MNI EUROPEAN OPEN: USD BBDXY Index Supported Sub 1200, Oil Up

EXECUTIVE SUMMARY

- TRUMP SAYS US DOING 'VERY WELL' AS IRAN WAR SHAKES REGION - BBG

- MNI DISCUSSES THE BOJ'S CHALLENGES AS IT NAVIGATES A POTENTIAL OIL PRICE SHOCK - MNI POLICY

- CHINA SETS LOWEST ANNUAL GDP TARGET SINCE 1991 - MNI

- CHINA KEEPS FISCAL EXPANSION SIMILAR TO 2025 - NPC

- FORMER RBA STAFFERS LOOK AT REACTION TO OIL & LIKELY NEXT POLICY MOVES - MNI

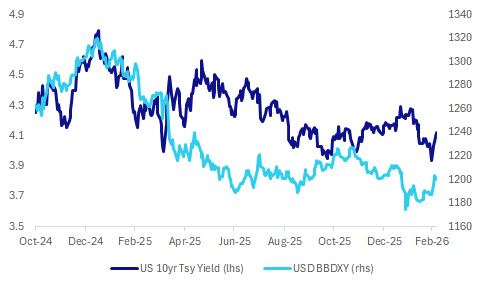

Fig 1: USD BBDXY index & Nominal 10yr UST Yield

Source: Bloomberg Finance L.P./MNI

UK

GOVERNMENT (BBG): "More than 100 Labour Party lawmakers have urged Prime Minister Keir Starmer’s government to rethink changes to the UK’s immigration system, underscoring the scale of opposition confronting him from within his own ranks."

EU

EUR (BBG): “The European Central Bank must prepare for a stronger euro if the continent wants to boost the single currency’s global status, Governing Council member Pierre Wunsch said. “If we want a greater role for the euro, we might have a further appreciation,” the Belgian central-bank chief said in an interview in Brussels.”

SPAIN (BBG): "Banco Santander SA is owed between £200 million ($267 million) and £300 million by a company tied to Market Financial Solutions Ltd., the failed UK lender that has rattled Wall Street, a person familiar with the matter said. "

US

IRAN (BBG): "President Donald Trump expressed confidence in the US military campaign against Iran even as the timeline for operations remained deeply unclear on the fifth day of the Middle East war. "

ECONOMY (MNI BRIEF): U.S. economic activity expanded "a slight to moderate pace" in seven of the Federal Reserve's 12 Districts, while the number of regions reporting flat or declining activity rose to five from four, according to the latest Beige Book published Wednesday.

SERVICES (MNI INTERVIEW): The U.S. service economy picked up steam in the early part of 2026, a jump that will likely be extended as long as the higher energy costs, uncertainty, and geopolitical risk linked to U.S. and Israeli attacks on Iran do not last too long, Institute for Supply Management services chair Steve Miller told MNI.

FED (MNI BRIEF): President Donald Trump on Wednesday officially nominated Kevin Warsh to be the next chairman of the Federal Reserve and to serve a 14-year term as governor.

TARIFFS (BBG): "A US judge has ordered that the Trump administration halt a key step in the tariff payment process in order to make any refunds simpler after the US Supreme Court struck down the president’s global levies."

JAPAN

BOJ (MNI POLICY): MNI discusses the BOJ's challenges ahead as it navigates an impending oil supply shock. On MNI Policy MainWire now, for more details please contact sales@marketnews.com

BOJ (BBG): "Bank of Japan officials are still on track to raise interest rates, with the possibility of April not ruled out, as they continue to monitor the implications of Middle East tensions for Japan’s economy, according to people familiar with the matter."

OTHER

SHIPPING (BBG): "A bulk carrier signaled it was Chinese-owned as it transited the Strait of Hormuz this week, highlighting how vessels are trying to ensure safe passage through the waterway during the war in the Middle East."

AUSTRALIA (MNI): Former RBA staffers look at its reaction to the oil price surge and its likely next moves. On MNI Policy MainWire now, for more details please contact sales@marketnews.com.

FINANCE (MNI BRIEF): Digitalisation means that the financial system is increasingly reliant on a small number of third-party providers, the Bank for International Settlements General Manager will say on Wednesday, which could pose financial stability concerns as disruptions affect multiple institutions simultaneously.

CANADA (MNI BRIEF): Bank of Canada Governor Tiff Macklem said Wednesday his policy interest rate remains appropriate as long as the economic outlook holds up, and financial markets have continued to function since the outbreak of fighting in Iran.

CHINA

GDP TARGET (MNI): China has set its 2026 economic growth target range at 4.5% to 5%, marking the weakest expansion goal since 1991 and aligning with MNI’s earlier report as well as market expectations. The lower target signals policymakers’ greater tolerance for slower growth as they prioritise economic restructuring over short-term stimulus.

POLICY (MNI BRIEF): China will maintain a moderately accommodative monetary stance, take measures to stabilise inflation, and implement structural innovations in key sectors, according to the Government Work Report delivered by Premier Li Qiang during the opening session of the National People's Congress in Beijing on Thursday.

