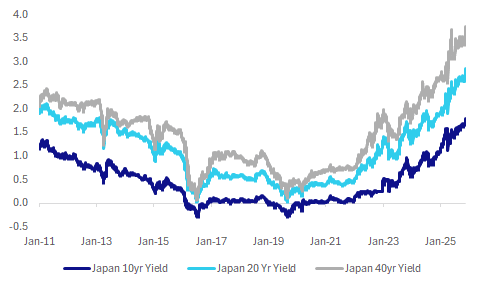

MNI EUROPEAN OPEN: JGB Yields Surge Higher

EXECUTIVE SUMMARY

- FOMC DEEPLY SPLIT ON NEED FOR MORE RATE CUTS - MINUTES - MNI

- NVIDIA’S UPBEAT FORECAST SOOTHES FEARS OF AI SPENDING BUBBLE - BBG

- BOJ’S KOEDA SEES UNDERLYING CPI AT 2% - MNI BRIEF

- JAPAN FINALIZING ECONOMIC STIMULUS PACKAGE WORTH 21.3t YEN: NHK

- CHINA WEIGHS NEW PROPERTY STIMULUS PACKAGE AS CRISIS DRAGS ON - BBG

Fig 1: Japan JGB Yields Breaking Higher

Source: MNI - Market News/Bloomberg/Refinitiv.

UK

RUSSIA (BBC): “A Russian spy ship has used lasers for the first time to disrupt RAF pilots tracking its activity near UK waters, the defence secretary has said. John Healey told reporters the "deeply dangerous" move from the Yantar was being taken "extremely seriously" by the government.”

POLITICS (BBC): “Labour MP Clive Lewis has offered to give up his seat to allow Andy Burnham to challenge Sir Keir Starmer for the Labour leadership. There has been ongoing speculation that Greater Manchester Mayor Burnham wants to take on Sir Keir for the top job, but he would need to be an MP to do so.”

HOUSING (TIMES): “Nearly 20 per cent of potential home movers have put their plans on hold due to possible property tax changes in the budget next week, according to research.”

EU

UKRAINE (BBC): “Senior Pentagon officials have arrived in Ukraine to "discuss efforts to end the war" with Russia, the US military has said. The team, led by US Army Secretary Dan Driscoll, is expected to meet Ukrainian President Volodymyr Zelensky in Kyiv on Thursday when he returns from a trip to Turkey.”

EU (POLITICO): “EU foreign ministers will be briefed on Thursday about a spate of sabotage attempts and airspace incursions that Russia’s neighbors say marks a “very dangerous phase of escalation” by the Kremlin, and one that endangers civilians. Lithuania’s Foreign Minister Kęstutis Budrys told POLITICO that the Kremlin’s shadowy campaign of subversion shows “we are reaching the hot phases of escalation.””

EU (POLITICO): “Top EU diplomat Kaja Kallas sounded the alarm for Europe on Wednesday after Warsaw accused Russian-backed operatives of carrying out an explosion targeting a Polish railway. “It is clear that these kinds of attacks are an extreme danger also for our critical infrastructure,” Kallas told journalists.”

EU (POLITICO): “A fresh proposal by European Commission President Ursula von der Leyen to reform digital laws on Wednesday was welcomed by lawmakers on the right but shunned on the left.”

US

FED (MNI): Federal Reserve officials offered "strongly differing views" about whether to keep cutting rates this year after deciding to reduce them at the October meeting, as policymakers balanced conflicting risks of higher inflation and weaker employment, minutes released Wednesday showed.

TECH (BBG): “ Nvidia Corp. delivered a surprisingly strong revenue forecast and pushed back on the idea that the AI industry is in a bubble, easing concerns that had spread across the tech sector.”

TECH (BBG): White House officials are urging members of Congress to reject a measure that would limit Nvidia Corp.’s ability to sell AI chips to China and other adversary nations, according to people familiar with the matter, dimming prospects for legislation opposed by the world’s most valuable company.

FED (MNI BRIEF): The Federal Reserve should interfere in financial markets as little as possible which means shrinking the balance sheet to the fullest extent it can, Fed Governor Stephen Miran said Wednesday.

OTHER

JAPAN (MNI BRIEF): Bank of Japan board member Junko Koeda said Thursday that the BOJ will continue raising its policy interest rate to adjust the degree of monetary easing in line with improvements in the economy and prices, though she gave no indication of the timing of the next move.

JAPAN (BBG): “The yen is experiencing sudden, one-way movements that are concerning and which require close monitoring, Japan’s chief cabinet secretary said. Excessive fluctuations and disorderly movements in exchange rates must be monitored with vigilance, Minoru Kihara said during a press conference on Thursday.

JAPAN (NHK/BBG): “The Japanese government is making final arrangements to compile an economic stimulus package of ~21.3t yen, public broadcaster NHK reports, citing an unidentified person.”

CANADA (MNI): Business leaders see Canada as a hard place to invest central bank deputy Nicolas Vincent said in a speech Wednesday aimed at creating dialogue about the affordability squeeze, but also pressures governments to build an economy that can grow faster without boosting inflation.

