MNI US MARKETS ANALYSIS - $, Yields Higher Ahead of Data Drop

Highlights:

- Strong election performance for Democrats could temper optimism for imminent end to shutdown

- USD, yields higher ahead of key private sector data prints

- Overnight GBP vols bid into close-to-call BoE decision

US TSYS: Twist Steeper With ADP, ISM Services, QRA & Shutdown Progress All Eyed

- Treasuries have pared gains to trade mildly twist steeper on decent overnight volumes ahead of a heavier docket with multiple focal points including ADP (0815ET), Treasury's QRA (0830ET) and ISM services (1000ET) – see preview links below.

- Larger gains in early Asia trade were pared with help from a report on a handful of moderate Senate Democrats considering voting to end the government shutdown whilst some colleagues to their left urge them to hold out.

- Odds of the shutdown ending sooner rather than later had improved since Monday with an acceleration in rank-and-file talks aimed at finding an offramp. However, our political risk team cautions that a strong performance in yesterday’s elections may temper optimism by validating Democrats’ assumption that voters approve of Senate Minority Leader Schumer’s hardline strategy to extract concessions on healthcare.

- Cash yields range from 1bp lower to 0.5bp higher.

- TYZ5 trades at 112-27, back to only 2 ticks higher off an overnight high of 113-02 on elevated cumulative volumes of 385k.

- That 113-02 marks new initial resistance although it needs to trade above 113-18+ (Oct 28 high) to signal a possible bullish reversal away from recent lows. Support is seen at 112-16 (Oct 30 low).

- Data: MBA mortgage applications (0700ET), ADP Oct (0815ET), S&P Global serv/comp PMI Oct final (0945ET), ISM services Oct (1000ET)

- Fedspeak: A break in scheduled appearances todayqra

- Bill issuance: US Tsy $69B 17W bill auction (1130ET)

- Politics: Trump delivers remarks at breakfast with Republican Senators (0830ET), Trump delivers remarks at America Business Forum Miami (1300ET)

- MNI QRA preview found here. It predates Monday’s borrowing estimates which were below MNI expectations and at the lower end of most estimates seen. Current quarter borrowing requirements were lowered to $569B from August's $590B estimate and the initial estimate of Jan-Mar requirements saw a slight further uptick to $578B.

- ADP mini preview: See "Private Labor Indicators To Watch Over The Next Two Days" [Nov 4]

- ISM services preview: “Oct ISM Services: Activity Steadying Out At A Weak Level (1/2)” and “Oct ISM Services: Price Gauge Seen At 4-Month Low (2/2)” [Nov 4]

STIR: Fed Rates Steady Before Important Data Updates

- Fed Funds implied rates hold yesterday’s modest decline in risk-off moves ahead of a more notable docket today with the October ADP and ISM Services reports plus any spillover to front rates from Treasury’s QRA at 0830ET.

- Dec FOMC pricing still holds nearly all of the hawkish adjustment seen after Powell noted a strongly divided committee around December cut prospects at Wednesday’s press conference.

- Cumulative cuts from 3.87% effective: 17bp Dec, 26bp Jan, 35bp Mar, 41.5bp Apr and 56bp Jun.

- SOFR futures are mostly 2 ticks higher on the day looking out to end-2027, with the terminal implied yield edging a little lower to 3.075% (H7) after Monday’s 3.115% highest close since August.

- Today sees a pause in scheduled Fedspeak before a heavy schedule tomorrow with Barr, Hammack, Musalem, Paulson, Waller and Williams.

