FOREX: USDJPY Recovery Extends, Dovish Riksbank Minutes Weigh on SEK

Feb-04 10:31

- USDJPY continues to grind higher on Wednesday, extending the recovery from last week’s lows to 3%. The move back above the 50-day EMA, intersecting at 155.75, undermines the recent bear theme and highlights a stronger short-term bull cycle. Price action this morning has bridged the gap to initial resistance at 156.64, the 61.8% retracement of the Jan 14 - 27 bear leg, with 157.72 the next topside level of note.

- The swift recovery has been primarily driven by a more stable backdrop for the dollar following Kevin Warsh’s nomination, while expectations for the LDP securing a majority bring concerns surrounding Japan’s fiscal trajectory back to the fore. The firmer dollar has weighed on NZD (-0.45%) after mixed Q4 unemployment has failed to reignite bullish Kiwi momentum.

- USDCNY and USDCNH saw some buying interest in European trade, with both pairs edging to new session highs of 6.9425 and 6.9404 respectively - but we note no specific headlines behind the move. News that Putin is holding a videocall with Xi Jinping unlikely to be the driver here, but moves do follow the further strength in the CNY fix Wednesday: the 6.9533 fix was again the lowest since mid-2023 but still well above expectations (survey saw today's fix at 6.9363).

- Riksbank minutes are driving SEK underperformance. The debate amongst the Board over the next few months is clearly between holding the policy rate steady (the most likely scenario) and delivering another cut (only likely if both inflation and economic activity are weaker than expected). EURSEK has advanced 0.5% to 10.58, extending a moderate bounce from yesterday’s 10.50 cycle lows. The 20-day EMA intersects at 10.6336.

- Fed's cook is scheduled to speak on monetary policy and the economy later today, and ISM services highlights the data calendar today. Focus then turns to tomorrow's ECB and BoE decisions.

