MNI US MARKETS ANALYSIS - Awaiting 1st Post-Shutdown Payrolls

Highlights:

- Markets await first post-shutdown payrolls print, with post-data Fed speakers the next focus

- Fed December cut pricing fading further, with markets now seeing 1/3 odds

- USDJPY rally continues apace, even as BoJ members tilt hawkish

US TSYS: TY Tests Overnight Lows, Between Notable Technical Levels Ahead Of NFPs

Treasuries have seen a brief test of overnight lows as US desks filter in, with risk sentiment broadly supported since yesterday’s Nvidia earnings after the close. Today’s focus is clearly on the NFP September report, as part of a busy docket including a resumption of national-level jobless claims data and six different Fedspeakers all after payrolls.

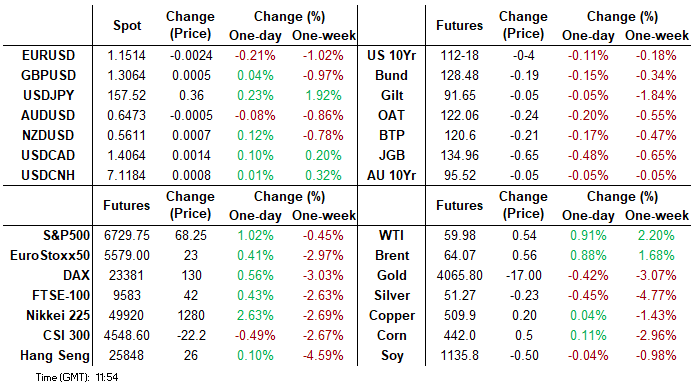

- Cash yields are 0.5-2.2bp higher, led by 3s.

- The modest flattening sees curves away from recent steeps, with 5s30s at 103.2bp vs highs of ~105.5bp in the past two days being the highest since mid-Oct and before that Sept.

- TYZ5 touched session lows of 112-17+ (-04+) - currently 112-19 - and has seen reasonable cumulative overnight volumes of 390k for pre-payrolls.

- It has pulled away from resistance at 113-04+ (Nov 14 high) in what was small clearance of congestion around 113-02 since early November. Support meanwhile is seen at 112-11 (100-dma) and 112-07+ (trendline from May 22 low), just above a key 112-06 (Sep 25 low).

- Data: Delayed NFP September report (0830ET), Resumption of weekly national jobless claims (0830ET), Philly fed mfg Nov (0830ET), Existing home sales Oct (1000ET), KC Fed mfg Nov (1100ET)

- Fedspeak: Hammack (0845ET), Barr (0930ET), Cook (1100ET), Goolsbee (1240ET and 1800ET), Miran (1815ET) and Paulson (1845ET) - see Fed bullet.

- Coupon issuance: US Tsy $19bn 10Y TIPS re-open - 91282CNS6 (1300ET)

- Bill issuance: US Tsy $110bn 4-wk, $95bn 8-wk bills (1130ET)

- Politics: White House Press Sec Leavitt press briefing (1300ET)