FISCAL (MNI BRIEF): China will continue to implement a more proactive fiscal policy in 2026, keeping fiscal expansion roughly in line with last year though falling short of market expectations.

HOUSING (MNI BRIEF): China will focus on stabilising the real-estate market with city-specific policies, highlighting housing support to encourage marriage and childbirth, according to the Government Work Report delivered by Premier Li Qiang during the opening session of the National People's Congress in Beijing on Thursday.

ENERGY (YICAI): “China’s energy development still faces several major challenges, including structural shortcomings in energy supply that require further optimisation, said Yang Changli, a member of the CPPCC National Committee and chairman of China General Nuclear Power Group (CGN).”

ENERGY (BBG): "China’s government has told the country’s largest oil refiners to suspend exports of diesel and gasoline as an escalating conflict in the Persian Gulf disrupts the arrival of crude from one of the world’s largest producing regions."

CHEMICALS (MNI INTERVIEW): A China chemicals expert discusses potential impacts due to the Iran conflict. On MNI Policy MainWire now, for more details please contact sales@marketnews.com

MNI: PBOC Net Drains CNY297.5 Bln via OMO Thursday

MNI (BEIJING) - The People's Bank of China (PBOC) conducted CNY23 billion via 7-day reverse repos, with the rate unchanged at 1.40%. The operation led to a net drain of CNY297.5 billion after offsetting the maturity of CNY320.5 today, according to Wind Information.

- The seven-day weighted average interbank repo rate for depository institutions (DR007) fell to 1.4008% at 09:31 am local time from the close of 1.4189% on Wednesday.

- The CFETS-NEX money-market sentiment index, measuring interbank money-market liquidity, closed at 49 on Wednesday, compared with the close of 48 on Tuesday. A higher reading points to tighter liquidity condition, with 50 representing an equilibrium.

MNI: PBOC Sets Yuan Parity Lower At 6.9007 Thurs; +5.51% Y/Y

MNI (BEIJING) - The People's Bank of China (PBOC) set the dollar-yuan central parity rate lower at 6.9007 on Thursday, compared with 6.9124 set on Wednesday. The fixing was estimated at 6.9027 by Bloomberg survey today.

MARKET DATA

NEW ZEALAND Q4 VOLUME OF ALL BUILDINGS Q/Q -3.1%; MEDIAN 1.9%; PRIOR 0.2%

AUSTRALIA JAN HOUSEHOLD SPENDING M/M 0.3%; MEDIAN 0.4%; PRIOR -0.5%

AUSTRALIA JAN HOUSEHOLD SPENDING Y/Y 4.6%; MEDIAN 5.1%; PRIOR 5.0%

AUSTRALIA JAN TRADE BALANCE A$2631MN; MEDIAN A$3800MN; PRIOR A$3373MN

AUSTRALIA JAN EXPORTS M/M -0.9%; PRIOR 0.9%

AUSTRALIA JAN IMPORTS M/M 0.8%; PRIOR -1.8%

SOUTH KOREA FEB FOREIGN RESERVES $427.62BN; PRIOR $425.91BN

MARKETS

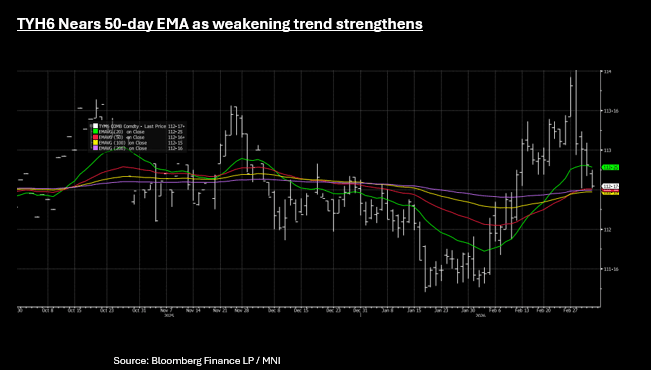

US TSYS: 10-Yr Through 4.10%, Upper Momentum in Yields Strengthens

The weakness continued for US bonds in Asia Thursday with yields higher again as the long end stumbled. US bond futures were all lower with the 10-Yr down -08+ to 112-17+, nearing the downside resistance from the 50-day EMA of 112-16+. The dramatic convergence of the 50,100 and 200-day EMA suggest a potential major trend reversal or a significant, high-volume breakout in the short term given no longer term trend to anchor price action.

Yields were higher across the curve by +0.8bp to 3.0bps in Asia Thursday, ignoring regional equity strength .

- The 2-Yr was up +0.6bps at 3.56%

- The 5-Yr was up +1.7bps at 3.701%

- The 10-Yr was up +2.3bps at 4.123%

- The 30-Yr was up +2.7bps at 4.764%

MNI UST Issuance Deep Dive: March 2026: We've just published our latest US Treasury Issuance Deep Dive - Download Full Report Here:

https://media.marketnews.com/MNI_US_Deep_Dive_Issuance_2026_02_c9b4586b77.pdf

US Data/Speaker Calendar (prior, estimate).

