MNI EUROPEAN OPEN: NZ GDP Contraction Hits NZD & Local Yields

EXECUTIVE SUMMARY

- FED ON EASING PATH AS JOB MARKET RISKS MOUNT - MNI FED WATCH

- FED’S POWELL, NO WIDESPREAD SUPPORT FOR 50BP CUT - MNI

- AUSSIE EMPLOYMENT LOWER OVER AUGUST - MNI BRIEF

- MNI DISCUSSES THE RBA'S LABOUR MARKET VIEW - MNI POLICY

- NZ Q2 GDP CONTRACTS 0.9% Q/Q - MNI BRIEF

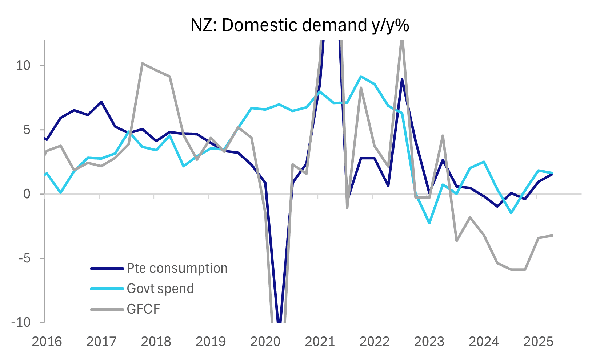

Fig 1: NZ GDP Growth Weighed By Weak Investment

Source: MNI - Market News/Bloomberg/Refinitiv.

UK

UK/US (BBG): “King Charles III urged the defense of Ukraine and the environment as he welcomed US President Donald Trump and top tech and finance executives for a lavish state dinner at Windsor Castle on Wednesday”

US (BBC): “King Charles has commended President Trump's personal commitment to "finding solutions to some of the world's most intractable conflicts", as he called for US support for Ukraine against "tyranny", in a speech at the US state visit banquet. In response, President Trump hailed the special relationship between the US and the UK, saying the word "special does not begin to do it justice".”

ECONOMY (BBC): “A record-breaking £150bn package of US investment into the UK has been announced during US President Donald Trump's state visit. The UK government is calling this the largest commercial deal of its kind and expects it to create more than 7,600 "high-quality jobs" across the country.”

CHINA (POLITICO): “China is sending the Istanbul Bridge container ship on an 18-day trip from Ningbo-Zhoushan port — the world's largest — to Felixstowe in the U.K. on Sept. 20, accompanied by ice breakers. The goal is not a one-off voyage — that's been done before — but to establish a regular service via Russia’s Northern Sea Route linking multiple ports in Asia and Europe.”

EU

FRANCE (MNI BRIEF): France's acting Finance Minister Eric Lombard will attempt to deliver a reassuring message to eurozone finance ministers meeting in Copenhagen on Friday that the country will maintain efforts towards fiscal consolidation, a French government source told MNI.

FRANCE (EURONEWS): “France is gearing up for more nationwide strikes and mass protests this Thursday, expected to be one of the largest in recent years. All of the country's major unions have joined forces.”

ECB (MNI SOURCES): Questions over the future of the European Union’s new carbon-charging scheme, which is set to add significantly to inflation from 2027 onwards, will be a material factor in determining whether the European Central Bank can extend its current easing cycle, Eurosystem sources told MNI.

CHINA/RUSSIA (BBG): “China suspended an unofficial subsidy for copper and nickel imports from countries including Russia, which has become more dependent on purchases by its Asian neighbor since western nations imposed sanctions after the invasion of Ukraine.”

POLAND (POLITICO): “Russia’s military drills may be over, but Poland isn’t relaxing — and has decided to keep its border with Belarus closed indefinitely, severing a €25-billion-a-year trade artery between China and the EU.”

RUSSIA (BBC): “Fifteen people have been charged with terrorism offences in Lithuania over the alleged Russian-backed detonation of parcels in Germany, Poland and the UK, prosecutors say.”

UKRAINE (POLITICO): “Ukraine’s EU accession would serve as a deterrent to future Russian attacks once a peace deal is reached, the president of the European Parliament told Volodymyr Zelenskyy.”

US

FED (MNI FED WATCH): A rising risk of worsening employment conditions prompted the Federal Reserve Wednesday to begin moving toward a more neutral monetary policy even as inflation is expected to remain above target through next year, Fed Chair Jerome Powell said Wednesday after the FOMC resumed rate cuts for the first time since December.

FED (MNI): Federal Reserve Chair Jerome Powell said Wednesday there was not broad support for a larger interest rate cut despite a dissent from newly appointed governor Stephen Miran.

FED (MNI): The Federal Reserve lowered official borrowing costs by a quarter point Wednesday, the first interest rate cut since December, and indicated two more cuts are expected this year, with newly-appointed governor Stephen Miran dissenting in favor of a larger 50 basis point reduction.

TECH (BBG): “Meta Platforms Inc., seeking to turn its smart glasses lineup into a must-have product, on Wednesday unveiled its first version with a built-in screen.”

OTHER

JAPAN (MNI BRIEF): The balance of financial assets held by Japanese households rose 1.0% y/y to a record JPY2,239 trillion at the end of June, marking a 10th straight quarterly gain, preliminary Bank of Japan data showed Thursday.

