MNI US MARKETS ANALYSIS - Core Bonds Pressured into CPI Print

Highlights:

- Core bonds under pressure on solid European PMI data

- Gilts spared from sell-off as Chancellor reportedly considers income tax rise

- Much delayed CPI to be scrutinized for data quality concerns

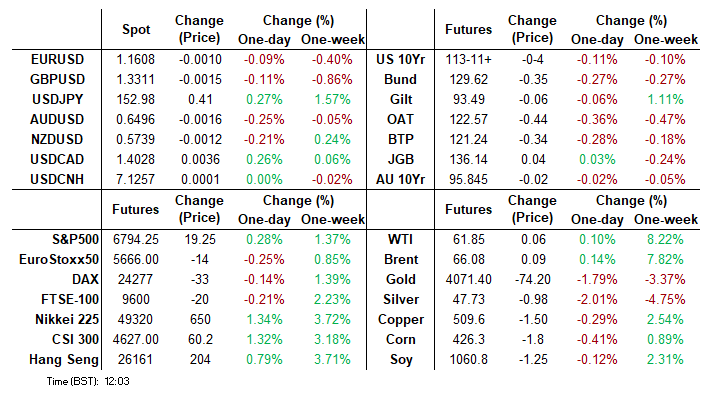

US TSYS: Firm EZ PMIs Help Consolidate Thursday Sell-Off, CPI and PMIs Ahead

- Treasuries consolidate yesterday’s sell-off in moves that were driven by a surge in oil futures before strong gains in equities after the US cash open.

- The biggest overnight move came on stronger than expected Eurozone PMIs, led by Germany. It more than unwound a small rally on Trump halting Canada trade negotiations.

- Today’s focus is firmly on US CPI but with mention also for flash PMIs and less so the U.Mich consumer survey. President Trump has an open schedule before flying to Malaysia tonight.

- Cash yields are 0.2-0.9bp higher on the day, led by 30s.

- 10Y yields at 4.005% (+0.4bp) sit just above the 4.00% handle with the next target at 4.05%, equating to 113-01 in TYZ5 today.

- TYZ5 trades at 113-11+ (-04) on modest cumulative volumes of 240k, off an earlier low of 113-10+ after yesterday’s 113-12.

- It nudges closer to support at 113-06+ (20-day EMA) which sits before that yield-driven 113-01, although a bullish trend structure remains with resistance seen at 114-02 (Oct 17 high).

- Data: US CPI Sep (0830ET), S&P Global Flash PMIs Oct (0945ET), U.Mich consumer survey Oct F (1000ET), KC Fed services Oct (1100ET)

- Politics: Trump departs White House for Malaysia (2240ET)

