US TSYS: Ringing in the New Year with Final S&P Global Mfg PMI

Jan-02 11:48

- Treasuries are ringing in the new year mildly weaker - off early London session lows on rather decent volumes: TYH6 currently -1.5 at 112-12.5 vs. 112-05 low on just over 280,000 contracts; 10Y yield retreating from 4.1907% overnight high to 4.1573% (-.0097).

- Technical trend theme remains bearish and a break of 111-29 would confirm a resumption of the bear cycle. This would open 111-19, a Fibonacci projection.

- Limited data today: final S&P Global US Manufacturing PMI at 0945ET. No scheduled Fed speakers today - while Philadelphia Fed President Anna Paulson answers questions at a AEA conference tomorrow at 1015ET.

- Looking ahead: the first two full weeks of the year see nonfarm payrolls (next Friday) and CPI reports (Jan 13) for December with those two key reports back on their original schedules having been prioritized by the BLS.

- Private sector reports meanwhile are highlighted by ISM manufacturing and services reports Jan 5 and 7.

- PPI and retail sales are also released (Jan 14) but they’re still lagging and will only be for November (along with a full set of October details in the case for PPI). Note that PPI for December will then follow at the end of the month as the BLS continues to work on returning that report to its original schedule.

- These all build up to the FOMC meeting on Jan 27-28, which is currently seen with low odds of a fourth consecutive 25bp cut with just 3bp of cuts priced. The next cut is fully priced for the June meeting under a new Fed chair.

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

OUTLOOK: Price Signal Summary - Resistance In WTI Remains Intact

Dec-03 11:36

- On the commodity front, the trend condition in Gold is unchanged and remains bullish. The bear phase between Oct 20 and 28 appears to have been a correction and note that the recovery since Oct 28 signals the end of that corrective cycle. Key support to watch lies at the 50-day EMA, at $4009.2. Clearance of this EMA would signal scope for a deeper retracement. Sights are on key resistance and the bull trigger at $4381.5, the Oct 20 high.

- Recent gains in WTI futures are considered corrective. Note that moving average studies are in a bear-mode position, highlighting a dominant downtrend. A resumption of the bear leg would open the key support and the bear trigger at $55.99, the Oct 20 low. Clearance of this level would resume the downtrend. Key short-term resistance to watch is $61.84, the Oct 24 high. A clear break of this hurdle would signal scope for a stronger correction.

LOOK AHEAD: Wednesday Data Calendar: ADP, Import/Exp Prices, IP/Cap-U, ISMs

Dec-03 11:30

- US Data/Speaker Calendar (prior, estimate). All times ET

- 12/03 0700 MBA Mortgage Applications (0.2%, --)

- 12/03 0815 ADP Employment Change (42k, 10k)

- 12/03 0830 Import Price Index MoM (0.3%, 0.1%), YoY (0.0%, 0.4%)

- 12/03 0830 Export Price Index MoM (0.3%, -0.1%), YoY (3.4%, --)

- 12/03 0915 Industrial Production MoM (-0.1% rev, 0.1%), Capacity Utilization (75.8% rev, 77.2%)

- 12/03 0945 S&P Global US Services PMI (55.0, 55.0), Composite PMI (54.8, --)

- 12/03 1000 ISM Services Index (52.4, 52.0), ISM Services Prices Paid (70.0, 68.0}

- 12/03 1000 ISM Services New Orders (56.2, --), Employment (48.2, --)

- 12/03 1130 US Tsy $69B 17W bill auction

- 12/03 1430 US Pres Trump to make an announcement

- Source: Bloomberg Finance L.P. / MNI

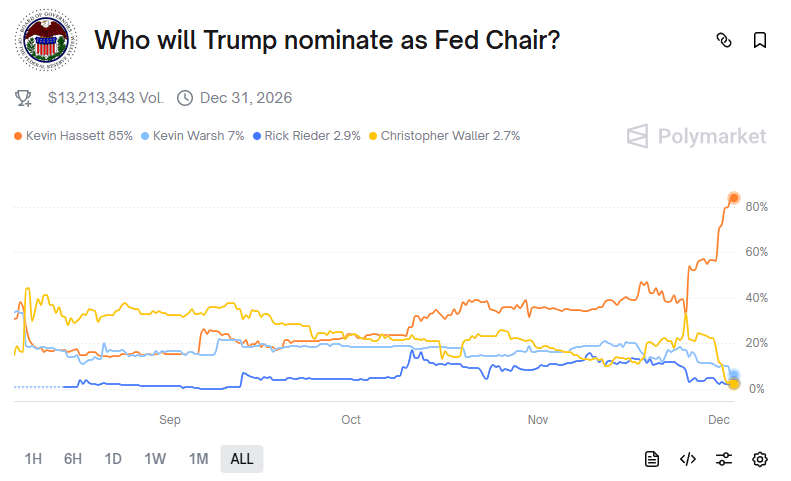

STIR: US Rates Reflect Latest Leg Higher In Hassett Fed Chair Probability

Dec-03 11:25

- Overnight rate moves chime with another tick higher in odds that NEC’s Hassett will be the next Fed chair, even if there was little initial reaction to Trump explicitly referring to him as potential chair yesterday when the likelihood in betting markets increased from 65-70% to 85%.

- WSJ reporting has since helped solidify the modest rally, led by mid-2026/early-2027 contracts, noting that the Trump administration canceled a slate of interviews set to start on Wed with a group of finalists. A person familiar with the matter said the cancellation was because of a scheduling conflict for the vice president.

- Fed Funds implied rates are unchanged through March after which they sit a touch lower on the day.

- Cumulative cuts from 3.89% effective: 23.5bp Dec, 31bp Jan, 38.5bp Mar, 46bp Apr and 60.5bp Jun.

- SOFR futures are up to +0.02 on the day, with the terminal implied yield of 3.035% (H7) extending the week’s decline back towards the 3% seen since NY Fed’s Williams’ dovish guidance on Nov 21.