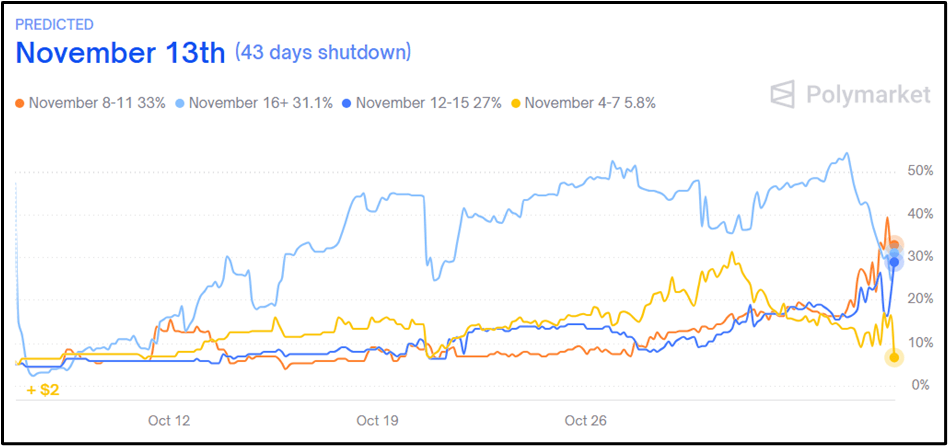

US: Strong Election Day Performance Tempers Optimism Of Shutdown Resolution

Its Day 36 of the US government shutdown, officially the longest shutdown in US history. Yesterday, the Senate rejected the House-passed November 21 funding bill for a 14th time. However, there is increased optimism of an offramp following an acceleration of bipartisan talks on an emerging deal to end the impasse, as noted in yesterday’s edition of the US Daily Brief. Punchbowl reports there are now 'more than a dozen Senate Democrats' engaging with Republicans on reopening the government. In response, the most likely end date of the shutdown has been revised down from November 29 to November 13, per Polymarket.

- However, a strong performance in yesterday’s elections may temper optimsim by validating Democrats’ assumption that voters approve of Senate Minority Leader Chuck Schumer’s (D-NY) hardline strategy to extract concessions on healthcare.

- Senator Chris Murphy (D-CT) said in a statement, “the [election] results should also give Democrats confidence that the American people have our back as we engage in the fight to protect people’s health care and save our Democracy.”

- Murphy also reposted this message from pollster Lakshya Jain: “Well, you're probably not going to see the Democrats fold on a shutdown anytime soon after tonight. No reason for them to, especially given the absolute pummeling they've just given Republicans tonight.”

- Indeed, President Trump appeared to acknowledge as such in a post on Truth Social overnight: “TRUMP WASN’T ON THE BALLOT, AND SHUTDOWN, WERE THE TWO REASONS THAT REPUBLICANS LOST ELECTIONS TONIGHT.”

At 08:30 ET 13:30 GMT, Trump will deliver remarks at a White House breakfast with Republican Senators. The event is likely to be broadcast on C-SPAN. Trump’s Truth suggests he will renew his drive for Senate Republicans to sidestep the filibuster, a move opposed by Senate Minority Leader John Thune (R-SD) and House Speaker Mike Johnson (R-LA), but supported by less institutionally-minded Republican Senators like Mike Hawley (R-MO).

- Hawley said yesterday, "feeding 42 million Americans ... [who] have to have federal food assistance to eat" [over] "defending the arcane rules of the Senate."

- Axios reports that Trump is ready to make the lives of GOP holdouts "a living hell," one adviser told us: "He will call them at three o'clock in the morning. He will blow them up in their districts. He will call them un-American. He will call them old creatures of a dying institution," the source continued.

- A long-held view is that the shutdown will only be resolved when Trump inserts himself into negotiations. If Trump fails to convince GOP Senators to back the ‘nuclear option’ to bypass the filibuster, he may look to strike a deal with Schumer on extending ACA subsidies. A pledge from Trump to hold an ACA vote would carry more weight than the shutdown offramp under discussion and would likely allow both Trump and Schumer to claim victory. Trump's Truth could be a signal he is willing to cut a deal.

Figure 1: When will the Government Shutdown End?

Source: Polymarket

CENTRAL BANK PREVIEW

MNI NORGES BANK PREVIEW: Steady Rates, Steady Guidance

Norges Bank is unanimously expected to hold the deposit rate at 4.00% on Thursday. The November decision will not be accompanied by an updated MPR or rate path projection, only a concise Monetary Policy Assessment. Norges Bank rarely makes meaningful policy rate or guidance pivots at these interim meetings, so the base case is for a short policy statement with no new signals.

