RATINGS: No Sovereign Reviews Of Note Scheduled After Close, ’26 Calendar Here

No major sovereign credit rating reviews scheduled for after hours on Friday.

- Click here to access the indicative 2026 sovereign rating review schedules across the five most prominent rating agencies (Fitch, Moody's, S&P, Morningstar DBRS & Scope Ratings).

- Note that the schedules are indicative only and ratings can be reviewed on an ad-hoc basis.

- Rating agencies may also adjust their schedules during the year.

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

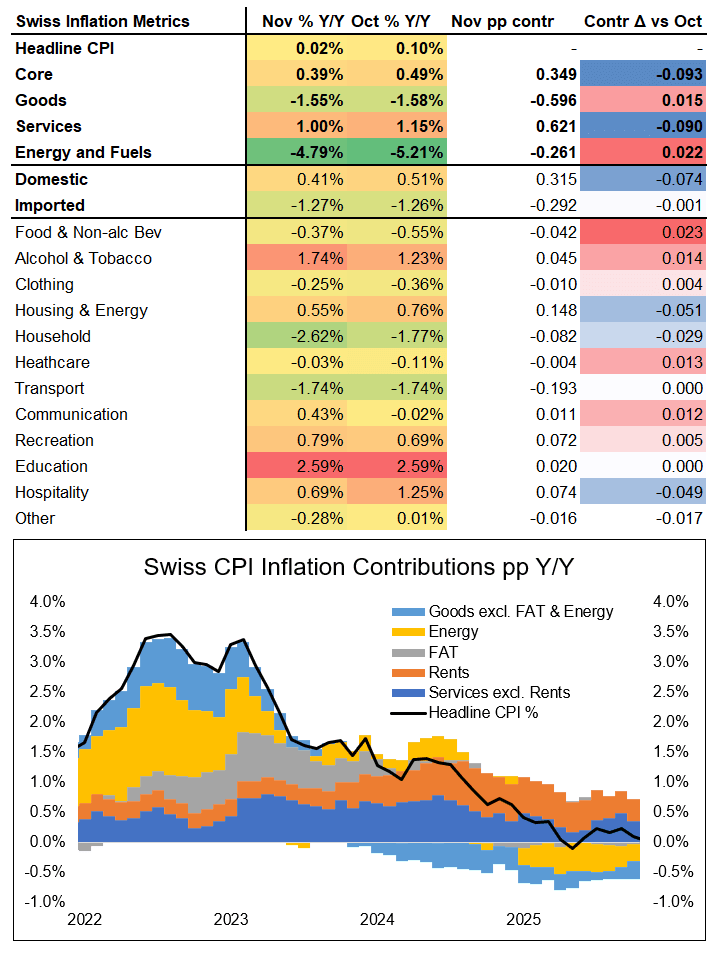

SWITZERLAND DATA: CPI Details Confirms Downside Centred Around Housing / Hotels

Looking at the details of the Swiss CPI print shows the following:

- Unrounded headline CPI was 0.02% (down from 0.10% in October, a 0.08ppt slowdown).

- Housing rentals contributed -0.05pp to the change in headline CPI (this only updates quarterly and is likely to remain persistent)

- Hospitality also contributed -0.05ppt to the change in headline CPI (coming from hotels, volatile package holidays playing only a minor part)

- Food and energy both contributed around +0.02ppt each, to partially offset this.

- These were the major drivers, for detailed calculations, see chart / table below.

What remains on net is a soft print which, while by itself is very unlikely to prompt an SNB cut into negative territory, warrants further monitoring. This applies especially as the downside this time was centred around domestic categories - which the SNB has flagged previously when looking at underlying inflationary pressures. Having said that, what's not quite so clear is their stance on the housing slowdown, with some previous comments suggesting that they merely view it as a lagged function of headline which may imply less feedthrough to policy. Also, we don't know what number they had pencilled in for rentals, either. So it's hard to know if this is the driver of the surprise, or if it is more broad based.

CHF saw a limited reaction to the release.

MNI: SPAIN NOV SERV PMI 55.6 (56.3 FCAST, 56.6 OCT)

- MNI: SPAIN NOV SERV PMI 55.6 (56.3 FCAST, 56.6 OCT)

STIR: Short End Still Shows Outside Odds Of Further ECB Easing

EUR STIRs little changed early today, with the market continuing to price only limited odds of an additional rate cut in the current cycle as the ECB deems policy to be in “a good place”.

- ~7bp of easing is priced through September.

- Still, markets have been hesitant to completely unwind pricing of some easing, as there remains some uncertainty around how tolerant the Governing Council will be of a sub-2% inflation rate - even if this would be in line with ECB projections. Sell-side recommendations and recent Euribor options flow have suggested that dovish positions at the front of the EUR curve offer good risk/reward at current levels.

- The November low in ERZ6 held yesterday, with the contract rallying by 2.5bp since that test.

- Services PMIs (final readings for the Eurozone and larger regional economies) are due this morning.

Elsewhere, we will hear from ECB President Lagarde, chief economist Lane and acting Governing Council member Dolenc will cross through the day.

ECB Meeting | €STR ECB-Dated OIS (%) | Difference Vs. Current Effective €STR (bp) |

Dec-25 | 1.929 | +0.0 |

Feb-26 | 1.925 | -0.4 |

Mar-26 | 1.902 | -2.7 |

Apr-26 | 1.897 | -3.2 |

Jun-26 | 1.865 | -6.4 |

Jul-26 | 1.862 | -6.7 |

Sep-26 | 1.857 | -7.2 |