MNI US MARKETS ANALYSIS - Data Timing in Focus as Gov Reopens

Highlights:

- On watch for advisories, data scheduling as government shifts to reopen mode

- Pricing for the Fed's December meeting shifts to 50/50 split between cut and hold

- Australian jobs grow at twice the pace expected, helping AUD reverse bearish trend pattern

US TSYS: Bear Flatter With The Government Open Again, Data Schedules Watched For

- Treasuries have pushed lower with US desks filtering in, extending overnight losses and with bear flattening in play possibly related to positioning unwinds following the re-opening of the government.

- Today see 30Y supply and we suspect only state-level claims data in the afternoon but we can't completely rule out a national print at 0830ET.

- There will be additional focus on whether we receive any updates around data release schedules, although we note that the BLS only published its revised schedule at 1630ET on the first day of re-opening in 2013 after what was a much shorter shutdown.

- Cash yields are 1-2.5bp higher, with declines led by 3s.

- 5s30s at 98bps is only back to Nov 6 levels.

- TYZ5 trades at 112-27 (-05) on reasonable cumulative volumes of 330k.

- Yesterday saw 113-02+ in a probe of a key near-term resistance at 113-02 (Nov 5 & 7 joint highs), after which lies 113-18+ (Oct 28 high).

- Data: Outside chance of national-level jobless claims released at 0830ET but not our baseline (although state-level details released at ~1700ET), Chicago Fed CARTS retail sales estimate (0830ET), Dallas Fed weekly economic index (1130ET)

- Fedspeak: Daly on balance sheet management (0800ET), Kashkari opening remarks (1030ET), Musalem in fireside chat on mon pol (1215ET, hawk), Hammack in fireside chat (1220ET, hawk)

- Coupon issuance: US Tsy $25bn 30Y - 912810UP1 (1300ET)

- Bill issuance: US Tsy $110bn 4-Week Bills, $95bn 8-Week Bills (1130ET)

- Politics: Trump participates in executive order signing (1400ET)