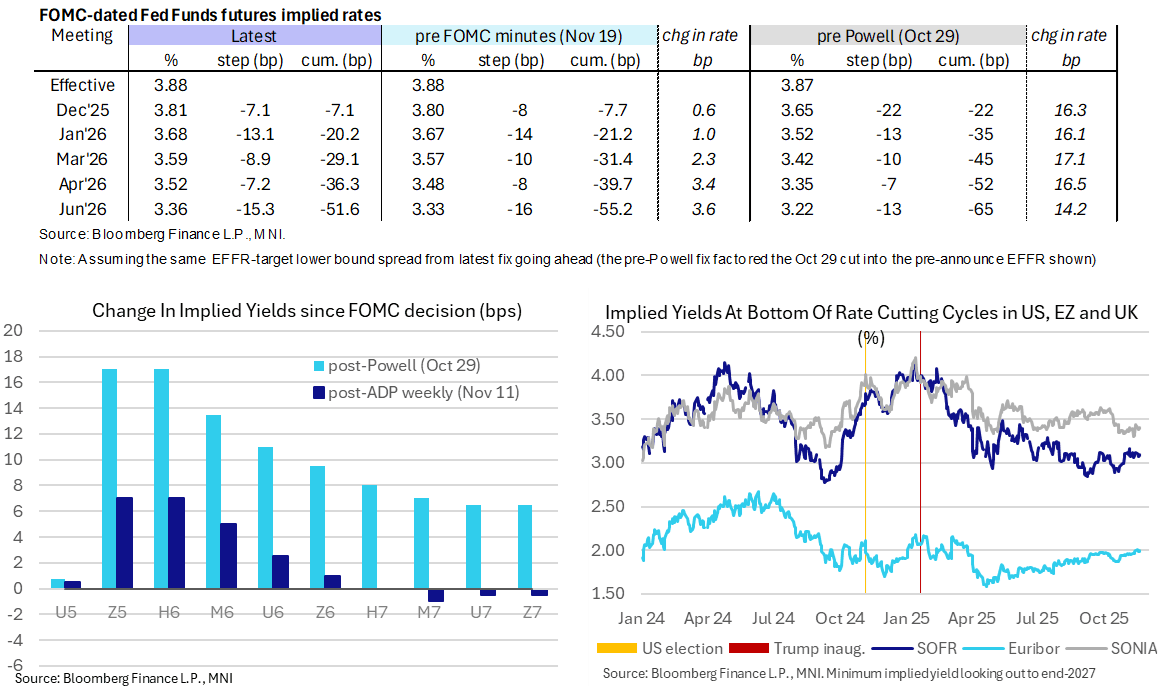

STIR: Less Than 1/3 Odds Of Fed December Cut Ahead Of Sept NFP Report

US rates consolidate yesterday’s two-pronged (and latest) hawkish shift on very near-term rate cut prospects from 1) the BLS confirming that today’s NFP report for September will be the last payrolls report the FOMC sees before its Dec 9-10 meeting and 2) the FOMC minutes further highlighting committee divisions.

- Fed Funds implied rates are unchanged overnight for December although 2bp higher for Mar-Jun meetings, aided by firmer risk sentiment stemming from Nvidia’s earnings after yesterday’s close.

- Cumulative cuts from 3.88% effective: 7bp Dec, 20bp Jan, 29bp Mar, 36.5bp Apr and 51.5bp Jun.

- SOFR futures meanwhile are up to 1.5 tick lower looking out to end-2027 contracts.

- SFRZ5 trades at 96.16, paring a lift to 96.17 overnight, vs 96.195 pre-BLS scheduling headlines.

- The terminal implied yield of 3.10% (SFRH7) has lifted a little off the low end of its 3.065-3.16% range for closes in recent weeks, a range primarily dictated by data developments.

- MNI NFP Preview, with this September report now having added importance with the October establishment figures being rolled into the November release on Dec 16: https://media.marketnews.com/USNFP_Sep2025_Preview_postshutdown_6c53ab7531.pdf

- Along with payrolls, there’s also the formal resumption of national jobless claims data after a technical error led to a single week of data being published earlier this week. It should be hard to see material surprises to historical data considering the large share of state-level data already known, although continuing claims data are always prone to reasonable revisions.

Fedspeak Focus On Paulson After NFP Reactions

There are plenty of opportunities to hear FOMC participant reactions to today’s NFP September report with six different speakers scheduled. Barring those reactions, Fedspeak focus should be on Philly Fed’s Paulson after the close, who has so far given little away since replacing Harker on Jul 1. In her debut speech on Oct 13, she said the Fed should move cautiously and that with rates "modestly restrictive now", she saw easing through year-end in line with the September SEP median - i.e. cutting in Oct and Dec meetings. The median FOMC participant has clearly turned more hawkish on December rate cut prospects since then, and this should be a useful update for a ’26 voter who last month described 2026 as a “long way off right now”.

- 0845ET – Hammack (’26 voter, hawk) delivers opening remarks at financial conference in a 10min slot but Bloomberg suggests set to give Q&A as well

- 0930ET – Fed Gov. Barr (voter, most hawkish of permanent voters) in AI discussion (no text)

- 1100ET – Fed Gov. Cook (voter) on financial stability (text + Q&A)

- 1240ET – Goolsbee (’25 voter, a less clear cut dove than in the past) in a moderated discussion (no text)

- 1800ET – Goolsbee in interview with PBS NewsHour

- 1815ET – Fed Gov. Miran (voter, outright dove) speaks at American Investment Council (no text)

- 1845ET – Paulson (’26 voter) on the economic outlook (text only)

US TSY FUTURES: Early December'25-March'26 Roll Update

The latest Tsy quarterly futures roll volumes for December'25 to March'26 outlined below. Early morning volumes light while percentage complete gradually rising ahead the "First Notice" date of Friday, November 28. Current roll details:

