MNI US MARKETS ANALYSIS - GBP Hits a New Recovery High

Highlights:

- Curve sits bull flatter into PPI, weekly jobless claims numbers

- GBP hits new recovery high as UK GDP prints ahead of expectations

- Prepwork for Russia-US meet begins in earnest; Trump & Putin to hold joint presser

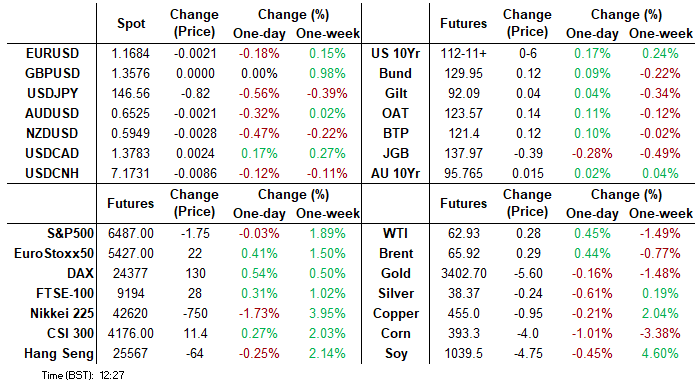

US TSYS: Bull Flatter With PPI and Claims Headlining Docket

- Treasuries sit bull flatter today, with the front end somewhat pinned ahead of important updates from PPI inflation for July and latest jobless claims data. SF Fed’s Daly pushed back on the need for a 50bp cut.

- Some flattener flow at play earlier: TUU5 10K blocked at 103-31.375 (suggest seller) and WNU5 2K blocked at 118-28 (suggest buyer) at 0349ET.

- Cash yields are 0.5-2.5bp lower, with the front end lagging declines.

- 10Y yields (currently 4.211%) came close to re-testing 4.20% earlier with 4.2018%, having recently bottomed at 4.1826% in the days after the July payrolls report on Aug 1.

- TYU5 trades at 112-11 (+05+) off an earlier high of 112-13, on modest cumulative volumes of 275k after some particularly thin overnight sessions recently.

- Extending yesterday’s gains, it has moved close to resistance at 112-15+ (Aug 5 high) after which lies 112-23 (May 1 high).

- Data: PPI Jul (0830ET), Weekly jobless claims (0830ET)

- Fedspeak: Musalem (1000ET), Barkin (1400ET) – see STIR bullet

- Bill issuance: US Tsy to sell $100B 4-wk, $85B 8-wk bills (1130ET)

- Politics: Trump delivers remarks from the Oval Office (1300ET). Tomorrow’s Trump-Putin meeting in Alaska remains front of mind from a geopolitical angle (reported for Fri at 1130 local time or 1530ET).

