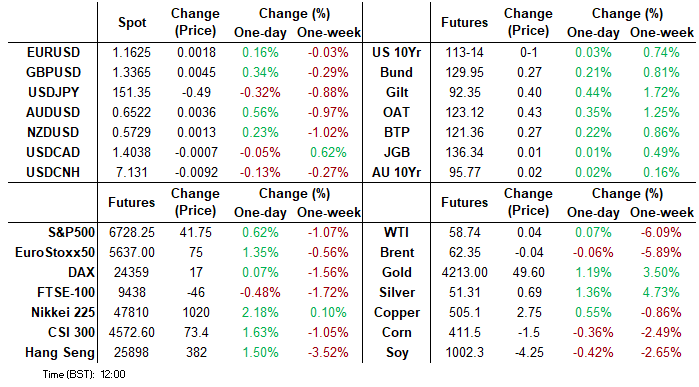

MNI US MARKETS ANALYSIS - CNY Fix Helps Drag USD Lower

Highlights:

- Markets still carry Powell's comments endorsing a next rate cut this month

- 10y Treasuries make short-lived test of 4.00%

- CNY fixed at strongest level in close to a year, helps aide USD weakness

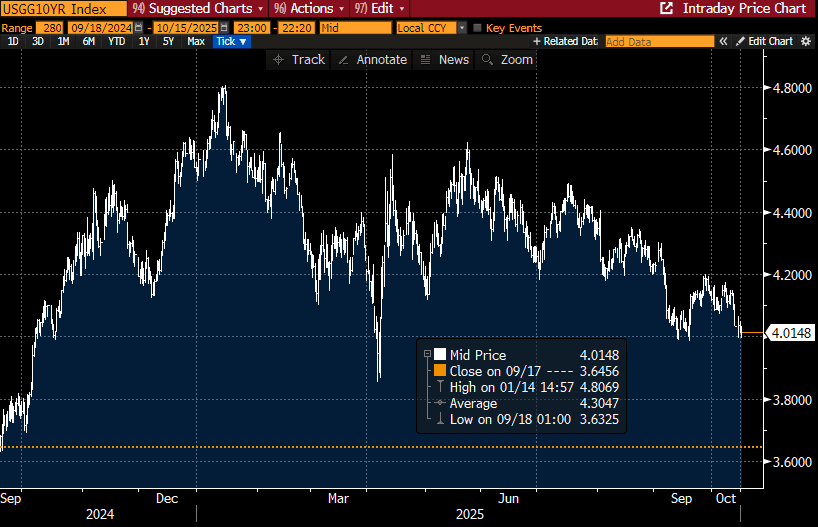

US TSYS: Another Short-Lived Probe Of Sub-4% 10Y Yields

- Treasuries are within overnight ranges but hold firmer on the day, underperforming EGBs which benefit from yesterday’s easing of near-term French political risks.

- Today sees calendar focus on the NY Fed Empire Survey for a latest look at regional manufacturing activity/sentiment before the Fed’s Beige Book. Earnings season also continues, with BofA results currently well-received and Morgan Stanley still to come.

- Cash yields are 0.5-2.5bp lower across the curve, bull flattening.

- 10Y yields (currently 4.0148%, -1.7bps) again tested the 4% handle earlier with a low of 3.9975% after yesterday’s 3.9976%, but are finding support at this level. Whilst there were brief clearances on Sep 17 and Sep 11, yields were last materially sub-4% in early April under reciprocal tariff deliberations.

- TYZ5 trades at 113-13+ (+00+) on modest cumulative volumes of 270k.

- An earlier high of 113-17+ matched that from yesterday, in signs of some resistance ahead of a bull trigger at 113-29 (Sep 11 high). The recent uplift has dragged support up to 112-26 (20-day EMA).

- Data: MBA mortgage applications (0700ET), Empire mfg Oct (0830ET), Beige Book (1400ET). Today’s CPI report has been rescheduled to Oct 24.

- Fedspeak: Miran (0930ET), Miran (1230ET), Waller (1300ET) and Schmid (1430ET) – see FED bullet.

