OIL: Oil Supply Lines Severly Tested, Brent Eyes $85 bbl

- After a slow start to the trading day, oil prices rallied significantly; leaving investors scratching their heads as to the latest catalyst.

- With constant news flow from the ongoing conflict hitting screens pointing to one particular news item is difficult. The reality is at present almost all news items are pointing to supply challenges, or the re-shaping of global supply chains.

- China’s government has told the country’s largest oil refiners to suspend exports of diesel and gasoline as an escalating conflict in the Persian Gulf disrupts the arrival of crude from one of the world’s largest producing regions.

- UK Maritime Operations reports an oil tanker near Kuwait reported a large port side explosion, with a small craft leaving shortly after.

- Hostilities have widened beyond the Persian Gulf after a U.S. submarine reportedly sank an Iranian warship near Sri Lanka, an event described by U.S. officials as the first such attack on an enemy since World War II.

- A bulk carrier signaled it was Chinese-owned as it transited the Strait of Hormuz this week, highlighting how vessels are trying to ensure safe passage through the waterway during the war in the Middle East.

- Iraq has begun shutting down production at giant southern oil fields like Rumaila (approx. 460,000 bpd) due to overflowing storage, while QatarEnergy declared force majeure on LNG exports after suspending production at key facilities.

- WTI is nearing intra-day highs at US$77.29 bbl for gains of +3.5%

- Brent has gained +2.9% today to reach US$83.82 bbl

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

JGBS: Cheaper But Holding Above Worst Levels Despite Poor 10Y Auction

JGB futures are weaker, -27 compared to settlement levels, but holding above today’s session low despite today’s lacklustre 10-year bond auction.

- The 10-year JGB auction delivered weakish results, with the low price failing to meet expectations at 98.75, according to the Bloomberg dealer poll. Moreover, the cover ratio decreased to 3.0196x from 3.3037x. The tail was unchanged 0.05.

- This performance came despite an outright yield hovering just below the cycle high, around 15bps higher than the level of last month's auction.

- The 2s/10s yield curve was also steeper than last month’s auction, although around 20bps below its a cycle high.

- Cash US tsys are little changed in today's Asia-Pac session after yesterday’s heavy session.

- Cash JGBs are mixed across benchmarks, with yields 3bps higher (5-year) to 2.5bps lower (30-year). The benchmark 10-year yield is 1.4bps higher at 2.258% versus the cycle high of 2.359%.

- Swap rates are also slightly mixed with a flattening bias.

- Tomorrow, the local calendar will see S&P Global PMI (Composite & Services).

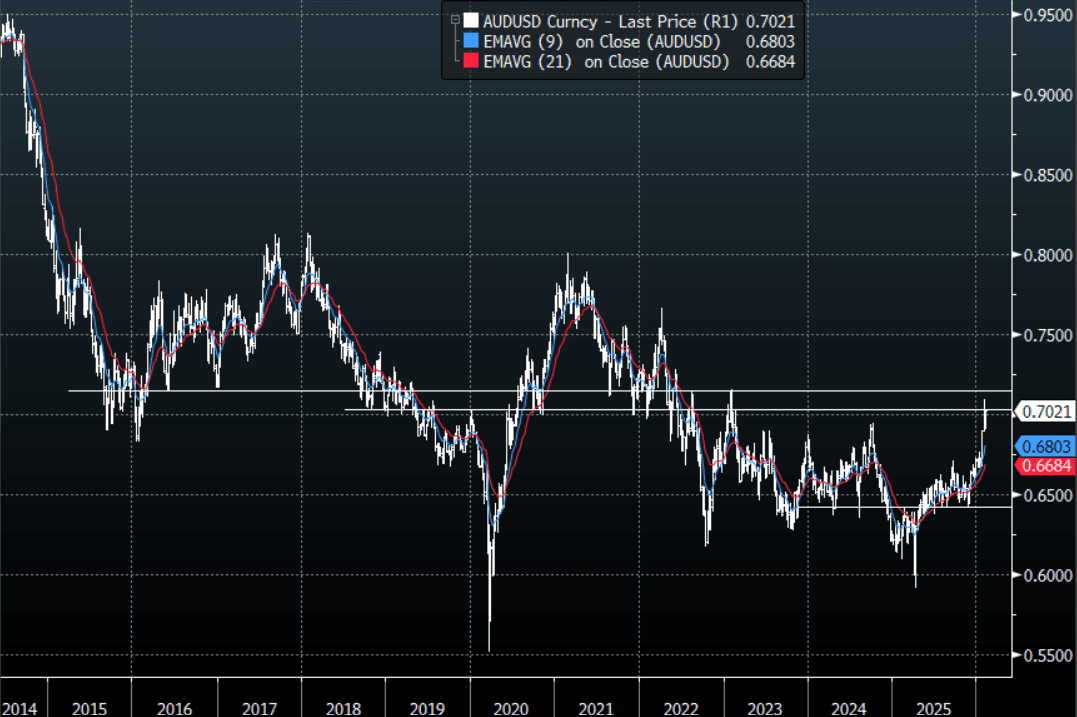

AUD: AUD/USD - Back Above 0.7000 On A Hawkish Hike, Dips To Be Supported

The AUD/USD has had a range today of 0.6945 - 7033 in the Asia- Pac session, it is currently trading around 0.7020, +1.05%. The AUD has exploded higher thanks to a hawkish hike by the RBA. The AUD has been outperforming across the board as leveraged funds increase their longs anticipating today's hike and I suspect these trades will now begin to be added to. The AUD has moved quickly back to 0.7030 where I suspect we find some initial resistance, but this should now see the AUD supported on dips. On the day, the first buy-zone is back toward the 0.6965-0.6985 area, looking for a break above 0.7030 which could give it the momentum to retest the pivotal 0.7100-0.7200 area.

- MNI BRIEF: RBA Lifts Cash Rate To 3.85% On Higher Demand. The Reserve Bank of Australia Board unanimously decided to raise the cash rate by 25 basis points to 3.85% on Tuesday, citing stronger-than-expected private demand, greater capacity pressures than previously assessed, and a still tight labour market.

- The Bank’s updated forecasts showed headline inflation rising to 4.2% by June, up from November’s 3.7%, before returning below 3% by June 2027 at 2.9%, 20 basis points higher than previous estimates. The projections assume a higher cash rate, peaking at 4.3% by December 2027.

- MNI AU - RBA-dated OIS pricing is 3-7bps firmer across all meetings, with another 25bp hike more than fully priced by August (+30bps).

- "RBA GOV BULLOCK: CANNOT ALLOW INFLATION TO GET AWAY FROM US, PULSE OF INFLATION IS TOO STRONG" - [RTRS]

- "RBA GOV BULLOCK: WILL NOT GIVE FORWARD GUIDANCE, BOARD WILL REMAIN FOCUSED ON DATA " - [RTRS]

- Options : Closest significant option expiries for NY cut, based on DTCC data: 0.6830(AUD315m), 0.6900(AUD338mm). Upcoming Close Strikes : 0.6875(AUD913m Feb 6), 0.6950(AUD1.96b Feb 4) - BBG

- The AUD/USD Average True Range for the last 10 Trading days: 81 Points

Fig 1: AUD/USD spot Weekly Chart

Source: MNI - Market News/Bloomberg Finance L.P

MNI EXCLUSIVE: Advisors Want Beijing To Transfer SOE Shares Into Pension Funds