AUSTRALIA (MNI BRIEF): Australia lost 5,400 jobs in August, well short of the 21,000 expected to be created, while the unemployment rate held steady at 4.2%, Australian Bureau of Statistics data showed Thursday.

AUSTRALIA (MNI POLICY): MNI discusses the RBA's labour market view. On MNI Policy MainWire now, for more details please contact sales@marketnews.com.

AUSTRALIA (BBG): “Shareholders wiped A$3 billion ($2 billion) off the market value of Australian oil and gas group Santos Ltd. after a third attempted sale faltered on Wednesday, raising pressure on management to increase returns.”

NEW ZEALAND (MNI BRIEF): New Zealand’s economy contracted 0.9% q/q in Q2, sharply undershooting the Reserve Bank of New Zealand and market expectations for a 0.3% decline, official data showed Thursday.

NEW ZEALAND (MNI BRIEF): Finance Minister Nicola Willis has appointed Hayley Gourley to the Reserve Bank of New Zealand’s Monetary Policy Committee, replacing longtime member Bob Buckle. Gourley, who has an extensive background in New Zealand’s agribusiness sector, will join the Committee for the October Monetary Policy Review, following the end of Buckle’s term on Sept. 30.

CANADA (MNI BOC WATCH): The Bank of Canada lowered its policy rate a quarter point to 2.5% after three meetings on hold citing weak hiring and less inflation pressure, dropping guidance about potential easing while keeping a phrase about being less forward looking during the trade war.

CANADA (MNI BRIEF): Canada's Finance Minister Francois-Philippe Champagne said the central bank's interest-rate cut on Wednesday helps the economy but more of a push is coming in the federal budget due Nov 4.

BRAZIL (MNI EM BCB WATCH): The Central Bank of Brazil reinforced a higher-for-longer strategy in its statement Wednesday, taking one more step to curb premature expectations for cuts by saying it will keep borrowing costs elevated for a "prolonged period."

CHINA

TAX REVENUE (YICAI): “China’s tax revenue from the securities industry surged by more than 70% in July and August, while the insurance industry growth exceeding 10%, Yicai reported.”

FISCAL (SECURITIES TIMES): “China has issued CNY1.14 trillion in ultra-long-term special government bonds so far this year, completing 88% of the annual plan, according to Securities Times.”

BANKS (BBG): “ Just as China’s long bull run for bonds is fading, the nation’s banks have loaded up on government debt at the fastest pace since 2019.”

MNI: PBOC Net Injects CNY195 Bln via OMO Thursday

MNI (BEIJING) - The People's Bank of China (PBOC) conducted CNY487 billion via 7-day reverse repos, with the rate unchanged at 1.40%. The operation led to a net injection of CNY195 billion after offsetting maturities of CNY292 billion today, according to Wind Information.

- The seven-day weighted average interbank repo rate for depository institutions (DR007) fell to 1.4935% at 09:31 am local time from the close of 1.5404% on Wednesday.

- The CFETS-NEX money-market sentiment index, measuring interbank money-market liquidity, closed at 59 on Wednesday, compared with the close of 51 on Tuesday. A higher reading points to tighter liquidity condition, with 50 representing an equilibrium

MNI: PBOC Sets Yuan Parity Higher At 7.1085 Thurs; -1.20% Y/Y

MNI (BEIJING) - The People's Bank of China (PBOC) set the dollar-yuan central parity rate higher at 7.1085 on Thursday, compared with 7.1013 set on Wednesday. The fixing was estimated at 7.1101 by Bloomberg survey today.

