MNI US MARKETS ANALYSIS - AUD Outperforms on Equity Strength

Highlights:

- A solid rally for the major equity benchmarks to start the year has propelled AUD to the top of the G10 FX leaderboard this morning.

- Headline flow has been relatively light, save for US President Trump issuing a warning to Iran on the treatment of peaceful protestors.

- Today's data calendar is also light, with the final December US Manufacturing PMI not expected to move the needle, but Fed's Paulson and Kashkari scheduled to speak over the weekend.

US TSYS: Ringing in the New Year with Final S&P Global Mfg PMI

- Treasuries are ringing in the new year mildly weaker - off early London session lows on rather decent volumes: TYH6 currently -1.5 at 112-12.5 vs. 112-05 low on just over 280,000 contracts; 10Y yield retreating from 4.1907% overnight high to 4.1573% (-.0097).

- Technical trend theme remains bearish and a break of 111-29 would confirm a resumption of the bear cycle. This would open 111-19, a Fibonacci projection.

- Limited data today: final S&P Global US Manufacturing PMI at 0945ET. No scheduled Fed speakers today - while Philadelphia Fed President Anna Paulson answers questions at a AEA conference tomorrow at 1015ET.

- Looking ahead: the first two full weeks of the year see nonfarm payrolls (next Friday) and CPI reports (Jan 13) for December with those two key reports back on their original schedules having been prioritized by the BLS.

- Private sector reports meanwhile are highlighted by ISM manufacturing and services reports Jan 5 and 7.

- PPI and retail sales are also released (Jan 14) but they’re still lagging and will only be for November (along with a full set of October details in the case for PPI). Note that PPI for December will then follow at the end of the month as the BLS continues to work on returning that report to its original schedule.

- These all build up to the FOMC meeting on Jan 27-28, which is currently seen with low odds of a fourth consecutive 25bp cut with just 3bp of cuts priced. The next cut is fully priced for the June meeting under a new Fed chair.

US TSY FUTURES: Short Setting Most Prominent During Wednesday's Downtick

OI data points to a mix of net short setting (TU, UXY, US & WN) and long cover (FV & TY) as Tsy futures ticked lower on Wednesday. Net short setting weas more prominent in curve-wide DV01 terms, although the biggest individual positioning swing came via net long cover in TY futures.

| 31-Dec-25 | 30-Dec-25 | Daily OI Change | OI DV01 Equivalent Change ($) | |

| TU | 4,589,575 | 4,530,062 | +59,513 | +2,307,930 |

| FV | 6,696,998 | 6,703,900 | -6,902 | -302,438 |

| TY | 5,458,381 | 5,499,033 | -40,652 | -2,713,335 |

| UXY | 2,544,674 | 2,530,043 | +14,631 | +1,318,529 |

| US | 1,857,955 | 1,846,846 | +11,109 | +1,569,529 |

| WN | 2,094,986 | 2,089,356 | +5,630 | +1,030,683 |

| Total | +43,329 | +3,210,897 |

SOFR: Mix of Short Setting & Long Cover Seen in Futures on Wednesday

OI data points to net short setting dominating in the whites and reds, before net long cover came to the fore in the greens and blues as SOFR futures ticked lower in the wake of the weekly jobless claims data on Wednesday.

| 31-Dec-25 | 30-Dec-25 | Daily OI Change |

| Daily OI Change In Packs |

SFRZ5 | 1,517,303 | 1,522,510 | -5,207 | Whites | +37,289 |

SFRH6 | 1,290,530 | 1,281,728 | +8,802 | Reds | +32,188 |

SFRM6 | 1,160,353 | 1,149,913 | +10,440 | Greens | -13,814 |

SFRU6 | 1,202,940 | 1,179,686 | +23,254 | Blues | -22,762 |

SFRZ6 | 1,167,088 | 1,150,941 | +16,147 |

|

|

SFRH7 | 869,987 | 862,568 | +7,419 |

|

|

SFRM7 | 757,313 | 755,285 | +2,028 |

|

|

SFRU7 | 804,118 | 797,524 | +6,594 |

|

|

SFRZ7 | 851,903 | 853,469 | -1,566 |

|

|

SFRH8 | 474,351 | 476,412 | -2,061 |

|

|

SFRM8 | 395,775 | 396,767 | -992 |

|

|

SFRU8 | 367,732 | 376,927 | -9,195 |

|

|

SFRZ8 | 342,038 | 349,605 | -7,567 |

|

|

SFRH9 | 210,380 | 216,130 | -5,750 |

|

|

SFRM9 | 208,816 | 213,249 | -4,433 |

|

|

SFRU9 | 172,196 | 177,208 | -5,012 |

|

|

US/IRAN: Pezeshkian Offers Economic Reforms Amid Escalating Protest Movement

Earlier today, US President Donald Trump threatened the Iranian gov't with the prospect of military action, saying that the US would come to the rescue of protesters in the country if Iranian forces continue to fire upon them. This marks a further escalation in Trump's rhetoric regarding Iran, after saying last week that the US could participate in airstrikes alongside Israel if Tehran resumes its nuclear and ballistic missile programmes.