- Challenger Job Cuts

- Initial Jobless Claims (212k, 215k), Continuing Claims (1.833M, 1.848M)

- Import Price Index MoM (0.1%, 0.3%), YoY (0.0%, 0.2%)

- Export Price Index MoM (0.3%, 0.2%), YoY (3.1%, --)

- Nonfarm Productivity (4.9%, 1.8%)

- Unit Labor Costs (-1.9%, 2.0%)

- US TSY US$105B 4 week & US$95B 8 week bill auctions

- Chicago Fed Goolsbee may address policy related topics at Foreign Policy Association Financial Services Dinner (no text)

Source: Bloomberg Finance L.P. / MNI

JGBS: Cheaper Despite Solid Demand At Today's 30Y Auction

At the Tokyo lunch break, JGB futures are weaker, -26 compared to settlement levels.

- Today’s weekly international investment flow data again through support the idea that offshore investors continue to shift funds into Japanese bonds. Year to date net inflows into Japan bonds are now over 7.6trln.

- Cash US tsys are flat to 2bps cheaper in today's Asia-Pac session.

- Cash JGBs are 1-5bps cheaper across benchmarks, with a steepening bias after today's 30-year supply.

- The benchmark 30-year yield is 3.5bps higher at 3.405% versus the cycle high of 3.876%.

- Swap rates are 1-4bps higher.

- Currently, BOJ-dated OIS is slightly 1-4bps softer than pre-January MPM levels. This is a marked turnaround from mid-February, when the market was 1-5bps firmer than pre-January MPM levels.

- Notably, this move seems at odds with the current inflationary threat from the price of oil. BOJ Governor Ueda on Wednesday warned that a sustained rise in crude oil prices could push up underlying inflation, which the Bank monitors closely as a key factor in guiding monetary policy. The governor reiterated the bank's stance of gradually raising the policy rate if economic and price conditions evolve as expected.

- Tomorrow, the local calendar will see

Source: Bloomberg Finance LP / MNI

AUSSIE BONDS: Cheaper After Subdued Session Despite HH Spend Undershoot

ACGBs (YM -5.0 & XM -5.0) are weaker after trading in relatively narrow ranges in today’s session.

- This came despite Australia household spend for Jan printing a little weaker than forecast. The m/m print rose 0.3%m/m versus 0.4% forecast. This saw the y/y outcome print at 4.6%, versus 5.1% forecast and 5.0% prior. Yesterday's national accounts also showed some slowing in household consumption growth.

- Cash US tsys are flat to 2bps cheaper in today's Asia-Pac session.

- Cash ACGBs are 5bps cheaper with the AU-US 10-year yield differential at +68bps.

- (MT Newswires) "Commonwealth Bank of Australia (ASX:CBA) said that it still expects the Reserve Bank of Australia (RBA) to hold rates in March and raise in May as the latest household spending data completed the major data set ahead of a rate decision, according to a Thursday report by the bank." - via BBG

- The bills strip has bear-steepened, with pricing -1 to -6.

- RBA-dated OIS pricing shows tightening across all meetings, with the probability of a 25bp hike rising from 26% for March to 121% by June and 198% by December 2026.

- Tomorrow, the local calendar will see Foreign Reserves.

- The AOFM also plans to sell A$800mn of the 1.50% 21 June 2031 bond on Friday.

Bloomberg Finance LP

BONDS: NZGBS: Solidly Cheaper Despite Solid Demand At Weekly Supply Auctions

NZGBs closed 4-5bps cheaper, tracking global bonds. The NZ-US 10-year yield differential was unchanged on the day. Cash US tsys are flat to 2bps cheaper in today’s Asia-Pac session.

- Today’s weekly supply auctions drew strong demand, with cover ratios ranging from 3.58x (May-35) to 4.98x (may-31).

- (Bloomberg) “The number of New Zealanders moving to Australia is at its highest level in 12 years, with about 41,000 people making the move last year. Australia is the top destination for New Zealand migrants, with higher pay and stronger career prospects being a major draw, and the wage gap between the two countries is significant. The exodus of New Zealanders to Australia has become a major political issue ahead of New Zealand's general election, with opposition leader Chris Hipkins tying the departures to high living costs and limited opportunity at home."

- Swap rates closed 4-5bps higher.

- RBNZ-dated OIS pricing closed firmer across meetings. No tightening is priced for April, while December 2026 assigns 38bps.

- Tomorrow, the local calendar will be empty and will remain so until next Thursday release of Q4 Mfg Activity data.

Bloomberg Finance LP

FOREX: USD - BBDXY Finds Bids Below 1200 On First Attempt

The BBDXY has had a range today of 1198.47 - 1202.28 in the Asia-Pac session; it is currently trading around 1202, +0.20%. The BBDXY has seen quite a reversal from above 1210 and presents as an ugly bearish shadow on the daily chart. The market is looking at everything through rose tinted glasses and the way risk trades expects the conflict to be short and the Straits back open similarly and up and running. I am not so optimistic and feel the USD is central to how risk unfolds from here. On the day, I suspect dips could now be supported with the first buy-zone back toward 1197-1198 and then 1191-1194. Bulls will be looking for demand to return down here to form a base of sorts from which to retest the 1210-1215 area.

