FOREX: USD Remains on Front-Foot, DXY Testing August Highs

Nov-05 10:34

- After some moderate weakness during the APAC session, the US dollar has reversed back to recovery highs, keeping the post-FOMC topside momentum firmly intact. Gains today for the DXY would represent a sixth consecutive winning session, as the index currently flirts with the August highs, a break of which would represent 5-month highs.

- The most notable price action overnight was for USDJPY, which had a sharp selloff to 152.96, as the risk off sentiment across global markets initially extended. Assisting the yen rally was the BOJ minutes, where one board member, apart from the two dissenters, said it was time to consider another hike. Subsequently, risk stabilised and provided a more supportive tone for USDJPY, which has risen to a session high of 153.84 ahead of the NY crossover.

- In line with the broader greenback advance, USDCAD is also on a 5-session winning streak, currently trading at 6-month highs. Canada yesterday budgeted its biggest ever cash deficit this fiscal year, excluding the pandemic, on a fiscal push to revitalize sluggish growth in the country. This week’s extension of USDCAD highlights a clear reversal of the corrective bear leg between Oct 14 - 29. Spot is currently testing 1.4136, the top of a bull channel drawn from the Jul 23 low. Above here, 1.4167 is the next level of note, the 50.0% retracement of the Feb 3 - Jun 16 bear leg.

- GBPUSD remains in focus following its pronounced downtrend since mid-September. The pair remains close to cycle lows today as markets digest Chancellor Reeves’ speech on Tuesday hinting at tax increases, and await tomorrow's BoE MPC decision, set to be a close decision between a hold and a 25bp cut. Following the break of 1.3041, sights are on 1.2971 next, a Fibonacci projection point. Note that the trend is in oversold territory and a recovery would allow this condition to unwind. Initial resistance is at 1.3142, the Aug 1 low.

- ISM services highlights today's data calendar. A set of ECB speakers including Schnabel are scheduled over the next couple of days, while we will also hear from SNB's Tschudin today.

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

JPY: Most But Not All Analysts See No Material USDJPY Upside Beyond 150

Oct-06 10:29

Most but not all analysts seen by MNI tend to remain on the cautious side towards further material gains in USDJPY from current levels, while most larger volume options transactions in USDJPY have been skewed towards call structures with strikes in 151-155.00 region.

- Deutsche Bank: "We went long JPY in our FX Blueprint but are now getting out following the LDP election outcome this weekend. Sanae Takaichi’s surprise victory reintroduces too much uncertainty around Japan’s policy priorities and the timing of the BoJ hiking cycle. There is agreement that inflation is a problem in Japan, but uncertainty is now going up again on how it will be dealt with. […] Our base case is for near-term losses in the JPY towards 150 as the market adjusts to the surprise, but not material weakness beyond."

- Goldman Sachs: "Elevated two-way risk [after market open] as markets assess the likely policy path ahead. [...] expect only modest changes to the fiscal stance and no change to our modal path for the BoJ. This argues that much of the new fiscal risk premium should fade […] For some time, we have been making the case that global risk sentiment should be more important than domestic developments for the direction of the Yen, and that is still the case. However, it seems likely that domestic developments will add another headwind to Yen performance. We see upside risks to our USD/JPY forecasts and are closing our trade recommendation to go short USD/JPY (initiated at 147.69)."

- ING: "We don’t see much more upside room for USD/JPY from here. A much weaker yen stands to add to Japan’s cost of living concerns; the rally in USD/JPY could cause friction with Washington, and the yen may still be preferred should the US government shutdown last longer. Our base case is that this break above 150.0 is temporary, rather than the start of a more sustained rally in USD/JPY."

- JP Morgan: "Takaichi, who positions countermeasures against rising prices as her top economic policy priority, is not expected to welcome yen depreciation that accelerates domestic inflation further, and is unlikely to stand in the way of rate hikes to curb it. […] The long-standing view – that both the Japanese and US governments do not desire a significant rise in USD/JPY; if USD/JPY rises well above 150 yen, some form of policy response will cap further gains – remains unchanged."

- MUFG: "The combination of heightened fiscal risks in Japan and risk of delayed or even derailed BoJ rate hike plans will continue to encourage a weaker yen in the near-term unless evidence emerges that those initial policy expectations will not be realized. It may even open the door to a retest of the year to date highs for USD/JPY"

- SEB: "Is the JPY carry trade set for a comeback? The potential for a more dovish BoJ revives interest in the JPY carry trade as market volatility, especially at the short end, remains subdued. However, unlike before the August 2024 unwind, major central banks are now further into easing cycles. Although some emerging market currencies like BRL offer high carry, they entail much greater risk and volatility than G10 pairs. Thus, there may be some interest to reenter the yen carry trade, but the current setup remains less favorable than before."