- Bill issuance: US Tsy $69B 17W bill auction (1130ET)

- Politics: Trump participates in press conference with FBI Director (1500ET), Trump hosts Ballroom Dinner (1930ET)

- Earnings: Morgan Stanley still to report along with Abbot Labs and Prologis pre-market. BofA has already reported, beating trading revenue estimates. MNI Earning Calendar found here.

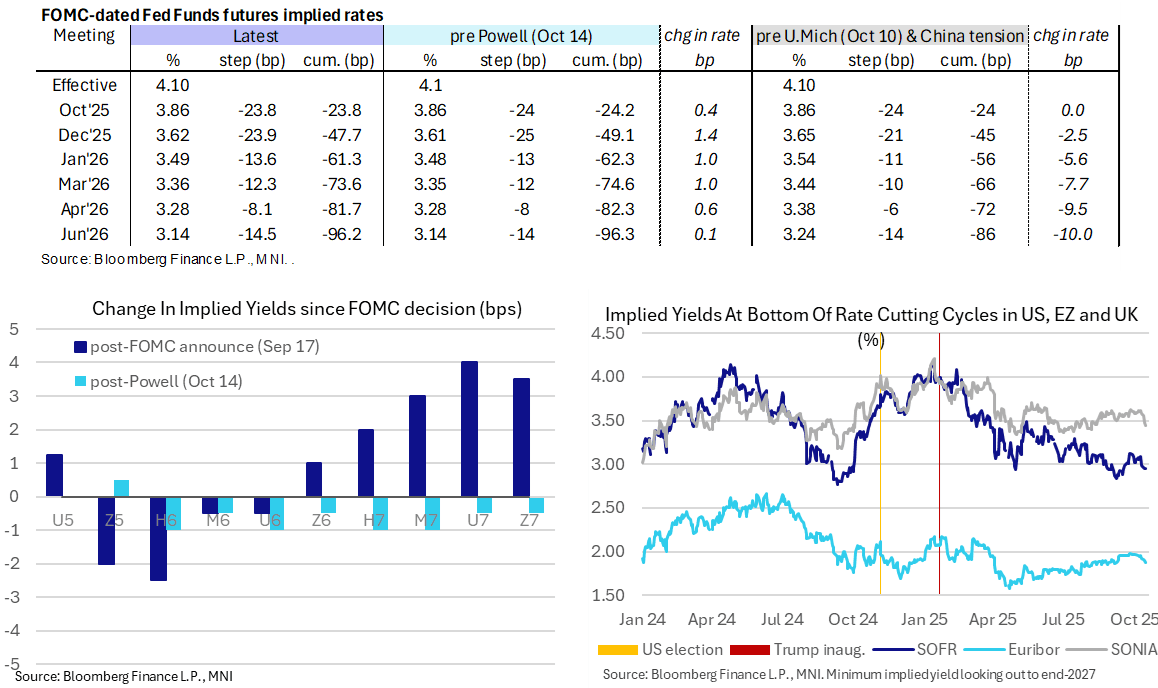

STIR: Maintaining Little Impact From Powell Remarks

- Fed Funds implied rates are little changed overnight, sitting marginally higher than pre-Powell levels for near-term meetings but unchanged out in mid-2026 on the same post-Powell basis.

- SOFR futures are within -0.5 to +1 ticks post-Powell looking out to 2027.

- FF cumulative cuts from 4.10% effective: 24bp Oct, 47.5bp Dec, 61.5bp Jan, 73.5bp Mar, 81.5bp Apr and 96bp Jun.

- The SOFR implied terminal yield of 2.95% (SFRH7) is unchanged on the day, towards recent lows (2.84% close on Sep 8 vs cycle lows of 2.77% in Sep 2024 ahead of the then start of the FOMC’s easing cycle). It points to 115-120bp of cuts ahead depending on fixed rate assumptions.

- Powell yesterday kept an October cut on track. Written remarks: "based on the data that we do have, it is fair to say that the outlook for employment and inflation does not appear to have changed much since our September meeting four weeks ago" when of course they cut rates 25bp eyeing "Rising downside risks to employment". Though in a slightly less dovish note, "data available prior to the shutdown, however, show that growth in economic activity may be on a somewhat firmer trajectory than expected."