CHINA

PROPERTY (BBG): “ China is considering new measures to turn around its struggling property market, as concerns mount that a further weakening of the sector will threaten to destabilize its financial system, according to people familiar with the matter.”

LOAN PRIME RATES (MNI BRIEF): China’s Loan Prime Rate was left unchanged on Thursday, as expected, with the central bank maintaining its stance amid ongoing pressure on banks’ interest margins and confidence that the 5% annual GDP growth target remains within reach.

CHINA/JAPAN (YICAI): “Chinese travellers have cancelled more than 500,000 flight tickets to Japan, with passengers sharply down for three consecutive days, as geopolitical tensions between the two countries intensify, according to Yicai.”

MNI: PBOC Net Injects CNY110 Bln via OMO Thursday

MNI (BEIJING) - The People's Bank of China (PBOC) conducted CNY300 billion via 7-day reverse repos, with the rate unchanged at 1.40%. The operation led to a net injection of CNY110 billion after offsetting maturities of CNY190 billion today, according to Wind Information

The seven-day weighted average interbank repo rate for depository institutions (DR007) fell to 1.4091% at 09:41 am local time from the close of 1.5131% on Wednesday.

- The CFETS-NEX money-market sentiment index, measuring interbank money-market liquidity, closed at 49 on Wednesday, compared with the close of 51 on Tuesday. A higher reading points to tighter liquidity condition, with 50 representing an equilibrium.

MNI: PBOC Sets Yuan Parity Higher At 7.0905 Thurs; +1.96% Y/Y

MNI (BEIJING) - The People's Bank of China (PBOC) set the dollar-yuan central parity rate higher at 7.0905 on Thursday, compared with 7.0872 set on Wednesday. The fixing was estimated at 7.1228 by Bloomberg survey today.

MARKET DATA

CHINA OCT. SHARE OF SWIFT GLOBAL PAYMENTS 2.47%; SEP. 3.17%

MARKETS

US TSYS: Labour Data Tonight Last Chance for Rate Cuts

- The ever diminishing hope for a December rate cut hinges on the labour market data out Thursday in the US.

- Bond futures were lower across maturities with the 10-Yr down -03 to 112.19, remaining at the mid-point between the 50-day EMA of 112-25+ and the 100-day EMA of 112-14+.

Whilst the ultra long end was broadly flat on the day, elsewhere on the curve saw yields higher by up to +1.5bps as rate expectations continue to re-price. Fed meeting expectations re-priced further: Dec'25 at -6bp (-7bps at open), Jan'26 at -20.1bp, Mar'26 at -0.29bps (-30.3bp), Apr'26 at -36.6 (-38.1bp).

- The 2-Yr is up +1.3bps to 3.606%

- The 5-Yr is up +1.1bps to 3.721%

- The 10-Yr is up +0.4bps to 4.143%

- The 30-Yr is flat at 4.75%

Key focus for issuance tonight will be 4-week and 8-week bills and a 10-Yr TIPS auction.

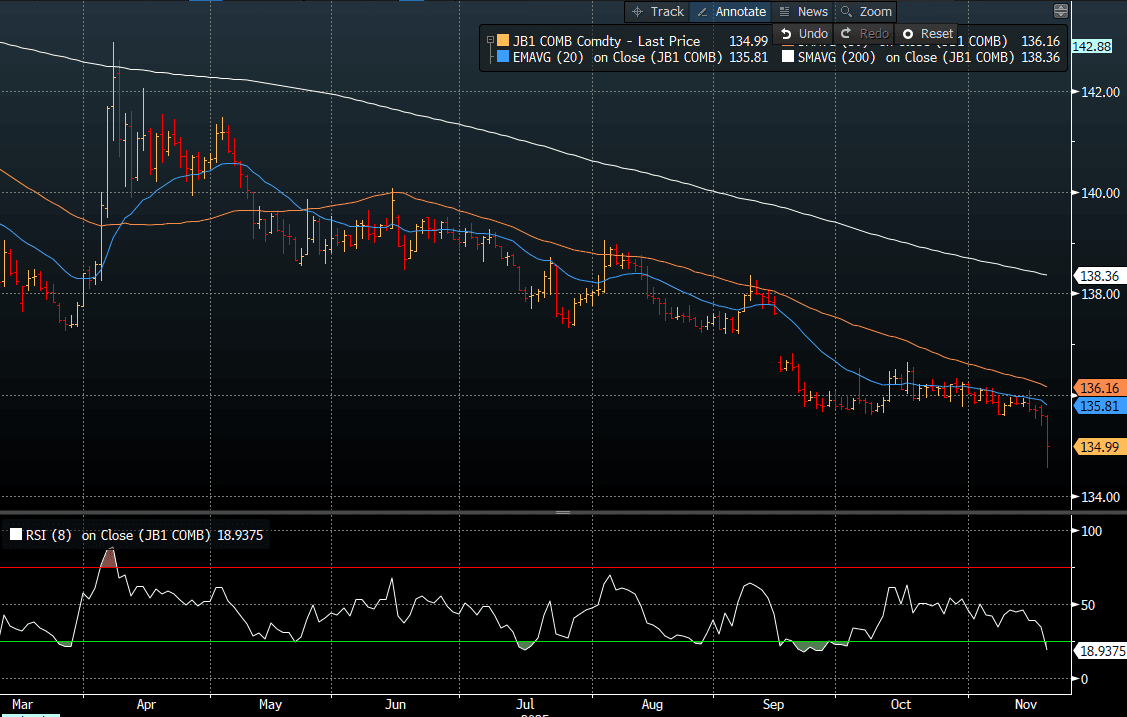

JGBS: Yields Explode Higher As Fiscal Fears Drive Positioning Change

JGB futures are trading sharply weaker at 134.99, -62 compared to settlement levels, albeit well above the session low of 134.56. (see chart)