MNI NBP PREVIEW: Cut on Cards After Soft CPI Print

The November meeting may be the last chance for the NBP to cut interest rates this year as an unwritten local convention dictates that the MPC sits on its hands in December. Although recent communications signalled continued vigilance amid lingering inflationary risks, another dovish CPI reading prompted a realignment of market consensus around a 25bp rate reduction. We too are inclined to think that the MPC will deliver an opportunistic cut before taking the next couple of months to reconsider its stance.

MNI BCB PREVIEW: Prolonged Pause Still Required

The Copom is widely expected to leave the Selic rate unchanged at 15.00% for a third consecutive meeting on Wednesday, as the committee maintains its hawkish stance to rein in unanchored inflation expectations. Though inflation and inflation expectations have been declining gradually, they remain above target and officials have continued to reiterate their high for longer messaging recently. Nonetheless, with activity showing some further signs of softening as well, focus will be on the forward guidance and whether there are any signals for a possible rate cut in the near future.

MNI BANXICO PREVIEW: Majority to Maintain Easing Bias

Banxico is expected to deliver another 25bp rate cut on Thursday, bringing the overnight target rate down to 7.25%. Although core inflation remains stuck above the ceiling of the 2-4% target range, the majority of the Board continues to place more emphasis on the weakness of economic activity. Nonetheless, the vote is likely to be split once again, with Deputy Governor Heath continuing to focus on the stalling of the core disinflation process. Focus will therefore remain on the forward guidance, which is likely to keep the door open to further easing ahead given the backdrop of Fed rate cuts and a resilient Mexican peso.

MNI BNM PREVIEW: BNM on Hold as Easing Cycle Ends

Growth in Malaysia remains underpinned by resilient domestic demand, strong employment and wage growth. Exports rebounded strongly in the September data, and have been surprisingly resilient for much of 2025 supported by the electronics upcycle. Malaysia has seen moderating inflation for most of this year, causing the Central Bank to reduce inflation forecast ranges. The CPI for September result of +1.5% is the first time CPI YoY has printed in line with the bottom end of the new range since the beginning of the year.

MNI CNB PREVIEW: Steady As She Goes

The Czech National Bank (CNB) remains in a holding pattern, with the current slightly restrictive monetary policy settings deemed appropriate to tackle lingering inflationary risks. With the two-week repo rate sitting at 3.50%, the upper end of the range of neutral-rate estimates, a resumption of monetary easing in this cycle hangs in the balance. We expect the Bank Board to stand pat on rates at least until the end of this year as it monitors the evolution of risks and price developments. Although the new projection may chart a slightly lower inflation path, Governor Michl is likely to reaffirm his hawkish rhetoric to signal continued resolve in the efforts to bring residual price pressures under control.

US TSY FUTURES: Long Setting In WN Dominates On Tuesday

OI data points to a mix of net long setting (TU, FV & WN) and short cover (TY, UXY & US) as Tsy futures ticked higher on Tuesday.

- There was a bias towards net long setting, with the movement in WN positioning providing the only real swing of note.

| 04-Nov-25 | 03-Nov-25 | Daily OI Change | OI DV01 Equivalent Change ($) | |

| TU | 4,622,213 | 4,596,654 | +25,559 | +995,257 |

| FV | 6,816,873 | 6,796,041 | +20,832 | +910,609 |

| TY | 5,434,597 | 5,445,139 | -10,542 | -715,395 |

| UXY | 2,470,454 | 2,472,105 | -1,651 | -150,249 |

| US | 1,883,365 | 1,888,998 | -5,633 | -729,410 |

| WN | 2,144,627 | 2,133,029 | +11,598 | +2,214,520 |

| Total | +40,163 | +2,525,333 |

SOFR: Long Setting Dominates In Futures On Tuesday

OI data points to net long setting dominating across all 16 of the front SOFR futures during Tuesday's uptick.