- EUR/USD - Asian range 1.1609-1.1647, Asia is currently trading 1.1610. The pair drifted higher after finding some demand below 1.1600 but its bounce has been pretty underwhelming considering the moves seen elsewhere. The price action does not look great for the bulls and I suspect rallies will now be faded as the market eyes a move back toward the 1.1400-1.1500 area. On the day, the first sell-zone is back toward 1.1650-1.1680 and then the 1.1750 area, looking for the move lower to now build for a potential test of the pivotal 1.1400-1.1500 support. CFTC Data shows asset managers are very long the EUR and this move could potentially get them to start paring back some of that exposure.

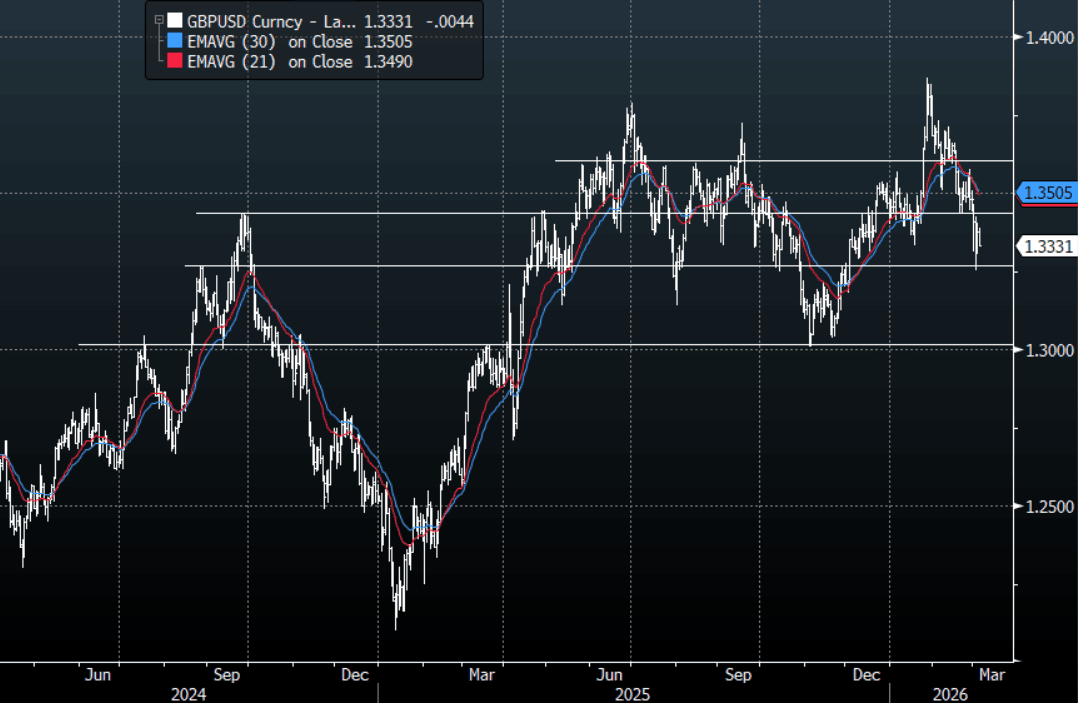

- GBP/USD - Asian range 1.3330-1.3387, Asia is currently dealing around 1.3335. GBP looks like it is now trying to put a top in place. It really needs to close below the pivotal 1.3300 area to confirm but I suspect rallies could now be faded. On the day, I suspect rallies toward 1.3400-1.3450 will continue to be faded as the USD looks to build on its gains. Sellers will be looking for the 1.3300 area to give way, signaling a potential move back to 1.3000.

- Cross asset : SPX -0.20%, Gold $5180, US 10-Year 4.11%, BBDXY 1202, Crude Oil $77.40

- Data/Events : France Jan. Industrial Production, Germany Feb. Construction PMI, ECB’s Guindos speaks, Italy Jan. Retail Sales, ECB’s Rehn speaks, Bundesbank’s Nagel presents 2025 annual report, US Feb. Challenger Job Cuts, US Weekly Initial Jobless Claims, ECB’s Lagarde speaks, The ECB publishes accounts of its last meeting.