MARKET DATA

NEW ZEALAND Q2 GDP -0.9% Q/Q; EST. -0.3%; Q1 +0.9%

NEW ZEALAND Q2 GDP -0.6% Y/Y; EST. 0%; Q1 -0.6%

AUSTRALIA AUG. EMPLOYMENT -5.4K M/M; EST. +21K; JUL. +26.5K

AUSTRALIA AUG. JOBLESS RATE 4.2%; EST. 4.2%; JUL. 4.2%

AUSTRALIA AUG. PARTICIPATION RATE 66.8%; EST. 67.0%; JUL. 67.0%

AUSTRALIA AUG. FULL-TIME EMPLOYMENT -40.9K M/M; JUL. +63.6K

AUSTRALIA AUG. PART-TIME EMPLOYMENT +35.5K M/M; JUL. -37.1K

JAPAN JULY CORE MACHINE ORDERS -4.6% M/M; EST. -1.5%; JUN. +3.0%

JAPAN JULY CORE MACHINE ORDERS +4.9% Y/Y; EST. +5.2%; JUN. +7.6%

CHINA AUG. GLOBAL SWIFT PAYMENTS +2.93%; JUL. +2.88%

MARKETS

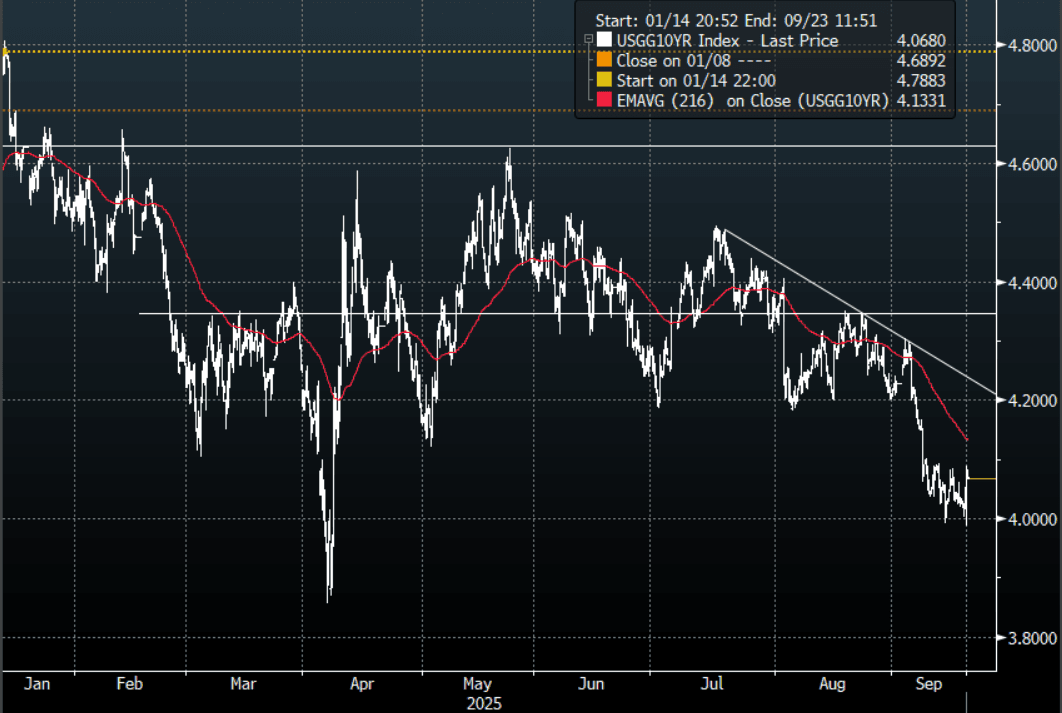

US TSYS: Asia Wrap - Yields Edge Lower

The TYZ5 range has been 113-00 to 113-07 during the Asia-Pacific session. It last changed hands at 113-06+, up 0-02 from the previous close.

- The US 2-year yield has edged lower trading 3.536%, down 0.02 from its close.

- The US 10-year yield has edged lower trading around 4.068%, down 0.02 from its close.

- (Bloomberg) -- The Federal Reserve’s first interest rate cut since December to shield the jobs market collides with a revision higher for its economic growth and inflation forecasts, leaving the central bank ever-more data dependent.

- RenMac on X: “We have two sided risks which means there is no risk free path.” The next two meetings should be priced closer to a coin flip for rate cuts.”

- Jim Bianco on X: “This meeting was a mess. One member of the FOMC thinks the Fed is going to HIKE rates this year. One (Stephen Miran) thinks it is going to cut 1.25% this year (5 cuts over two meetings). Add to this is Powell using the term "Risk Management" to describe this cut. If this is the case now, then the Fed cannot also be data dependent. Both cannot be true at the same time.”

- Data/Events: Initial Jobless Claims, Philadelphia Fed Business Outlook, Leading Index, Net Long-term TIC Flows

Fig 1: 10-Year US Yield 2H Chart

Source: MNI - Market News/Bloomberg Finance L.P

JGBS: Long-End Rallies Ahead Of BoJ Policy Decision, Natl CPI Tomorrow Too

JGB futures are weaker and near session lows, -13 compared to settlement levels.

- Cash US tsys are 2-3bps richer in today's Asia-Pac session after yesterday's post-FOMC sell-off. Focus turns to Thursday's weekly claims.

- Cash JGBs are little changed across benchmarks out to the 10-year but 2-4bps richer beyond. The benchmark 10-year yield is 0.4bp higher at 1.603% versus the cycle high of 1.6490%.

- Swap rates have twist-flattened, with rates 2bps higher to 2bps lower. Swap spreads are mostly wider.

- Tomorrow, the local calendar will see National CPI and Weekly Investment Flow data alongside the BoJ Policy Decision.

- The Bank of Japan is expected to keep policy unchanged in September, with future decisions hinging on October's Tankan survey and branch managers' meeting, which will clarify corporate sentiment and investment trends.

- External risks, particularly the impact of U.S. tariffs and potential weakness in U.S. labour markets, are now the central concern, limiting the urgency for near-term rate hikes despite inflation hovering near 3%.

- Political uncertainty following Prime Minister Ishiba's resignation complicates the outlook, with leading candidates and opposition parties generally favouring fiscal stimulus and accommodative monetary policy. Full MNI BoJ Preview here:

AUSSIE BONDS: Modestly Richer After Employment Data

ACGBs (YM +2.0 & XM +1.5) are slightly richer after the August jobs data missed expectations.

- Australia’s monthly labour market data are volatile and August seemed to unwind July’s moves. Looking through this, annual employment growth was its lowest since the pandemic but the unemployment rate held steady at 4.2% and underemployment continued to trend down to its lowest since 1991. RBA Governor Bullock focused on the Q2 average unemployment rate, given the data’s volatility and that is likely to remain the case. September prints on 16 October.