- He echoed other speakers including Gov Waller last week in saying that the activity and labor market data aren't necessarily telling the same story, and future policy could depend on how that discrepancy plays out.

FED: Beige Book Likely More Notable Than Dovish Permanent Voter Fedspeak

We don’t expect today’s scheduled Fedspeak events to spring particular surprises on the rate outlook, with appearances geared for meaningful discussions coming from dovish members with well-known views. QT-related commentary, realistically from Miran, could be interesting however after Powell indicated it may be nearing an end in the coming months. More notable for us will be the Fed’s Beige Book at 1400ET, with anecdotal evidence of heightened importance amidst a dearth of government data releases.

Today’s Fedspeak schedule:

- 0930ET – Gov. and CEA’s Miran (voter, outright dove) on the “The Game Plan and The Fed” at Invest in American Forum (no text)

- 1230ET – Gov. and CEA’s Miran (voter, outright dove) in moderated conversation at Nomura Research Forum (no text)

- 1300ET – Gov. Waller (voter, dove) speaks on AI (text + Q&A)

- 1430ET – Kansas City Fed’s Schmid (’25, hawk) holds public townhall event (no text)

Recent context:

- Speaking on CNBC on Friday, Gov Waller - reportedly a finalist in Fed Chair considerations - unsurprisingly affirmed his view that the Fed should follow through with a series of cuts in light of developing labor market weakness (saying the labor market is "not tight in any way, shape or form"). While it's clear he's among the most dovish members on the Committee, eyeing 2 more rate cuts this year, he doesn't advocate too aggressive an easing: "I'm still in the belief we need to cut rates, but we need to kind of be cautious about it."

- Miran pencilled in 150bp of cuts to end-2025 in last month’s SEP, eyeing a Fed Funds target rate range of 2.75-3.0%. Speaking on Oct 7 on how his thinking might evolve with missing government data: “My view is that monetary policy should be forward looking and should be forecast dependent. And so given the forecasts I have in mind, I would be looking for evidence that there was a reason why they might not come to pass. […] Thus far, at any rate, I haven't seen anything that would make me think that my view has to be materially adjusted.”

- Schmid is likely one of the six dots who supported a cut in September before no further cuts in Oct or Dec. From Sep 26: "I viewed the 25-basis point cut in the policy rate last week as a reasonable risk-management strategy as the Fed balances its inflation objective with some heightened concern over the health of the labor market [...] My view is that inflation remains too high while the labor market, though cooling, still remains largely in balance."

STIR: Downside Risk To SONIA/Euribor Dec '26 Spread Remains Evident

The December ’26 SONIA future (SFIZ6) has extended on yesterday’s outperformance vs. Euribor (ERZ6). This leaves the SFIZ6/ERZ6 spread at the lowest level since late September (154.5bp last), ~10bp off month-to-date closing highs.

- We think the market has more room to reprice a dovish BoE outlook than a dovish ECB outlook, which points to the risk of further downside in the SFIZ6/ERZ6 spread.

- The next level of downside interest comes in at the September closing low, 153bp. A meaningful break there would expose cycle closing lows at 145bp.

- Downside risks to the spread remain evident, given the relatively shallow pricing of the BoE cutting cycle. ~10bp of easing priced through year-end, with the next cut not fully discounted until the March MPC.

- Yesterday’s data showed the UK labour market continues to slow, signalling a need for further easing. However, sticky inflation data had previously deferred the pricing of further easing and presents a risk to dovish views.

- Meanwhile, ECB rhetoric points to monetary policy being in a “good place”, suggesting the bank is nearing the end of the easing cycle.

- Markets still price greater-than-even odds of one further ECB cut in the cycle, with several Governing Council members noting the risks to inflation are skewed towards the downside.

Fig. 1: SONIA/Euribor December ’26 Futures Spread (SFIZ6/ERZ6)

Source: MNI - Market News/Bloomberg Finance L.P.

EUROPE ISSUANCE UPDATE

Gilt linker auction results

- Slightly disappointing 10-year gilt linker auction with the pre-auction mid-price above the average price. The price had fallen post-results despite the 3.49x decent bid-to-cover.