Fig 1: GBP/USD Spot Daily Chart

Source: MNI - Market News/Bloomberg Finance L.P

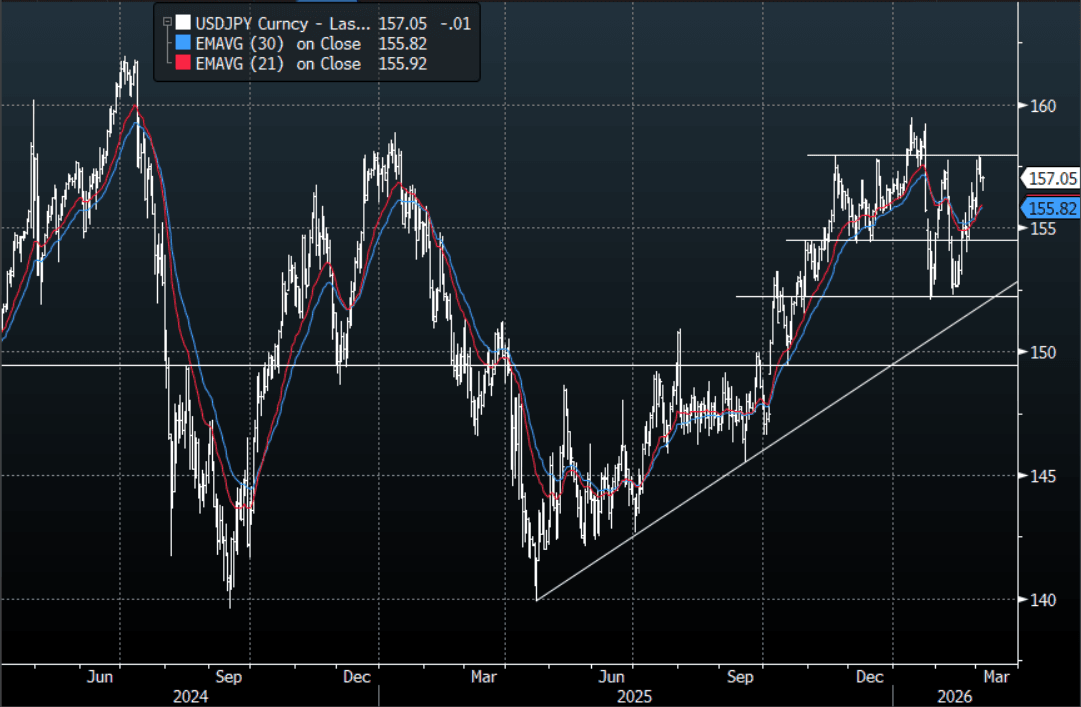

JPY: USD/JPY - Finds Demand Around 156.50 And Reverses Early Losses

The USD/JPY range today has been 156.46-157.12 in the Asia-Pac session, it is currently trading around 157.05 back where it opened. The pair found solid demand in the 156.50 area and has reversed all its early Asian losses. The pair is still looking to re-challenge the 158.00 area. A break above 158.00 and the market will again be looking toward the 160.00 area and then beyond, the jaw-boning by officials has started to increase and for the moment the market is wary but you can only cry wolf so many times and eventually they will need to act for the market to stop doubting them. Personally I don’t see them coming in when the USD has been so bid and I suspect it would need levels above 160-162 to force them to come in. On the day, the first support is back toward 156.50 and then the 155.00-155.50 area.

- MNI AU - Japan Offshore Inflows Continue Into Local Bonds & Stocks: Offshore investors continue to shift funds into both Japan bonds and equities, continuing recent trends.

- “China set its annual economic growth goal at a range of 4.5% to 5%, the least ambitious expansion target since 1991. Separately, Beijing told the country’s largest oil refiners to suspend exports of diesel and gasoline.” - BBG

- Options : Close significant option expiries for NY cut, based on DTCC data: 157.00($1.04b). Upcoming Close Strikes : 153.25($1.27b March 6), 155.00($1.49b March 9), 156.40($869m March 6) - BBG.