- Cash US tsys are 2-3bps richer in today's Asia-Pac session after yesterday's post-FOMC sell-off. Focus turns to Thursday's weekly claims.

- Cash ACGBs are 2bps richer on the day, 2-3bps richer after the data. The AU-US 10-year yield differential is at +14bps.

- Swap rates are 3bps lower post-data.

- The bills strip is +2 to +4 across contracts, with a flattening bias.

- RBA-dated OIS pricing is softer across meetings after the data. A 25bp rate cut in September is given a 10% probability, with a cumulative 30bps of easing priced by year-end (based on an effective cash rate of 3.60%).

- Tomorrow, the local calendar will be empty apart from the AOFM’s planned sale of A$1000mn of the 1.00% 21 December 2030 bond.

BONDS: Market Ponders A 50bp Cut After Weak Q2 GDP

NZGBs closed showing a massive bull-steepener, with benchmark yields 4-12bps lower.

- Both the production and expenditure-based GDP measures fell 0.9% q/q in Q2, the weakest since the pandemic. The RBNZ had expected a 0.3% q/q decline. This and the broad-based softness across sectors as well as a sluggish recovery in Q3 to date are likely to drive 25bp rate cuts in October and November in line with the RBNZ’s August OCR path. With two votes for a 50bp cut in August, the risk of a larger move before year-end is material.

- Statistics NZ reported that 10 out of 16 industries contracted in Q2 with manufacturing the largest falling 3.5% q/q. Construction was down 1.8% q/q with the sector continuing to struggle.

- GFCF fell 1.1% q/q, the seventh quarterly decline in the last 2 years, with residential building down 1.9% q/q and other assets -0.9% q/q. GFCF is down 3.2% y/y after -3.4% in Q1.

- Today’s weekly supply saw solid demand, with cover ratios ranging from 3.22x (May-34) to 3.41x (May-30).

- Swap rates closed 5-11bps lower.

- RBNZ dated OIS pricing closed sharply softer across meetings. 33bps of easing is priced for October, with a cumulative 57bps by November 2025.

- Tomorrow, the local calendar will see trade balance data.

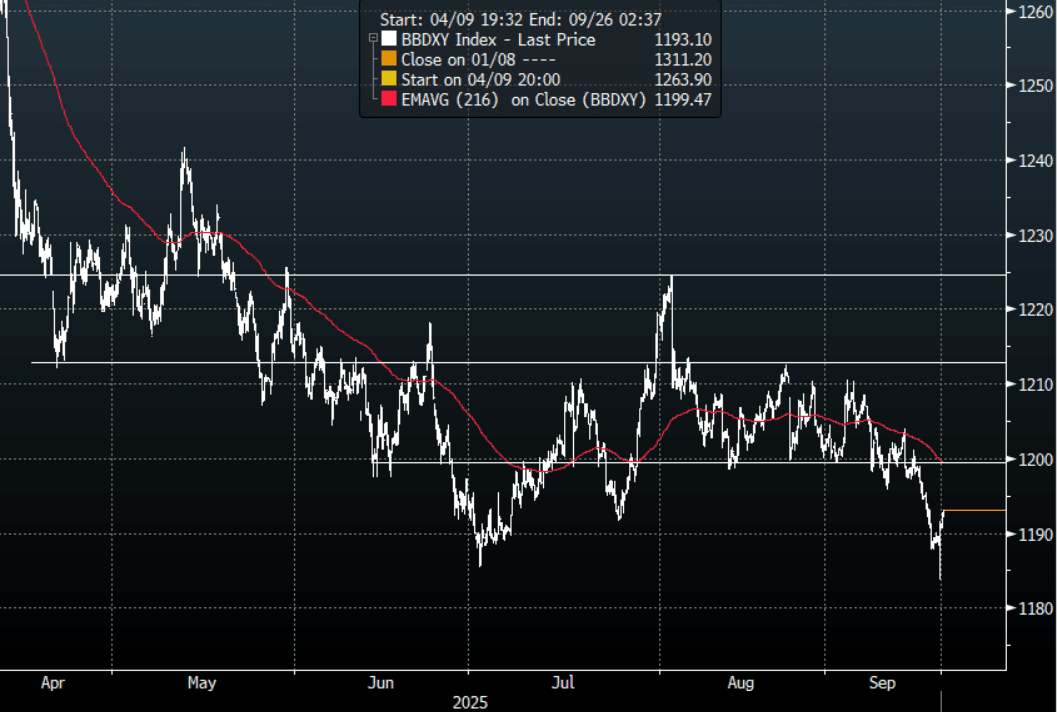

FOREX: Asia FX Wrap - The USD Gets A Reprieve, For How Long ?

The BBDXY has had a range of 1190.63 - 1192.71 in the Asia-Pac session; it is currently trading around 1193, +0.20%. The USD bounced as the Fed could not reach the levels of dovishness the market had been pricing in. How far can this market retrace, I suspect sellers would be all over a bounce back toward 1200 initially. A break below 1180 has been put off for now, but it feels like we will have another look down there at some point.

- EUR/USD - Asian range 1.1808 - 1.1829, Asia is currently trading 1.1800. The pair is is consolidating above 1.1800 after the USD failed to break lower. Should this level be sustained the first target is 1.2000 then the focus moves to the 1.2200/2300 area.