- GBP1.5bln of the 0.125% Aug-31 Linker. Avg yield 0.889% (bid-to-cover 3.49x).

Germany auction results

- E1bln (E757mln allotted) of the 0% Aug-50 Bund. Avg yield 3.14% (bid-to-offer 1.53x; bid-to-cover 2.02x).

- E1.5bln (E1.182bln allotted) of the 2.90% Aug-56 Bund. Avg yield 3.17% (bid-to-offer 1.11x; bid-to-cover 1.40x).

US TSY FUTURES: Mix Of Short Cover & Long Setting On Tuesday

OI data points to a mix of net short cover and long setting as Tsy futures rallied on Tuesday.

- Net short cover in US futures provided the most meaningful net positioning adjustment (~$5.7mln DV01 equivalent), tilting the curve-wide positioning swing in that direction.

| 14-Oct-25 | 13-Oct-25 | Daily OI Change | OI DV01 Equivalent Change ($) |

TU | 4,589,469 | 4,613,433 | -23,964 | -934,901 |

FV | 6,693,393 | 6,718,630 | -25,237 | -1,104,588 |

TY | 5,410,066 | 5,395,260 | +14,806 | +1,006,011 |

UXY | 2,466,290 | 2,452,629 | +13,661 | +1,244,858 |

US | 1,880,889 | 1,924,764 | -43,875 | -5,694,897 |

WN | 2,065,293 | 2,059,001 | +6,292 | +1,203,809 |

|

| Total | -58,317 | -4,279,708 |

SOFR: Mix Of Net Long Setting & Short Cover Dominates In Futures On Tuesday

OI data points to a mix of net long setting and short cover across most SOFR futures on Tuesday, with net short cover in the red pack providing the most prominent swing.

- Global trade tensions and wider global inputs drove the rally seen across much of the strip.