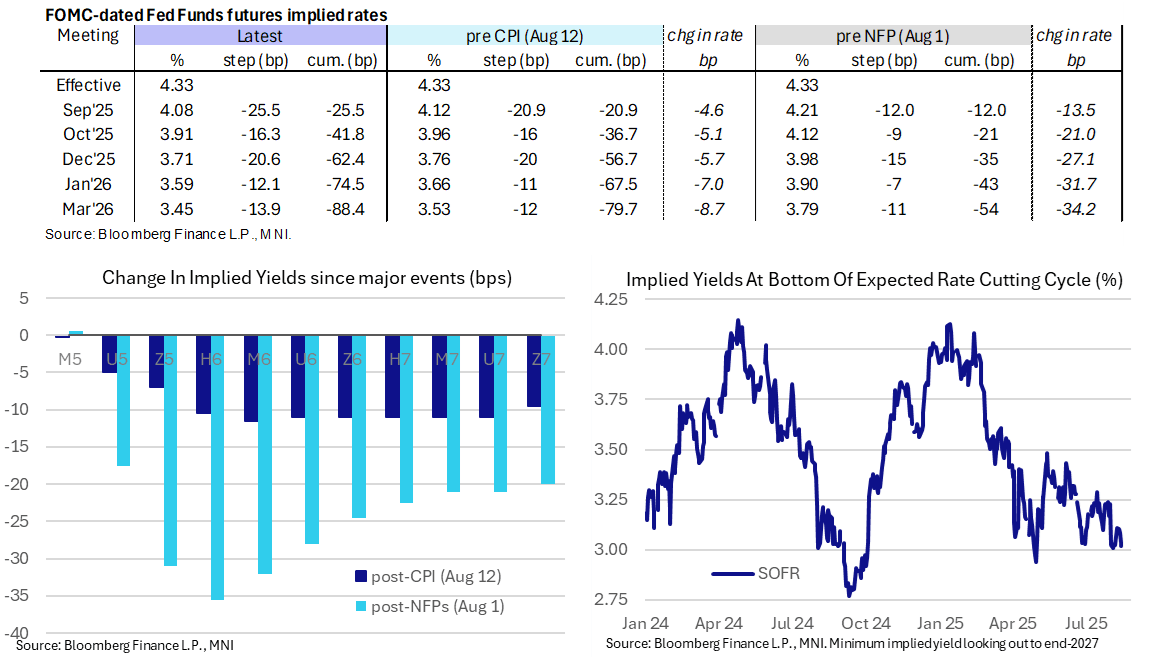

STIR: Somewhat Patient Fedspeak Helps Trimming Of Dovish Extremes

- Fed Funds implied rates are 1.5bps higher for near-term meetings, aided by recent Fedspeak pushing back against Tsy Sec Bessent’s call for a 50bp cut.

- Cumulative cuts from 4.33% effective: 25.5bp for Sept (vs 26.5bp overnight), 42bp Oct, 62.5bp Dec, 74.5bp Jan and 88.5bp Mar.

- The SOFR implied yield of 3.02% (SFRH7, -1.5bp) holds yesterday’s dip back closer to recent lows.

- The WSJ earlier today published an interview with SF Fed’s Daly (non-voter) saying a large cut next month doesn’t seem warranted as it would signal urgency but reiterated that the Fed can’t ignore the softening labor market. That didn’t surprise us after she last week characterized policy adjustments as "Recalibrating it to match the collective risks to both of our mandated goals", suggesting she doesn't see aggressive cuts.

- Chicago Fed’s Goolsbee (’25 voter, dove) said yesterday that FOMC meetings in the fall are "going to be live" but, notably for one of the more dovish members that he's "uneasy" about the idea that tariffs have only a one-off impact on prices and that he wants more surety that inflation won’t be persistent.

- Today sees two FOMC member appearances with more focus on St Louis Fed’s Musalem after he didn’t appear notably swayed by the payrolls report earlier this month.

- 1000ET – Musalem (’25 voter, hawk) said on Aug 8 that we’re missing on our inflation target and not employment. The labor market is in balance although below potential growth could pose risks to it. On inflation, he expects the tariff inflation boost will most likely be short-lived but there is a reasonable probability that inflation may be persistent.

- 1400ET – Barkin (non-voter) speaks in a NABE webinar having already spoken twice this week since CPI.

MNI: INVITE: Livestream MNI Connect ECB's Luis de Guindos On Sep 18

You are invited to listen to a Livestreamed MNI Connect Video Conference with Luis de Guindos, the Vice-President of the European Central Bank.

Details below:

- Speaker: Luis de Guindos, Vice-President of the European Central Bank

- Topic of discussion: 'Euro Area Growth and Inflation Outlook.'

- Date: Thursday 18 September, 9am-10:30am London time

- This event is on the record and will run as a Zoom Webinar

To register please go to: MNI Webcast Registration

US TSY FUTURES: Net Long Setting Dominated On Wednesday

OI data points to net long setting dominating during Wednesday’s rally, with only modest net short cover in TU futures breaking the wider theme.

- The most meaningful net positioning swing came in TY futures, with nearly $4mln DV01 equivalent of fresh net exposure added in that contract.

| 13-Aug-25 | 12-Aug-25 | Daily OI Change | OI DV01 Equivalent Change ($) |

TU | 4,495,170 | 4,509,933 | -14,763 | -536,987 |

FV | 7,084,428 | 7,055,193 | +29,235 | +1,247,009 |

TY | 5,286,228 | 5,225,969 | +60,259 | +3,983,918 |

UXY | 2,472,206 | 2,458,108 | +14,098 | +1,238,637 |

US | 1,768,421 | 1,765,950 | +2,471 | +347,743 |

WN | 2,008,790 | 2,005,650 | +3,140 | +576,746 |

|

| Total | +94,440 | +6,857,067 |

SOFR: Net Long Setting Most Prominent On Wednesday

OI data points to a mix of net long setting and short cover in SOFR futures on Wednesday, with the former proving more prominent.

