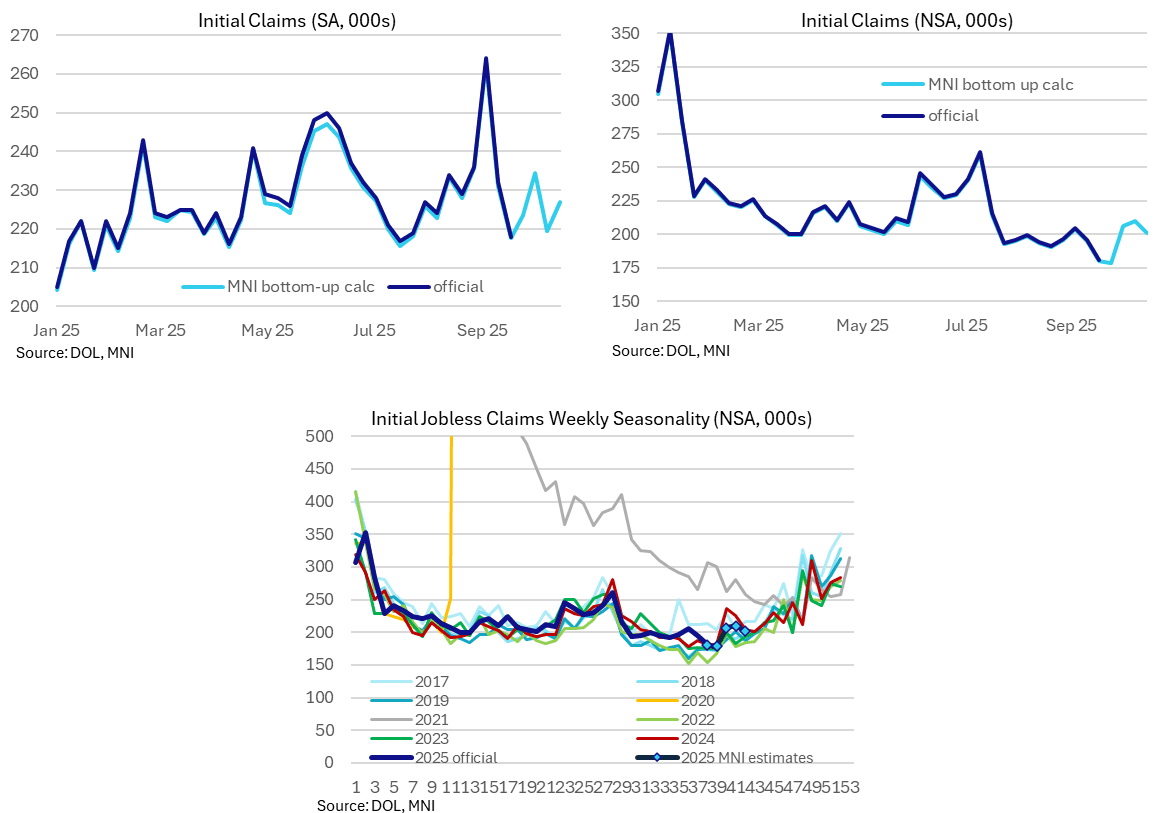

US DATA: Initial Claims Favorable Compared To Prior NFP Ref Periods

MNI estimates for initial jobless claims from state-level data saw a small increase last week but are still close to levels from prior historically tight labor markets. It’s a payrolls reference week and compares somewhat favorably to both September and August equivalent readings (not that we can be sure when the Sept or Oct payroll reports will be released).

- MNI estimates initial jobless claims at a seasonally adjusted 227k in the week to Oct 18, down from 220k in the week to Oct 11 (revised slightly from our initial estimate of 218k).

- It’s a payrolls reference period and compares to the 231k we estimate for the September reference period and the 234k in official data for August.

- The four-week average increased from 224k back to 226k, still low historically. That’s down from a recent peak of 241k in the official data back in early September, with much of that increase down to Texas fraud. Whilst there haven’t been revisions to that previous spike, Texas claims are at least back running at more typical levels (a non-seasonally adjusted 16.5k last week vs 32k in early September).

- As has been the case under the government shutdown, this uses the state-level data released yesterday afternoon ET with pre-released seasonal factors.

- There is still another reasonable error band, missing figures from Tennessee (6.0k in the previous week), Massachusetts (5.3k) and Colorado (3.4k) in the published non-seasonally adjusted data. We use last year’s seasonal pattern to estimate these states which might leave a small upside risk to our overall estimate.

- When looking at the historical chart below, remember that the uplift in recent weeks in the 2024 line was driven by Hurricanes Helene and Milton.

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

EGBS: Spreads To Bunds Wider On Russia-Ukraine Fears; Short End IT Supply Due

10-year EGB spreads to Bunds are up to 1.5bps wider on the session, with BTPs lightly underperforming (spread to Bunds at ~81bps). Concerns around President Trump’s remarks on the Russia-Ukraine conflict yesterday and Russia pointing to further advances in Ukraine this morning may be contributing to peripheral underperformance versus Bunds intraday.

- The BTP/Bund spread has tightened almost 40bps year-to-date, but has struggled to consolidate below the 2010 lows of ~76bps in recent weeks.

- BTP futures are +8 ticks at 119.75, lightly underperforming Bunds (+18 ticks at 128.36). The primary trend condition in BTP futures remains bullish, with the pullback from the Sep 11 considered corrective. Initial support is the Sep 4 low at 119.06, with key support at the Sep 3 low of 118.36.

- Italian short-end (and linker) supply is due at 1000BST, with E2.0-2.5bln of the on-the-run 2.10% Aug-27 BTP Short Term on offer.

- This BTP Short Term was last re-opened in August, where it attracted a 1.56x bid-to-cover ratio for the E3bln on offer.

- The Italian curve is lightly bear flatter ahead of the supply, with 2-year yields little changed and 30-year yields down almost 1bp.

FOREX: FX OPTION EXPIRY

Of Note:

EURUSD 1.39bn at 1.1800 (could act as magnet).

GBPUSD 1.31bn at 1.3500 (could act as magnet).

USDJPY 1.1bn at 148.40/148.50.

AUDUSD ~1bn at 0.6600.

EURUSD 2.32bn at 1.1800/1.1805 (thu).

EURUSD 2.02bn at 1.1750 (fri).

AUDUSD 1.29bn at 0.6625 (mon).

- EURUSD: 1.1730 (628mln), 1.1750 (978mln), 1.1760 (324mln), 1.1800 (1.39bn), 1.1811 (355mln).

- GBPUSD: 1.3500 (1.31bn).

- USDJPY: 147.90 (241mln), 148.00 (296mln), 148.40 (350mln), 148.50 (729mln).

- USDCAD: 1.3850 (540mln).

- AUDUSD: 0.6600 (904mln), 0.6625 (575mln).

- NZDUSD: 0.5890 (351mln), 0.5900 (372mln).

- EURNOK: 11.7500 (405mln).

RBA: VIEW: TD Remove Call For Nov & Feb Cuts, Pay Nov RBA OIS

Sell-side names continue to adjust their RBA calls in a hawkish direction after the latest round of monthly CPI data. TD Securities note that “CPI is running hotter than the RBA would probably like and with activity holding up, this prompts a change of RBA call. We no longer forecast RBA cuts in November and February”. They will issue a full update of their view on Friday. They recommended paying November ‘25 RBA-dated OIS alongside this call change.