STIR: Fed December Cut Shifts To 50/50 Call

- US rates have seen a concerted hawkish shift overnight, gaining momentum again in recent trade as US desks filter in and concentrated in the front end with a cut next month now seen as a 50/50 call.

- It extends moves seen late yesterday. Initial timing coincided with NY Fed SOMA Manager Perli yesterday saying the Fed “won’t have to wait long” before purchasing assets. However, that’s difficult to square away as it broadly chimed with implications from NY Fed’s Williams earlier in the day along with other recent commentary from FOMC members including Powell re reserves having shifted close to ample.

- The front-end focused nature of the shift sees some question marks over pinning it on the government re-opening (i.e. having dodged any last-minute hiccups from the House), although it could still be a positioning unwind related to this.

- Fed Funds implied rates are 2.5-3.5bp higher on the day for meetings out to mid-2026.

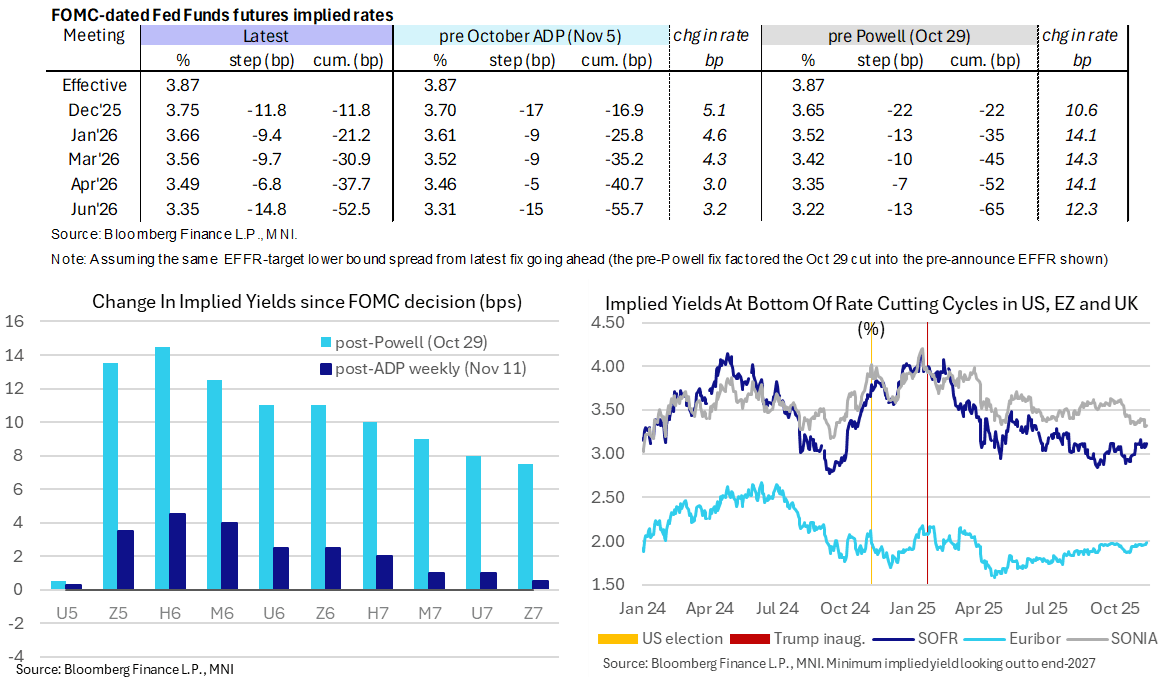

- Cumulative cuts from an assumed 3.87% effective: 12bp Dec, 21bp Jan, 31bp Mar, 38bp Apr, 52.5bp Jun.

- SOFR futures are -0.05 in the SFRH6 through to -0.025/-0.030 in 2027 contracts.

- It sees the terminal implied yield rise to 3.115% (SFRH7, +3bp), +5bp from Tuesday’s close having digested the soft weekly ADP print but still off the multi-month high close of 3.16% from last Wednesday after more encouraging monthly ADP and especially ISM Services data.