- The most meaningful net positioning swing came via net long setting in SFRU5 futures, with markets moving to fully discount a 25bp cut at the Sep FOMC and starting to price outside odds of a 50bp step in the wake of comments from Tsy Sec Bessent (hedging for such an outcome via SFRU5 call structures was also noted).

- Note that the likes of Fed's Goolsbee & Daly have played down the idea of a 50bp move.

| 13-Aug-25 | 12-Aug-25 | Daily OI Change |

| Daily OI Change In Packs |

SFRM5 | 1,199,377 | 1,207,180 | -7,803 | Whites | +34,875 |

SFRU5 | 1,344,952 | 1,281,264 | +63,688 | Reds | +4,202 |

SFRZ5 | 1,364,426 | 1,370,728 | -6,302 | Greens | -5,141 |

SFRH6 | 1,026,729 | 1,041,437 | -14,708 | Blues | +11,601 |

SFRM6 | 897,468 | 894,564 | +2,904 |

|

|

SFRU6 | 876,164 | 885,067 | -8,903 |

|

|

SFRZ6 | 1,017,926 | 1,008,469 | +9,457 |

|

|

SFRH7 | 742,954 | 742,210 | +744 |

|

|

SFRM7 | 921,540 | 932,524 | -10,984 |

|

|

SFRU7 | 587,080 | 584,935 | +2,145 |

|

|

SFRZ7 | 580,141 | 577,589 | +2,552 |

|

|

SFRH8 | 344,940 | 343,794 | +1,146 |

|

|

SFRM8 | 271,499 | 273,038 | -1,539 |

|

|

SFRU8 | 205,294 | 206,036 | -742 |

|

|

SFRZ8 | 233,518 | 222,814 | +10,704 |

|

|

SFRH9 | 155,454 | 152,276 | +3,178 |

|

|

UKRAINE: Zelenskyy To Meet w/UK's Starmer After High-Profile Trump Call

President Volodymyr Zelenskyy meets with UK PM Sir Keir Starmer at the bottom of the hour in the aftermath of a series of high-level videocalls on 13 August related to the situation of the war, and more specifically, the upcoming meeting between US President Donald Trump and Russian President Vladimir Putin in Alaska on 15 August. Three main calls took place on 13 Aug: the first between Zelesnkyy and European Union leaders, the second involving Zelensky, European leaders (incl. Starmer), the NATO Secretary General Mark Rutte, and Trump and his VP JD Vance, and the third involving the 'coalition of the willing', those countries that have committed to providing peacekeeping troops to Ukraine if a peace deal is reached.

- Politico reports that the Starmer-Zelenskyy meeting is set to be a private conversation, with no press conference or media availability from either man afterwards. Zelenskyy warned on the various 13 August calls that Putin is not taking the prospect of a ceasefire seriously, and will be 'bluffing' in the talks with Trump.

- Trump warned of 'severe consequences' for Russia if Putin does not agree to an eventual peace deal, but gave no details of what these might entail. Politico reports that the US may also be willing to provide some security guarantees for Ukraine if a ceasefire is reached. Again, no details were forthcoming on what these guarantees might be, but they go some way to explaining the near-universal positive response to yesterday's calls from European leaders.

US-RUSSIA: Kremlin: Putin-Trump Summit Starts 11:30 Local, Joint Presser After

Senior aide to Russian President Vladimir Putin, Yuri Ushakov, has given details of the upcoming summit between Putin and US President Donald Trump set to take place in Anchorage, Alaska, tomorrow (15 August). Ushakov says that the summit will begin at 11:30 local time (15:30ET, 20:30BST, 21:30CET, 04:30JST). Ushakov says that the two leaders will have a one-on-one meeting with only translators present, as well as a wider meeting with delegations present and a working breakfast.

- State-run Tass reports Ushakov saying the delegations will take the 'five-to-five' formula. The Russian delegation will include Foreign Minister Sergey Lavrov, Defence Minister Andrey Belousov, Finance Minister Anton Siluanov, the Special Presidential Envoy on Foreign Investment and Economic Cooperation Kirill Dmitriev, and Ushakov himself.

- The high-ranking status of this delegation stands in stark contrast to the relatively junior group of officials sent to the three rounds of talks with Ukraine that have taken place in Istanbul in recent months.