| 14-Oct-25 | 13-Oct-25 | Daily OI Change |

| Daily OI Change In Packs |

SFRU5 | 1,429,303 | 1,429,965 | -662 | Whites | +16,325 |

SFRZ5 | 1,552,747 | 1,505,430 | +47,317 | Reds | -41,578 |

SFRH6 | 1,162,616 | 1,196,091 | -33,475 | Greens | +15,142 |

SFRM6 | 1,031,521 | 1,028,376 | +3,145 | Blues | +2,734 |

SFRU6 | 1,010,678 | 1,037,469 | -26,791 |

|

|

SFRZ6 | 1,014,052 | 1,046,188 | -32,136 |

|

|

SFRH7 | 822,163 | 811,353 | +10,810 |

|

|

SFRM7 | 787,117 | 780,578 | +6,539 |

|

|

SFRU7 | 682,192 | 676,469 | +5,723 |

|

|

SFRZ7 | 749,904 | 747,999 | +1,905 |

|

|

SFRH8 | 441,901 | 434,055 | +7,846 |

|

|

SFRM8 | 376,942 | 377,274 | -332 |

|

|

SFRU8 | 303,042 | 300,757 | +2,285 |

|

|

SFRZ8 | 329,625 | 331,518 | -1,893 |

|

|

SFRH9 | 195,480 | 193,294 | +2,186 |

|

|

SFRM9 | 173,087 | 172,931 | +156 |

|

|

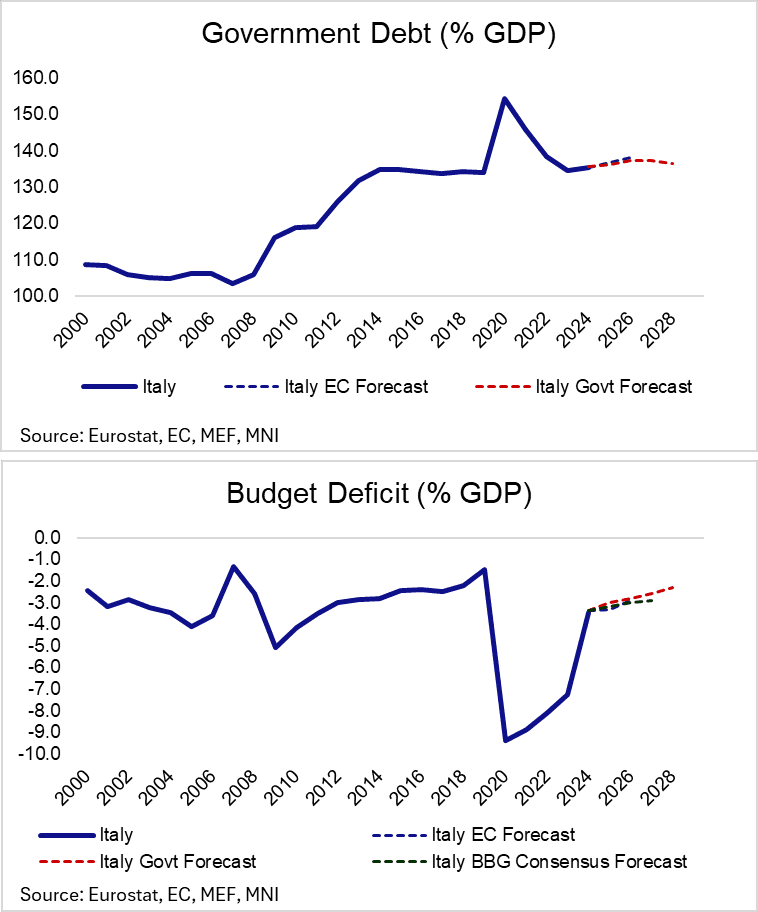

ITALY: 2026 Budget Proposal Sees 2026 Deficit At 2.8%; Growth and Ratings Key

Italy’s 2026 draft budget was approved by the government yesterday. As has been reported in recent weeks, the government expects the budget deficit to fall to 3% GDP in 2025. The deficit is expected to fall to 2.8% in 2026, 2.6% in 2027 and 2.3% in 2028. The 2026 deficit forecast is slightly more optimistic than current Bloomberg consensus of 3.0% and the EC’s Spring Projection round forecast of 2.9% (which of course do not yet account for the policies incorporated into the budget proposal).

- Having already tightened by ~35bps this year, the 10-year BTP/Bund spread has struggled to sustainably consolidated below 80bps in recent months. Upcoming growth data and ratings action will be key in determining whether further near-term narrowing is plausible.

- Growth: Q3 flash GDP is due on October 30. Consensus (according to Bloomberg’s ECFC page) looks for 0.1% Q/Q growth (vs -0.1% prior). We have previously noted that the main barrier to continued Italian fiscal consolidation is the country’s weak growth trajectory.

- Ratings: Moody’s will review Italy’s rating on November 21 (current rating Baa3, Outlook Positive). Moody's rating is two notches below Fitch and S&P, so at least a one notch upgrade is expected. We still think a one notch upgrade to Baa2 while maintaining a positive outlook seems reasonable.

- Some details of the budget proposal via Politico:

- “While ongoing discussions between the government and banks have yet to yield an agreement on what form the tax would take, the hard-right League, of which Giorgetti is a member, is seeking between €4 billion and €4.5 billion from a range of measures, according to two people familiar with the matter. The measures would also apply to insurers, one of the people said”.

- “Major policies in the draft budget, which Italian lawmakers will study in the coming months, includes a €9 billion cut to income taxes for the Italian middle class to 33 percent from 35 percent and €2 billion to align salaries with the cost of living after years of stagnation.

“The draft, which is due to be sent to the European Commission on Wednesday, also earmarks €3.5 billion for “anti-poverty measures” and €2.4 billion for health care in 2026".

FOREX: Powell Ripple Effect, CNY Fix Drive USD Lower

- The USD Index has stepped lower early Wednesday, prompting USD to fade further off the early October highs. This leaves the USD Index 0.8% off the October highs of 99.563, however still well toward the upper-end of the month's range. The USD is lower for a second session, with European markets taking the lead of the Wall Street close and Powell's appearance just after the close.

- Markets are growing in conviction that an October rate cut is far from the last at the Fed - and Powell's focus on the downside risk for the labour market raises focus for the 10y yield, which is narrowing in on 4.00%. A major break lower here could be the next trigger to extend the USD weaker. In tandem, the stronger-than-expected CNY fix has also proved USD negative. The PBOC set the reference rate at 7.0995, the strongest level in close to twelve months.