- Secretary of the Supreme National Security Council Ali Larijani posts on X: "With the stances taken by Israeli officials and Trump, the behind-the-scenes of the matter has become clear. We consider the positions of the protesting merchants separate from those of the destructive elements, and Trump should know that American interference in this internal issue is equivalent to chaos across the entire region and the destruction of American interests. [...]"

- These comments come after five days of protests that have spread across the country and seen at least seven demonstrators killed in clashes with security forces.

- The protests were sparked by a collapse in the rial, resulting in a spike in inflation and eroding purchasing power. However, some of the protests have broadened in scope and are more squarely aimed at the ruling regime as an entity.

- Compared to the last major protests in 2022, which resulted in widespread crackdowns, the regime has taken a (somewhat) more measured approach, with the internet remaining available and state media reporting on the demonstrations.

- Larijani's comments above, citing a difference between 'protesting merchants' (angry at the economic situation) and 'destructive elements' (those protesting the regime as a whole), is a notable shift in tone from previous protests. It remains to be seen whether the economic reform measures announced by President Masoud Pezeshkian prove sufficient to quell the demonstrations, or if this broadens into a wider anti-gov't movement.

EUROZONE DATA: Dec Manuf PMI: Unsurprising Downward Revision; Two Way Risks In

The downward revision to the Eurozone December manufacturing PMI doesn’t come as a surprise after this morning’s country-level readings. We estimate the Germany/France manufacturing PMI was revised down to 48.0 (vs 48.5 flash, 48.1 prior), driven by the German reading. Meanwhile, the ex-Germany/France reading saw a smaller downward revision to 49.8 (vs 50.1 cons, 51.5 prior). The Eurozone manufacturing industry faces two-way risks this year. On the positive side, increases in German spending and an anticipated broader recovery in regional consumption may support industrial demand. However, continued Chinese import penetration (exacerbated by the competitive level of the yuan) and the impact of higher US tariffs present ongoing headwinds. Progress on the Russia/Ukraine peace deal also remains an area of high uncertainty. Notes from the Eurozone-wide release:

- “After nine successive months of growth, factory production volumes across the eurozone decreased in December. The decline was only mild overall, however. Pulling output lower was an accelerated fall in new order intakes. The latest deterioration in sales performances – the second in as many months – was also the sharpest since the beginning of 2025. Exports drove total new business volumes lower, sub-index data showed, with demand from international clients decreasing at the fastest rate in 11 months”

- “Notably, there was growing evidence of supply-chain pressure for eurozone manufacturers. Average lead times on items purchased from vendors lengthened to the greatest extent since October 2022”….”Stronger cost pressures did not dissuade eurozone factories from discounting their goods prices. Charges fell for the seventh time over the last eight months during December.”

- “As for employment, factory job losses were extended into the final month of 2025, stretching the current sequence of decrease to just over two-and-a-half years”

- “Lastly, manufacturers’ sentiment towards the year-ahead outlook for production improved in December.”

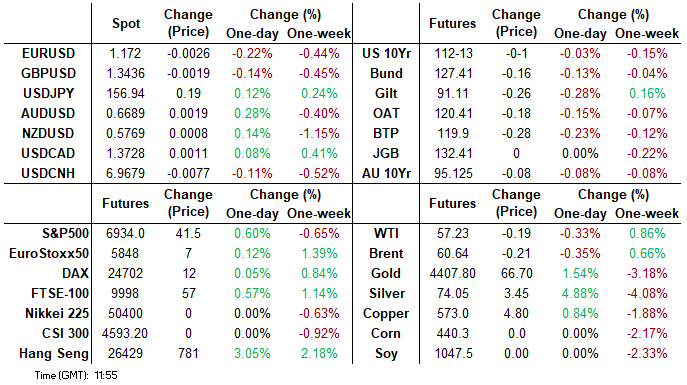

FOREX: AUDUSD Rises Back to 0.6700 Amid Equity Strength

- A solid rally for the major equity benchmarks to start the year has propelled AUD to the top of the G10 FX leaderboard this morning, with AUDUSD rising ~0.4%. With the notable bounce, spot has returned to pre-Christmas levels around the 0.6700 handle, maintaining the supportive tone that was on display throughout December. Recent clearance of a key resistance point at 0.6707 (Sep 17 high) confirms a resumption of the medium-term uptrend that started Apr 9. This signals scope for an extension towards 0.6759 next, the Apr 11 2024 high.

