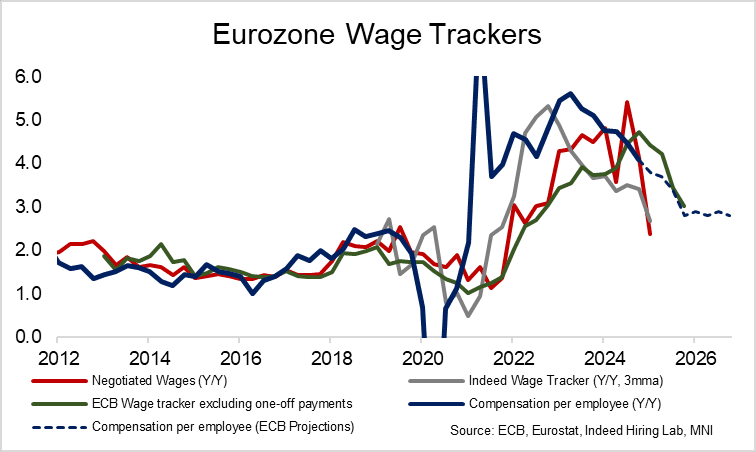

EUROZONE DATA: Negotiated Wage Growth Eases A Little More Than Expected In Q1

The ECB series for negotiated wage growth was softer than expected in Q1, by 0.1pp compared to the ECB’s own forward-looking wage tracker and slightly more so for some analysts although with some caveats. It will add confidence to the ECB that disinflationary pressures from the labor market – one of the Governing Council’s key views – remains in train.

- Eurozone negotiated wage growth slowed from 4.12% Y/Y in Q4 to 2.38% Y/Y in Q1 for its softest since 4Q21.

- It’s on the low side of expectations: there wasn't a solid consensus, but the ECB's forward looking wage tracker alongside some sell-side estimates we had seen suggested around 2.5-2.7% Y/Y. However, some of the higher estimates had come prior to yesterday’s German data for instance.

- The ECB’s wage tracker including unsmoothed one-off payments looked for 2.51% Y/Y in Q1 (which it sees ending the year at 2.9% Y/Y) but the much smoother tracker ex one-off payments was estimated at 4.4% Y/Y in Q1 which it sees easing to 3.0% in 4Q25.

- Note that the miss relative to analyst estimates reflects German and possibly French relative weakness, something that continued to be reflected in yesterday’s PMIs. Nomura for instance had forecast 2.6% Y/Y for Q1 based on 65% of country-level data that were already known - the main elements that hadn’t been published were German data for Mar 2025 and French data for 1Q25.

- Since then, the Bundesbank noted in its monthly report yesterday that Q1 negotiated pay including ancillary agreements rose just 0.9% Y/Y vs 5.8% Y/Y in Q4. The sharp slowdown reflected the end of a tax exemption on extra bonuses used to compensate for inflation and without these special payments wage growth would have been 6.7% Y/Y.

- For context with alternative indicators more broadly, the 2.4% YY is softer than the three-month average of the Eurozone Indeed wage tracker eased to 2.67% Y/Y in March from 2.86% in Feb and 3.41% in Dec. It follows a period with negotiated wage growth coming in notably stronger.

RATINGS: Moody’s On Italy Headlines After Hours

Sovereign credit rating reviews of note scheduled for after hours on Friday include:

- Fitch on Cyprus (current rating: A-; Outlook Stable)

- Moody’s on Cyprus (current rating: A3; Outlook Stable), Italy (current rating: Baa3; Outlook Stable) & the United Kingdom (current rating: Aa3; Outlook Stable)

- Morningstar DBRS on Slovenia (current rating: A (high), Positive Trend)

- Scope Ratings on Italy (current rating: BBB+; Outlook Stable)

- Please use this link to access the indicative sovereign rating review schedule covering the five most notable rating agencies for 2025.

- Note that this schedule is indicative only and ratings can be reviewed on an ad-hoc basis. Rating agencies may also adjust their schedules during the year.

FOREX: USD Weakness Pervades, China Currency Leading Gains

- Greenback slippage has resumed ahead of the NY crossover, with the USD lower against all others in G10 and adding additional pressure to the USD Index. The greenback is testing early May lows, with the USD/CNH chart a particular standout. A close at current or lower levels for the pair would be the lowest since November and the lowest of Trump's Presidential term so far, with prices cementing the recent close below the 200-dma in the price.