- GBP/USD - Asian range 1.3610 - 1.3635, Asia is currently dealing around 1.3610. The pair is probing the top-end of its recent 1.3350-1.3650 range after a false break overnight, price action suggests it may be looking to break these highs and reassert its momentum higher. A sustained break above 1.3650 will initially target the year's highs just below 1.3800, through here it would open a move back to the 1.4200/1.4300 area.

- USD/CNH - Asian range 7.0934 - 7.1087, the USD/CNY fix printed 7.1085, Asia is currently dealing around 7.1050. Sellers should be around on bounces while price holds below the 7.2200/2500 area and the PBOC manages the fix lower. Above 7.2500 and we could see a test of the USD Shorts.

- Cross asset : SPX +0.50%, Gold $3656, US 10-Year 4.066%, BBDXY 1193, Crude Oil $63.81

- Data/Events : EZ Current Account & Construction Output MoM, Italy Current Account Balance

Fig 1: BBDXY Spot 2H Chart

Source: MNI - Market News/Bloomberg Finance L.P

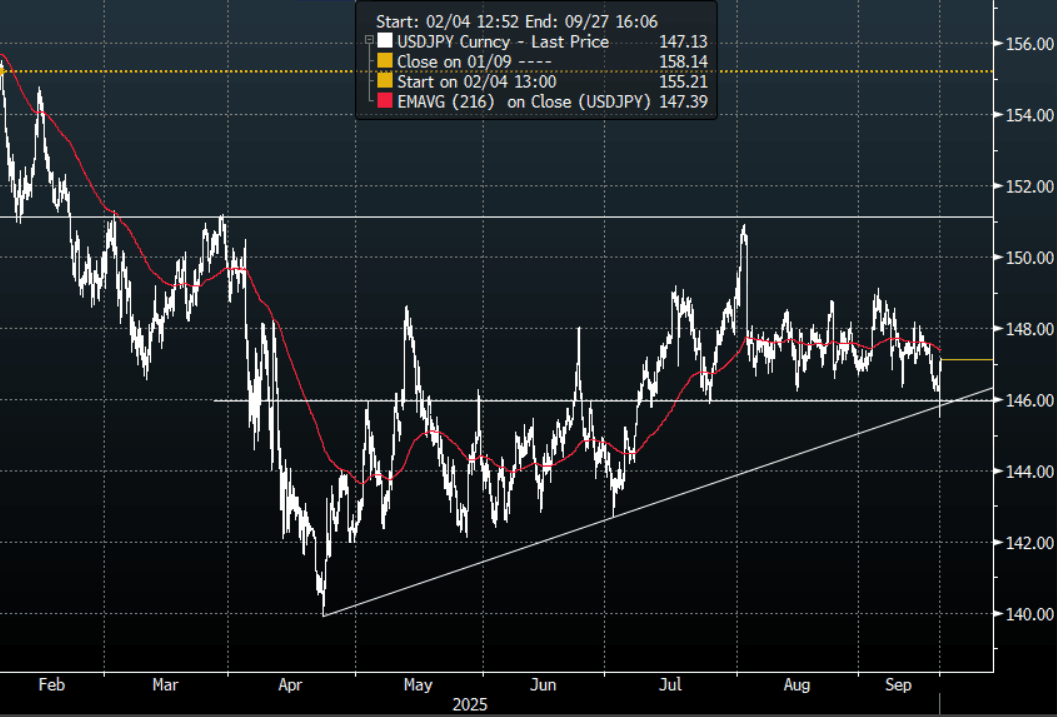

JPY: Asia Wrap - USD/JPY Consolidates Around 147.00 After False Break Lower

The USD/JPY range has been 146.77 - 147.15 in the Asia-Pac session, it is currently trading around 147.10, +0.10%. USD/JPY tried and failed to break lower as the USD bounced when the FOMC could not deliver on the markets level of dovishness priced in. The price is now back towards the middle of its recent 146-149 range, and we need a convincing break on either side to see a clearer direction again. A move back below 145/146 is needed to potentially start seeing the short Yen positions being flushed out. Just the BOJ left this week to potentially be that catalyst ?

- MNI AU - July Core Machine Orders Below Forecasts, Y/Y Momentum Holding Up: Japan July core machine orders printed below forecasts. We fell 4.6%m/m in July against a -1.5% forecast (and after a 3.0% rise in June). In y/y terms we rose 4.9%, against a 5.2% forecast and 7.6% gain in June. We are off recent highs, but the July machine orders update is not pointing to sharp weakening in y/y momentum.

- Nikkei Asia via BBG - “The Bank of Japan is expected to hold interest rates steady at its monetary policy meeting this week, Nikkei has learned, as the central bank continues to mull the effects of U.S. tariffs on wages, business investment and the domestic economy.”

- Options : Close significant option expiries for NY cut, based on DTCC data: 144.00($600m), 146.00($820m), 148.00($539m). Upcoming Close Strikes : 145.00($1.92b Sept 19), 146.40($897m Sept 19) - BBG.

- CFTC data shows last week asset managers again added to their JPY longs again as they look to rebuild their position +87239( Last +78427), leveraged funds reduced their short position perhaps losing confidence the support will continue to hold -49591(Last -66914).