- The Euro is the main underperformer in G10 this morning following downward revisions in the Eurozone December Manufacturing PMI. Attempts above the 1.1800 handle across December have proved short-lived, with the pair tracking back towards 1.17 at typing. The breach of the 20-day EMA at 1.1724, will be monitored as a clear break would signal scope for a deeper retracement, allowing an overbought condition to unwind.

- Over the holiday period, USDJPY has unsurprisingly traded in a more contained manner, broadly respecting a 156.00-157.00 range. Topside momentum stalled at 157.00 this morning for a second time this week, however, spot continues to hover close to recent highs. Moving average studies highlight a dominant uptrend, with attention remaining on 157.89, the Nov 20 high and the bull trigger.

- Today's data calendar is light, with the final December US Manufacturing PMI not expected to move the needle, but Fed's Paulson and Kashkari scheduled to speak over the weekend. Both of them are under elevated scrutiny as they newly come into rotation of FOMC voters with the start of the new year.

RATINGS: No Sovereign Reviews of Note Scheduled After Close, ’26 Calendar Here

No major sovereign credit rating reviews scheduled for after hours on Friday.

- Click here to access the indicative 2026 sovereign rating review schedules across the five most prominent rating agencies (Fitch, Moody's, S&P, Morningstar DBRS & Scope Ratings).

- Note that the schedules are indicative only and ratings can be reviewed on an ad-hoc basis.

- Rating agencies may also adjust their schedules during the year.

EUROPEAN ISSUANCE

Slovenia New 10-year: Mandate

- "The Republic of Slovenia has mandated Barclays, DZ BANK, HSBC, J.P. Morgan, OTP Banka Slovenia and Raiffeisen Bank International to lead manage a new benchmark EUR transaction with a 10-year tenor. The deal is expected to be launched in the near future, subject to market conditions"

- Slovenia's 2026 funding plan noted financing needs of E5.26bln (up from E4.58bln in 2025). For context, Slovenia held two EUR syndications last year, both for E1bln in January (Apr-55 SLOREP) and June (Jul-35 SLOREP Sustainable). In 2024, there were three syndicated transactions for the Mar-34 SLOREP (E1.5bln in Jan, E0.5bln in Mar and E0.75bln in Sep).

- Early January syndications for the past four years: E1.75bln in 2022, E1.5bln in 2023, E1.5bln in 2024 and E1bln in 2025.

Details as per Bloomberg

Ireland Q1 Issuance Plan: Mar 12 Auction and Q1 Syndi

- NTMA has announced that Ireland will hold one bond auction and a syndication in Q1.

- Bond auction: Thursday March 12, with details announced on Monday March 9.

- Syndication: One transaction in Q1, which is in line with our expectations. There is no guidance on the syndication but we look for a new 10-year Oct-36 bond to be launched.

EQUITIES: Bull Cycle in Eurostoxx Futures Intact, Contract Close to Cycle Highs

- A bull cycle in Eurostoxx 50 futures remains intact. The first key support to watch lies at 5691.88, the 50-day EMA. A clear break of the EMA would highlight a potential short-term reversal. This would open 5622.00, the Nov 26 low. For bulls, sights are on key resistance at 5847.00, the Nov 13 high. The price pattern on Dec 18 is a bullish engulfing candle - a reversal signal.

- Short-term weakness in S&P E-Minis appears corrective. A key short-term support has been defined at 6771.50, the Dec 18 low. A break of this level is required to signal scope for a deeper retracement and would highlight a possible short-term reversal. For bulls, sights are on key resistance at 7014.00, the Oct 30 high. Clearance of this hurdle would confirm a resumption of the primary uptrend.

COMMODITIES: Trend Condition in WTI Futures Remains Bearish

- The trend condition in WTI futures remains bearish and gains are considered corrective - for now. MA studies are in a bear-mode position, highlighting a dominant downtrend. A key support and the bear trigger at $56.11, the Oct 17 low, has recently been breached. The break highlights a continuation of the downtrend and opens $53.77, a Fibonacci projection. Key S/T resistance is $61.25, the Oct 24 high. First resistance is at $58.56, the 50- day EMA.

- The trend structure in Gold is unchanged, it remains bullish and the sharp sell-off earlier this week appears corrective - for now. The trend is overbought and a deeper retracement would allow this condition to unwind. First support at $4324.8, the 20-day EMA, has been pierced. A clear break of the average would expose the 50-day EMA at $4183.5. For bulls, a resumption of gains would open $4578.3, a Fibonacci projection.

| Date | GMT/Local | Impact | Country | Event |

| 02/01/2026 | 1445/0945 | *** | S&P Global Manufacturing Index (final) | |

| 03/01/2026 | 1930/1430 | Philly Fed's Anna Paulson | ||

| 04/01/2026 | 1730/1230 | Minneapolis Fed's Neel Kashkari |