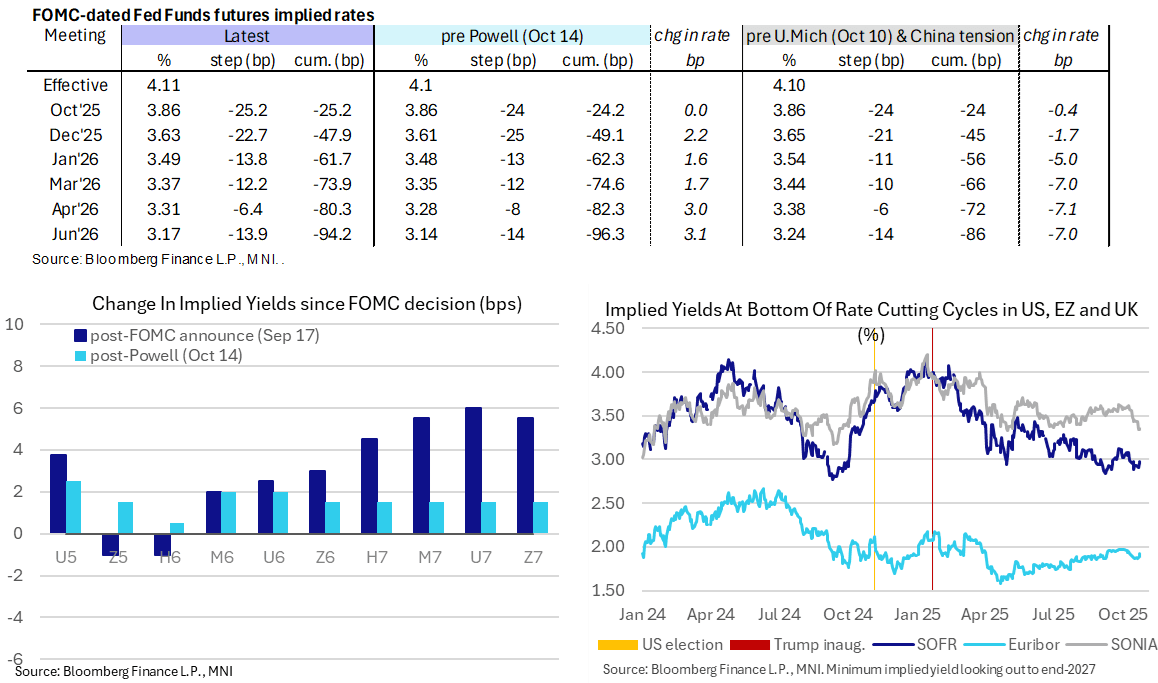

STIR: Fed Rates Close To Most Hawkish In Two Weeks With CPI Eyed

- Fed Funds implied rates consolidate yesterday’s hawkish shift on a surge in oil futures, having seen little impact from Trump terminating trade negotiations with Canada overnight.

- Today’s delayed CPI report is in firm focus. MNI US CPI Preview: https://media.marketnews.com/USCPI_Prev_Oct2025_update_24969dda49.pdf

- Cumulative cuts from 4.11% effective: 25bp Oct, 48bp Dec, 61.5bp Jan, 74bp Mar, 80.5bp Apr and 94bp Jun.

- SOFR futures are 0-1.5 ticks lower when looking out to end-2027, leaving the terminal implied yield at 2.975% (SFRZ6, +1.5bp). It last closed higher on Oct 10 at which point US-China trade tensions increased before last week’s further decline on brief US regional bank concerns.

- Yesterday saw a further $3bn of SRF uptake and potentially chimed with a lift back higher in SOFR from 4.21% the day prior.