- Japanese political uncertainty has failed to keep JPY under pressure, with the currency broadly higher against the rest of G10. Opposition talks are scheduled over the coming days and while betting markets have shifted back in Takaichi's favour. A bullish trend condition in USDJPY remains intact and the pullback from last week’s high appears corrective. The next important support lies at 149.92, the 20-day EMA. On the upside, clearance of 153.27, the Oct 10 high, would resume the uptrend and open 154.39, a Fibonacci retracement point.

- EURUSD has made further progress as markets de-risk after the suspension of France's pension reform yesterday. Increased political stability is outweighing fiscal concerns, but rallies may be contained by potential ratings downgrades on any fiscal slippage. EURUSD printed 1.1645 just after the open, meeting the 100-dma in the process.

- US September CPI was originally set to print today, but with the government shutdown extending further (and looking likely to persist well toward the end of October / early November) it's set to be a quieter session for economic data. Canada's manufacturing sales data, NY Fed's Empire Manufacturing and the latest Beige Book are still due, however.

- This should keep focus on what's already been a busy week of central bank communications. Fed's Miran, Waller & Schmid are due, as well as BoE's Breeden, RBA's Bullock and ECB's Villeroy.

OPTIONS: Expiries for Oct14 NY cut 1000ET (Source DTCC)

- EUR/USD: $1.1450(E537mln), $1.1500(E848mln), $1.1600(E663mln), $1.1650(E636mln)

- USD/JPY: Y151.50($691mln), Y152.00($751mln)

- AUD/USD: $0.6500(A$1.0bln), $0.6580-00(A$1.2bln)

- USD/CAD: C$1.4000-10($598mln)

INDIA: RBI Sees INR Under Speculative Attack, Will Intervene Further: BBG

Citing a person familiar with the matter, Bloomberg report that the RBI considers recent weakness in the rupee as driven by speculative attacks and is prepared to continue its market intervention until the currency settles at a stronger level. Highlights from the piece below:

- “The RBI was alarmed to see the rupee nearing the 89 a dollar level in recent trading sessions”

- “The central bank is unwilling to let the currency breach its record low of 88.8050 a dollar level anytime soon”

- "The RBI will continue to intervene until it is satisfied that speculative positions are broken"

EQUITIES: Eurostoxx 50 Futures Remain Above Key Support Zone

- The trend condition in Eurostoxx 50 futures is unchanged, the direction is up and the latest pullback appears to have been a correction. A key support zone between 5553.01 - 5481.41, the area between the 20- and 50-day EMAs, remains intact. A clear break of the 50-day average would highlight a stronger reversal. On the upside, the bull trigger is 5689.00, the Oct 2 high. Clearance of this hurdle would confirm a resumption of the uptrend.

- A sharp sell-off in S&P E-Minis last Friday appears corrective - for now. The contract has found support below the 50-day EMA, currently at 6605.62, and the Oct 10 low of 6540.25 has been defined as a key short-term support. Moving average studies are in a bull-mode position, highlighting a dominant uptrend. The bull trigger is 6812.25, the Oct 9 high. A breach of this hurdle would confirm a resumption of the uptrend.

COMMODITIES: Gold Pierces $4200 Round Number Resistance

- A bearish theme in WTI futures remains intact and Tuesday’s fresh cycle low reinforces current conditions. The move down last week resulted in a break of support at $60.40, the Oct 2 low. This highlights an extension of the bearish price sequence of lower lows and lower highs and the move down opens $57.50 next, the May 30 low. On the upside, key resistance is at $66.42, the Sep 26 high. First resistance is at $62.47, the 50-day EMA.

