FOREX: USD Index Consolidating Close to Recovery Highs

Nov-20 10:20

- Broad strength for the greenback on Wednesday prompted an impressive lurch higher for the DXY, which has traded to within four pips of the recovery highs overnight. Safe haven dynamics were behind much of the move during yesterday’s session, however, gains were exacerbated by confirmation that the Fed will not receive any additional jobs reports before the December meeting.

- On data fog grounds, front-end rates now price a smaller chance of a December Fed cut (around 35%), cementing the bullish short-term theme for the greenback.

- Uncertainty over a Fed cut combines within uncertainty over a BOJ hike in December, continuing to drive the USDJPY rally overnight. The spike to 157.78 had additional tailwinds contributing, that being the ongoing fiscal concerns and associated pressure on JGBs as well as global technology stocks advancing after Nvidia reported better than expected chip sales.

- USDJPY has pulled back 60 pips or so, with some citing the moderate hawkish tilt to BOJ Koeda’s remarks overnight, however, this is more likely some profit taking given the 2% surge this week, and the upcoming US data.

- For NZDUSD, spot has stabilised back above 0.5600 today after falling over 1% on Wednesday to the lowest level since April. Despite the stabilisation, we remain at very depressed levels, and the bearish trend remains firmly entrenched. Support appears scant until the year’s lows at 0.5486.

- GBPUSD support was found around 1.3040 overnight and the pair is currently pushing fresh session highs around 1.3080. Yesterday’s sharp sell-off reinforces a bearish theme and highlights the fact that gains since Nov 4 have been corrective. A move through 1.3010, the Nov 4 / 5 low, would confirm the next phase lower, increasing in significance ahead of next week’s budget.

- September US payrolls will be the main event of the day, while BoE's Dhingra and Mann are scheduled to speak alongside Fed's Hammack, Barr, Cook, Goolsbee, Miran, and Paulson.

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

ECB: ETS2 Delay Could Bring Forward Rate Cut Expectations

Oct-21 10:15

The fall in EUR traded inflation metrics through October has been one contributor to recent dovish ECB repricing. For some Governing Council members, the downward impact that a delay to ETS2 would have on the ECB’s December inflation projections could be enough to support another rate cut.

- If an ETS2 delay to 2030 is confirmed, there may be scope for ECB-dated OIS to increase the implied probability of a cut in December (3.5bps of cuts priced) or March (12bps of cumulative cuts priced). However, we don’t expect it to drive a material repricing of terminal rate expectations for now.

- The expected introduction of ETS2 in 2027 is currently pushing up the ECB’s headline inflation projections towards the 2% target. A delay would mechanically lower the 2027, and likely 2028, projections at the December projection round.

- Last week, ECB’s Simkus noted that “For me, the forecast for inflation in 2028 will be an important piece of information for the decision in December,”..... “If it’s more than marginally below the target, we should act on that.”

- However, it’s unclear how much stock some of the more centrist/hawkish ECB officials are putting into the impact of ETS2. Whether the change is delayed or not, it would just impact the timing of a one-time price level shift, and have limited impact on the medium-term underlying inflation outlook. ECB’s de Guindos said at last month's MNI Connect Event that “We can speculate what's going to happen with ETS2 whether it will be there or not but I don't tend to pay much attention to this kind of very concrete and specific developments that can give rise to the opposite movement in inflation for the year or the year after."

- Last week, Belgian CB Governor Wunsch (considered hawkish leaning) said that he would not get “nervous when inflation deviates by 10, 20, 30 basis points from the target".

EGB SYNDICATION: 3.25% Jan-34 ESTONI tap: Revised guidance

Oct-21 10:14

- Guidance revised to MS + 75bps area (from MS + 80bps area)

- Tap Size: E500bln (WNG)

- Books in excess of E1.4bln (inc E120mln JLM interest)

- Settlement: 28 October 2025 (T+5)

- Joint Leads: Erste Group, J.P. Morgan (B&D) and Societe Generale

- Timing: Books open, today’s business

From market source

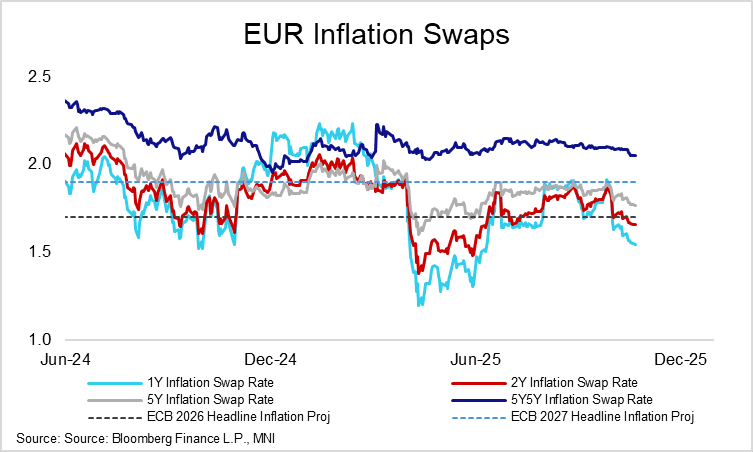

ECB: EUR 5y5y Inflation Swap At Lowest Since June

Oct-21 10:12

The EUR 5y5y inflation swap has fallen 5bps through October, currently hovering around 2.05%. This is the lowest since the start of June, a time when tariff-driven growth concerns dominated the outlook for near-term ECB policy.

- Shorter-dated swaps have also moved further below the 2% target, with 1- and 2-year swaps currently tracking below the ECB’s 2026 headline inflation projection of 1.7% (caveating that swaps are priced on a HICP ex-tobacco basis).

- There have been several drivers of the recent fall in market implied EUR inflation expectations:

- A renewed pullback in Brent crude futures amid excess supply concerns and an uptick in US/China trade tensions.

- Weak growth signals from the likes of Germany through October, increasing concerns that sequential GDP growth in Europe’s largest economy could be negative again in Q3. Note that Friday’s October flash PMIs will provide a more timely look at regional growth momentum (including the impact of recent US/China rhetoric).

- An increasing likelihood of a delay to the EU’s ETS2 carbon pricing scheme.

- A delay to ETS2 beyond the current 2027 implementation date has been a well-known risk for some time (e.g. MNI Policy Team’s piece on September 17). Following a letter from member states last week, the EU’s Environmental Council could announce (or set the stage for) a delay to 2030 at today’s meeting (timing details here).