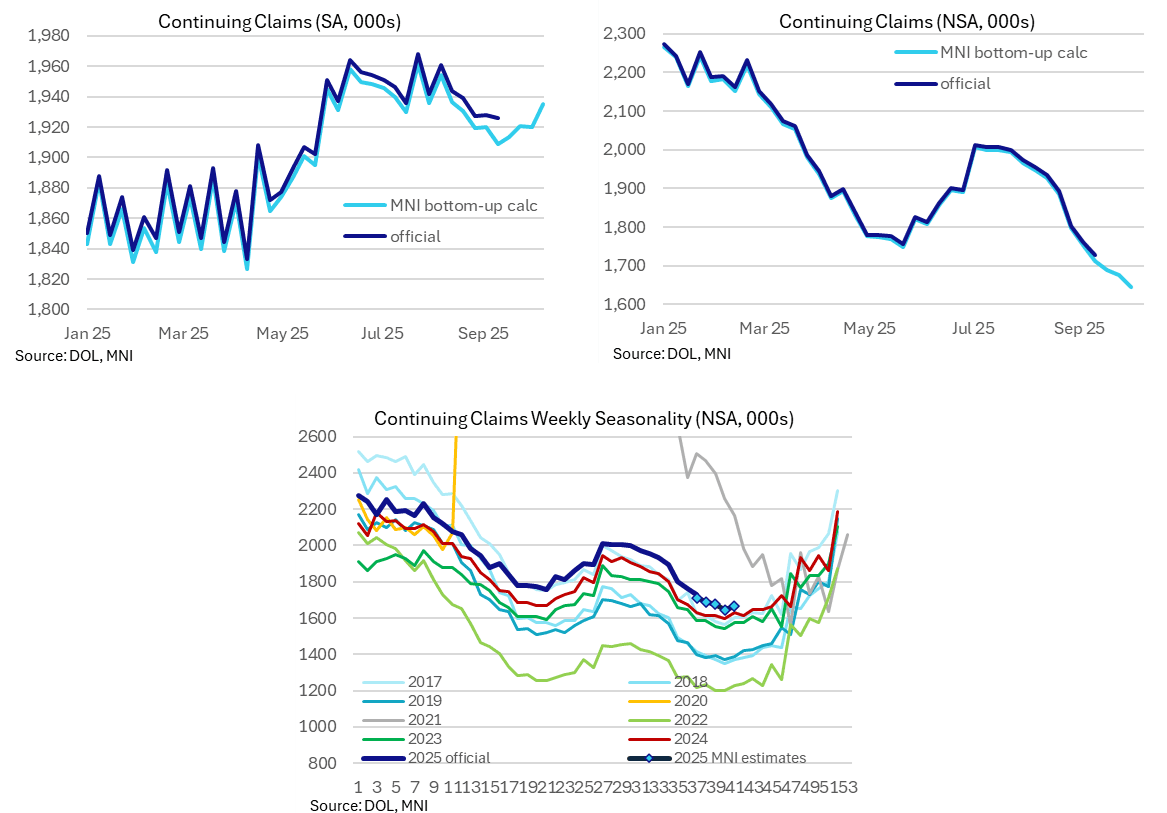

US DATA: Continuing Claims Hold Off June/July Cycle Highs

Continuing claims have drifted higher in recent weeks, although we’re still cautious of a strong pattern of downward revisions to latest weeks. They remain somewhat elevated by recent year standards but off cycle highs. We see the combination with initial claims as a continuation of a low fire, low hire labor market without any notable deterioration being seen.

- MNI estimates continuing claims at a seasonally adjusted 1935k in the week to Oct 11 after another downward revised 1920k (we initially estimated 1929k).

- It’s tentatively the highest since mid-August but we again note the continued trend of downward revisions.

- Whilst it’s another small increase from what we calculate to have been a recent low of 1909k in mid-September, it’s still below recent cycle highs around 1960k’s in June and July.

- That push higher to those levels came with a marked slowdown in hiring at the time, with the continuing claims trend since then implying a stabilization and modest improvement but still chiming with soft hiring conditions.

- The initial jobless claims figures are still consistent with periods of a healthier labor market than continuing claims, but this trend has been seen for some time now. The combination points to a continuation of a low fire, low hire labor market.