| 04-Nov-25 | 03-Nov-25 | Daily OI Change |

| Daily OI Change In Packs |

SFRU5 | 1,395,212 | 1,376,441 | +18,771 | Whites | +59,985 |

SFRZ5 | 1,496,677 | 1,478,664 | +18,013 | Reds | +58,953 |

SFRH6 | 1,184,917 | 1,169,253 | +15,664 | Greens | +31,798 |

SFRM6 | 1,091,053 | 1,083,516 | +7,537 | Blues | +17,502 |

SFRU6 | 1,082,442 | 1,080,514 | +1,928 |

|

|

SFRZ6 | 1,191,488 | 1,151,515 | +39,973 |

|

|

SFRH7 | 820,965 | 813,814 | +7,151 |

|

|

SFRM7 | 774,774 | 764,873 | +9,901 |

|

|

SFRU7 | 754,318 | 739,221 | +15,097 |

|

|

SFRZ7 | 794,382 | 792,984 | +1,398 |

|

|

SFRH8 | 417,753 | 406,551 | +11,202 |

|

|

SFRM8 | 403,866 | 399,765 | +4,101 |

|

|

SFRU8 | 332,770 | 325,731 | +7,039 |

|

|

SFRZ8 | 323,745 | 319,392 | +4,353 |

|

|

SFRH9 | 206,030 | 204,373 | +1,657 |

|

|

SFRM9 | 188,417 | 183,964 | +4,453 |

|

|

EUROPE ISSUANCE UPDATE

ITALY: Results of today's E5bln buyback via Banca d'Italia. MEF purchased:

- E1.067bln of 3.20% Jan-26 BTP Short Term (ISIN: IT0005584302) at price 100.206.

- E0.607bln of 4.50% Mar-26 BTP (ISIN: IT0004644735) at price 100.746.

- E0.978bln of 3.80% Apr-26 BTP (ISIN: IT0005538597) at price 100.724

- E0.560bln of 2.10% Jul-26 BTP (ISIN: IT0005370306) at price 100.045.

- E0.910bln of 3.85% Sep-26 BTP (ISIN: IT0005556011) at price 101.463

- E0.878bln of 0.50% Apr-26 CCTeu (ISIN: IT0005428617) at price 100.241.

GERMANY: 15-year Bund results:

- E1bln (E846mln allotted) of the 2.60% May-41 Bund. Avg yield 3.02% (bid-to-offer 2.89x; bid-to-cover 3.41x).

- E1bln (E800mln allotted) of the 2.50% Jul-44 Bund. Avg yield 3.09% (bid-to-offer 1.41x; bid-to-cover 1.77x).

FOREX: USD Remains on Front-Foot, DXY Testing August Highs

- After some moderate weakness during the APAC session, the US dollar has reversed back to recovery highs, keeping the post-FOMC topside momentum firmly intact. Gains today for the DXY would represent a sixth consecutive winning session, as the index currently flirts with the August highs, a break of which would represent 5-month highs.

- The most notable price action overnight was for USDJPY, which had a sharp selloff to 152.96, as the risk off sentiment across global markets initially extended. Assisting the yen rally was the BOJ minutes, where one board member, apart from the two dissenters, said it was time to consider another hike. Subsequently, risk stabilised and provided a more supportive tone for USDJPY, which has risen to a session high of 153.84 ahead of the NY crossover.

- In line with the broader greenback advance, USDCAD is also on a 5-session winning streak, currently trading at 6-month highs. Canada yesterday budgeted its biggest ever cash deficit this fiscal year, excluding the pandemic, on a fiscal push to revitalize sluggish growth in the country. This week’s extension of USDCAD highlights a clear reversal of the corrective bear leg between Oct 14 - 29. Spot is currently testing 1.4136, the top of a bull channel drawn from the Jul 23 low. Above here, 1.4167 is the next level of note, the 50.0% retracement of the Feb 3 - Jun 16 bear leg.

- GBPUSD remains in focus following its pronounced downtrend since mid-September. The pair remains close to cycle lows today as markets digest Chancellor Reeves’ speech on Tuesday hinting at tax increases, and await tomorrow's BoE MPC decision, set to be a close decision between a hold and a 25bp cut. Following the break of 1.3041, sights are on 1.2971 next, a Fibonacci projection point. Note that the trend is in oversold territory and a recovery would allow this condition to unwind. Initial resistance is at 1.3142, the Aug 1 low.

