MNI US MARKETS ANALYSIS - Earnings Reach Quarterly Crescendo

Highlights:

- Earnings season reaches crescendo - over half of S&P market cap will have reported by end-of-day

- USDJPY rallies to new weekly high, above 50-dma ahead of weekend elections

- ADP & ISM Services fill data gap; labour market in focus

US TSYS: TY Trend Structure Remains Bearish Ahead Of QRA, Key Data & Alphabet

Treasuries are modestly cheaper overnight ahead of an important session including the full QRA (0830ET), notable data releases from ADP (0815ET) & ISM Services (1000ET) plus a President Trump interview. After the close, Alphabet earnings are in focus before Fed Governor Cook on monetary policy.

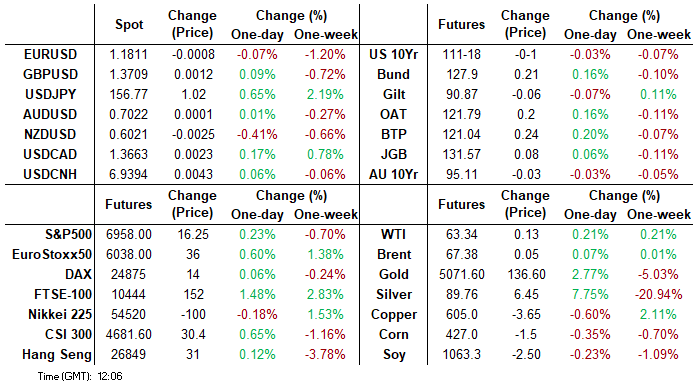

- Cash yields are 0.9-1.2bps higher across the curve.

- 10Y yields at 4.276% (+1.0bp) yesterday topped out at 4.2975% in a renewed look at the 4.30% level.

- TYH6 trades at 111-17+ (-01+) on lighter cumulative volumes of 275k after some heavier overnight sessions recently.

- It remains within yesterday’s range in moves that include a push to a low of 111-13+ as the bear trigger of 111-09 (Jan 20 low) starts to see more focus again - clearance could open the round 111-00. Support is seen at 112-02 (Feb 2 high).

- Data: MBA applications (0700ET), ADP employment Jan (0815ET), S&P Global US Services/Composite PMI Jan final (0945ET), ISM Services Jan (1000ET)

- Fedspeak: Cook on mon pol and economy (1830ET) – see STIR bullet

- Refunding: Monday’s quarterly financing estimates as usual shouldn't really change the expectations for the main event of Refunding week: the full announcement including Treasury policy statement today at 0830ET. See MNI's preview, published on Friday, here (link).

- Bill issuance: US Tsy $69B 17W bill auction (1130ET)

- Politics: Trump in TV interview (1100ET), Trump in policy meeting (1600ET)

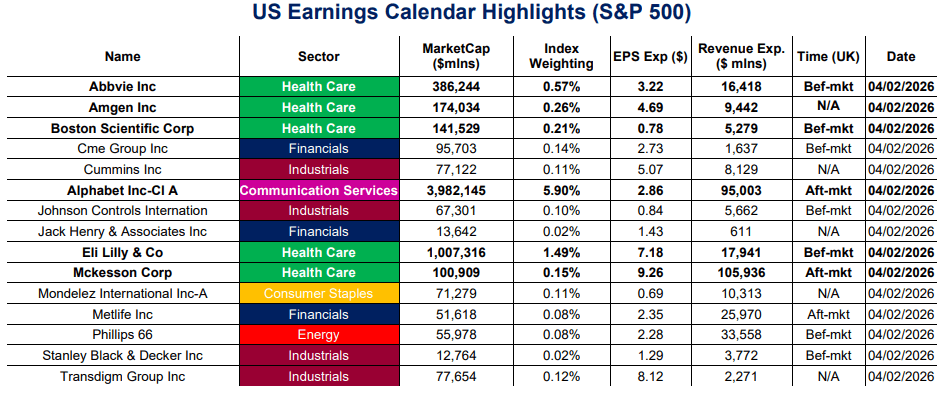

- Earnings: Dominated by Alphabet after the close. Eli Lilly has already reported, seeing 2026 revenue at $80-83B vs estimates of $77.7B