- MNI’s technical analysts had viewed fresh cycle lows as confirmation of the downtrend that had dominated prices since mid-September. Their Fibonacci projection of 134.69 was hit today.

- “The Japanese government is making final arrangements to compile an economic stimulus package of ~21.3t yen, public broadcaster NHK reports, citing an unidentified person.” - BBG

- "Major investors, including domestic banks, insurers, and overseas accounts, collectively pared net purchases of 10-year JGBs to the lowest since October 2023, according to the latest Japan Securities Dealers Association data. In contrast, demand remained firm for 2- to 5-year notes, while super-long bonds also continued to see modest net buying." – BBG

- BoJ Koeda's speech appeared to be in line with recent rhetoric from key BoJ board members. There were some hawkish undertones, although she didn't give any hints on rate hike timing.

- Cash JGBs are off worst levels but remain 2-7bps cheaper across benchmarks. The 10-year yield is currently at 1.813% versus a session high of 1.845%.

- Tomorrow’s local calendar will see National CPI, Trade Balance and S&P Global PMI(P) data alongside an Enhanced Liquidity Auction for 1-5-year JGBs.

Source: Bloomberg Finance LP

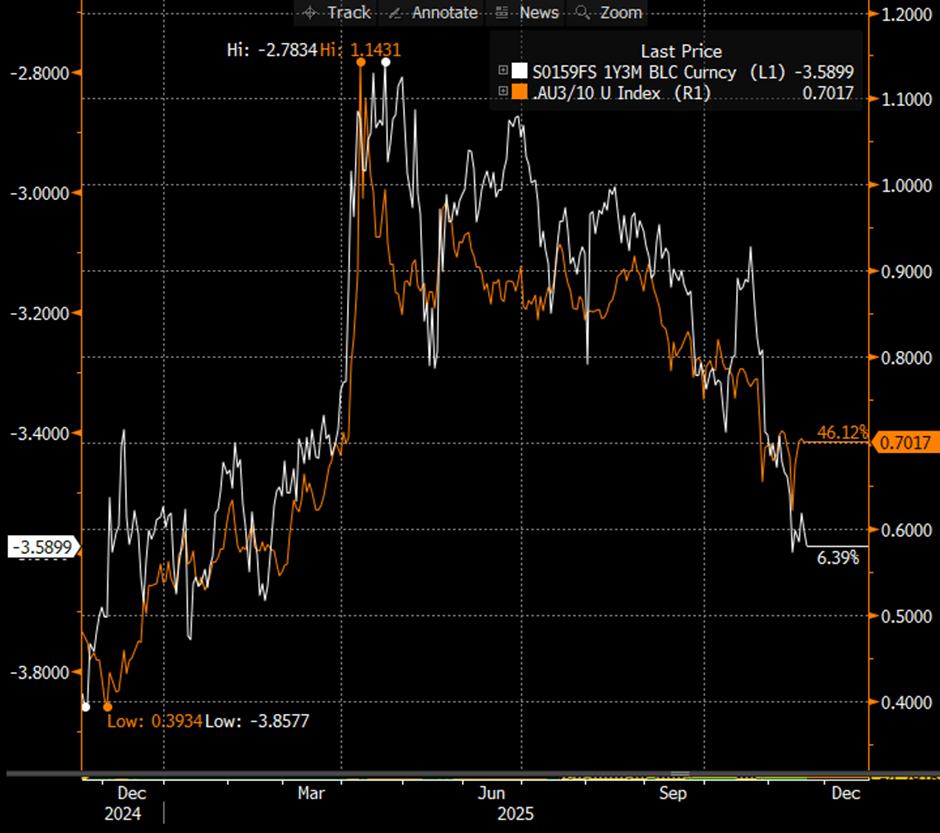

AUSSIE BONDS: Trading Heavy As RBA Research Suggests Prolonged Pause

ACGBs (YM -5.0 & XM -5.0) are weaker and at/near session lows.

- Cash US tsys are slightly mixed, with a flattening bias, in today's Asia-Pac session as the market continues to digest yesterday's release of the FOMC Minutes.

- Cash ACGBs are 5bps cheaper, with the AU-US 10-year yield differential at +33bps.

- Unlike its New Zealand counterpart, which has recently steepened to its highest level since 2021, the ACGB yield curve remains near its flattest point since April, albeit slightly steeper than its recent low. Moreover, the AU 3s10s yield curve appears vulnerable to any upward revision in year-ahead cash rate expectations (see chart).