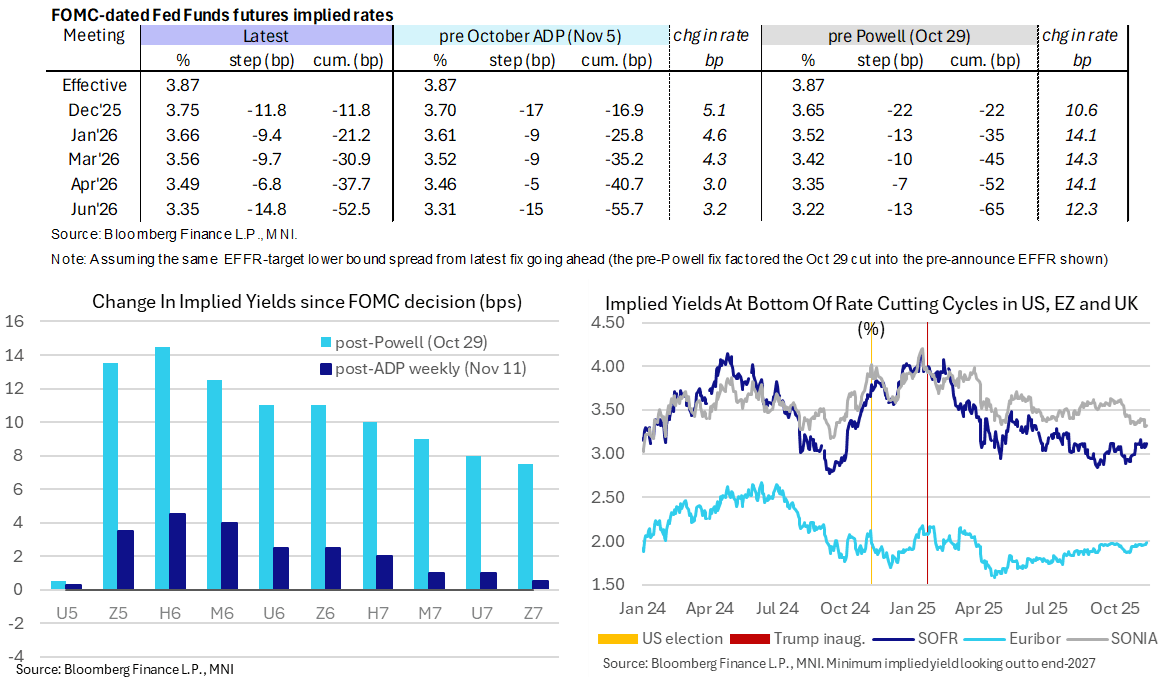

STIR: Fed December Cut Shifts To 50/50 Call

- US rates have seen a concerted hawkish shift overnight, gaining momentum again in recent trade as US desks filter in and concentrated in the front end with a cut next month now seen as a 50/50 call.

- It extends moves seen late yesterday. Initial timing coincided with NY Fed SOMA Manager Perli yesterday saying the Fed “won’t have to wait long” before purchasing assets. However, that’s difficult to square away as it broadly chimed with implications from NY Fed’s Williams earlier in the day along with other recent commentary from FOMC members including Powell re reserves having shifted close to ample.

- The front-end focused nature of the shift sees some question marks over pinning it on the government re-opening (i.e. having dodged any last-minute hiccups from the House), although it could still be a positioning unwind related to this.

- Fed Funds implied rates are 2.5-3.5bp higher on the day for meetings out to mid-2026.

- Cumulative cuts from an assumed 3.87% effective: 12bp Dec, 21bp Jan, 31bp Mar, 38bp Apr, 52.5bp Jun.

- SOFR futures are -0.05 in the SFRH6 through to -0.025/-0.030 in 2027 contracts.

- It sees the terminal implied yield rise to 3.115% (SFRH7, +3bp), +5bp from Tuesday’s close having digested the soft weekly ADP print but still off the multi-month high close of 3.16% from last Wednesday after more encouraging monthly ADP and especially ISM Services data.

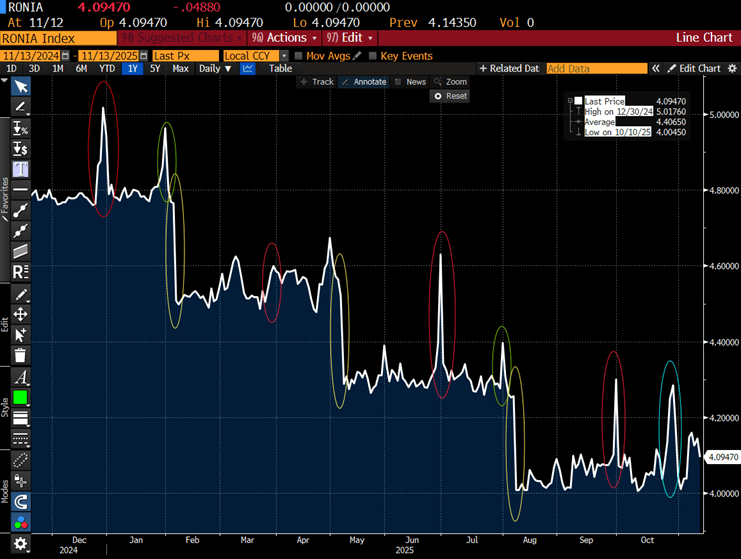

STIR: MNI Market Analysis: UK Funding: Gilt Demand Impacts

- We have focused a lot on the supply-side impacting UK funding markets and we draw together some of our recent coverage on that topic in this document. However, we also look at the demand side of the equation and an increase in long gilt positioning may also have been a contributing factor to the most recent increase in funding costs and RONIA.

- We think that some of the moves higher in repo funding costs will potentially have been due to the market buying gilts (particularly to establish new long positions). Hedge funds in particular use repo to held fund long gilt positions.

- Therefore as long gilt positions are established if these are funded using repo, demand for repo increases. Higher demand for repo will increase the interest rates applicable.