JPY: Where next for JPY?

Oct-06 10:29

- USDJPY consolidates above the 150.00 handle on elevated volumes (Z5 JPY futures have printed more than double their average volume for this time of day) as markets digest the unexpected victory for fiscal dove Takaichi at the LDP leadership contest, and the spillover impacts on reduced pricing for the BoJ's October meeting.

- From a technical perspective, the USDJPY breach of key short-term resistance at 149.96 paves the way for a test of the key medium-term resistance at 150.92, the Aug 1 high. A break of this hurdle would confirm a resumption of the bull leg that started Apr 22. Today’s intraday low at 149.05 is the first support.

- EURJPY meanwhile has faded off alltime highs on French PM Lecornu's resignation. EMAs in EURJPY continue to point to the upside, clearance of 175.13 resistance confirmed a resumption of the primary uptrend opens the 177.00 handle next. On the downside, key short-term support has been defined at 172.27, the Oct 2 low.

- Conversely, Takaichi moderated her firmer views on the BoJ during the campaign trail, and stressed the responsible approach to spending her government would adopt. As a result, JPY weakness could prove limited beyond today's moves, in which case 149.56 and 148.54 mark intraday supports before 147.47 would close the Takaichi gap.

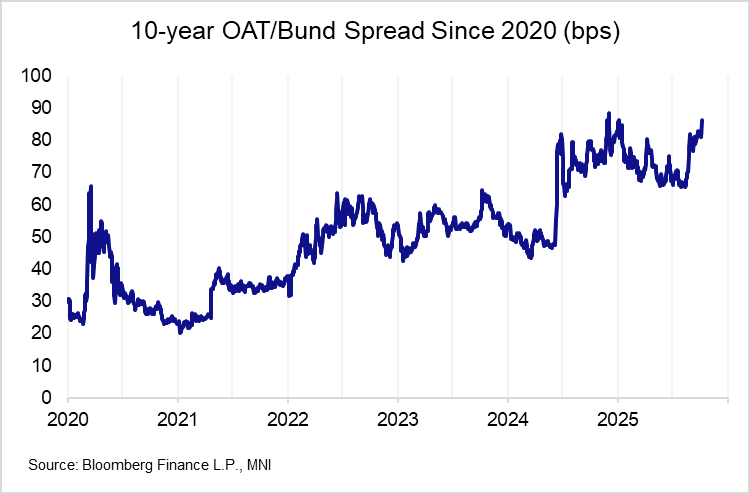

OAT: OAT/Bund Spread Consolidates Around 86bps; Analysts Flag '25 Election Risk

Oct-06 10:27

- After widening to a knee-jerk high of 89bps following PM Lecornu’s resignation, the 10-year OAT/Bund spread has consolidated around 86bps. While the timing of Lecornu’s resignation came as a surprise, intraday widening has been limited by the fact Lecornu’s prospects of passing a 2026 budget were appearing bleak from the onset. Lecornu’s resignation today may have just delayed the inevitable.

- Today’s moves in spreads can be classed as orderly and reflective of fundamentals (i.e. political/fiscal risk premium). That should dispel any fresh speculation around the use of the ECB’s TPI – something almost all Governing Council members have strongly pushed back on in recent months.

- In an interview with the MNI Policy Team, a Greek treasury source noted that “investors don't doubt that the ECB or the EU would step in the case of an unwarranted dysfunction in European sovereign debt markets.”. While not an immediate concern right now, this implicit backstop may also contain blowout episodes in spreads without requiring a formal triggering of the TPI.

- Sellside views following Lecornu’s resignation highlight the challenges facing France. Some note that fresh legislative elections may come as soon as this year:

- Barclays: Macron has two main options: "appointing a new Prime Minister or dissolving the National Assembly. Even if President Macron chooses the former, we now think that early legislative elections are the baseline before year-end."

- Commerzbank: “After two centrist politicians have failed in quick succession, the choice is likely to fall on a moderate right-wing politician or a left-wing politician. The latter is the more likely scenario”…“a prime minister from the left-wing camp is likely to focus on higher taxes in the budget dispute and intensify conflicts with Macron's camp”…“ there are no signs of a resolution to the political deadlock, and a consensus on ambitious reforms of public finances remains a long way off.”

- Berenberg: “This further increases the risk that France's fiscal troubles will remain unresolved and that economic policies will become less growth-friendly. It adds to the risk that France may be heading for new parliamentary elections in late 2025 or early 2026.”