- Assistant Governor Hunter spoke today on RBA research in areas where the transmission of monetary policy may have changed. The research appears to reflect that the economy has been stronger than the RBA expected, including inflation. This may be another indication that its current pause could be prolonged.

- RBA-dated OIS pricing is showing a 25bp rate cut in December at a 2% probability, with a cumulative 10bps of easing priced by mid-2026.

- The bills strip is -4 to -7 beyond the 1st contract (-1).

- Tomorrow, the local calendar will see S&P Global PMIs (P).

- The AOFM plans to sell A$700mn of the 1.25% 21 May 2032 bond on Friday.

Bloomberg Finance LP

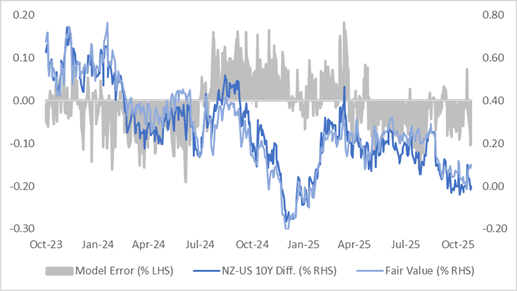

BONDS: NZGBS: Bear-Steepener, NZ-US 10Y Diff Looks Too Low

NZGBs closed showing a bear-steepener, with benchmark yields flat to 4bps higher.

- Cash US tsys are slightly mixed, with a flattening bias, in today's Asia-Pac session as the market continues to digest yesterday’s release of the FOMC Minutes for the October meeting.

- The NZ-US 10-year yield differential finished 2bps wider at flat. A simple regression of the 1Y3M forward swap spread against the 10-year yield differential over the past three years suggests the current differential is about 10bps below its estimated fair value of +10bps. The regression’s standard error has been ±15bps over the past two years, highlighting the inherent variability in the relationship. Even so, the 1Y3M spread continues to anchor market expectations around the longer-term path of yield convergence. (see chart)

- Swap rates closed 2-5bps higher, with implied swap spreads wider.

- RBNZ dated OIS pricing closed little changed across meetings. 25bps of easing is priced for November, with a cumulative 34bps by February 2026.

- Tomorrow, the local calendar will see Trade Balance data.

Figure 1: NZ-US 10-Year Yield Differential

Source: Bloomberg Finance LP / MNI

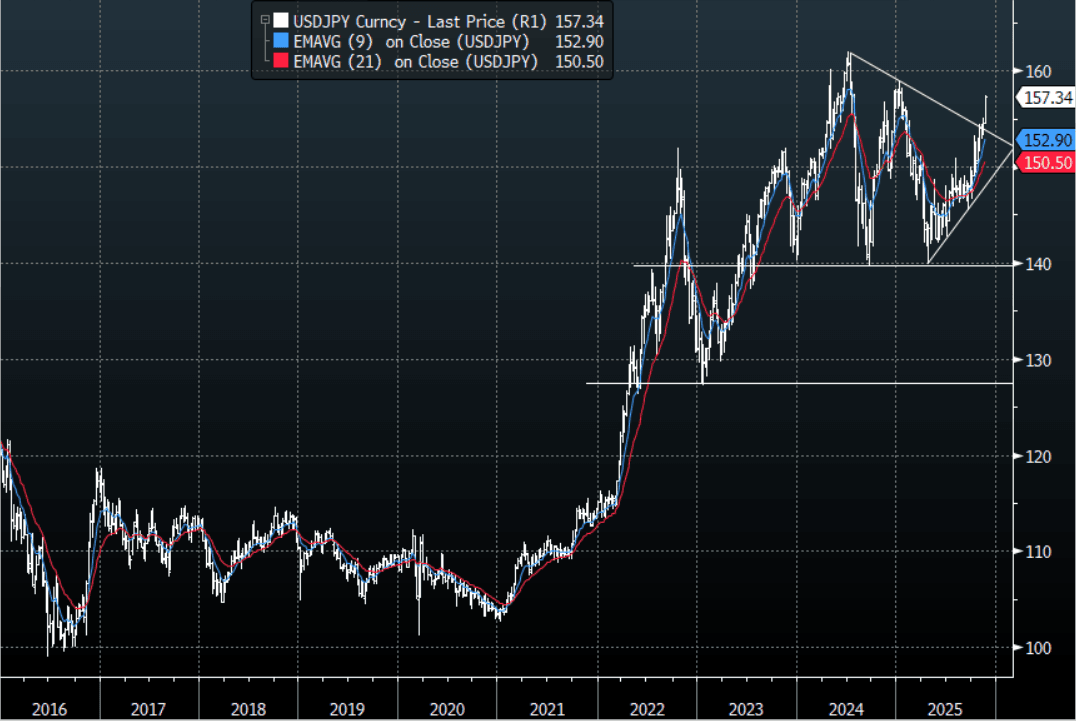

JPY: USD/JPY - Building On Gains Above 157.00

The USD/JPY range today has been 156.88 - 157.47 in the Asia-Pac session, it is currently trading around 157.35, +0.15%. The pair continued to extend higher in our session as dips remain well supported. This price action will certainly worry officials as this acceleration above 155 looks ominous and on track for a very quick test of the 160 highs seen in 2024. Japan is in a tough bind, they want to provide a significant stimulus package to boost the economy, they want to cap bond yields and they also do not want USD/JPY to explode higher. Some would say that is an impossible task and they will have to let something go, the easiest lever to pull back on is the Yen. This will not make the US happy but it's a far easier and palatable outcome than bond yields getting out of control. I suspect they will have to show some sign of fighting this above 160, but given the current inputs this could potentially go a lot higher than that.