- The USD/JPY Average True Range(ATR) for the last 10 Trading days: 116 Points

Fig 1 : USD/JPY Spot Daily Chart

Source: MNI - Market News/Bloomberg Finance L.P

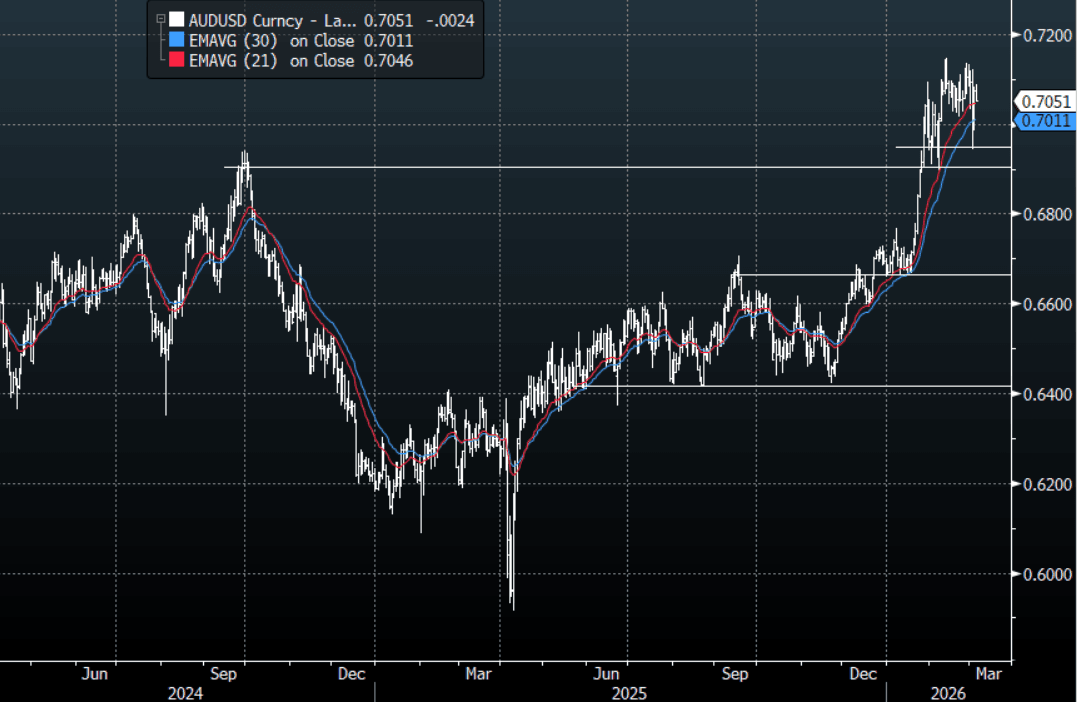

AUD/USD - Stalls Toward 0.7100 & Drifts Lower As Oil Moves Higher

The AUD/USD has had a range today of 0.7049-0.7089 in the Asia- Pac session, it is currently trading around 0.7050,-0.35%. The AUD has stalled toward 0.7100 and drifted lower as Oil moved up on reports of a tanker being hit off Kuwait and risk topping out. Still an Amazing comeback by risk in the current environment, I still remain wary though and would probably be skewed to fading rallies until we see an end to the conflict or the Strait of Hormuz being fully opened. On the day, I would be looking for sellers to return in the 0.7100-0.7120 area looking for risk to come back under pressure at some point. A sustained close back above 0.7120-0.7140 would see the downward pressure negated and the upward trend would likely be resumed.

- MNI AU - AU Jan Household Spending Lower Forecast, Y/Y Back Under 5%: Australia household spend for Jan was a little weaker than forecast. Spending appears to be moderating but from reasonable levels. The RBA is unlikely to be concerned and it may not prevent another rate hike, given still elevated inflation pressures and a tight labour market.

- MNI: Behind-Curve RBA To Wait Till May Before Hike-Ex Staffers. The Reserve Bank of Australia is likely to wait until May before lifting its cash rate from 3.85%, but could consider a larger 50-basis-point increase if the Iran conflict pushes oil prices higher and feeds into first-quarter CPI, especially with inflation already above the target band, former officials told MNI, warning that repeated forecast misses combined with an energy shock risk de-anchoring inflation expectations.

- Options : Closest significant option expiries for NY cut, based on DTCC data: 0.6950(AUD943m), 0.7000(AUD1.5b), 0.7150(AUD1.38b). Upcoming Close Strikes : 0.7000(AUD957m Mar 9), 0.7050(AUD687m Mar 6) - BBG

- The AUD/USD Average True Range for the last 10 Trading days: 88 Points

Fig 1: AUD/USD spot Daily Chart

Source: MNI - Market News/Bloomberg Finance L.P

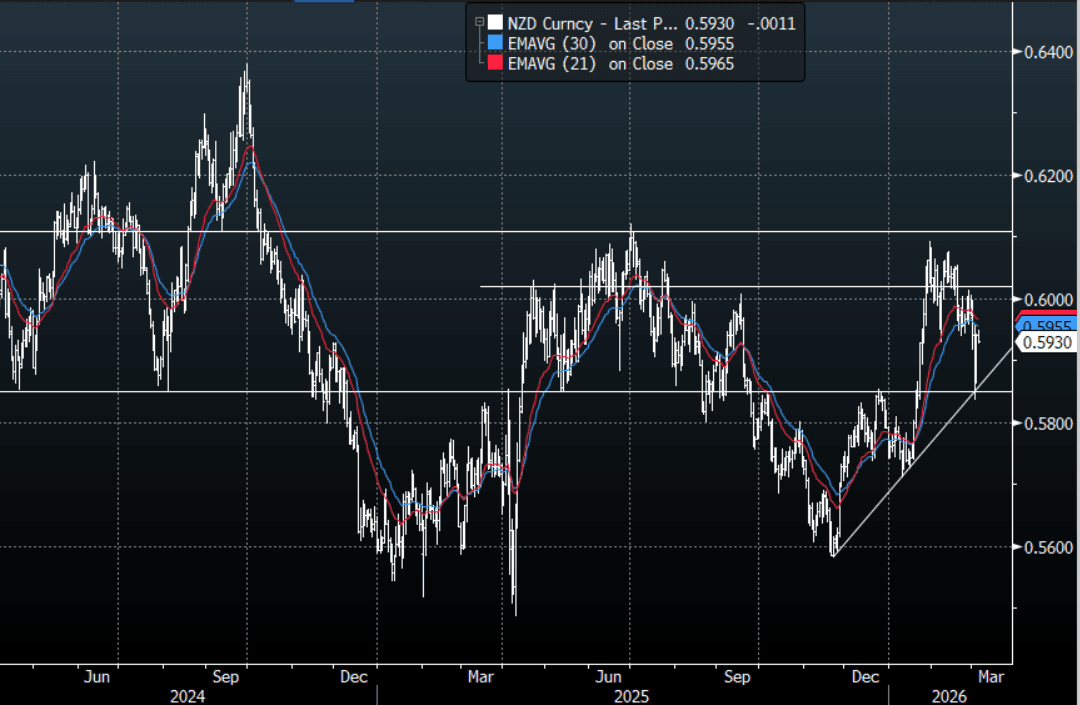

NZD/USD - Drifts Lower From 0.5950, Albeit Back Within Its Range

The NZD/USD had a range today of 0.5926-0.5940 in the Asia-Pac session, it is currently trading around 0.5930, -0.17%. The NZD has drifted lower in Asia as the USD finds a bid on the bump up in oil. The NZD is again back into its 0.5885-0.6015 range after a false break lower, I would still be skewed to fading rallies while below 0.6005-0.6025. On the day, I suspect sellers could return back toward the 0.5965-0.5995 area, looking for the pair to move lower at some point. As mentioned though a break back above 0.6025 would be problematic for the bears.

