FOREX: NZDUSD Stabilises Back Above 0.5600 on Firmer Risk Sentiment

Nov-20 10:14

- Overall, currency market adjustments have been limited on Thursday, again likely due to the upcoming US data later in the session. With that said, the firmer risk sentiment following Nvidia’s results have provided a more stable backdrop for the likes of NZD and GBP, while the Euro remains a touch weaker.

- For NZDUSD, spot has stabilised back above 0.5600 today after falling over 1% on Wednesday to the lowest level since April. Despite the stabilisation, we remain at very depressed levels, and the bearish trend remains firmly entrenched. Support appears scant until the year’s lows at 0.5486.

- GBPUSD support was found around 1.3040 overnight and the pair is currently pushing fresh session highs around 1.3080. Yesterday’s sharp sell-off reinforces a bearish theme and highlights the fact that gains since Nov 4 have been corrective. A move through 1.3010, the Nov 4 / 5 low, would confirm the next phase lower, increasing in significance ahead of next week’s budget.

- The trend structure in EURUSD remains bearish and the pullback from the Nov 13 high, reinforces a bear theme. Sights are on key support at 1.1469, the Nov 5 low. The Eurozone November flash PMIs will provide a timely update on economic activity in the region, scheduled for release Friday. Recent growth signals have been resilient, with Q3 GDP printing above ECB expectations and the October PMI round pointing to a solid pickup in services sector activity.

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

EGB SYNDICATION: 3.25% Jan-34 ESTONI tap: Revised guidance

Oct-21 10:14

- Guidance revised to MS + 75bps area (from MS + 80bps area)

- Tap Size: E500bln (WNG)

- Books in excess of E1.4bln (inc E120mln JLM interest)

- Settlement: 28 October 2025 (T+5)

- Joint Leads: Erste Group, J.P. Morgan (B&D) and Societe Generale

- Timing: Books open, today’s business

From market source

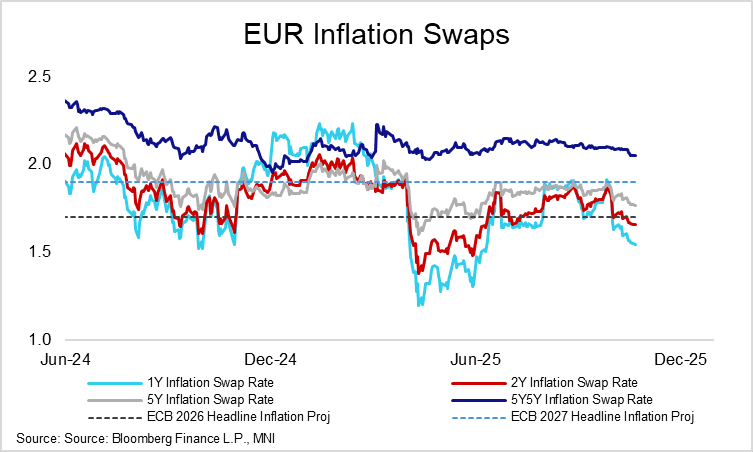

ECB: EUR 5y5y Inflation Swap At Lowest Since June

Oct-21 10:12

The EUR 5y5y inflation swap has fallen 5bps through October, currently hovering around 2.05%. This is the lowest since the start of June, a time when tariff-driven growth concerns dominated the outlook for near-term ECB policy.

- Shorter-dated swaps have also moved further below the 2% target, with 1- and 2-year swaps currently tracking below the ECB’s 2026 headline inflation projection of 1.7% (caveating that swaps are priced on a HICP ex-tobacco basis).

- There have been several drivers of the recent fall in market implied EUR inflation expectations:

- A renewed pullback in Brent crude futures amid excess supply concerns and an uptick in US/China trade tensions.

- Weak growth signals from the likes of Germany through October, increasing concerns that sequential GDP growth in Europe’s largest economy could be negative again in Q3. Note that Friday’s October flash PMIs will provide a more timely look at regional growth momentum (including the impact of recent US/China rhetoric).

- An increasing likelihood of a delay to the EU’s ETS2 carbon pricing scheme.

- A delay to ETS2 beyond the current 2027 implementation date has been a well-known risk for some time (e.g. MNI Policy Team’s piece on September 17). Following a letter from member states last week, the EU’s Environmental Council could announce (or set the stage for) a delay to 2030 at today’s meeting (timing details here).

FINLAND AUCTION RESULTS: 2.625% Apr-32 / 3.00% Sep-35 RFGB

Oct-21 10:11

| 2.625% Apr-32 RFGB | 3.00% Sep-35 RFGB | |

| ISIN | FI4000591862 | FI4000587415 |

| Amount | E548mln | E869mln |

| Previous | E150mln | E874mln |

| Avg yield | 2.578% | 2.936% |

| Previous | 2.720% | 3.067% |

| Bid-to-cover | 1.48x | 1.40x |

| Previous | 2.00x | 1.48x |

| Avg Price | 100.28 | 100.54 |

| Pre-auction mid | 100.164 | 100.398 |

| Prev avg price | 99.450 | 99.430 |

| Prev mid-price | 99.430 | 99.429 |

| Previous date | 28-Aug-25 | 16-Sep-25 |

Source: Bloomberg Finance L.P.