- MNI AU - Koeda - Gives Upbeat Comments On Inflation But No Hint On Rate Hike Timing: Headlines have crossed from BoJ board member Koeda's speech. At first glance they appear in line with recent rhetoric from key BoJ board members. There were some hawkish undertones, with Koeda noting that the central bank must normalize rates to avoid distortions in the future and that underlying inflation is around 2%. She didn't give any hints on rate hike timing (which is hardly surprising ahead of Ueda's speech on Dec 1).

- "JAPAN’S 30-YEAR YIELD HITS FRESH RECORD HIGH SINCE 1999 DEBUT" - BBG

- “JAPAN CHIEF CABINET SECRETARY KIHARA: WATCHING MARKET MOVES, INCLUDING BOND MARKET, CLOSELY. RECENT FX MOVES ARE SHARP, ONE-SIDED" RTRS

- “KATAYAMA: HARD TO STRIKE BALANCE BTWN PRICES, RATES, WEAK YEN. RATES, FX ARE DECIDED BY MARKET ON VARIOUS FACTORS" - BBG

- Options : Close significant option expiries for NY cut, based on DTCC data: 155.00($1.49b). Upcoming Close Strikes : 155.00($933m Nov 21), 155.00{$824m Nov 24), 156.00($795m Nov 21) - BBG.

- The USD/JPY Average True Range(ATR) for the last 10 Trading days: 105 Points

Fig 1 : USD/JPY Spot Weekly Chart

Source: MNI - Market News/Bloomberg Finance L.P

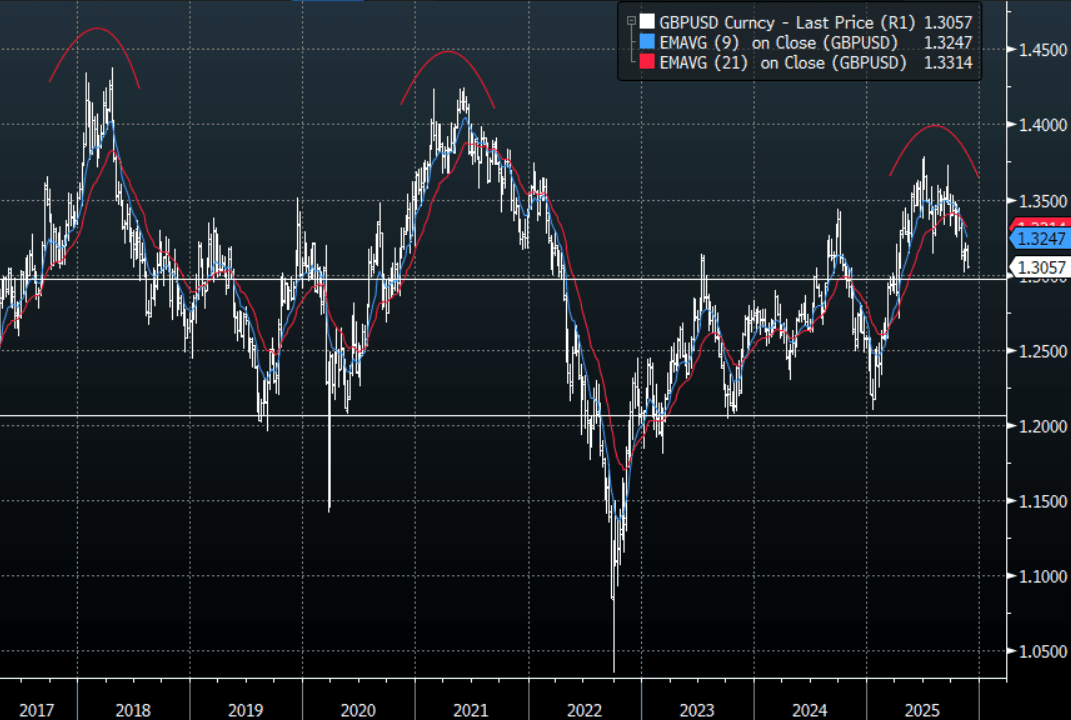

FOREX: USD - BBDXY Consolidates Overnight Gains

The BBDXY has had a range today of 1224.32 - 1226.47 in the Asia-Pac session; it is currently trading around 1225, +0.05%. The USD has grinded higher in our session trying to build on its overnight gains. The break back above 1221-1222 saw the USD accelerate higher and is now looking to challenge the pivotal 1230-40 area. On the day I would now be looking for dips toward 1222-1224 to be supported as the market tries to build a base from which to extend higher.