Fig 1 : USD/JPY Spot 2H Chart

Source: MNI - Market News/Bloomberg Finance L.P

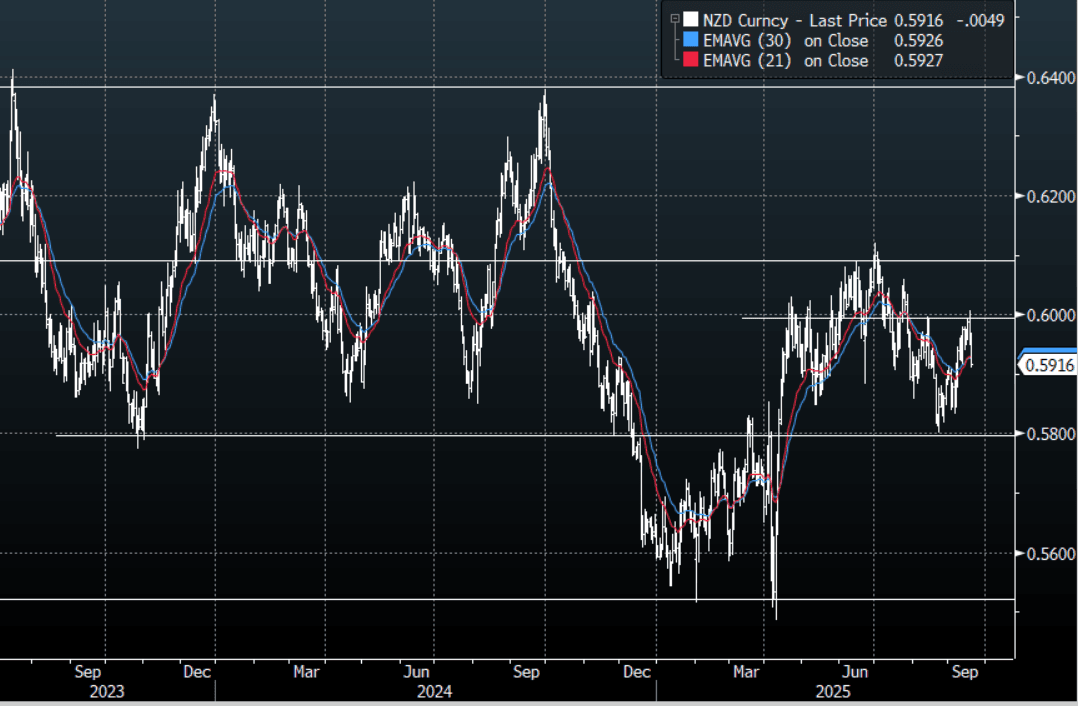

NZD: Asia Wrap - Very Weak GDP Sees NZD Underperform Across The Board

The NZD/USD had a range of 0.5911 - 0.5968 in the Asia-Pac session, going into the London open trading around 0.5920, -0.80%. The very weak GDP data this morning points to a poor backdrop for growth and increases the chance of larger rate cuts. The NZD rejected the 0.6000 area and looks set to potentially move lower now, I suspect some demand will reemerge back towards the 0.5900 area first up, through here and the pivotal 0.5800 support looms. The trend against the USD is a little harder to predict but the NZD underperformance in the crosses is beginning to gain real momentum.

- MNI AU - NZ Q2 GDP, Very Weak Growth Increases Chance Of Larger Rate Cut: Both the production and expenditure-based GDP measures fell 0.9% q/q in Q2, the weakest since the pandemic. The RBNZ had expected a 0.3% q/q decline. This and the broad-based softness across sectors as well as a sluggish recovery in Q3 to date are likely to drive 25bp rate cuts in October and November in line with the RBNZ’s August OCR path. With two votes for a 50bp cut in August, the risk of a larger move before year end is material.

- Bloomberg - Westpac Sees Kiwi Falling to 58 US Cents on Deep RBNZ Rate Cuts. Westpac now expects RBNZ to cut by 50bps at its Oct. meeting and another 25bps in November to bring the official cash rate to 2.25%. They entered a short NZD/USD position “targeting 0.5800 or lower". "The USD leg has already priced in an aggressive easing cycle, and there is no top-tier US data until GDP”.

- “ASB BANK NOW SEES RBNZ CUTTING CASH RATE TO 2.5% IN OCTOBER, NOW SEES RBNZ CUTTING CASH RATE TO 2.25% BY YEAR END" - BBG

- Options : Closest significant option expiries for NY cut, based on DTCC data: 0.5935(NZD737m). Upcoming Close Strikes : 0.6020(NZD 374m Sept 22) - BBG

- AUD/NZD range for the session has been 1.1143 - 1.1241, currently trading 1.1210. The Cross is breaking above the multiple highs around the 1.1200 area and is looking to accelerate higher on the back of some very poor Q2 GDP data. Dips should now continue to be supported as the move higher begins to gather pace.