- TUZ5/TUH6 appr 90,800 from -6.0 to -5.75, -5.88 last; 15% complete

- FVZ5/FVH6 appr 11,300 from -2.5 to -2.25, -2.5 last; 18% complete

- TYZ5/TYH6 appr 84,800 from 1.5 to 2.0, 2.0 last; 18% complete

- UXYZ5/UXYH6 26,200 from 5.0 to 5.5, 5.5 last; 13% complete

- USZ5/USH6 12,800 from 12.75 to 13.5, 13.0 last; 11% complete

- WNZ5/WNH6 appr 5,900 from 9.75 to 10.25, 9.75 last; 16% complete

- Reminder, Dec'25 futures don't expire until next month: 10s, 30s and Ultras on December 19, 2s and 5s on December 31. Meanwhile, Dec'25 Tsy options will expire this Friday, November 21.

SOFR: Short Setting In Very Front End Of Futures Dominates On Wednesday

OI data suggests that short setting across the white pack provided the most meaningful net positioning swing as most SOFR futures settled lower on Wednesday.

- A mix of net short setting and long cover was then seen further out the curve.

- Hawkish leaning Fed meeting minutes and the BLS noting that it will not release the October NFP release in isolation triggered much of the modest hawkish adjustment.

| 19-Nov-25 | 18-Nov-25 | Daily OI Change |

| Daily OI Change In Packs |

SFRU5 | 1,390,620 | 1,381,015 | +9,605 | Whites | +125,143 |

SFRZ5 | 1,448,461 | 1,423,560 | +24,901 | Reds | -2,855 |

SFRH6 | 1,351,230 | 1,292,399 | +58,831 | Greens | +9,426 |

SFRM6 | 1,125,797 | 1,093,991 | +31,806 | Blues | +6,745 |

SFRU6 | 1,139,666 | 1,147,255 | -7,589 |

|

|

SFRZ6 | 1,169,701 | 1,175,116 | -5,415 |

|

|

SFRH7 | 879,030 | 862,525 | +16,505 |

|

|

SFRM7 | 800,663 | 807,019 | -6,356 |

|

|

SFRU7 | 821,164 | 815,101 | +6,063 |

|

|

SFRZ7 | 827,737 | 811,260 | +16,477 |

|

|

SFRH8 | 452,590 | 456,118 | -3,528 |

|

|

SFRM8 | 401,127 | 410,713 | -9,586 |

|

|

SFRU8 | 349,905 | 348,395 | +1,510 |

|

|

SFRZ8 | 324,355 | 318,169 | +6,186 |

|

|

SFRH9 | 195,637 | 197,239 | -1,602 |

|

|

SFRM9 | 187,844 | 187,193 | +651 |

|

|

FOREX: USD Index Consolidating Close to Recovery Highs

- Broad strength for the greenback on Wednesday prompted an impressive lurch higher for the DXY, which has traded to within four pips of the recovery highs overnight. Safe haven dynamics were behind much of the move during yesterday’s session, however, gains were exacerbated by confirmation that the Fed will not receive any additional jobs reports before the December meeting.

- On data fog grounds, front-end rates now price a smaller chance of a December Fed cut (around 35%), cementing the bullish short-term theme for the greenback.

- Uncertainty over a Fed cut combines within uncertainty over a BOJ hike in December, continuing to drive the USDJPY rally overnight. The spike to 157.78 had additional tailwinds contributing, that being the ongoing fiscal concerns and associated pressure on JGBs as well as global technology stocks advancing after Nvidia reported better than expected chip sales.

- USDJPY has pulled back 60 pips or so, with some citing the moderate hawkish tilt to BOJ Koeda’s remarks overnight, however, this is more likely some profit taking given the 2% surge this week, and the upcoming US data.

- For NZDUSD, spot has stabilised back above 0.5600 today after falling over 1% on Wednesday to the lowest level since April. Despite the stabilisation, we remain at very depressed levels, and the bearish trend remains firmly entrenched. Support appears scant until the year’s lows at 0.5486.

- GBPUSD support was found around 1.3040 overnight and the pair is currently pushing fresh session highs around 1.3080. Yesterday’s sharp sell-off reinforces a bearish theme and highlights the fact that gains since Nov 4 have been corrective. A move through 1.3010, the Nov 4 / 5 low, would confirm the next phase lower, increasing in significance ahead of next week’s budget.

- September US payrolls will be the main event of the day, while BoE's Dhingra and Mann are scheduled to speak alongside Fed's Hammack, Barr, Cook, Goolsbee, Miran, and Paulson.