- EUR/USD - Asian range 1.1510 - 1.1542, Asia is currently trading 1.1520. The pair broke lower overnight as the USD moved higher across the board. On the day look for sellers to reemerge back toward the 1.1545-65 area, as the market looks to challenge the support toward 1.1400.

- GBP/USD - Asian range 1.3038 - 1.3063, Asia is currently dealing around 1.3145. I continue to favor fading rallies, as GBP looks to have put in a medium term top. GBP broke back below the 1.3100 support and accelerated toward the 1.3000 area overnight. I suspect rallies back toward the 1.3075-1.3095 area will be faded if we do see a bounce as the market looks to challenge the 1.3000 support.

- Cross asset : SPX +1.30%, Gold $4075, US 10-Year 4.135%, BBDXY 1225, Crude Oil $59.58

- Data/Events : EZ Construction Output MoM, Germany PP

Fig 1: GBP/USD Spot Weekly Chart

Source: MNI - Market News/Bloomberg Finance L.P

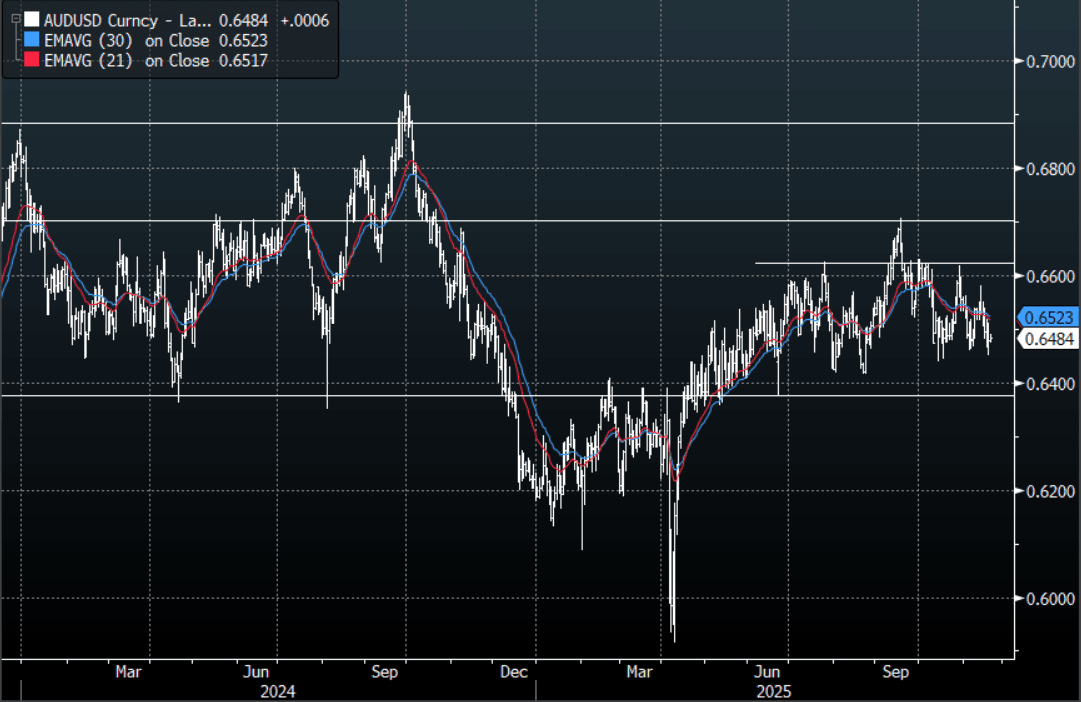

AUD/USD - Drifts Higher With Risk

The AUD/USD has had a range today of 0.6474 - 0.6491 in the Asia- Pac session, it is currently trading around 0.6485, +0.10%. The AUD/USD has drifted higher in our session thanks to the gains for global risk provided by the strong Nvidia earnings. The AUD/USD continues to chop around within its wider 0.6350-0.6650 range, the first support is right here around 0.6440-0.6460 which has been pretty solid the last couple of months, then 0.6350 below that. It would need this move lower in risk to accelerate and become something more significant to challenge down there I would think. The AUD would need to move back above the 0.6530 area for the direction to change, until then suspect we see offers above 0.6500 initially.

- MNI AU - RBA Researching Why Inflation & Housing Stronger Than It Expected: Assistant Governor (Economic) Hunter spoke today on RBA research in areas where the transmission of monetary policy may have changed. She said it is looking at if businesses have changed price-setting after Covid, how to estimate capacity and full employment, and if monetary policy transmission channels have changed, given the larger than expected housing response to 2025’s 75bp of easing. The research appears to reflect where the economy has been stronger than the RBA expected, including inflation. This may be another indication that its current pause could be prolonged.