RONIA Spikes and Event Drivers

Ovals denote: Red: Quarter-end. Yellow: Bank Rate cut. Green: APF gilt redemption. Blue: TFSME repayment

Source: MNI, Bloomberg Finance L.P.

- Last week, the extent of the demand for repo funding may not have been clear at the time market participants were bidding in the STR (given that gilt positions may have been established during or after the bidding window for the operation closed). It may also be to some extent that market participants do not attempt to anticipate repo rate increases when deciding on their STR demand, and rather only react to higher repo rates after a clear market signal.

- Given the significance of the MPC meeting last week, it may also been that there wasn’t clear sight across the market as to the extent of additional demand to go long gilts and to fund this via repo, too.

- There is no real way of really proving our hypothesis that increased demand for gilts was a contributing factor to the increase in RONIA seen last Thursday. But it does add even more focus to today’s STR operation (results due at 10:40GMT).

- The other consideration when looking at today’s STR operation will be usage of the ILTR operation. On Tuesday gross takeup in the operation was GBP6.073bln, leading to a net increase of GBP5.518bln (the third highest net increase on record – the highest being the week of the first Covid lockdown and the second highest two weeks ago aligned with peak TFSME repayments).

- See the full MNI Analysis piece for more details.

US TSY FUTURES: Mix Of Positioning Swings Seen Wednesday

OI data points to a mix of net long cover (TU & FV), short setting (TY), long setting (UXY & WN) and short cover (US) as the curve twist flattened on Wednesday. Net curve-wide OI was essentially flat.

| 12-Nov-25 | 11-Nov-25 | Daily OI Change | OI DV01 Equivalent Change ($) |

TU | 4,618,317 | 4,642,706 | -24,389 | -911,919 |

FV | 6,914,254 | 6,923,883 | -9,629 | -412,730 |

TY | 5,457,818 | 5,428,925 | +28,893 | +1,933,808 |

UXY | 2,506,215 | 2,499,661 | +6,554 | +589,940 |

US | 1,847,948 | 1,853,953 | -6,005 | -768,049 |

WN | 2,174,869 | 2,170,409 | +4,460 | +839,466 |

|

| Total | -116 | +1,270,514 |

SOFR: Short Setting Dominated In Futures On Wednesday

OI data suggests that net short setting dominated in SOFR futures on Wednesday, with only limited instances of net long cover seen.

| 12-Nov-25 | 11-Nov-25 | Daily OI Change |

| Daily OI Change In Packs |

SFRU5 | 1,370,925 | 1,361,512 | +9,413 | Whites | +46,488 |

SFRZ5 | 1,429,349 | 1,408,475 | +20,874 | Reds | +22,120 |

SFRH6 | 1,221,710 | 1,207,200 | +14,510 | Greens | +16,275 |

SFRM6 | 1,102,575 | 1,100,884 | +1,691 | Blues | +10,643 |

SFRU6 | 1,116,654 | 1,111,204 | +5,450 |

|

|

SFRZ6 | 1,194,321 | 1,194,474 | -153 |

|

|

SFRH7 | 853,770 | 829,462 | +24,308 |

|

|

SFRM7 | 812,801 | 820,286 | -7,485 |

|

|

SFRU7 | 770,747 | 764,561 | +6,186 |

|

|

SFRZ7 | 809,953 | 806,649 | +3,304 |

|

|

SFRH8 | 434,548 | 430,410 | +4,138 |

|

|

SFRM8 | 410,586 | 407,939 | +2,647 |

|

|

SFRU8 | 351,207 | 351,772 | -565 |

|

|

SFRZ8 | 334,958 | 330,459 | +4,499 |

|

|

SFRH9 | 206,269 | 202,051 | +4,218 |

|

|

SFRM9 | 189,589 | 187,098 | +2,491 |

|

|

EUROPE ISSUANCE UPDATE

Italy auction results:

- E3.5bln of the 2.35% Jan-29 BTP. Avg yield 2.38% (bid-to-cover 1.46x).