FOREX: NZDUSD Stabilises Back Above 0.5600 on Firmer Risk Sentiment

- Overall, currency market adjustments have been limited on Thursday, again likely due to the upcoming US data later in the session. With that said, the firmer risk sentiment following Nvidia’s results have provided a more stable backdrop for the likes of NZD and GBP, while the Euro remains a touch weaker.

- For NZDUSD, spot has stabilised back above 0.5600 today after falling over 1% on Wednesday to the lowest level since April. Despite the stabilisation, we remain at very depressed levels, and the bearish trend remains firmly entrenched. Support appears scant until the year’s lows at 0.5486.

- GBPUSD support was found around 1.3040 overnight and the pair is currently pushing fresh session highs around 1.3080. Yesterday’s sharp sell-off reinforces a bearish theme and highlights the fact that gains since Nov 4 have been corrective. A move through 1.3010, the Nov 4 / 5 low, would confirm the next phase lower, increasing in significance ahead of next week’s budget.

- The trend structure in EURUSD remains bearish and the pullback from the Nov 13 high, reinforces a bear theme. Sights are on key support at 1.1469, the Nov 5 low. The Eurozone November flash PMIs will provide a timely update on economic activity in the region, scheduled for release Friday. Recent growth signals have been resilient, with Q3 GDP printing above ECB expectations and the October PMI round pointing to a solid pickup in services sector activity.

OPTIONS: Expiries for Nov20 NY cut 1000ET (Source DTCC)

- EUR/USD: $1.1500(E2.0bln), $1.1550(E559mln), $1.1600(E1.1bln), $1.1625-30(E1.8bln), $1.1675-80(E1.5bln)

- USD/JPY: Y150.00($1.3bln), Y155.00($1.4bln)

- GBP/USD: $1.3250(Gbp679mln)

- EUR/GBP: Gbp0.8750(E524mln)

- AUD/USD: $0.6500(A$737mln)

- AUD/NZD: N$1.1400(A$537mln)

- USD/CNY: Cny7.1080-89($2.0bln)

EQUITIES: Eurostoxx 50 Futures Recovery Places Contract Back Above 50-Day EMA

- A medium-term bull trend in Eurostoxx 50 futures remains intact, however, recent weakness highlights a stronger corrective cycle. The contract has breached two key support points; 5601.75, the 50-day EMA, and 5615.50, the base of a bull channel drawn from the Aug 1 low. The breach signals scope for a deeper pullback and opens 5503.00, a Fibonacci retracement. Initial firm resistance to watch is 5652.52, the 20-day EMA.

- S&P E-Minis maintain a softer S/T tone - for now - despite the recovery from Tuesday’s low. The recent breach of 6655.70, the Nov 7 low cancels recent bullish signals and signals scope for an extension of the current corrective cycle. Note that price has also traded through support at the 50-day EMA. A resumption of weakness would open 6540.25, the Oct 10 low and the next key support. Initial firm resistance to watch is 6767.81, the 20-day EMA.

COMMODITIES: WTI Futures Remain Contained Within The Month's Tight Range

- WTI futures are trading in a range. A sell-off on Nov 12 strengthens a bearish theme. A resumption of the bear leg would pave the way for a move towards key support and the bear trigger at $55.99, the Oct 20 low. Clearance of this level would resume the downtrend. Note that it is still possible a bullish corrective cycle remains in play. Resistance to watch is $61.84, the Oct 24 high. Clearance of this hurdle would signal scope for a stronger correction.

- The bearish phase in Gold between Oct 20 and 28 appears to have been a correction and has allowed a recent overbought condition to unwind. The recovery since Oct 28 suggests that correction is over. Key support to watch lies at the 50-day EMA, at $3943.0. Clearance of this EMA would signal scope for a deeper retracement. The first short-term bull trigger has been defined at $4245.23, the Nov 13 high.

| Date | GMT/Local | Impact | Country | Event |

| 20/11/2025 | 1330/0830 | *** | Jobless Claims | |

| 20/11/2025 | 1330/0830 | ** | WASDE Weekly Import/Export | |

| 20/11/2025 | 1330/0830 | * | Industrial Product and Raw Material Price Index | |