- As such, the 'five-to-five' formula could indicate that the US delegation will therefore comprise Secretary of State Marco Rubio, Secretary of Defense Pete Hegseth, Treasury Secretary Scott Bessent, Commerce Secretary Howard Lutnick and USTR Jamieson Greer (although this lineup is yet to be confirmed).

- Putin and Trump will hold a joint news conference after the summit. There is no set timeline for how long the talks could last, so presser could take place well into the evening on the east coast/early hours of the morning in Europe.

FOREX: USD/JPY Ends Consolidation Phase With Break Lower

- USDJPY has turned lower, ending the consolidation phase that dictated play last week. Weakness today puts the price through support drawn off the early August lows as well as 146.71, a key retracement. Price action this week marks a full reversal of the previously overbought condition.

- Meanwhile, speculation around the Trump-Putin meeting in Alaska at the end of the week continues to build - after which TASS have confirmed that Trump and Putin are to hold a joint press briefing. Trump is set to pursue an immediate ceasefire in the conflict - at which point more sincere negotiations and talks can begin over a conclusion to the war.

- Territory remains the key issue, with Kyiv ruling out the handing over of eastern territories, and Putin requiring some concessions as a result of his multi-year special operation. Oil and risk markets remain sensitive to the issue, with Trump warning of "very severe consequences" if no interim agreement is reached. Reports now suggest talks are to start at 1130 local time on Friday, in Joint Base Elmendorf-Richardson, Anchorage, Alaska. That's 2030BST/1530ET. The summit will include one-on-one talks as well as delegation talks between US and Russian ministers, followed by a joint press briefing with both the Russian and US Presidents.

- NOK traded stronger despite the unchanged Norges Bank rate decision - as the Bank's decision to play down the likely downward revision to near-term inflation forecasts in the September MPR and a lack of attention to the rise in LFS unemployment leans slightly hawkish. Since the release, however, 2-year NOK swap rates fully erased the ~4bp increase, in turn helping EURNOK and NOKSEK fade a good proportion of post-decision moves. EURNOK support at the 20-day EMA was pierced earlier, but the cross is now back above this level, currently -0.2% today at ~11.9000.

- PPI data is the scheduled highlight Thursday, with markets expecting PPI inflation to rise by ~0.2ppts on both the M/M and Y/Y metrics. Weekly jobless claims numbers are also set to cross. Fed speakers include Musalem and Barkin.

HONG KONG: Sizeable Move in HKD Spot, But Not Consistent With HKMA Intervention

- Spot USD/HKD is under pressure in recent trade, slipping to touch 7.8358 before stabilising - the lowest print since late May, and well before the test of the weak-side of the band at 7.85.

- Given the scale of the spot move, no surprise to see a sharp move in HKD points: the 12m forward point discount has risen to -1105 from -1160, nearing the narrowest level since mid-July.

- The move in spot didn't appear to coincide with a test of the weak-side of the band, which hasn't really been challenged Thursday - and as such, would be inconsistent with HKMA buying HKD. That said, they have been active this week, buying HKD3.38bln off the weak-side yesterday. Resultantly, the aggregate balance should decline further once these purchases are settled: dropping to HKD 53bln and closer to the prevailing levels earlier this year (HKD 44bln).

- Instead, it appears a local liquidity squeeze may be prompting the HKD strength here: overnight HKD swaps have risen back above 0.50 and a close at current levels would be the highest since late July, and the higher HIBOR fix set overnight (1m +13bps to 1.045%) may further reflect this.

OPTIONS: Expiries for Aug14 NY cut 1000ET (Source DTCC)

- EUR/USD: $1.1500(E2.8bln), $1.1590-00(E1.8bln), $1.1625-35(E829mln), $1.1645-50(E1.3bln), $1.1660-65(E943mln), $1.1695-02(E4.9bln), $1.1710-15(E1.2bln), $1.1750(E774mln)

- USD/JPY: Y145.00($924mln), Y146.00($616mln), Y146.65-85($1.0bln), Y147.00-20($1.3bln), Y148.15-30($1.2bln), Y149.00($1.2bln)

- GBP/USD: $1.2975-00(Gbp1.2bln)

- EUR/GBP: Gbp0.8690-05(E1.1bln)

- AUD/USD: $0.6575(A$516mln), $0.6600(A$1.3bln)

- NZD/USD: $0.6000-11(N$636mln)

- USD/CAD: C$1.3860-70($768mln)

EQUITIES: E-Mini S&P at New Highs, Targets Retracement Levels Next

- The bounce off post-NFP lows in global equity indices persists, with the Eurostoxx 50 future recovering back above the 50-day EMA. Markets look to build a base above this level, through which additional strength refocuses attention on 5486.00, the May 20 high. To the downside, recent impulsive weakness did result in a temporary breach of the bear trigger - this makes the April 30 hi/lo range at 5078-5138 the area of downside interest.