- JPY crosses remain a point of interest given the extended volatility in Japanese government bond markets. National CPI data came in ahead of expectations, supporting the recent run higher in the longer-end of the JGB curve and firming the downside argument for USD/JPY. Markets have tested, but failed to break meaningfully below, Y143.24 - the 61.8% retracement of the upleg posted off April's pullback low. The JGB yield curve has steepened further, putting the 2y10y spread to 80bps this week.

- Scandi currencies are outperforming early Friday, with NOK and SEK firming against all others alongside a generally better picture for European equity markets. Core indices are higher by 0.1 - 0.5%, with outperformance in German firms as final GDP data came in ahead of expectations.

- US data is few and far between Friday, with Canadian retail sales the highlight. CAD is underperforming headed into the release, undermined by weaker oil prices this week as markets anticipate a further production output hike from OPEC+ in the coming months.

OPTIONS: Expiries for May23 NY cut 1000ET (Source DTCC)

- EUR/USD: $1.1145-50(E1.1bln), $1.1180-85(E1.1bln), $1.1225-30(E746mln), $1.1295-00(E1.7bln), $1.1330-50(E1.3bln), $1.1400(E1.1bln), $1.1495-05(E1.9bln)

- USD/JPY: Y143.00($1.4bln), Y143.20-40($788mln), Y143.50($598mln), Y144.00($2.1bln), Y144.35-50($1.1bln), Y145.00($2.2bln)

- EUR/JPY: Y160.90-00(E570mln)

- AUD/USD: $0.6375(A$684mln)

- USD/CAD: C$1.4000-15($1.3bln)

EQUITIES: Eurostoxx 50 Futures Holding Onto Latest Gains

- Eurostoxx 50 futures are holding on to their recent gains and a bullish theme remains intact. The contract is extending the recent breach of 5263.01, 76.4% of the Mar 3 - Apr 7 bear leg, and maintains the sequence of higher highs and higher lows. Sights are on 5516.00, the Mar 3 high and the key bull trigger. Key support to watch lies at 5219.78, the 50-day EMA. Clearance of this level would signal a possible reversal.

- A bullish trend condition in S&P E-Minis remains intact and the latest pullback is considered corrective - for now. Moving average studies have recently crossed into a bull-mode position. This has strengthened the current bullish theme and signals scope for a continuation near-term. Sights are on the 6000.00 handle next. Initial firm support to watch lies at 5715.60, the 50-day EMA. A clear break of it would highlight a potential reversal.

COMMODITIES: Gold Recovers Well From Recent Lows

- WTI futures traded to a fresh S/T cycle high Wednesday before finding resistance. The recovery since Apr 9, appears corrective. Key resistance to watch is $62.82, the 50-day EMA. It has been pierced, a clear break of it would highlight a stronger reversal and open $65.82, Apr 4 high. For bears a reversal lower would refocus attention on $54.33, the Apr 9 low and bear trigger. Wednesday’s price pattern is a shooting star - a reversal signal.

- Gold has recovered from its recent lows. The climb signals the end of the corrective phase between Apr 22 - May 15. Medium-term trend signals are unchanged, they remain bullish. Note that moving average studies are in a bull-mode position highlighting a dominant uptrend. A continuation higher would open $3435.6 next, the May 7 high. Key support and the bear trigger has been defined at $3121.0, the May 15 low.

| Date | GMT/Local | Impact | Country | Event |

| 23/05/2025 | 1230/0830 | * | Quarterly financial statistics for enterprises | |

| 23/05/2025 | 1230/0830 | ** | Retail Trade | |

| 23/05/2025 | 1230/0830 | ** | Retail Trade | |

| 23/05/2025 | 1335/0935 | Kansas City Fed's Jeff Schmid | ||

| 23/05/2025 | 1400/1000 | *** | New Home Sales | |

| 23/05/2025 | 1400/1000 | *** | New Home Sales | |

| 23/05/2025 | 1600/1800 | ECB's Schnabel Speech on Financial Education and Monpol | ||

| 23/05/2025 | 1600/1200 | Fed Governor Lisa Cook | ||

| 23/05/2025 | 1700/1300 | ** | Baker Hughes Rig Count Overview - Weekly | |

| 23/05/2025 | 1700/1300 | ** | Baker Hughes Rig Count Overview - Weekly |