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

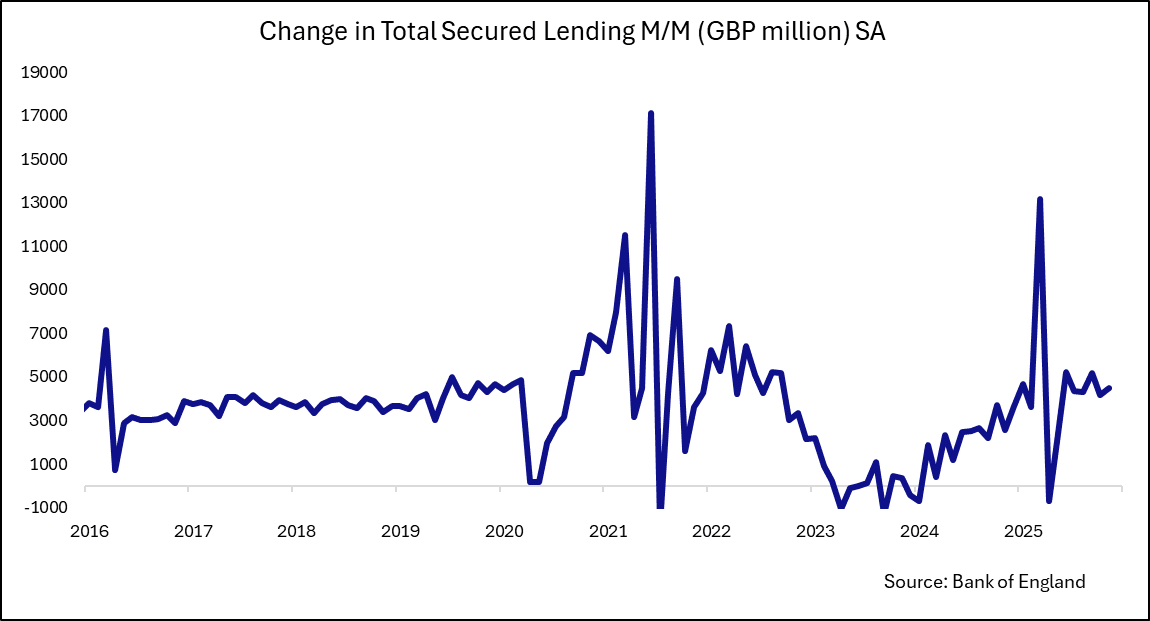

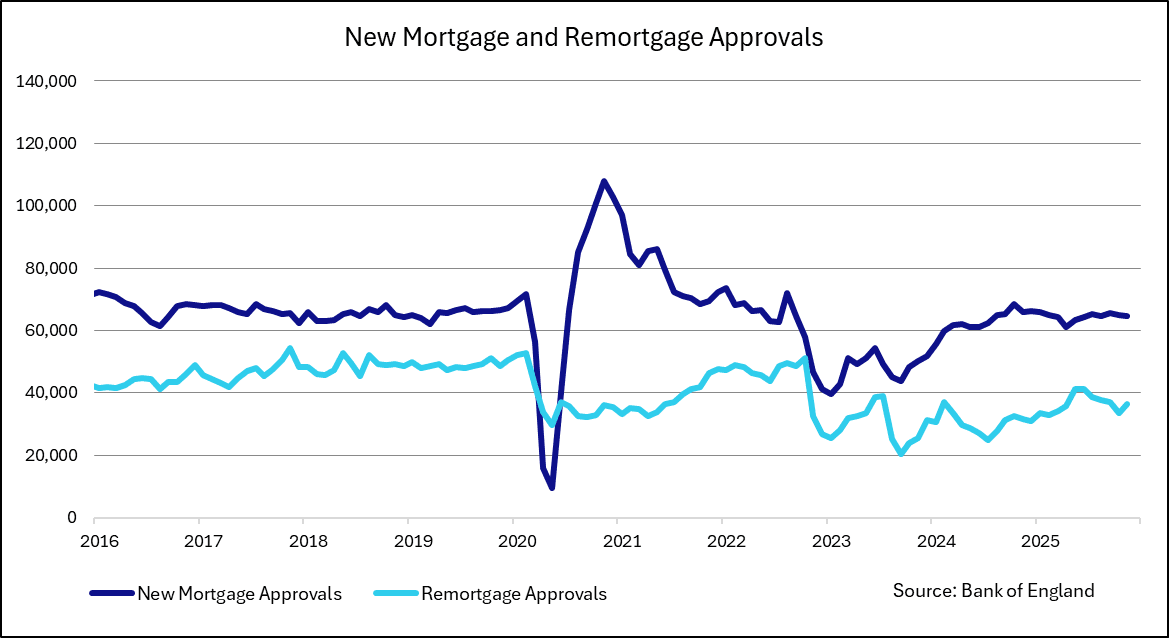

UK DATA: Lending On The Stronger Side In Nov, Mortgage Approvals In Line

Jan-05 10:30

UK net mortgage lending increased to GBP4.5bln in November, on the stronger side of expectations, while mortgage approvals again printed broadly in line with consensus and historical norms. Net consumer credit increased to GBP2.08bln, nearly 1bln above consensus. The release points to continued housing market resilience and stronger demand for consumer credit towards the end of 2025.

- Data from the BoE show net lending on dwellings increased to GBP4.49bln, above consensus of 4.1bln, after a slightly downward revised GBP4.16bln (initially 4.27bln) in October.

- New mortgage approvals came in at 64.5k, broadly in line with consensus of 64.0k, and still trending in line with the historical average.

- Both of these datapoints have shown stability since the effect of Stamp Duty-driven frontloading in March subsided, with this month's report unlikely to have fully captured any post-Budget reaction with it only coming on Nov 26.

- Within the strong net consumer credit figure, "net borrowing through credit cards was GBP1.0bln in November, up from 0.7bln in October. Net borrowing through other forms of consumer credit (such as car dealership finance and personal loans) slightly increased in November, to GBP1.1bln from 1.0bln"