- Options : Closest significant option expiries for NY cut, based on DTCC data: 0.6500(AUD736m), 0.6530 (AUD422m), 0.6550 (AUD739m). Upcoming Close Strikes : 0.6550(AUD2.28b Nov 21) - BBG

- The AUD/USD Average True Range for the last 10 Trading days: 51 Points

Fig 1: AUD/USD spot Daily Chart

Source: MNI - Market News/Bloomberg Finance L.P

NZD/USD - Grinds Back Above 0.5600 As Risk Surges Higher

The NZD/USD had a range today of 0.5595 - 0.5615 in the Asia-Pac session, going into the London open trading around 0.5610, +0.15%. The NZD/USD has tried to push higher but the move has been very underwhelming considering the move in risk, perhaps the relief rally arrives when London comes in. The next target is the pivotal 0.5500 area which has been very strong support in the past. On the day look for rallies back toward 0.5635-0.5655 to find sellers initially if we do get a bounce.

- Options : Closest significant option expiries for NY cut, based on DTCC data: 0.5675(NZD300m). Upcoming Close Strikes : 0.5480(NZD644m Nov 21), 0.5600(NZD450m Nov 25), 0.5720(NZD646m Nov 25) - BBG

- The NZD/USD Average True Range for the last 10 Trading days: 41 Points

Fig 1: NZD/USD Spot Weekly Chart

Source: MNI - Market News/Bloomberg Finance L.P

ASIA STOCKS: Tech Stocks Boosted by Nvidia, US Rate Outlook Concerns Remain

Nvidia's stronger earnings gave those tech heavy bourses a boost today, bouncing back from several days of caution. For those markets less tech-led the overnight softening of expectations for US rate cuts, the mood was less buoyant and will watch carefully for the key data release tonight on US labour markets. Korea, Japan and Taiwan led the way today with some individual stocks delivering strong daily returns.

- The NIKKEI had it's biggest daily gain since in a month as it jumped +2.8% today as it tries to hold above 49,900

- The KOSPI roared back above 4,000 with gains of almost 3% as SK Hynix jumped +1.2% and Samsung +4.8%

- TSMC in Taiwan led the way with gains of almost 4% as the TAIEX rose +3.1%

- China's major bourses were mostly green today, though returns were much more subdued. The Hang Seng rose just +0.14% and CSI 300 +0.38% whilst Shenzhen fell -0.10%

- SE Asian bourses all were up with Jakarta up +0.8%, Malaysia +0.27% and SE Thai +1.4%

- India's NIFTY 50 is up modestly at the open by +0.19% as new highs are reached of 26,108 as profits for the largest 100 firms grew 12% for the September quarter according to BBG.

OIL: Crude Slightly Higher As Watching Russia Events, New Sanctions From Friday

Oil prices are slightly higher in today’s APAC session but have been moving in a very narrow range as they wait for key US economic data and any further developments on a Ukraine-Russia deal after reports of a new US peace plan. WTI is up 0.2% to $59.58/bbl off the intraday high at $59.81 and Brent is 0.3% higher at $63.69/bbl after peaking at $63.83.

- Bloomberg is reporting an increase in tankers booked to bring crude from the Middle East to India signalling a shift away from Russia. Sanctions on Russian majors Rosneft and Lukoil come into effect on Friday and there have already been signs of a shift away from them and to other smaller Russian suppliers and non-Russian sources.

- The pressure is likely to stay on Russia with European leaders speaking out against its aggression involving Poland and other EU members, as well as the UK this week. The EU is also looking at measures to curtail the ongoing problem of its shadow fleet. Rosneft and Lukoil have begun considering options to divest their overseas assets.

- Later the Fed’s Hammack, Barr, Cook, Goolsbee, Miran and Paulson speak as well as BoE’s Mann and Dhingra. US November 15 jobless claims, delayed September payrolls, November Philly & Kansas Fed Indices, October existing home sales and euro area preliminary November consumer confidence print.

- Bloomberg consensus expects the US unemployment rate to be stable at 4.3% in September, payrolls to rise 51k and average earnings to rise 0.3% m/m.

Gold Steady As Fed Cut Pricing Down & US$ Up, Sept Payrolls Out Later

Gold prices are slightly lower in Thursday’s APAC trading following the October FOMC minutes showing “strongly differing views” as a result pricing for a December rate cut fell substantially and the US dollar rose, both usually negatives for non-yield bearing bullion. The US dollar is slightly higher again today and risk appetite stronger following Nvidia’s results. Gold will be monitoring US data closely, especially today’s September payrolls, as delayed releases are published.

- Our US analysts believe that Q3 GDP and November payrolls & CPI should be released before the 10 December Fed decision.

- Gold is flat at $4077.2 off the intraday low of $4042.1 which followed a peak of $4110.15, above initial resistance at $4106.7, 17 November high.

- Silver is flat at $51.36 after falling to $50.694 following an increase to $51.869 earlier. The bull trigger is at $54.480.

- Equities are rallying with the S&P e-mini up 1.2% and KOSPI +3.0%. Oil prices are slightly higher with WTI +0.2% to $59.55/bbl. Copper is down 0.1%.

- Later the Fed’s Hammack, Barr, Cook, Goolsbee, Miran and Paulson speak as well as BoE’s Mann and Dhingra. US November 15 jobless claims, delayed September payrolls, November Philly & Kansas Fed Indices, October existing home sales and euro area preliminary November consumer confidence print.