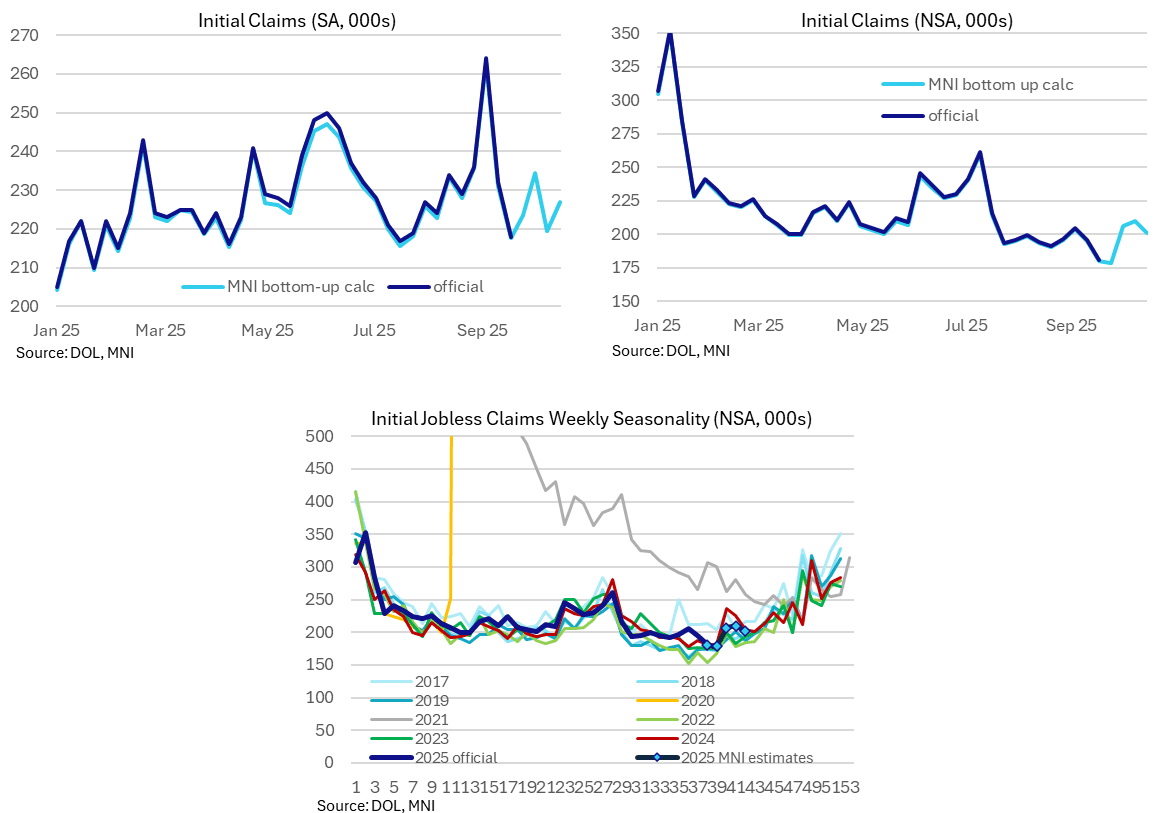

US DATA: Initial Claims Favorable Compared To Prior NFP Ref Periods

MNI estimates for initial jobless claims from state-level data saw a small increase last week but are still close to levels from prior historically tight labor markets. It’s a payrolls reference week and compares somewhat favorably to both September and August equivalent readings (not that we can be sure when the Sept or Oct payroll reports will be released).

- MNI estimates initial jobless claims at a seasonally adjusted 227k in the week to Oct 18, down from 220k in the week to Oct 11 (revised slightly from our initial estimate of 218k).

- It’s a payrolls reference period and compares to the 231k we estimate for the September reference period and the 234k in official data for August.

- The four-week average increased from 224k back to 226k, still low historically. That’s down from a recent peak of 241k in the official data back in early September, with much of that increase down to Texas fraud. Whilst there haven’t been revisions to that previous spike, Texas claims are at least back running at more typical levels (a non-seasonally adjusted 16.5k last week vs 32k in early September).

- As has been the case under the government shutdown, this uses the state-level data released yesterday afternoon ET with pre-released seasonal factors.

- There is still another reasonable error band, missing figures from Tennessee (6.0k in the previous week), Massachusetts (5.3k) and Colorado (3.4k) in the published non-seasonally adjusted data. We use last year’s seasonal pattern to estimate these states which might leave a small upside risk to our overall estimate.

- When looking at the historical chart below, remember that the uplift in recent weeks in the 2024 line was driven by Hurricanes Helene and Milton.

CANADA: Trump Cancelling Trade Talks Puts Carney In Tough Position

Following US President Donald Trump's announcement on Truth Social that he is terminating all trade talks with Canada, Prime Minister Mark Carney faces a binary choice. Either seek to repair ties with the White House, or follow in Ontario Premier Doug Ford's footsteps and pursue a more aggressive line with the US regarding trade.

- Trump claimed that a TV advertisement run in the US and sponsored by the gov't of Ontario, in which the late US President Ronald Reagan is heard talking of the economic costs of tariffs, intended "to interfere with the decision of the U.S. Supreme Court, and other courts."

- The announcement came just hours after Carney appeared at a press conference alongside Ford. In the presser, Ford, asked what his advice to Carney would be, said, “If you can’t get a deal, let’s start hitting them back.”

- During the presser, Carney said on trade talks with the US and the upcoming review of the CUSMA trade deal, "If we ultimately don't make progress in these various sectors [steel and aluminium], we're going to do what's necessary to protect our workers [...] If it's the case that the Americans have access to our markets in a way that's inappropriate given the level of access we have to their markets, we will change the terms."

- Pursuing Ford's 'hit back' strategy would be politically popular domestically, but risk further escalation from the White House and as such may prove an unlikely option for Carney.