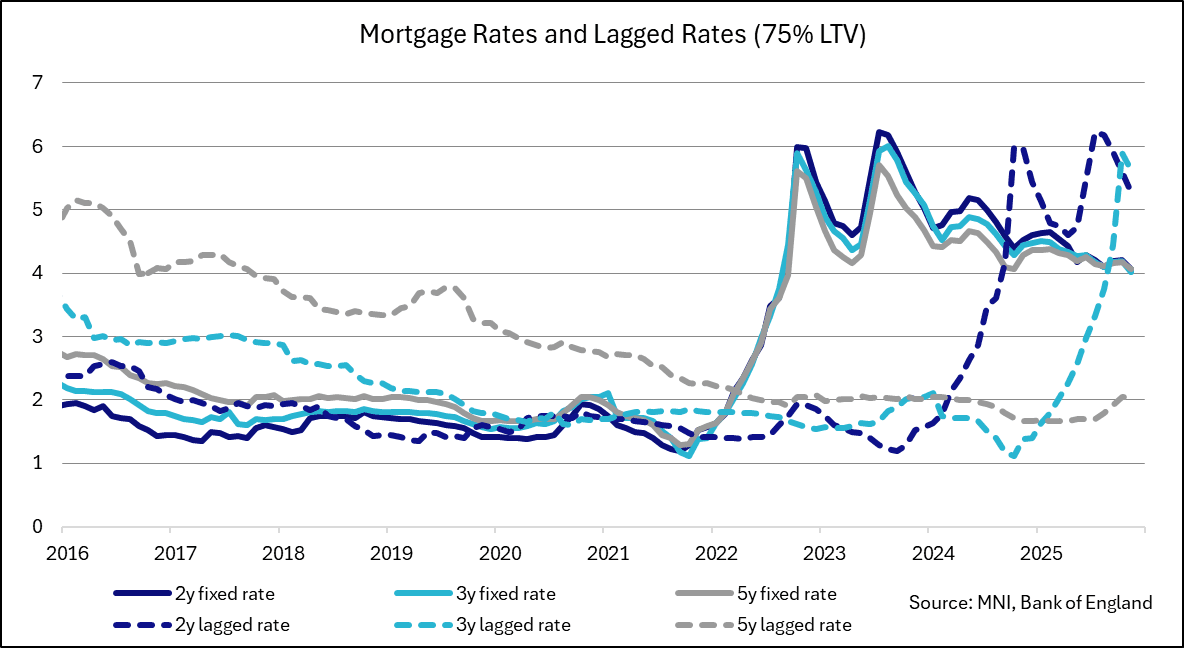

- Average mortgage rates were little changed: those remortgaging from 2-year and 3-year fixed-rate mortgages continue to see big drops to their borrowing costs in excess of 1.5ppt, while those remortgaging from a 5-year fixed rate will see a jump of around 2ppt on average.

- Also in the release, M4 money supply grew a considerable 0.8% M/M (vs -0.2% Oct) and 4.3% Y/Y (vs 3.5% Oct). The BOE notes that the net flow of sterling money (M4ex) was the highest since January 2025, at GBP15.3bln in November - "largely driven by households and non-intermediate other financial corporations increasing their holdings of money."

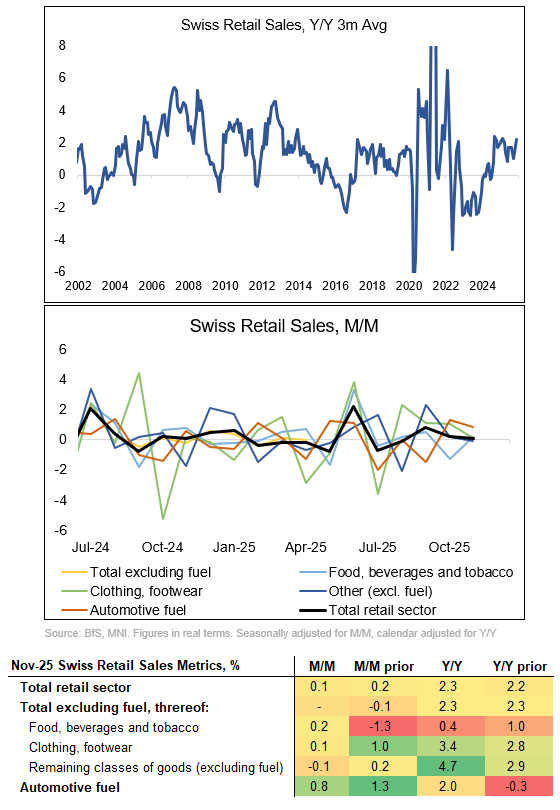

SWITZERLAND DATA: Moderate October Retail Sales

Jan-05 10:06

Retail sales data underpins the narrative that the Swiss consumer is in solid shape and, barring new shocks, the SNB is likely to hold its policy rate at 0% for the foreseeable future. The series continued Q4 growing marginally, at 0.1% M/M in November (0.2% October, revised from 0.7%).