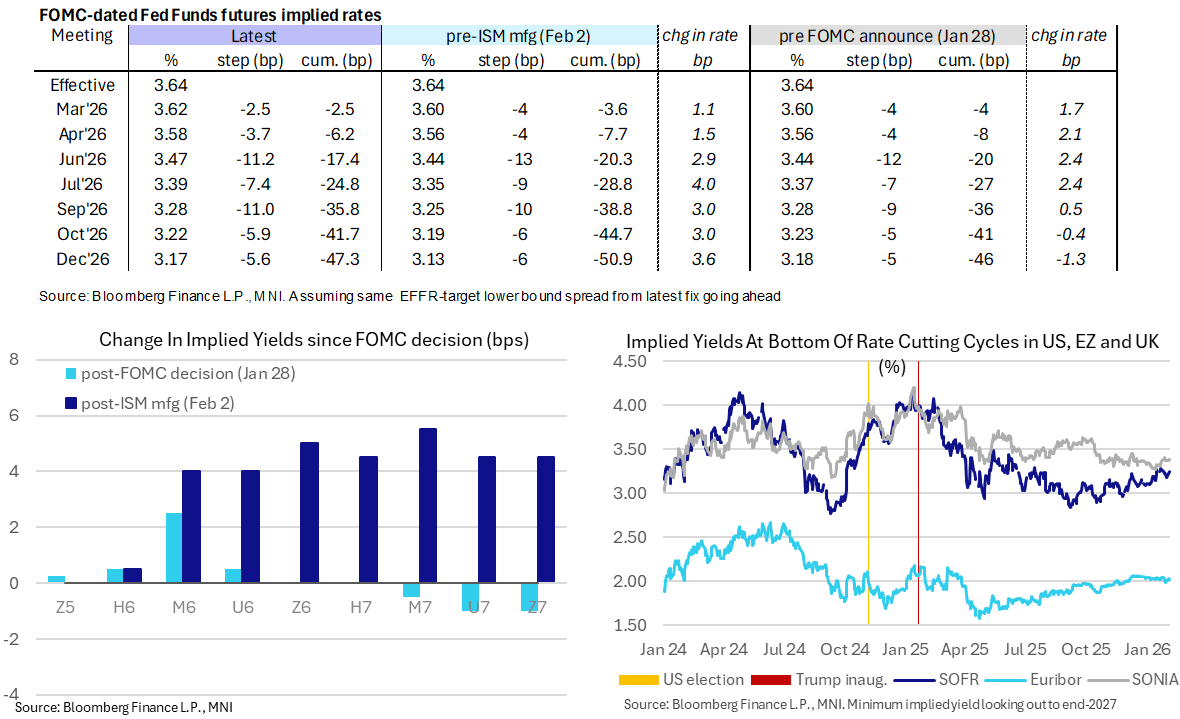

STIR: Next Fed Cut In July Ahead Of ADP and ISM Services, Cook Speech Late On

- Fed Funds implied rates are 0-2bp higher for 2026 meetings, primarily 2H26, as they shift back towards yesterday’s more hawkish levels.

- It’s ahead of the week’s main data releases (ADP employment and ISM services) with the BLS payrolls report delayed. Monday’s strong ISM manufacturing report drew a hawkish reaction.

- Cumulative cuts from 3.64% effective: 2.5bp Mar, 6bp Apr, 17.5bp Jun, 25bp Jul, 36bp Sep, 41.5bp Oct and 47.5bp Dec.

- SOFR futures are 2 ticks lower across 2027 contracts, with the terminal implied yield 3.245% (Z6, +2bp) vs the Jan 22 highest close since Jul at 3.285%.