- A bull cycle in Gold remains intact and this week’s extension reinforces current conditions. The move higher maintains the price sequence of higher highs and higher lows. Sights are on the $4200.00 handle, and $4239.7, a Fibonacci projection point. Note that the trend is in overbought territory. A move down would be considered corrective and would allow the overbought set-up to unwind. Support lies at $3889.3, 20-day EMA.

| Date | GMT/Local | Impact | Country | Event |

| 15/10/2025 | 1100/0700 | ** | MBA Weekly Applications Index | |

| 15/10/2025 | 1230/0830 | ** | Monthly Survey of Manufacturing | |

| 15/10/2025 | 1230/0830 | ** | Wholesale Trade | |

| 15/10/2025 | 1230/0830 | ** | Empire State Manufacturing Survey | |

| 15/10/2025 | 1330/0930 | Fed Governor Stephen Miran | ||

| 15/10/2025 | 1545/1645 | BOE Breeden in Panel on Financial Regulation | ||

| 15/10/2025 | 1610/1210 | Atlanta Fed's Raphael Bostic | ||

| 15/10/2025 | 1630/1230 | Fed Governor Stephen Miran | ||

| 15/10/2025 | 1700/1300 | Fed Governor Christopher Waller | ||

| 15/10/2025 | 1735/1335 | Kansas City Fed's Jeff Schmid | ||

| 15/10/2025 | 1800/1400 | Fed Beige Book | ||

| 15/10/2025 | 1800/2000 | ECB de Guindos at Alantra Anniversary Event | ||

| 15/10/2025 | 1800/1900 | BOE Breeden in Panel at Fintech Foundation | ||

| 16/10/2025 | 2350/0850 | * | Machinery orders | |

| 16/10/2025 | 0030/1130 | *** | Labor Force Survey | |

| 16/10/2025 | 0600/0700 | *** | UK Monthly GDP | |

| 16/10/2025 | 0600/0700 | ** | Trade Balance | |

| 16/10/2025 | 0600/0700 | ** | Index of Services | |

| 16/10/2025 | 0600/0700 | ** | Index of Production | |

| 16/10/2025 | 0600/0700 | ** | Output in the Construction Industry | |

| 16/10/2025 | 0800/1000 | *** | HICP (f) | |

| 16/10/2025 | 0830/0930 | BOE Credit Conditions Survey | ||

| 16/10/2025 | 0900/1100 | * | Trade Balance | |

| 16/10/2025 | 0900/0500 | * | CREA Existing Home Sales | |

| 16/10/2025 | 0900/1100 | Foreign Trade | ||

| 16/10/2025 | 1200/0800 | Richmond Fed's Tom Barkin | ||

| 16/10/2025 | 1215/0815 | ** | CMHC Housing Starts | |

| 16/10/2025 | 1230/0830 | ** | Philadelphia Fed Manufacturing Index | |

| 16/10/2025 | 1300/1400 | BOE Mann in Panel on MonPol and Trade Shocks | ||

| 16/10/2025 | 1300/0900 | Fed Governor Christopher Waller | ||

| 16/10/2025 | 1300/0900 | Fed Governor Michael Barr | ||

| 16/10/2025 | 1300/0900 | Fed Governor Stephen Miran | ||

| 16/10/2025 | 1400/1000 | ** | NAHB Home Builder Index | |

| 16/10/2025 | 1400/1000 | Fed Governor Michelle Bowman | ||

| 16/10/2025 | 1445/1545 | BOE Mann in MonPol Panel at IMF/World Bank Meetings | ||

| 16/10/2025 | 1530/1130 | * | US Bill 08 Week Treasury Auction Result | |

| 16/10/2025 | 1530/1130 | ** | US Bill 04 Week Treasury Auction Result | |

| 16/10/2025 | 1545/1745 | ECB Lane in Policy Panel at IIF Annual Meeting | ||

| 16/10/2025 | 1600/1800 | ECB Lagarde in IMF Policy Debate | ||

| 16/10/2025 | 1645/1245 | Richmond Fed's Tom Barkin | ||

| 16/10/2025 | 1730/1330 | BOC Governor Macklem speaks at Peterson Institute event in Washington. | ||

| 16/10/2025 | 1830/1930 | BOE Greene in Panel on UK/EU Relations | ||

| 16/10/2025 | 2015/1615 | Fed Governor Stephen Miran | ||

| 16/10/2025 | 2030/1630 | Richmond Fed's Tom Barkin | ||

| 16/10/2025 | 2200/1800 | Minneapolis Fed's Neel Kashkari |