- Looking at the drivers of the release shows limited moves within the subcategories, with auto fuel standing out positively, at 0.8% M/M (1.3% prior). However, over the last couple of months, none of the main subseries have exhibited a clear directional trend on a M/M basis.

- On a broader 3-month moving average of the Y/Y measure, Swiss retail sales picked up and grew quicker than their long term average rate, at a current 2.2% (1.4% October).

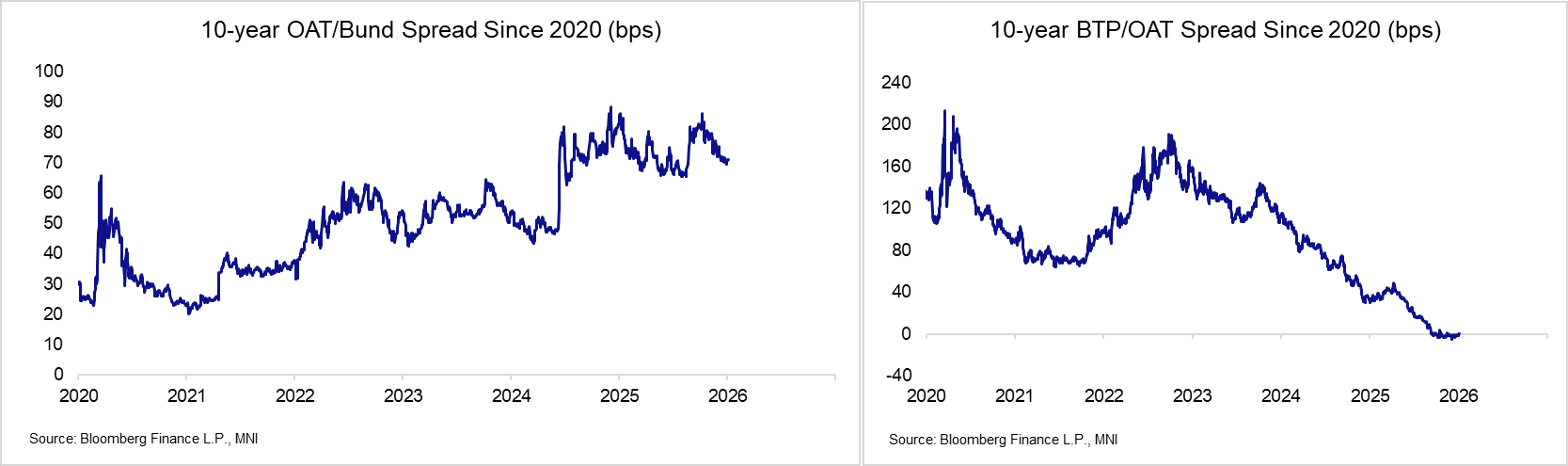

EGBS: French Political Risks Still A Focus For OAT Investors

Jan-05 10:02

- French political risks remain a focus in January, with the Government set to restart 2026 budget negotiations on Thursday. PM Lecornu will have to walk a fine line between ensuring enough fiscal restraint to get the conservative Les Republicains on board, while ensuring that the budget is not so austere that the centre-left Socialists cannot abstain (the only path for a majority in the National Assembly).

- Accordingly, the 10-year OAT/Bund spread has continued to struggle pushing below the 70bp handle in recent weeks.

- A reminder that before Christmas, the Government passed a “special law” to ensure that taxes can continue to be levied, gov't debt can be issued, and public sector workers can be paid in the absence of a state budget for 2026. This is a stop-gap solution, with the budget rollover doing little to improve France’s concerning fiscal position.

- Elsewhere, the BTP/OAT spread has struggled to deviate meaningfully from the 0bp level since October. Although relative fiscal and political backdrops may argue for lower yields in Italy compared to France, there still seems to be some hesitance amongst participants to endorse this fully. That may reflect acknowledgement that Italy is still the largest bond issuer in the Eurozone, alongside historical biases of Italy as a source of volatility and instability in the region (e.g. during the sovereign debt crisis).

Trending Top

Mar-27 20:13