- E1.5bln of the 3.25% Jul-32 BTP. Avg yield 2.95% (bid-to-cover 1.78x).

- E1.5bln of the 3.25% Nov-32 BTP. Avg yield 3% (bid-to-cover 1.69x).

- E1.5bln of the 4.65% Oct-55 BTP. Avg yield 4.3% (bid-to-cover 1.56x).

FOREX: USD Fade Leads EURUSD Pierce Above 50day-EMA

- The fade in the USD sees the USD Index dip below 99.20 for the first time since October 30. Price action keeps the short-term series of lower lows and lower highs in the dollar index intact. This put upward pressure on EURUSD, with the pair briefly piercing the 1.1622 50-day EMA (which also marks the 76.4% retracement for the Oct 28 - Nov 05 downleg). Key resistance remains into the 1.1669 Oct 28 high.

- USDJPY remains capped into the 155.0 handle, having tested the mark on three occasions over the past two days, potentially building a short-term resistance zone around that area. BoJ's Ueda appeared content overnight, saying underlying CPI is gradually moving toward the bank’s 2% target, and that the mechanism in which wages and prices rise moderately in tandem will be maintained.

- A resumption of the uptrend in USDJPY after dollar-driven weakness this morning would put sights on 155.53, a Fibonacci projection. Initial support to watch lies at 153.03, the 20-day EMA.

- AUD outperforms (+0.5%) following stronger-than-expected overnight labour market data, with jobs growth doubling consensus. The recent trend, if sustained, is likely to keep RBA rates on hold in the short-term given the Q3 increase in price pressures and uncertainty over policy restrictiveness. Today's price action in AUDUSD undermines the recent bearish theme and instead signals scope for a stronger short-term recovery. The move higher has exposed resistance at 0.6618, the Oct 29 high.

- With the reopening of the US government imminent, markets await any advisories or updates on release schedules for now much-delayed data. ECB's Elderson, BoE's Greene and SNB's Tschudin are scheduled to appear next to a set of speakers from the Fed.

OPTIONS: Expiries for Nov13 NY cut 1000ET (Source DTCC)

- EUR/USD: $1.1575(E1.3bln), $1.1590(E1.7bln), $1.1600(E1.1bln), $1.1615(E1.1bln)

- USD/JPY: Y147.00($1.6bln), Y152.96-00($1.1bln), Y154.00($977mln), Y155.00($1.2bln)

- AUD/USD: $0.6520-30(A$1.8bln)

EQUITIES: Medium-Term Bull Trend in Eurostoxx 50 Futures Remains Intact

- A medium-term bull trend in Eurostoxx 50 futures remains intact and this week’s gains reinforce bullish conditions. The contract has traded through resistance at 5742.00, the Oct 29 high to confirm a resumption of the uptrend. Attention is on 5818.00 next, a Fibonacci projection. Clearance of this hurdle would open 5848.00, a bull channel top drawn from the Aug 1 low. On the downside, initial firm support is seen at 5669.13, the 20-day EMA.

- The trend condition in S&P E-Minis remains bullish and the bear leg since the Oct 30 high appears to have been a correction. The contract has managed to find support below the 50-day EMA, currently at 6728.13, and a key level. Activity on Nov 7 highlights a potential reversal signal - a bullish doji candle. This defines key support at 6655.50, the Oct 7 low. Sights are on 6953.75, Oct 30 high and bull trigger.

COMMODITIES: Yesterday's Sell-Off Strengthens a Bearish Theme for WTI

- A sell-off in WTI futures yesterday, strengthens a bearish theme. A continuation lower would pave the way for a move towards key support and the bear trigger at $55.96, the Oct 20 low. Clearance of this level would confirm a resumption of the downtrend. Note that it is still possible a bullish corrective cycle remains in play. Resistance to watch is $62.59, the Oct 24 high. A breach of this hurdle would signal scope for a stronger correction.