- MNI AU - NZ Q4 Building Volume Work Falls, Below Forecasts, Q3 Rise Revised: At the margin, lack of upside momentum in the construction side of the economy should give the RBNZ confidence around core inflation pressures remaining contained. We will get more partials for NZ Q4 GDP next Thursday, when manufacturing activity is due. Note that Q4 GDP prints on March 19.

- MNI AU - NZ House Prices Edge Up In Feb But Still Negative Y/Y: The RBNZ noted at its last policy meeting the lack of house price recovery in this cycle, and that the consumption recovery would have to be aided more so by labour income (as opposed to improving housing wealth, like we have seen in previous cycles).

- Options : Closest significant option expiries for NY cut, based on DTCC data: 0.5950(NZD924m). Upcoming Close Strikes : 0.6000(NZD322m March 6) - BBG

- The NZD/USD Average True Range for the last 10 Trading days: 68 Points

Fig 1: NZD/USD Spot Daily Chart

Source: MNI - Market News/Bloomberg Finance L.P

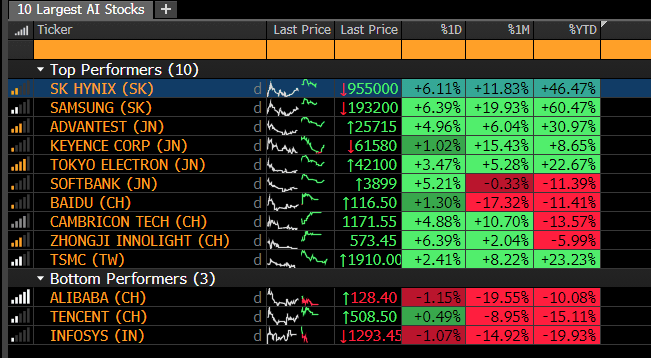

ASIA STOCKS: Wall Steet Lead and AI Bounce Boosts Stocks

Asian equity markets staged a broad-based recovery, rebounding from a multi-day sell-off triggered by Middle East hostilities. Sentiment was bolstered by overnight gains on Wall Street and a temporary stabilization in oil prices following U.S. efforts to secure Persian Gulf flows. Comments from regulators/central banks and key ministers helped to bolster risk appetite, supporting gains.

AI stocks bounced back heavily towo with the 9 out the 10 largest AI stocks in Asia posting gains - supporting their domestic returns.

The KOSPI led the region with a massive 12% surge in the morning, largely recouping a record loss from the previous session before profit takers emerged. Program trading was briefly suspended due to high volatility with the index looking to finish over 10% higher. Key AI stocks SK Hynix and Samsung delivered strong gains but remain down following falls earlier.

The NIKKEI is up +2.5% Thursday in a broad-based day of gains, thanks to the lead in from Wall Street overnight. Banks led the way on better US sentiment following stronger than expected economic data.

In mainland China, technology and power companies led gains (e.g., Biwin Storage +12%; ZhongJI Innolight +6.3%) following government pledges in the 15th Five-Year Plan to boost local innovation and high-tech sectors. Headlines from the NPC see a modest revision downward in GDP forecast to 4.5 - 5.0% as expected, whilst bond issuance targets were confirmed. Local press reports suggest a RRR cut is the most likely policy change in the short term.

Oil Supply Lines Severly Tested, Brent Eyes $85 bbl

- After a slow start to the trading day, oil prices rallied significantly; leaving investors scratching their heads as to the latest catalyst.

- With constant news flow from the ongoing conflict hitting screens pointing to one particular news item is difficult. The reality is at present almost all news items are pointing to supply challenges, or the re-shaping of global supply chains.

- China’s government has told the country’s largest oil refiners to suspend exports of diesel and gasoline as an escalating conflict in the Persian Gulf disrupts the arrival of crude from one of the world’s largest producing regions.

- UK Maritime Operations reports an oil tanker near Kuwait reported a large port side explosion, with a small craft leaving shortly after.

- Hostilities have widened beyond the Persian Gulf after a U.S. submarine reportedly sank an Iranian warship near Sri Lanka, an event described by U.S. officials as the first such attack on an enemy since World War II.

- A bulk carrier signaled it was Chinese-owned as it transited the Strait of Hormuz this week, highlighting how vessels are trying to ensure safe passage through the waterway during the war in the Middle East.

- Iraq has begun shutting down production at giant southern oil fields like Rumaila (approx. 460,000 bpd) due to overflowing storage, while QatarEnergy declared force majeure on LNG exports after suspending production at key facilities.