Fig 1: NZD/USD Spot Daily Chart

Source: MNI - Market News/Bloomberg Finance L.P

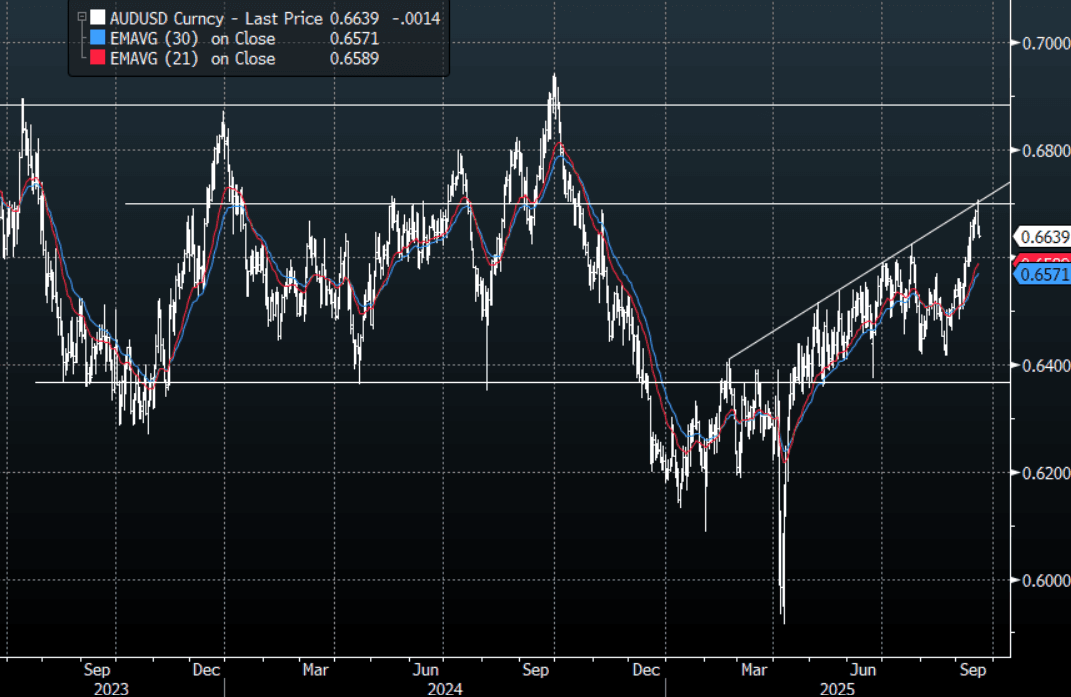

AUD: Asia Wrap - AUD/USD Extends Retracement On Employment Data

The AUD/USD has had a range of 0.6634 - 0.6659 in the Asia- Pac session, it is currently trading around 0.6640, -0.23%. The AUD pulled back overnight and this morning's unexpected drop in employment has seen the move extend lower, retracing some of its recent gains. The AUD move higher failed towards 0.6700 as the USD found some relief. Do we see a further short-term retracement in the USD, if so I suspect the reprieve is temporary. The price action in the AUD/USD suggests dips will be supported for now with the first buy-zone back towards the 0.6550 area. A retest of the 0.6700 area at some point seems to be a question of timing.

- MNI AU - Jobs Volatile, Underemployment Very Low: Australia’s monthly labour market data are volatile and August seemed to unwind July’s moves. Looking through this, annual employment growth was its lowest since the pandemic but the unemployment rate held steady at 4.2% and underemployment continued to trend down to its lowest since 1991. RBA Governor Bullock focussed on the Q2 average unemployment rate given the data’s volatility and that is likely to remain the case. September prints on 16 October.

- MNI AU - Q3 Data Show Stabilisation, Underemployment Still Trending Down: While the headline employment and unemployment rate numbers get most of the attention, the RBA looks deeper and monitors underemployment, youth unemployment, hours worked, vacancies, the quit rate and labour shortage measures closely. Governor Bullock was also clear that given the data’s volatility, it focuses on the quarterly averages. While August employment and hours were disappointing, other variables signalled that the labour market remains solid.

- " AUSTRALIA PM ALBANESE: ANNOUNCES A$5 BILLION NET ZERO FUND IN THE NATIONAL RECONSTRUCTION FUND, A$2 BILLION FOR THE CLEAN ENERGY FINANCE CORPORATION TO CONTINUE TO DRIVE DOWNWARDS PRESSURE ON ELECTRICITY PRICES" RTRS

- Options : Closest significant option expiries for NY cut, based on DTCC data: 0.6600(AUD1.13b), 0.6650(AUD774m). Upcoming Close Strikes : 0.6650(AUD906m Sept 23), 0.6750(AUD1.16b Sept 19) - BBG

Fig 1: AUD/USD spot Daily Chart

Source: MNI - Market News/Bloomberg Finance L.P

ASIA STOCKS: Global Tech Rally Benefits Asia

The global tech rally continues to support key markets in Asia with the Hang Seng Tech and the KOSDAQ up strongly. Chip related stocks were strong in Hong Kong following a regulatory ban on Nvidia, boosted expectations for growth for Chinese tech companies.

- The Hang Seng is down marginally by -0.18% whilst the CSI 300 is up +0.32%, Shanghai up +0.45% and Shenzhen up +0.70%.

- The NIKKEI is up +1.3% today, hitting new all time highs of 45,383.

- The KOSPI is up +1.13% to also reach a new high of 3,450.

- The FTSE Malay KLCI is down -0.81%, taking back all of yesterday's gains.