- The downleg in Gold since Oct 20 appears to have been a correction and the move down has allowed an overbought condition to unwind. Recent gains suggest that correction is over. A key support at the 50-day EMA, at $3910.9, is intact. Clearance of this EMA would signal scope for a deeper retracement. Initial resistance is $4264.7, a Fibonacci retracement. A stronger recovery would open $4381.5, the Oct 20 high and bull trigger.

| Date | GMT/Local | Impact | Country | Event |

| 13/11/2025 | 1200/1200 | BOE Greene in Panel on Central Bank Independence | ||

| 13/11/2025 | - | ECB de Guindos at ECOFIN Meeting in Brussels | ||

| 13/11/2025 | 1300/1400 | ECB Elderson Moderates Climate and Banks Panel | ||

| 13/11/2025 | 1300/0800 | San Francisco Fed's Mary Daly | ||

| 13/11/2025 | 1330/0830 | *** | Jobless Claims | |

| 13/11/2025 | 1330/0830 | ** | WASDE Weekly Import/Export | |

| 13/11/2025 | 1530/1030 | Minneapolis Fed's Neel Kashkari | ||

| 13/11/2025 | 1630/1130 | ** | US Bill 04 Week Treasury Auction Result | |

| 13/11/2025 | 1630/1130 | * | US Bill 08 Week Treasury Auction Result | |

| 13/11/2025 | 1700/1200 | ** | DOE Weekly Crude Oil Stocks | |

| 13/11/2025 | 1700/1200 | ** | US DOE Petroleum Supply | |

| 13/11/2025 | 1715/1215 | St. Louis Fed's Alberto Musalem | ||

| 13/11/2025 | 1720/1220 | Cleveland Fed's Beth Hammack | ||

| 13/11/2025 | 1800/1300 | *** | US Treasury Auction Result for 30 Year Bond | |

| 13/11/2025 | 1900/1400 | ** | Treasury Budget | |

| 14/11/2025 | 0001/0001 | KPMG/REC Report on Jobs | ||

| 14/11/2025 | 0200/1000 | *** | Fixed-Asset Investment | |

| 14/11/2025 | 0200/1000 | *** | Retail Sales | |

| 14/11/2025 | 0200/1000 | *** | Industrial Output | |

| 14/11/2025 | 0200/1000 | ** | Surveyed Unemployment Rate M/M | |

| 14/11/2025 | 0700/0800 | ** | Unemployment | |

| 14/11/2025 | 0745/0845 | *** | HICP (f) | |

| 14/11/2025 | 0800/0900 | *** | HICP (f) | |

| 14/11/2025 | 0900/1000 | Foreign Trade | ||

| 14/11/2025 | 1000/1100 | * | Trade Balance | |

| 14/11/2025 | 1000/1100 | *** | EZ GDP 2nd (Flash) | |

| 14/11/2025 | 1030/1130 | ECB Elderson Keynote at ECB Banking Supervision Forum | ||

| 14/11/2025 | 1330/0830 | ** | Monthly Survey of Manufacturing | |

| 14/11/2025 | 1330/0830 | ** | Wholesale Trade | |

| 14/11/2025 | 1330/1430 | ECB Elderson Remarks at COP30 Finance Day | ||

| 14/11/2025 | 1500/1000 | * | Business Inventories | |

| 14/11/2025 | 1500/1600 | ECB Lane Panel at Workshop on International Macroeconomics and Finance | ||

| 14/11/2025 | 1530/1030 | ** | Natural Gas Stocks | |

| 14/11/2025 | 1800/1300 | ** | Baker Hughes Rig Count Overview - Weekly | |

| 14/11/2025 | 1800/1300 | ** | Baker Hughes Rig Count Overview - Weekly | |

| 14/11/2025 | 1800/1300 | ** | Baker Hughes Rig Count Overview - Weekly | |

| 14/11/2025 | 1930/1430 | Dallas Fed's Lorie Logan | ||

| 14/11/2025 | 2020/1520 | Atlanta Fed's Raphael Bostic |