- ISM services highlights today's data calendar. A set of ECB speakers including Schnabel are scheduled over the next couple of days, while we will also hear from SNB's Tschudin today.

US: Yields, USD Edge Higher as WaPo Report on Move to End Shutdown

Washington Post report that "A handful of moderate Senate Democrats are considering voting to end what has now become the country's longest government shutdown, splitting the caucus as some colleagues to their left urge them to hold out. [...] A bipartisan group of senators is working to craft a deal in which Congress would pass three full-year appropriations bills to fund some agencies, along with a short-term bill that would reopen the rest of the government, according to four people familiar with the talks"

- US 10y yields inch to new daily highs on the back of that Washington Post story - testing 4.09%. In tandem, USDJPY edges higher, briefly printing 153.84. We note that much of that plan had emerged late yesterday - and while the move to end the shutdown is clearly gaining traction, it is still well short of any firm resolution in the very near-term.

- Core global FI markets tick lower, with TY, Bund and gilt futures to fresh session lows, but remain comfortably within week-to-date ranges given uncertainty whether a deal will ultimately be struck.

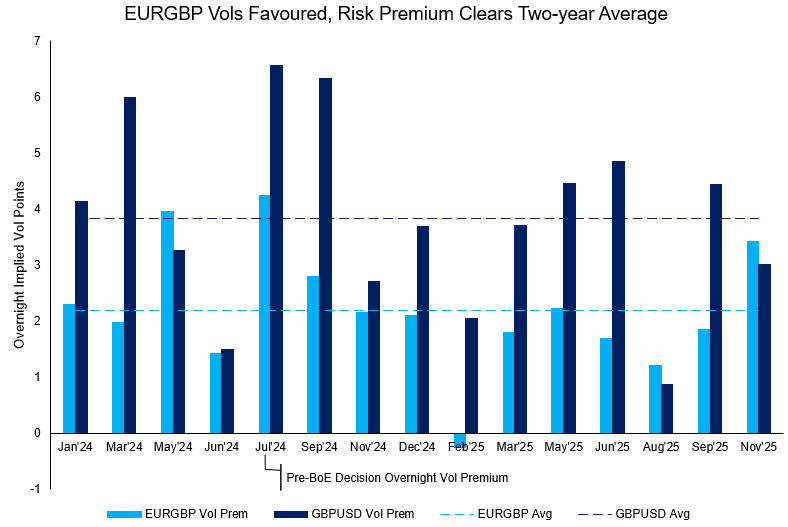

GBP: Vol Markets See More Interest in EURGBP Over GBPUSD into BoE

Markets are buying overnight GBP vol into tomorrow's BoE decision - which we see as a closer to 50/50 chance of cut vs. a hold - and therefore much more finely balanced than the ~7bps of cuts currently priced. Much of the buying interest has been via EURGBP rather than GBPUSD, with the cross a more popular expression for GBP weakness among the sell-side since the summer.

EURGBP markets added close to 3.5 points in overnight vol premium this morning, not far off double the pre-BoE decision average posted over the past two years. This doubles the break-even on an overnight straddle in the cross to +/- 35pips. In contrast, overnight GBPUSD vols have added 3.0 points - well shy of average and bucking the trend of 2025 so far.

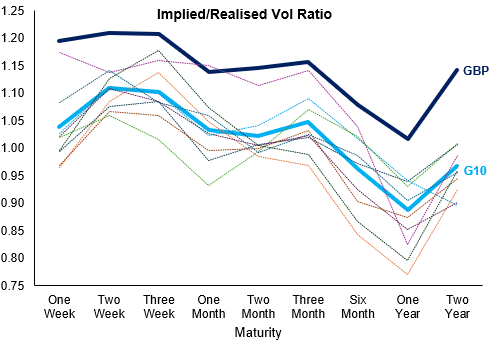

We noted yesterday that even beyond the Budget, markets see GBP remaining structurally volatile into 2026 - in excess of all other currencies in G10: For several months, implied vol contracts capturing the November 26th Budget have been trading at a premium relative to the rest of the curve. However, the ratio between implied/realised vol for maturities covering the end of the year and well into 2026 is well elevated relative to G10 peers, suggesting a persistent and sizeable GBP risk premium even beyond Reeves' next fiscal event:

Note: Dark blue line denotes GBP implied/realised vol ratio across all maturities out to two years. Light blue line is the G10 mean average, while pale dotted lines are respective G10 currencies.