- Today’s sole scheduled Fedspeak comes from Gov. Cook (voter) in a rare update on mon pol and the economy late on at 1830ET (text + Q&A). Focus around Cook has obviously been on her ongoing Supreme Court case (perhaps the most important case in Fed history according to Powell) and she last spoke on the economic outlook on Nov 3. We estimate she was one of the four dots at the December SEP who penciled in one cut in 2026, the median view on a highly divided FOMC.

- Gov. Miran (voter, dove) has stepped down from his CEA role (previously on unpaid leave) to remain on the Fed’s Board of Governors after the temporary role he filled ended in January. He can remain at the Fed until a successor is confirmed by the Senate.

ECB: MNI ECB Preview: Euro Intrigue Fades But Not Entirely

We have published and e-mailed to subscribers the MNI ECB Preview, found here.

- See the report for MNI analysis including the net implications for inflation forecasts from recent euro and commodity price strength

- A detailed review of pertinent ECBspeak

- Key macro developments since the last ECB meeting

- A snapshot of 27 analyst views

BOE: MNI BOE Preview: February 2026

For the full MNI BOE Preview click here

- The upcoming Bank of England meeting is probably the least anticipated quarterly meeting for some time with the MPC expected to leave Bank Rate on hold and leave guidance unchanged, but there are still aspects worth watching.

- Most in focus will be the vote split (we expect to be 7-2, in line with consensus), the Agents’ Pay Survey (which will be published alongside the decision) and the individual member paragraphs. We look at all of these in detail.

- We also summarise over 20 sellside previews - a 7-2 vote split is expected by around 2/3 of analysts with risks of 6-3 seen.

US TSY FUTURES: Mix Of Positioning Swings On Tuesday

OI data points to a mix of net short setting (TU), long cover (FV & US) and long setting (UXY) on Tuesday.

- Note that TY futures were unchanged come settlement, which means that we cannot provide much inference re: the largest net positioning swing on the day (which accounted for ~$5.7mln of the curve-wide net ~$8.2mln DV01 exposure reduction).

| 03-Feb-26 | 02-Feb-26 | Daily OI Change | OI DV01 Equivalent Change ($) |

TU | 4,648,451 | 4,639,203 | +9,248 | +342,533 |

FV | 6,825,088 | 6,851,544 | -26,456 | -1,131,862 |

TY | 5,448,848 | 5,536,359 | -87,511 | -5,728,164 |

UXY | 2,609,721 | 2,603,831 | +5,890 | +521,356 |

US | 1,711,064 | 1,724,249 | -13,185 | -1,796,525 |

WN | 2,183,694 | 2,186,179 | -2,485 | -447,937 |

|

| Total | -114,499 | -8,240,599 |

SOFR: Short Setting Dominated Through Front End Of Futures Strip On Tuesday

OI data points to net short setting dominating through the green pack on the SOFR futures strip on Tuesday as most contracts in that zone settled lower.

- Meanwhile, a mix of net long cover and long setting was seen in the blues as contracts in that pack finished either side of unchanged.