- The Jakarta Comp roared with the unexpected BI rate cut and is up at new all time highs of 8,046.

- The NIFTY 50 has opened Thursday strongly up +0.33% and has produced positive gains for the 17 of 19 last trading days.

OIL: Crude Trending Lower As Energy Demand In Focus

Oil prices have continued to trend lower after falling close to a percent on Wednesday driven by the Fed’s cautious tone especially in regards to downside risks to the labour market. The US dollar has also continued trending higher (BBDXY +0.2%) during today’s APAC trading impacting dollar-denominated crude. WTI is down 0.5% to $63.75/bbl off the intraday low of $63.56. It reached $64.14 early in the session. Brent is 0.3% lower at $67.73/bbl after falling to $67.50.

- The Fed’s warning of risks to the labour market added to market concerns regarding the strength of energy demand given the increase in US tariffs this year and the IEA’s forecast of a record oil surplus in 2026. The 25bp Fed cut was widely expected and so the outlook for future meetings will be monitored closely.

- Geopolitical risks stemming from Ukrainian attacks on Russian refining and export facilities as well as increased sanctions on Russia and those who buy its fossil fuels persist.

- Later the August US lead index, September Philly Fed and jobless claims print. The BoE is expected to leave rates unchanged at 4% and the ECB’s Lagarde, Buch, de Guindos and Schnabel speak.

Gold Holds Losses As USD Strengthens

The US dollar continued trending higher (BBDXY +0.2%) during today’s APAC trading, thus gold prices are moderately lower. They are down 0.1% to $3655/oz off the intraday low of $3651.98 which followed a peak of $3672.06. The downside has been limited by slightly lower Treasury yields.

- The Fed cut rates as expected due to a weaker labour market and Chair Powell’s comments were cautious. He said that “there’s no risk-free path now” and that while 10 FOMC members indicated two or more rate cuts by year end, 9 had fewer and so the committee is “in a meeting by meeting situation”. While Powell noted upside risks to inflation, he said that the impact from higher tariffs had been less than expected to date.

- The administration’s new FOMC appointment Miran voted for a 50bp cut adding to fears for the Fed’s independence.

- Silver has continued falling today after Wednesday’s 2.1% drop. It is currently down 0.7% to $41.38 after a low of $41.309.

- Equities are mixed with the S&P e-mini up 0.5% and CSI 300 +0.3% but Hang Seng down 0.2% and ASX -0.6%. Oil prices are lower with WTI -0.4% to $63.80/bbl. Copper is down 0.4%.

- Later the August US lead index, September Philly Fed and jobless claims print. The BoE is expected to leave rates unchanged at 4% and the ECB’s Lagarde, Buch, de Guindos and Schnabel speak.

UP TODAY (TIMES GMT/LOCAL)

| Date | GMT/Local | Impact | Country | Event |

| 18/09/2025 | 0710/0910 | ECB Lagarde Video Message at Women Leadership Summit | ||

| 18/09/2025 | 0800/1000 | *** | Norges Bank Rate Decision | |

| 18/09/2025 | 0800/1000 | ** | EZ Current Account | |

| 18/09/2025 | 0800/1000 | ECB de Guindos at MNI Connect Event | ||

| 18/09/2025 | 0900/1100 | ** | EZ Construction Output | |

| 18/09/2025 | 0945/1145 | ECB Schnabel Chairs Panel at ECB Research Conference | ||

| 18/09/2025 | 1100/1200 | *** | Bank Of England Interest Rate | |

| 18/09/2025 | 1100/1200 | *** | Bank Of England Interest Rate | |

| 18/09/2025 | 1230/0830 | *** | Jobless Claims | |

| 18/09/2025 | 1230/0830 | ** | WASDE Weekly Import/Export | |

| 18/09/2025 | 1230/0830 | ** | Philadelphia Fed Manufacturing Index | |

| 18/09/2025 | 1430/1030 | ** | Natural Gas Stocks | |

| 18/09/2025 | 1530/1130 | * | US Bill 08 Week Treasury Auction Result | |

| 18/09/2025 | 1530/1130 | ** | US Bill 04 Week Treasury Auction Result | |

| 18/09/2025 | 1700/1300 | ** | US Treasury Auction Result for TIPS 10 Year Note | |

| 18/09/2025 | 1915/1515 | BOC speech on payments ecosystem from director Ron Morrow. | ||

| 18/09/2025 | 2000/1600 | ** | TICS | |

| 19/09/2025 | 2301/0001 | ** | Gfk Monthly Consumer Confidence | |

| 19/09/2025 | 2330/0830 | *** | CPI | |

| 19/09/2025 | 0200/1100 | *** | BOJ Policy Rate Announcement | |

| 19/09/2025 | 0600/0700 | *** | Public Sector Finances | |

| 19/09/2025 | 0600/0700 | *** | Retail Sales | |

| 19/09/2025 | 0600/0800 | ** | PPI | |

| 19/09/2025 | 0645/0845 | ** | Manufacturing Sentiment | |

| 19/09/2025 | 1005/1205 | ECB Lagarde and Cipollone at Eurogroup ECOFIN Meeting | ||

| 19/09/2025 | 1230/0830 | ** | Retail Trade | |

| 19/09/2025 | 1230/0830 | ** | Retail Trade |