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

NORWAY: Analyst Views On 2026 Budget Proposal

See below for a selection of sell-side views ahead of tomorrow's budget proposal:

SEB: “We expect the government to hold back spending to leave room to meet demands from support parties"....“We expect petroleum revenue spending around 2.7-2.8% of GPFG, implying a still expansionary budget although a smaller impulse than the 1.3ppt in 2025”...“We expect broadly stable gross NST issuance next year (NOK 95-105bn in 2025). Considering large drawdowns in recent years there is still a need to continue the built up of the cash reserve”

DNB: “We anticipate a broadly neutral fiscal stance, with a structural non-oil budget deficit of NOK 573bn, corresponding to a 2.8% withdrawal rate in 2026 (vs. 2.7%)”.

JP Morgan: “Our economists expect Norwegian fiscal policy to remain expansionary in 2026 with plentiful room for fiscal thrust of 0.6% for next year"....“Our economists expect the structural non-oil budget deficit to be 2.8% of the oil fund’s value, i.e. complying with the 3% fiscal rule. Based on the current market value of the fund (which varies a lot on a daily basis), this translates, in nominal terms, to a structural non-oil deficit of ~NOK 570bn, up NOK 28bn from 2025”.

Nomura: "The government is likely to propose NOK billions for defence funding, and a reduction in electricity tax, which should contribute to lower energy inflation in 2026"..."Fiscal policy is likely to have an expansionary effect on GDP in 2026".

Danske Bank: “Currently we estimate a funding need of NOK87bn”....“Given that in previous years (2023 and 2024), the government has used the account to lower the issuance and thus drawn on the account, it could increase the account in 2026, as it has done in 2025, when we estimate it will be increased by some NOK3bn to NOK13bn. Hence, we end up with an issuance target of NOK90bn-100bn”

NORWAY: 2026 Budget Proposal Due Tomorrow Morning

The Norwegian 2026 budget proposal will be released tomorrow. Most market-relevant information will be released at 0700BST/0800CET, with the full budget presented at 0900BST.

- At 0700BST, the following “key figures” for 2026 will be released:

- Non-oil and structural non-oil deficit spending in NOK.

- Structural non-oil deficit spending as a % of Government pension fund assets (fiscal rule stipulates maximum spending of 3% of the GPFG).

- Structural non-oil deficit as a % of mainland GDP.

- Fiscal impulse (defined as the change in 3. relative to 2025)

- Summary of updated Govt’ macroeconomic forecasts.

- At 0900BST, the full budget will be presented, including details of polices and a full breakdown of fiscal figures (which analysts use to estimate Norges Bank FX transactions for the year ahead).

- In the September MPR, Norges Bank projected the structural non-oil deficit spending at 2.8% of the GPFG (vs 2.7% in 2025). Deviations from this forecast will feed into subsequent rate path projections.

- Note that support to Ukraine (which doesn’t provide an impulse to mainland activity) is included in the Government’s fiscal rule.

- The budget proposal will also inform analysts’ NGB issuance expectations for next year (see sell-side expectations in the following post for more).

- Following tomorrow’s proposals, the Government will negotiate with supporting Parties to finalise the budget by December. PM Store’s Labour party won the election in September, but relies on support from the Centre, Socialist Left, Green and Red Parties to have a majority in the Storting. Reliance on these smaller and mostly left-leaning parties will factor into budget discussions, with areas such as wealth taxes and welfare spending in focus.

ESM ISSUANCE: 2.75% Feb-35 ESM bond: Priced

- Reoffer: 2.884% / 98.906%

- Size: E1bln WNG (We had pencilled in a E1.0-1.5bln range for this week's ESM transaction, but leant towards a E1.25bln size rather than the E1bln WNG announced. Following today's sale, total ESM funding for the year will be broadly in line with the E7bln annual target)

- Books in excess of E18.5bln (exc. JLM interest)

- Final terms set earlier: MS + 31bps (Guidance was MS +34bps area)

- Hedge ratio: 98% vs 2.50% Feb-35 Bund (DE000BU2Z049) + 32.6bps (Spot ref: 99.511)

- Settlement: Oct. 21, 2025 (T+5)

- ISIN: EU000A1Z99W5

- Bookrunners: HSBC, MS (B&D), Natixis

- Timing: TOE 12:11BST / 13:11CET. FTT 12:30BST / 13:30CET

Source: Market sources / MNI colour.