- WTI is nearing intra-day highs at US$77.29 bbl for gains of +3.5%

- Brent has gained +2.9% today to reach US$83.82 bbl

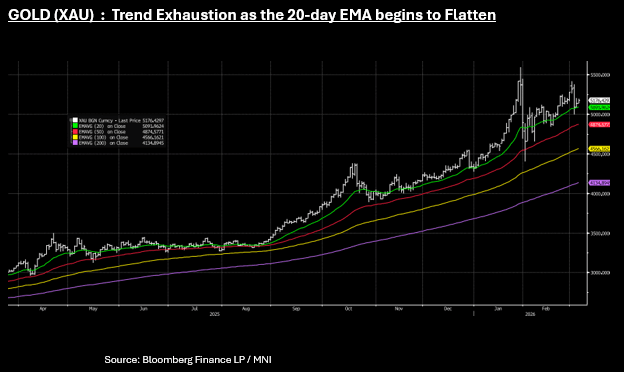

Gold Up; Though Momentum Weak as $5,200 Test Holds

- Gold prices regained upward momentum in Asia today, rising 0.75% to trade near US$5,178.

- Spot was higher from the open reaching US$5,194 per ounce but gave back some of those gains in the afternoon session as it failed its latest attempt at $5,200.

- $5,200 remains a key technical resistance in the short term for gold, having broken above it briefly at the beginning of the month, but ultimately couldn't sustain above.

- Prices continue to trend near to the 20-day EMA - which whilst upward sloping still, shows signs of trend exhaustion. When a 20-day EMA flattens, price tends to "yo-yo" or whip back and forth across the line, making it less reliable indicator and risks a volatility squeeze.

- Intensifying geopolitical conflict between the United States and Iran drove a flight to safety, marking gold's further gains though the technical backdrop makes the outlook less certain with pull backs more prevalent than for most of 2025.

UP TODAY (TIMES GMT/LOCAL)

| Date | GMT/Local | Impact | Country | Event |

| 05/03/2026 | 0700/0800 | *** | Flash Inflation Report | |

| 05/03/2026 | 0700/0800 | *** | Flash Inflation Report | |

| 05/03/2026 | 0745/0845 | * | Industrial Production | |

| 05/03/2026 | 0800/0900 | ** | Industrial Production | |

| 05/03/2026 | 0800/0900 | ** | Unemployment | |

| 05/03/2026 | 0830/0930 | ** | S&P Global Final Italy Construction PMI | |

| 05/03/2026 | 0830/0930 | ** | S&P Global Final Germany Construction PMI | |

| 05/03/2026 | 0830/0930 | ** | S&P Global Final Eurozone Construction PMI | |

| 05/03/2026 | 0850/0950 | ECB de Guindos in Conversation at IIF European Investment Summit | ||

| 05/03/2026 | 0900/1000 | * | Retail Sales | |

| 05/03/2026 | 0930/0930 | ** | S&P Global/CIPS Construction PMI | |

| 05/03/2026 | 0930/0930 | *** | BOE Decision Making Panel | |

| 05/03/2026 | 1000/1100 | ** | EZ Retail Sales | |

| 05/03/2026 | 1000/1000 | ** | Gilt Outright Auction Result | |

| 05/03/2026 | - | National People's Congress | ||

| 05/03/2026 | 1330/0830 | ** | WASDE Weekly Import/Export | |

| 05/03/2026 | 1330/0830 | *** | Jobless Claims | |

| 05/03/2026 | 1330/0830 | ** | Import/Export Price Index | |

| 05/03/2026 | 1330/0830 | ** | Preliminary Non-Farm Productivity | |

| 05/03/2026 | 1530/1030 | ** | Natural Gas Stocks | |

| 05/03/2026 | 1630/1130 | * | US Bill 08 Week Treasury Auction Result | |

| 05/03/2026 | 1630/1130 | ** | US Bill 04 Week Treasury Auction Result | |

| 05/03/2026 | 1700/1800 | ECB Lagarde Lecture on Global Risk | ||

| 05/03/2026 | 1815/1315 | Fed's Michelle Bowman | ||

| 06/03/2026 | 0700/0800 | ** | Manufacturing Orders | |

| 06/03/2026 | 1000/1100 | *** | EZ GDP 3rd (Regular) | |

| 06/03/2026 | 1000/1100 | ECB Lagarde Lecture at Politecnico di Milano | ||

| 06/03/2026 | 1330/0830 | *** | Employment Report | |

| 06/03/2026 | 1330/0830 | *** | Employment Report | |

| 06/03/2026 | 1330/0830 | *** | Employment Report | |

| 06/03/2026 | 1330/0830 | *** | Employment Report | |

| 06/03/2026 | 1330/0830 | *** | Employment Report | |

| 06/03/2026 | 1330/0830 | *** | Employment Report | |

| 06/03/2026 | 1330/0830 | *** | Employment Report | |

| 06/03/2026 | 1330/0830 | *** | Employment Report | |

| 06/03/2026 | 1330/1430 | ECB Cipollone Presentation at European Banking Federation Meeting | ||

| 06/03/2026 | 1330/0830 | *** | Retail Sales | |

| 06/03/2026 | 1330/0830 | *** | Retail Sales |