- Bloomberg consensus expects the US unemployment rate to be stable at 4.3% in September, payrolls to rise 51k and average earnings to rise 0.3% m/m.

UP TODAY (TIMES GMT/LOCAL)

| Date | GMT/Local | Impact | Country | Event |

| 20/11/2025 | 0700/0800 | ** | PPI | |

| 20/11/2025 | 1000/1100 | ** | EZ Construction Output | |

| 20/11/2025 | 1100/1100 | ** | CBI Industrial Trends | |

| 20/11/2025 | 1330/0830 | *** | Jobless Claims | |

| 20/11/2025 | 1330/0830 | ** | WASDE Weekly Import/Export | |

| 20/11/2025 | 1330/0830 | * | Industrial Product and Raw Material Price Index | |

| 20/11/2025 | 1330/0830 | ** | Philadelphia Fed Nonmanufacturing Index | |

| 20/11/2025 | 1330/0830 | *** | Employment Report | |

| 20/11/2025 | 1330/0830 | *** | Employment Report | |

| 20/11/2025 | 1330/0830 | *** | Employment Report | |

| 20/11/2025 | 1330/0830 | *** | Employment Report | |

| 20/11/2025 | 1330/0830 | *** | Employment Report | |

| 20/11/2025 | 1330/0830 | *** | Employment Report | |

| 20/11/2025 | 1345/0845 | Cleveland Fed's Beth Hammack | ||

| 20/11/2025 | 1430/0930 | Fed Governor Michael Barr | ||

| 20/11/2025 | 1500/1000 | *** | NAR existing home sales | |

| 20/11/2025 | 1500/1000 | * | Services Revenues | |

| 20/11/2025 | 1500/1600 | ** | Consumer Confidence Indicator (p) | |

| 20/11/2025 | 1530/1030 | ** | Natural Gas Stocks | |

| 20/11/2025 | 1600/1100 | ** | Kansas City Fed Manufacturing Index | |

| 20/11/2025 | 1600/1100 | Fed Governor Lisa Cook | ||

| 20/11/2025 | 1630/1130 | ** | US Bill 04 Week Treasury Auction Result | |

| 20/11/2025 | 1630/1130 | * | US Bill 08 Week Treasury Auction Result | |

| 20/11/2025 | 1740/1240 | Chicago Fed's Austan Goolsbee | ||

| 20/11/2025 | 1800/1300 | ** | US Treasury Auction Result for TIPS 10 Year Note | |

| 20/11/2025 | 1830/1830 | BOE Dhingra Speech on Trade and Tariffs | ||

| 20/11/2025 | 2100/2100 | BOE Mann at IMF Statistical Forum | ||

| 21/11/2025 | 2200/0900 | *** | Judo Bank Flash Australia PMI | |

| 20/11/2025 | 2315/1815 | Fed Governor Stephen Miran | ||

| 21/11/2025 | 2330/0830 | *** | CPI | |

| 20/11/2025 | 2345/1845 | Philly Fed's Anna Paulson | ||

| 21/11/2025 | 0001/0001 | ** | Gfk Monthly Consumer Confidence | |

| 21/11/2025 | 0030/0930 | ** | Jibun Bank Flash Japan PMI | |

| 21/11/2025 | 0700/0700 | *** | Public Sector Finances | |

| 21/11/2025 | 0700/0700 | *** | Retail Sales | |

| 21/11/2025 | 0745/0845 | ** | Manufacturing Sentiment | |

| 21/11/2025 | 0800/0900 | ECB de Guindos Remarks/Q&A at Foro Gran Via | ||

| 21/11/2025 | 0815/0915 | ** | S&P Global Services PMI (p) | |

| 21/11/2025 | 0815/0915 | ** | S&P Global Manufacturing PMI (p) | |

| 21/11/2025 | 0830/0930 | ** | S&P Global Services PMI (p) | |

| 21/11/2025 | 0830/0930 | ** | S&P Global Manufacturing PMI (p) | |

| 21/11/2025 | 0830/0930 | ECB Lagarde Speech at European Banking Congress | ||

| 21/11/2025 | 0900/1000 | ** | S&P Global Services PMI (p) | |

| 21/11/2025 | 0900/1000 | ** | S&P Global Manufacturing PMI (p) | |

| 21/11/2025 | 0900/1000 | ** | S&P Global Composite PMI (p) | |

| 21/11/2025 | 0930/0930 | *** | S&P Global Manufacturing PMI flash | |

| 21/11/2025 | 0930/0930 | *** | S&P Global Services PMI flash | |

| 21/11/2025 | 0930/0930 | *** | S&P Global Composite PMI flash | |

| 21/11/2025 | 1000/1100 | Negotiated Wage Growth | ||

| 21/11/2025 | 1130/1230 | ECB de Guindos Remarks/Q&A at Deusto Business School | ||

| 21/11/2025 | 1230/0730 | New York Fed's John Williams | ||

| 21/11/2025 | 1330/0830 | ** | Retail Trade | |

| 21/11/2025 | 1330/0830 | Fed Governor Michael Barr | ||

| 21/11/2025 | 1345/0845 | Fed Vice Chair Philip Jefferson |