| 03-Feb-26 | 02-Feb-26 | Daily OI Change |

| Daily OI Change In Packs |

SFRZ5 | 1,362,482 | 1,365,815 | -3,333 | Whites | +41,028 |

SFRH6 | 1,409,888 | 1,392,300 | +17,588 | Reds | +47,509 |

SFRM6 | 1,449,151 | 1,442,458 | +6,693 | Greens | +17,871 |

SFRU6 | 1,473,846 | 1,453,766 | +20,080 | Blues | -37 |

SFRZ6 | 1,424,857 | 1,412,335 | +12,522 |

|

|

SFRH7 | 1,061,860 | 1,058,246 | +3,614 |

|

|

SFRM7 | 895,832 | 868,322 | +27,510 |

|

|

SFRU7 | 835,939 | 832,076 | +3,863 |

|

|

SFRZ7 | 869,158 | 855,834 | +13,324 |

|

|

SFRH8 | 524,158 | 521,378 | +2,780 |

|

|

SFRM8 | 445,197 | 439,257 | +5,940 |

|

|

SFRU8 | 387,209 | 391,382 | -4,173 |

|

|

SFRZ8 | 378,828 | 381,555 | -2,727 |

|

|

SFRH9 | 216,301 | 215,490 | +811 |

|

|

SFRM9 | 210,162 | 208,565 | +1,597 |

|

|

SFRU9 | 171,179 | 170,897 | +282 |

|

|

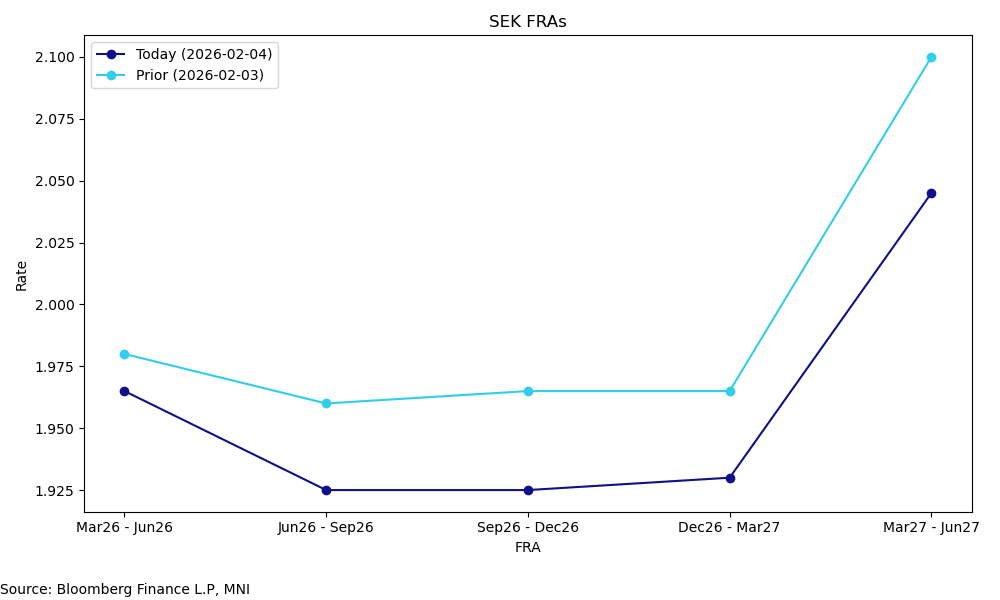

SWEDEN: Dovish Riksbank Minutes Pulls Front-end Yields Lower

This morning’s dovish set of Riksbank minutes sees the SEK FRA curve down 1.5-6bps across the front five contracts. This in turn has driven SEK FX underperformance versus the G10 basket.

- A reminder that the minutes saw Deputy Governor Jansson suggest he may vote for a cut in March, and Deputy Governor Seim soften her previously hawkish-leaning stance. While the base case is still for the policy rate to remain at 1.75% going forward, the risk of a cut has clearly risen. That places increasing focus on Friday’s flash January inflation reading.

- The dovish signals are reflected in rate market pricing, with the Sep26-Dec26 FRA down 4bps to 1.925% today, now ~8.5bps below yesterday’s 3M STIBOR fixing. This contract was trading around 2.10% in early January.

- EURSEK is up 0.65% to 10.5907. The magnitude of the bounce is likely being exacerbated by positioning dynamics. Morgan Stanley’s options-based positioning metrics assigned a 77/100 long score to EURSEK according to data as of Jan 30. The technical outlook in EURSEK remains bearish for now though, with rallies short of the 20-day EMA at 10.6393 considered corrective.

- NOKSEK is up 0.3% to 0.9272, off session highs of 0.9286. A short-term bull cycle remains in play, though the cross has struggled to push through resistance at 0.9276 in recent sessions (Dec 4 low and prior breakdown level).

FOREX: USDJPY Recovery Extends, Dovish Riksbank Minutes Weigh on SEK

- USDJPY continues to grind higher on Wednesday, extending the recovery from last week’s lows to 3%. The move back above the 50-day EMA, intersecting at 155.75, undermines the recent bear theme and highlights a stronger short-term bull cycle. Price action this morning has bridged the gap to initial resistance at 156.64, the 61.8% retracement of the Jan 14 - 27 bear leg, with 157.72 the next topside level of note.