| 20/11/2025 | 1330/0830 | ** | Philadelphia Fed Nonmanufacturing Index | |

| 20/11/2025 | 1330/0830 | *** | Employment Report | |

| 20/11/2025 | 1345/0845 | Cleveland Fed's Beth Hammack | ||

| 20/11/2025 | 1430/0930 | Fed Governor Michael Barr | ||

| 20/11/2025 | 1500/1000 | *** | NAR existing home sales | |

| 20/11/2025 | 1500/1000 | * | Services Revenues | |

| 20/11/2025 | 1500/1600 | ** | Consumer Confidence Indicator (p) | |

| 20/11/2025 | 1530/1030 | ** | Natural Gas Stocks | |

| 20/11/2025 | 1600/1100 | ** | Kansas City Fed Manufacturing Index | |

| 20/11/2025 | 1600/1100 | Fed Governor Lisa Cook | ||

| 20/11/2025 | 1630/1130 | ** | US Bill 04 Week Treasury Auction Result | |

| 20/11/2025 | 1630/1130 | * | US Bill 08 Week Treasury Auction Result | |

| 20/11/2025 | 1740/1240 | Chicago Fed's Austan Goolsbee | ||

| 20/11/2025 | 1800/1300 | ** | US Treasury Auction Result for TIPS 10 Year Note | |

| 20/11/2025 | 1830/1830 | BOE Dhingra Speech on Trade and Tariffs | ||

| 20/11/2025 | 2100/2100 | BOE Mann at IMF Statistical Forum | ||

| 21/11/2025 | 2200/0900 | *** | Judo Bank Flash Australia PMI | |

| 20/11/2025 | 2315/1815 | Fed Governor Stephen Miran | ||

| 21/11/2025 | 2330/0830 | *** | CPI | |

| 20/11/2025 | 2345/1845 | Philly Fed's Anna Paulson | ||

| 21/11/2025 | 0001/0001 | ** | Gfk Monthly Consumer Confidence | |

| 21/11/2025 | 0030/0930 | ** | Jibun Bank Flash Japan PMI | |

| 21/11/2025 | 0700/0700 | *** | Public Sector Finances | |

| 21/11/2025 | 0700/0700 | *** | Retail Sales | |

| 21/11/2025 | 0745/0845 | ** | Manufacturing Sentiment | |

| 21/11/2025 | 0800/0900 | ECB de Guindos Remarks/Q&A at Foro Gran Via | ||

| 21/11/2025 | 0815/0915 | ** | S&P Global Services PMI (p) | |

| 21/11/2025 | 0815/0915 | ** | S&P Global Manufacturing PMI (p) | |

| 21/11/2025 | 0830/0930 | ** | S&P Global Services PMI (p) | |

| 21/11/2025 | 0830/0930 | ** | S&P Global Manufacturing PMI (p) | |

| 21/11/2025 | 0830/0930 | ECB Lagarde Speech at European Banking Congress | ||

| 21/11/2025 | 0900/1000 | ** | S&P Global Services PMI (p) | |

| 21/11/2025 | 0900/1000 | ** | S&P Global Manufacturing PMI (p) | |

| 21/11/2025 | 0900/1000 | ** | S&P Global Composite PMI (p) | |

| 21/11/2025 | 0930/0930 | *** | S&P Global Manufacturing PMI flash | |

| 21/11/2025 | 0930/0930 | *** | S&P Global Services PMI flash | |

| 21/11/2025 | 0930/0930 | *** | S&P Global Composite PMI flash | |

| 21/11/2025 | 1000/1100 | Negotiated Wage Growth | ||

| 21/11/2025 | 1130/1230 | ECB de Guindos Remarks/Q&A at Deusto Business School | ||

| 21/11/2025 | 1230/0730 | New York Fed's John Williams | ||

| 21/11/2025 | 1330/0830 | ** | Retail Trade | |

| 21/11/2025 | 1330/0830 | Fed Governor Michael Barr | ||

| 21/11/2025 | 1345/0845 | Fed Vice Chair Philip Jefferson | ||

| 21/11/2025 | 1400/0900 | Dallas Fed's Lorie Logan | ||

| 21/11/2025 | 1400/0900 | Boston Fed's Susan Collins | ||

| 21/11/2025 | 1445/0945 | *** | S&P Global Manufacturing Index (Flash) | |

| 21/11/2025 | 1445/0945 | *** | S&P Global Services Index (flash) | |

| 21/11/2025 | 1500/1000 | *** | U. Mich. Survey of Consumers | |

| 21/11/2025 | 1500/1000 | ** | University of Michigan Surveys of Consumers Inflation Expectation | |

| 21/11/2025 | 1540/1540 | BOE Pill in Panel at Swiss National Bank | ||

| 21/11/2025 | 1800/1300 | ** | Baker Hughes Rig Count Overview - Weekly |