Source: MNI/Bloomberg Finance L.P.

OPTIONS: Expiries for Nov5 NY cut 1000ET (Source DTCC)

- EUR/USD: $1.1525(E630mln), $1.1600-20(E1.4bln)

- EUR/GBP: Gbp0.8745(Gbp753mln)

- USD/JPY: Y153.35-50($905mln)

- NZD/USD: $0.5650(N$1.2bln), $0.5675(N$1.2bln)

FOREX: USDCAD Extending Winning Streak, Testing Top of Bull Channel

- In line with the broader greenback advance since the FOMC, USDCAD is also on a 5-session winning streak, currently trading at the highest level since April 09. Yesterday, we highlighted that the pair had breached 1.4080, the Oct 16 high, to confirm a resumption of the uptrend.

- Topside momentum has gained traction, with domestic developments assisting the move above 1.41. Canada yesterday budgeted its biggest ever cash deficit this fiscal year, excluding the pandemic, on a fiscal push to revitalize sluggish growth in the country.

- This week’s extension for USDCAD highlights a clear reversal of the corrective bear leg between Oct 14 - 29. Spot is currently testing 1.4136, the top of a bull channel drawn from the Jul 23 low. 1.4167 is the next level of note, the 50.0% retracement of the Feb 3 - Jun 16 bear leg, and above here, attention will be on 1.4274, the April 09 high.

- Final services PMI data will be released later today, however, it’s the October employment data that will be the focus on the Canadian data calendar, set to be a cleaner release given the lack of accompanying US figures. Currently a -5k change in employment is expected, with the unemployment rate seen remaining steady - further increases from the current 7.1% could fuel dovish bets.

EQUITIES: E-Mini S&P Remains Above Key Pivot Support at 50-Day EMA

- Recent weakness in Eurostoxx 50 futures appears to have been corrective. The contract has found support ahead of the 50-day EMA, at 5571.03. Support below the EMA lies at 5555.00, the base of a bull channel drawn from the Aug 1 low. A breach of this level and the 50-day EMA, is required to highlight a stronger reversal. Sights are on resistance and the bull trigger at 5742.00, the Oct 29 high.

- The trend condition in S&P E-Minis is unchanged, it remains bullish and the latest pullback appears corrective. Support at the 20-day EMA, at 6803.81, has been breached. A clear break of this average signals scope for a deeper retracement and exposes the 50-day EMA at 6702.18 - a key pivot support. The bull trigger has been defined at 6953.75, the Oct 30 high. Clearance of this hurdle would confirm a resumption of the uptrend.

COMMODITIES: Gold Off Week's Lows, But Shy of Initial Resistance at $4161.40

- WTI futures are unchanged and the contract remains in a corrective cycle for now. Note that price has recently traded through the 50-day EMA, currently at $61.03. The breach of this EMA signals scope for a stronger recovery. Note too that a resistance at $62.34, the Oct 8 high, has also been pierced. A clear move through it would expose key resistance at $65.77, the Sep 26 high. First key support and the bear trigger is unchanged at $55.96, the Oct 20 low.