- The swift recovery has been primarily driven by a more stable backdrop for the dollar following Kevin Warsh’s nomination, while expectations for the LDP securing a majority bring concerns surrounding Japan’s fiscal trajectory back to the fore. The firmer dollar has weighed on NZD (-0.45%) after mixed Q4 unemployment has failed to reignite bullish Kiwi momentum.

- USDCNY and USDCNH saw some buying interest in European trade, with both pairs edging to new session highs of 6.9425 and 6.9404 respectively - but we note no specific headlines behind the move. News that Putin is holding a videocall with Xi Jinping unlikely to be the driver here, but moves do follow the further strength in the CNY fix Wednesday: the 6.9533 fix was again the lowest since mid-2023 but still well above expectations (survey saw today's fix at 6.9363).

- Riksbank minutes are driving SEK underperformance. The debate amongst the Board over the next few months is clearly between holding the policy rate steady (the most likely scenario) and delivering another cut (only likely if both inflation and economic activity are weaker than expected). EURSEK has advanced 0.5% to 10.58, extending a moderate bounce from yesterday’s 10.50 cycle lows. The 20-day EMA intersects at 10.6336.

- Fed's cook is scheduled to speak on monetary policy and the economy later today, and ISM services highlights the data calendar today. Focus then turns to tomorrow's ECB and BoE decisions.

CHINA: CNY, CNH Edge to New Daily Lows, Rebuffing Strongest CNY Fix Since 2023

USDCNY and USDCNH seeing some buying interest in recent trade, with both pairs edging to new session highs of 6.9425 and 6.9404 respectively - but we note no specific headlines behind the move. News that Putin is holding a videocall with Xi Jinping unlikely to be the driver here, but moves to follow the further strength in the CNY fix Wednesday: the 6.9533 fix was again the lowest since mid-2023 but still well above expectations (survey saw today's fix at 6.9363).

- We noted yesterday that recent fix behaviour endorses CNY appreciation - but only at a pace acceptable to the authorities. Outside of the fix strategy, liquidity management into the Lunar New Year (Feb 17th) and possible market management via state-owned banks are in focus: there were several instances of state-owned banks buying USD through phases of uncomfortable CNY strength in recent years, but not recycling the purchased USD via swaps - the net result being tighter local dollar liquidity - and more acute negative carry for USD/CNY shorts.

OPTIONS: Expiries for Feb04 NY cut 1000ET (Source DTCC)

- EUR/USD: $1.1600(E1.7bln), $1.1800(E1.2bln), $1.1850(E1.7bln)

- USD/JPY: Y151.50($1.1bln), Y153.25($801mln), Y156.25($663mln)

- AUD/USD: $0.6950(A$2.0bln)

- NZD/USD: $0.5975(N$746mln)

EQUITIES: This Week's Gain Reinforces Bullish EuroStoxx Theme

- A bull cycle in Eurostoxx 50 futures remains intact and this week’s gains reinforce this theme. Key support lies at the 50-day EMA at 5863.24. A clear breach of this average would signal scope for a deeper retracement. Moving average studies are in a bull-mode position, highlighting a dominant uptrend. The bull trigger at 6072.00, the Jan 14 / 15 high, has been pierced. A clear break would resume the primary uptrend.

- The trend in S&P E-Minis remains bullish. The recovery from Monday’s low suggests that a recent bear threat merely resulted in a short lived correction. Attention is on key resistance and the bull trigger at 7043.00, the Jan 28 high. A break of this level would confirm a resumption of the primary uptrend and open 7080.92, a Fibonacci projection. Key support and a bear trigger has been defined at 6814.50, the Jan 21 low.

COMMODITIES: Gold Continues to Retrace Jan 29 - Feb 2 Sell Off

- A bull cycle in WTI futures remains intact. However, Monday’s impulsive sell-off continues to highlight the beginning of a corrective phase. Attention is on support at the 20-day EMA, at $61.22. The 50-day EMA lies at $59.88. A clear breach of the 50-day average would highlight a stronger reversal and open $58.53, the Jan 20 low. Key resistance and the bull trigger has been defined at $66.48, the Jan 30 high.

