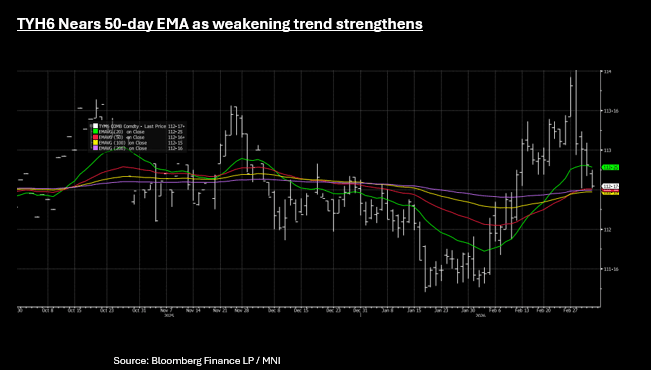

US TSYS: 10-Yr Through 4.10%, Upper Momentum in Yields Strengthens

The weakness continued for US bonds in Asia Thursday with yields higher again as the long end stumbled. US bond futures were all lower with the 10-Yr down -08+ to 112-17+, nearing the downside resistance from the 50-day EMA of 112-16+. The dramatic convergence of the 50,100 and 200-day EMA suggest a potential major trend reversal or a significant, high-volume breakout in the short term given no longer term trend to anchor price action.

Yields were higher across the curve by +0.8bp to 3.0bps in Asia Thursday, ignoring regional equity strength .

- The 2-Yr was up +0.6bps at 3.56%

- The 5-Yr was up +1.7bps at 3.701%

- The 10-Yr was up +2.3bps at 4.123%

- The 30-Yr was up +2.7bps at 4.764%

MNI UST Issuance Deep Dive: March 2026: We've just published our latest US Treasury Issuance Deep Dive - Download Full Report Here:

https://media.marketnews.com/MNI_US_Deep_Dive_Issuance_2026_02_c9b4586b77.pdf

US Data/Speaker Calendar (prior, estimate).

- Challenger Job Cuts

- Initial Jobless Claims (212k, 215k), Continuing Claims (1.833M, 1.848M)

- Import Price Index MoM (0.1%, 0.3%), YoY (0.0%, 0.2%)

- Export Price Index MoM (0.3%, 0.2%), YoY (3.1%, --)

- Nonfarm Productivity (4.9%, 1.8%)

- Unit Labor Costs (-1.9%, 2.0%)

- US TSY US$105B 4 week & US$95B 8 week bill auctions

- Chicago Fed Goolsbee may address policy related topics at Foreign Policy Association Financial Services Dinner (no text)

Source: Bloomberg Finance L.P. / MNI

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

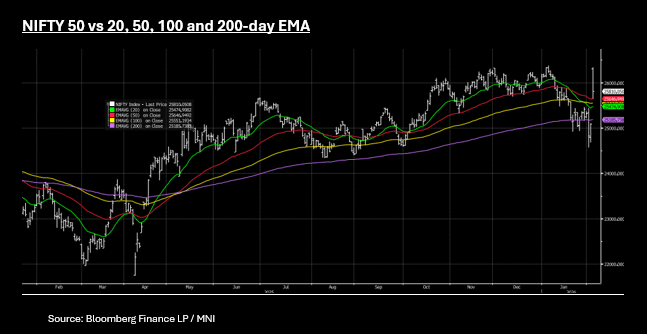

ASIA STOCKS: Dip Buyers Emerge, NIFTY Up on Tariff News

Asian equity markets surged today, rebounding sharply from a sell-off in precious metals and risk assets. The rally saw resurgent optimism in AI stocks and a major US-India trade agreement that reduced tariffs. In the AI sector South Korean chip giants Samsung (+8.7%) and SK Hynix (+7.0%) led the region after heavy selling on Monday. Indian equities are up strongly as President Trump announced a reduction of tariffs to 18%, following an agreement by PM Modi to cease oil purchases from Russia. The bias for higher stocks remains in the region as dip buyers emerge following the falls that began last week and stock futures point to a positive start in the US tonight. The sentiment shift came following better than expected US economic data, brushing off fears of its impact on interest rates.

- Tech heavy markets like Japan and Korea were the leaders today, up +3.9% and +5.4% respectively.

- The NIFTY 50 has had its biggest one day surge since May with gains of +2.8%, rallying back above all major moving averages.

- China's major bourses are all up today though lagging regional trends. The HSI is up just +0.65% whilst the tech heavy Shenzhen Comp faired better with gains of +1.4%

- News of a fiscal stimulus late Tuesday as the government detailed a major social assistance plan, and yesterday saw the release of critical inflation and manufacturing data which saw some modest improvements. After a horror week last week the JCI has bounced today by +1.5%, holding back above 8,000.

AUSSIE BONDS: Cheaper After RBA Decision But Off Worst Levels

ACGBs (YM -9.5 & XM -5.5) are holding weaker but well above session cheaps seen shortly after the RBA policy decision.

- The RBA Board unanimously decided to raise the cash rate by 25bps to 3.85%, citing stronger-than-expected private demand, greater capacity pressures than previously assessed, and a still tight labour market.

- The Bank's updated forecasts showed headline inflation rising to 4.2% by June, up from November's 3.7%, before returning below 3% by June 2027 at 2.9%, 20 basis points higher than previous estimates. The projections assume a higher cash rate, peaking at 4.3% by December 2027.

- "RBA GOV BULLOCK: CANNOT ALLOW INFLATION TO GET AWAY FROM US, PULSE OF INFLATION IS TOO STRONG" - [RTRS]

- "RBA GOV BULLOCK: WILL NOT GIVE FORWARD GUIDANCE, BOARD WILL REMAIN FOCUSED ON DATA " - [RTRS].

- Cash ACGBs are 5-8bps cheaper with the AU-US 10-year yield differential at +57bps and the 3/10 curve flatter.

- RBA-dated OIS pricing is 3-7bps firmer across all meetings, with another 25bp hike more than fully priced by August (+30bps).

- Tomorrow, the local calendar will see S&P Global PMI (Composite & Services).

- The AOFM plans to sell A$1200mn of the 4.25% 21 October 2036 bond on Wednesday and A$800mn of the 1.00% 21 December 2030 bond on Friday.

Bloomberg Finance LP

JGBS: Cheaper But Holding Above Worst Levels Despite Poor 10Y Auction

JGB futures are weaker, -27 compared to settlement levels, but holding above today’s session low despite today’s lacklustre 10-year bond auction.

- The 10-year JGB auction delivered weakish results, with the low price failing to meet expectations at 98.75, according to the Bloomberg dealer poll. Moreover, the cover ratio decreased to 3.0196x from 3.3037x. The tail was unchanged 0.05.

- This performance came despite an outright yield hovering just below the cycle high, around 15bps higher than the level of last month's auction.

- The 2s/10s yield curve was also steeper than last month’s auction, although around 20bps below its a cycle high.

- Cash US tsys are little changed in today's Asia-Pac session after yesterday’s heavy session.

- Cash JGBs are mixed across benchmarks, with yields 3bps higher (5-year) to 2.5bps lower (30-year). The benchmark 10-year yield is 1.4bps higher at 2.258% versus the cycle high of 2.359%.

- Swap rates are also slightly mixed with a flattening bias.

- Tomorrow, the local calendar will see S&P Global PMI (Composite & Services).