- A fresh cycle low last week in Gold highlights an extension of the bear cycle that started Oct 20. The retracement since Oct 20 has allowed an overbought trend condition to unwind. The 20-day EMA has been breached, signalling scope for a test of the 50-day EMA, at $3867.3. Clearance of this EMA would strengthen a short-term bear theme. Initial resistance is at $4161.4, the Oct 22 high.

| Date | GMT/Local | Impact | Country | Event |

| 05/11/2025 | 1200/0700 | ** | MBA Weekly Applications Index | |

| 05/11/2025 | 1315/0815 | *** | ADP Employment Report | |

| 05/11/2025 | 1330/0830 | *** | Treasury Quarterly Refunding | |

| 05/11/2025 | 1445/0945 | *** | S&P Global Services Index (final) | |

| 05/11/2025 | 1445/0945 | *** | S&P Global US Final Composite PMI | |

| 05/11/2025 | 1500/1000 | *** | ISM Non-Manufacturing Index | |

| 05/11/2025 | 1530/1030 | ** | DOE Weekly Crude Oil Stocks | |

| 05/11/2025 | 1530/1030 | ** | US DOE Petroleum Supply | |

| 05/11/2025 | 1610/1610 | BOE Breeden At SALT Blockchain Event | ||

| 06/11/2025 | 2330/0830 | ** | average wages (p) | |

| 06/11/2025 | - | NorgesBank Meeting | ||

| 06/11/2025 | 0030/0930 | ** | S&P Global Final Japan Services PMI | |

| 06/11/2025 | 0030/0930 | ** | S&P Global Final Japan Composite PMI | |

| 06/11/2025 | 0030/1130 | ** | Trade Balance | |

| 06/11/2025 | 0700/0800 | ** | Industrial Production | |

| 06/11/2025 | 0700/0800 | *** | Flash Inflation Report | |

| 06/11/2025 | 0700/0800 | *** | Flash Inflation Report | |

| 06/11/2025 | 0800/0900 | ** | Industrial Production | |

| 06/11/2025 | 0800/0900 | ** | Unemployment | |

| 06/11/2025 | 0810/0910 | ECB Schnabel At ECB Money Market Conference | ||

| 06/11/2025 | 0830/0930 | ** | S&P Global Final Eurozone Construction PMI | |

| 06/11/2025 | 0830/0930 | ECB De Guindos On Natixis Webinar | ||

| 06/11/2025 | 0900/1000 | *** | Norges Bank Rate Decision | |

| 06/11/2025 | 0930/0930 | ** | S&P Global/CIPS Construction PMI | |

| 06/11/2025 | 1000/1100 | ** | EZ Retail Sales | |

| 06/11/2025 | 1200/1200 | *** | Bank Of England Interest Rate | |

| 06/11/2025 | 1200/1200 | *** | Bank Of England Interest Rate | |

| 06/11/2025 | 1230/1230 | BOE Press Conference | ||

| 06/11/2025 | 1330/0830 | *** | Jobless Claims | |

| 06/11/2025 | 1330/0830 | ** | WASDE Weekly Import/Export | |

| 06/11/2025 | 1330/0830 | ** | Preliminary Non-Farm Productivity | |

| 06/11/2025 | 1400/1400 | Decision Maker Panel Data | ||

| 06/11/2025 | 1500/1000 | * | Ivey PMI | |

| 06/11/2025 | 1500/1000 | ** | Wholesale Trade | |

| 06/11/2025 | 1500/1000 | ** | Wholesale Trade | |

| 06/11/2025 | 1530/1030 | ** | Natural Gas Stocks | |

| 06/11/2025 | 1530/1030 | BOC Governor Macklem testifies at Senate. | ||

| 06/11/2025 | 1600/1100 | NY Fed's John Williams | ||

| 06/11/2025 | 1600/1100 | Fed Governor Michael Barr | ||

| 06/11/2025 | 1630/1130 | * | US Bill 08 Week Treasury Auction Result | |

| 06/11/2025 | 1630/1130 | ** | US Bill 04 Week Treasury Auction Result | |

| 06/11/2025 | 1700/1200 | Cleveland Fed's Beth Hammack | ||

| 06/11/2025 | 1830/1930 | ECB Lane At IMF Conference | ||

| 06/11/2025 | 1900/1400 | *** | Mexico Interest Rate | |

| 06/11/2025 | 2030/1530 | Fed Governor Christopher Waller | ||

| 06/11/2025 | 2130/1630 | Philly Fed's Anna Paulson | ||

| 06/11/2025 | 2230/1730 | St. Louis Fed's Alberto Musalem | ||

| 07/11/2025 | 2330/0830 | ** | Household spending |