- Gold has recovered from Monday’s low and is retracing the Jan 29 - Feb 2 sharp sell-off. The next two resistance points to monitor are $5139.9 and $5314.0, Fibonacci retracement levels. Note that the sharp sell-off from last week’s high still highlights a potential top in the L/T trend and from a S/T perspective, marks an unwinding of the recent extreme overbought condition. A reversal lower would refocus attention on $4403.0, the Feb 2 low.

US data appearing below is as originally scheduled. Due to the partial federal government shutdown, releases from agencies including the BLS and Department of Labor are subject to change.

| Date | GMT/Local | Impact | Country | Event |

| 04/02/2026 | 1200/0700 | ** | MBA Weekly Applications Index | |

| 04/02/2026 | 1315/0815 | *** | ADP Employment Report | |

| 04/02/2026 | 1330/0830 | *** | Treasury Quarterly Refunding | |

| 04/02/2026 | 1445/0945 | *** | S&P Global Composite & Services Index (final) | |

| 04/02/2026 | 1500/1000 | *** | ISM Non-Manufacturing Index | |

| 04/02/2026 | 1500/1000 | Treasury Secretary Scott Bessent | ||

| 04/02/2026 | 1530/1030 | ** | US DOE Petroleum Supply | |

| 04/02/2026 | 1530/1030 | ** | DOE Weekly Crude Oil Stocks | |

| 04/02/2026 | 1700/1200 | Richmond Fed's Tom Barkin | ||

| 04/02/2026 | 2330/1830 | Fed Governor Lisa Cook | ||

| 05/02/2026 | 0030/1130 | ** | Trade Balance | |

| 05/02/2026 | 0700/0800 | ** | Manufacturing Orders | |

| 05/02/2026 | 0745/0845 | * | Industrial Production | |

| 05/02/2026 | 0830/0930 | ** | S&P Global Final Eurozone Construction PMI | |

| 05/02/2026 | 0900/1000 | * | Retail Sales | |

| 05/02/2026 | 0930/0930 | ** | S&P Global/CIPS Construction PMI | |

| 05/02/2026 | 1000/1100 | ** | EZ Retail Sales | |

| 05/02/2026 | 1200/1200 | *** | Bank Of England Interest Rate | |

| 05/02/2026 | 1200/1200 | *** | Bank Of England Interest Rate | |

| 05/02/2026 | 1230/1230 | BOE Press Conference | ||

| 05/02/2026 | - | European Central Bank Meeting | ||

| 05/02/2026 | 1315/1415 | *** | ECB Deposit Rate | |

| 05/02/2026 | 1315/1415 | *** | ECB Main Refi Rate | |

| 05/02/2026 | 1315/1415 | *** | ECB Marginal Lending Rate | |

| 05/02/2026 | 1330/0830 | *** | Jobless Claims | |

| 05/02/2026 | 1330/0830 | ** | WASDE Weekly Import/Export | |

| 05/02/2026 | 1345/1445 | ECB Press Conference | ||

| 05/02/2026 | 1400/1400 | *** | BOE Decision Making Panel | |

| 05/02/2026 | 1500/1000 | Treasury Secretary Scott Bessent | ||

| 05/02/2026 | 1530/1030 | ** | Natural Gas Stocks | |

| 05/02/2026 | 1550/1050 | Atlanta Fed's Raphael Bostic | ||

| 05/02/2026 | 1630/1130 | * | US Bill 08 Week Treasury Auction Result | |

| 05/02/2026 | 1630/1130 | ** | US Bill 04 Week Treasury Auction Result | |

| 05/02/2026 | 1725/1225 | BOC Governor Macklem speech in Toronto, release time TBC. | ||

| 05/02/2026 | 1900/1400 | *** | Mexico Interest Rate | |

| 06/02/2026 | 2330/0830 | ** | Household spending |