EUROZONE DATA: Negotiated Wage Growth Eases A Little More Than Expected In Q1

May-23 09:39

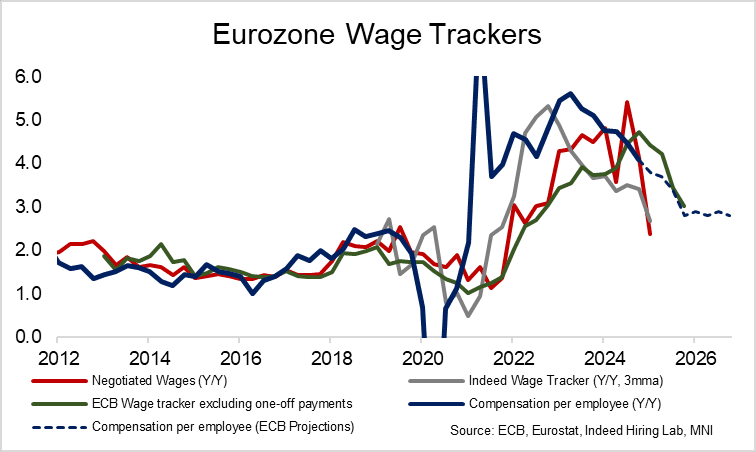

The ECB series for negotiated wage growth was softer than expected in Q1, by 0.1pp compared to the ECB’s own forward-looking wage tracker and slightly more so for some analysts although with some caveats. It will add confidence to the ECB that disinflationary pressures from the labor market – one of the Governing Council’s key views – remains in train.

- Eurozone negotiated wage growth slowed from 4.12% Y/Y in Q4 to 2.38% Y/Y in Q1 for its softest since 4Q21.

- It’s on the low side of expectations: there wasn't a solid consensus, but the ECB's forward looking wage tracker alongside some sell-side estimates we had seen suggested around 2.5-2.7% Y/Y. However, some of the higher estimates had come prior to yesterday’s German data for instance.

- The ECB’s wage tracker including unsmoothed one-off payments looked for 2.51% Y/Y in Q1 (which it sees ending the year at 2.9% Y/Y) but the much smoother tracker ex one-off payments was estimated at 4.4% Y/Y in Q1 which it sees easing to 3.0% in 4Q25.

- Note that the miss relative to analyst estimates reflects German and possibly French relative weakness, something that continued to be reflected in yesterday’s PMIs. Nomura for instance had forecast 2.6% Y/Y for Q1 based on 65% of country-level data that were already known - the main elements that hadn’t been published were German data for Mar 2025 and French data for 1Q25.

- Since then, the Bundesbank noted in its monthly report yesterday that Q1 negotiated pay including ancillary agreements rose just 0.9% Y/Y vs 5.8% Y/Y in Q4. The sharp slowdown reflected the end of a tax exemption on extra bonuses used to compensate for inflation and without these special payments wage growth would have been 6.7% Y/Y.

- For context with alternative indicators more broadly, the 2.4% YY is softer than the three-month average of the Eurozone Indeed wage tracker eased to 2.67% Y/Y in March from 2.86% in Feb and 3.41% in Dec. It follows a period with negotiated wage growth coming in notably stronger.

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

GERMAN AUCTION RESULTS: Very soft 10-year Bund auction; still no futures impact

Apr-23 09:37

- Another German auction with soft demand - this time for a 10-year Bund.

- That was the smallest volume of bids for a 10-year Bund auction since October 2022.

- Some of this is expected as it is a smaller auction size (E4.0bln rather than the recent E4.5bln) but the bid-to-offer of 1.06x compares to 1.64x earlier this month and the bid-to-cover of 1.38x compares to 2.16x - so those metrics are weak too.

- Still not a big impact on Bund futures.

GILTS: Twist Flattening Holds, BoE Comments Eyed

Apr-23 09:33

Twist flattening has dominated on the gilt curve this morning, with 3 factors defining this morning’s price action:

- Spillover from Tsys after U.S. President Trump pushed back against the idea that he was looking to fire Fed Chair Powell, as well as some comments pointing to the potential for a moderation in the Sino-U.S. trade war.

- The DMO’s revised gilt remit surprising most by coming in marginally lower than the prior estimate, skewing issuance further away from the long end in the process (T-bill, short-dated and unallocated bucket issuance was revised higher, while long-end issuance was revised lower).

- Softer-than expected flash PMIs.

- Gilt futures broke through initial resistance at the open, with bulls now looking to pierce 93.00 before shifting focus to a Fibonacci retracement at 93.44. The contract last prints 92.80 vs. session highs of 92.95.

- Yields 3.5bp higher to 9bp lower.

- 2s10s ~13bp off cycle closing highs, last ~65.6bp.

- 5s30s ~11bp off yesterday’s cycle closing high, last 127.8bp.

- BoE-dated OIS covering ’25 meetings back to little changed on the day, showing 92bp of cuts through year-end, with the next 25bp step still fully discounted through the May meeting. Recent range extremes of ~97bp of cuts through year-end remains untested/intact.

- Comments from BoE’s Pill (11:30 BST), Bailey (18:15 BST) & Breeden (19:00 BST) due throughout the day.

GERMAN AUCTION RESULTS: 2.50% Feb-35 Bund

Apr-23 09:31

| 2.50% Feb-35 Bund | Previous | |

| ISIN | DE000BU2Z049 | |

| Total sold | E4bln | E4.5bln |

| Allotted | E3.049bln | E3.42bln |

| Avg yield | 2.47% | 2.68% |

| Bid-to-offer | 1.06x | 1.64x |

| Bid-to-cover | 1.38x | 2.16x |

| Avg Price | 100.25 | 98.45 |

| Low Price | 100.23 | 98.43 |

| Pre-auction mid | 100.230 | 98.434 |

| Previous date | 02-Apr-25 |