- Wednesday saw new record highs in the e-mini S&P, clearing resistance through the 6477.31 mark. This cements the underlying uptrend, exposing projection levels into 6523.63 next. Vol-based resistance kicks in at 6521.12. Through recent phases of weakness, the 50-day EMA at 6240.28, has held as support - and will be important on any subsequent declines. Clearance of this average is required to signal a stronger reversal.

COMMODITIES: Gold Off Weekly Lows, But Bounces Appear Shallow

- WTI futures traded poorly into the Wednesday close, extending losses on the clearance of the 50-day EMA and bear trigger. Markets have built on this S/T momentum lower, with support breaking at $62.77. The clear break here exposes $58.17, the May 30 low. Gains early last week marked an extension of a corrective cycle - which may now have concluded to result in cleaner positioning. $69.41 marks the 50.0% retracement of the Jun 23-24 downleg - an important level on any recovery from here.

- Gold prices are off the weekly low, however bounces appear shallow at these levels, keeping price within the mid-point of the recent range. The phase of weakness into the end of July supported the view that short-term pullbacks are corrective - for now - and the bull cycle that started Jun 30 remains intact. However, the yellow metal has traded through support at $3333.9, the 50-day EMA. A clear break of this level continues to signal scope for a deeper retracement and exposes the next key support at $3248.7, the Jun 30 low. Key near-term resistance is $3439.0, the Jul 23 high.

| Date | GMT/Local | Impact | Country | Event |

| 14/08/2025 | 1230/0830 | *** | Jobless Claims | |

| 14/08/2025 | 1230/0830 | ** | WASDE Weekly Import/Export | |

| 14/08/2025 | 1230/0830 | *** | PPI | |

| 14/08/2025 | 1230/0830 | *** | PPI | |

| 14/08/2025 | 1430/1030 | ** | Natural Gas Stocks | |

| 14/08/2025 | 1530/1130 | ** | US Bill 04 Week Treasury Auction Result | |

| 14/08/2025 | 1530/1130 | * | US Bill 08 Week Treasury Auction Result | |

| 14/08/2025 | 1800/1400 | Richmond Fed's Tom Barkin | ||

| 15/08/2025 | 2350/0850 | *** | GDP | |

| 15/08/2025 | 0200/1000 | *** | Fixed-Asset Investment | |

| 15/08/2025 | 0200/1000 | *** | Retail Sales | |

| 15/08/2025 | 0200/1000 | *** | Industrial Output | |

| 15/08/2025 | 0200/1000 | ** | Surveyed Unemployment Rate M/M | |

| 15/08/2025 | 0430/1330 | ** | Industrial Production | |

| 15/08/2025 | 0700/0900 | * | CH Flash GDP | |

| 15/08/2025 | 1230/0830 | ** | Monthly Survey of Manufacturing | |

| 15/08/2025 | 1230/0830 | ** | Wholesale Trade | |

| 15/08/2025 | 1230/0830 | *** | Retail Sales | |

| 15/08/2025 | 1230/0830 | ** | Import/Export Price Index | |

| 15/08/2025 | 1230/0830 | ** | Empire State Manufacturing Survey | |

| 15/08/2025 | 1230/0830 | *** | Retail Sales | |

| 15/08/2025 | 1300/0900 | * | CREA Existing Home Sales | |

| 15/08/2025 | 1315/0915 | *** | Industrial Production | |

| 15/08/2025 | 1400/1000 | * | Business Inventories | |

| 15/08/2025 | 1400/1000 | *** | U. Mich. Survey of Consumers | |

| 15/08/2025 | 1400/1000 | ** | University of Michigan Surveys of Consumers Inflation Expectation | |

| 15/08/2025 | 1400/1000 | * | Business Inventories | |

| 15/08/2025 | 1700/1300 | ** | Baker Hughes Rig Count Overview - Weekly | |

| 15/08/2025 | 1700/1300 | ** | Baker Hughes Rig Count Overview - Weekly | |

| 15/08/2025 | 2000/1600 | ** | TICS |