EMERGING MARKETS: China Trade Discussions in Focus with Both US and EU

- US/CHINA (BBG): US President Donald Trump is aiming for a quick win in a pivotal Thursday meeting with Chinese counterpart Xi Jinping, even if the outcome falls short of the sweeping deal he’s teased on issues at the heart of the rivalry between the world’s two largest economies. Ahead of the sit-down, the US president said he wants to extend a pause on higher tariffs on Chinese goods in exchange for Xi resuming American soybean purchases, cracking down on fentanyl and backing off restrictions on rare-earth exports — all while maintaining some trade barriers he sees as essential.

- EU/CHINA (MNI): Beijing still hopes to resolve trade frictions with the European Union, and to separate its dealings with the bloc from its disputes with the U.S., Chinese policy advisors told MNI, while an official in Brussels said the EU is optimistic that it will obtain an agreement to loosen restrictions on rare earth exports.

- TURKEY (BBG): A Turkish court dismissed a case that could topple the leader of the country’s main opposition party, offering temporary relief to investors concerned about renewed political instability. The court case was looking into allegations of irregularities during 2023 internal elections at Turkey’s secular Republican People’s Party, known by its Turkish initials CHP.

OPTIONS: Expiries for Oct24 NY cut 1000ET (Source DTCC)

- EUR/USD: $1.1460(E560mln), $1.1500-20(E1.3bln), $1.1635-50(E1.1bln)

- USD/JPY: Y150.00($2.0bln), Y151.00-20($1.4bln), Y152.00($583mln), Y152.50($596mln), Y153.80-00($574mln)

- AUD/USD: $0.6450(A$1.6bln)

EGBS: Post-PMI Bund Pressure has Prices Through Support, Weighing on Treasuries

Bond futures across Europe continue to trade under pressure on the back of the German and EU PMIs beat, with spillover sales in Treasuries adding to the theme.

- Notably, both Bund and Dec-25 Treasuries have broken through initial support seen at Monday's lows. Next immediate target for Bunds is the ~2.62% yield level (200DMA), which coincides with the current price at 129.56. The 100DMA at 2.66% coincides with 129.16.

- For the US 10yr Yield, the next target comes at 4.05% and this would equate to 113.01 today.

COMMODITIES: WTI Recovery Holding, Clears Notable Resistance

A sharp pullback in Gold this week appears corrective - for now. Note that the trend is overbought and a deeper retracement would allow this condition to unwind. Support at the 20-day EMA, at $4046.2, has been pierced. The latest recovery in WTI futures appears corrective for now, however, note that price has traded through resistance at the 50-day EMA, at $61.11. The breach of this average signals scope for a stronger recovery and exposes $62.34.

- WTI Crude up $0.14 or +0.23% at $62

- Natural Gas down $0.01 or -0.27% at $3.337

- Gold spot down $65.83 or -1.6% at $4062.82

- Copper up $0.5 or +0.1% at $511.25

- Silver down $0.95 or -1.94% at $47.9027

- Platinum down $20.45 or -1.25% at $1607.83

| Date | GMT/Local | Impact | Country | Event |

| 24/10/2025 | 1200/0800 | ** | Brazil Preliminary CPI | |

| 24/10/2025 | 1230/0830 | *** | CPI | |

| 24/10/2025 | 1230/0830 | *** | CPI | |

| 24/10/2025 | 1230/0830 | *** | CPI | |

| 24/10/2025 | 1300/1500 | ** | BNB Business Confidence | |

| 24/10/2025 | 1345/0945 | *** | S&P Global Manufacturing Index (Flash) | |

| 24/10/2025 | 1345/0945 | *** | S&P Global Services Index (flash) | |

| 24/10/2025 | 1400/1000 | *** | New Home Sales | |

| 24/10/2025 | 1400/1000 | *** | U. Mich. Survey of Consumers | |

| 24/10/2025 | 1400/1000 | ** | University of Michigan Surveys of Consumers Inflation Expectation | |

| 24/10/2025 | 1400/1000 | *** | New Home Sales | |

| 24/10/2025 | 1700/1300 | ** | Baker Hughes Rig Count Overview - Weekly | |

| 24/10/2025 | 1700/1300 | ** | Baker Hughes Rig Count Overview - Weekly |