MNI EUROPEAN OPEN: Japan FinMin Says FX Intervention An Option

EXECUTIVE SUMMARY

- FED’S PAULSON EYES DEC. MEETING WITH CAUTION - MNI BRIEF

- JAPAN SAYS YEN INTERVENTION AN OPTION IN STEPPED UP WARNING - BBG

- JAPAN’S CABINET APPROVES LAVISH $135 BILLION STIMULUS AS MARKETS FRET OVER FISCAL POLICY - RTRS

- BOJ UEDA WARNS OF WEAK YEN IMPACT ON CPI- MNI BRIEF

- FORMER RBA BOARD MEMBER ON CASH RATE OUTLOOK - MNI INTERVIEW

- FORMER RBNZ ECONOMIST ON OCR OUTLOOK - MNI INTERVIEW

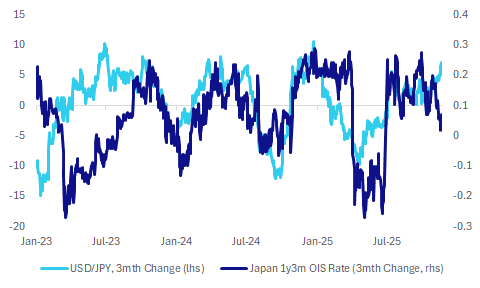

Fig 1: Market BoJ Pricing Outlook & USD/JPY Gains Diverging

Source: MNI - Market News/Bloomberg/Refinitiv.

UK

CONSUMERS (RTRS): "British consumer confidence edged down in November but remained in its narrow range of the past six months, a survey showed on Friday, in contrast to other data that has shown more weakness ahead of finance minister Rachel Reeves' budget next week."

TECH (BBG): "The UK plans to open a data center campus in south Wales, with developer Vantage Data Centers spending £10 billion ($13.1 billion) for facilities near a Microsoft Corp. site. "

EU

UKRAINE (BBG): "A 28-point peace plan floated by US and Russian envoys would force Ukraine to cede large chunks of territory taken by Russia, cap the size of its military and lift sanctions on Moscow over time, acceding to many of President Vladimir Putin’s wartime demands."

EU/AUSTRALIA (BBG): "The European Union is weighing direct investments in Australian mining companies to secure supplies of critical minerals, according to the bloc’s Commissioner for Trade and Economic Security Maros Sefcovic."

RUSSIA (BBG): "US sanctions that come into effect on Friday could leave nearly 48 million barrels of Russian crude stranded on the water, pushing dozens of tankers to scramble for alternative destinations in the latest overhaul of the global oil trade."

US

FED (MNI BRIEF): Philadelphia Federal Reserve Bank President Anna Paulson said Thursday she is taking a guarded approach to next month's decision on whether to keep cutting interest rates because borrowing costs are already close to neutral.

FED (MNI BRIEF): Federal Reserve Bank of Chicago President Austan Goolsbee said Thursday he is uncomfortable lowering interest rates too far before seeing evidence that tariff-related inflation is transitory and is not spilling over into services.

FED (MNI BRIEF): Federal Reserve Governor Lisa Cook on Thursday said the financial system remains resilient, supported by strong balance sheets among households and businesses and high capital levels across the banking system, but there are risks, including the increased likelihood of outsized asset price declines.

OTHER

JAPAN (MNI BRIEF): Bank of Japan Governor Kazuo Ueda on Friday warned that the weak yen could raise import costs and domestic prices, ultimately putting upward pressure on consumer prices.

JAPAN (RTRS): “Japanese Prime Minister Sanae Takaichi's cabinet approved a 21.3 trillion yen ($135.40 billion) economic stimulus package on Friday, marking the first major policy initiative under the new leader, who has pledged to pursue expansionary fiscal measures.”

JAPAN (BBG): “Japan issued its strongest warning yet to foreign exchange markets over sharp recent movements in the yen, with the nation’s finance minister specifically mentioning intervention as an option as she tries to push back against continued falls in the currency.”

JAPAN (MNI BRIEF): Bank of Japan Governor Kazuo Ueda on Friday said the bank is collecting data to assess the initial momentum for wage growth in fiscal 2026 and intends to use this information in policy decisions at or after the next policy-setting meeting.

JAPAN (MNI BRIEF): Japan’s annual core consumer inflation rose to 3.0% y/y in October from 2.9% in September, in line with expectations, driven by higher prices for household durable goods, although food prices excluding perishables eased, data released Friday by the Ministry of Internal Affairs and Communications showed.

JAPAN (MNI BRIEF): Japan’s exports rose 3.6% y/y in October, marking a second consecutive increase after September’s 4.2% gain, supported by higher shipments of semiconductors and power-generating machinery, as well as a modest pickup in automobile exports, Ministry of Finance data showed Friday.

ARGENTINA/US (WSJ): “A planned $20 billion bailout to Argentina from JPMorgan Chase, Bank of America and Citigroup has been shelved as bankers pivot instead to a smaller, short-term loan package to support the financially distressed government, people familiar with the matter said.”

AUSTRALIA (MNI INTERVIEW): A former RBA board member shares his cash rate outlook. On MNI Policy MainWire now, for more details please contact sales@marketnews.com.

NEW ZEALAND (MNI INTERVIEW): A former RBNZ economist shares his OCR outlook. On MNI Policy MainWire now, for more details please contact sales@marketnews.com.

CHINA

PMI (MNI INTERVIEW): The founder of RatingDog provides insight into China's private manufacturing purchasing managers index. On MNI Policy MainWire now, for more details please contact sales@marketnews.com.

FISCAL (YICAI): “China’s general public budget spending will need to grow 12.9% year-on-year in November and December, if authorities are to meet their annual budget targets, according to Yang Yewei, chief fixed-income analyst at Guosheng Securities.”

TRADE (YICAI): “China’s e-commerce exports to Europe are expanding rapidly as sellers redirect their focus amid U.S. geopolitical tensions, according to Jiang Qing, head of an international freight-forwarding company who spoke with Yicai.”

MNI: PBOC Net Injects CNY162.2 Bln via OMO Friday

MNI (BEIJING) - The People's Bank of China (PBOC) conducted CNY375 billion via 7-day reverse repos, with the rate unchanged at 1.40%. The operation led to a net injection of CNY162.2 billion after offsetting maturities of CNY212.8 billion today, according to Wind Information.

- The seven-day weighted average interbank repo rate for depository institutions (DR007) fell to 1.4094% at 09:58 am local time from the close of 1.4857% on Thursday.

- The CFETS-NEX money-market sentiment index, measuring interbank money-market liquidity, closed at 50 on Thursday, compared with the close of 49 on Wednesday. A higher reading points to tighter liquidity condition, with 50 representing an equilibrium.

MNI: PBOC Sets Yuan Parity Lower At 7.0875 Fri; +1.91% Y/Y

MNI (BEIJING) - The People's Bank of China (PBOC) set the dollar-yuan central parity rate lower at 7.0875 on Friday, compared with 7.0905 set on Thursday. The fixing was estimated at 7.1190 by Bloomberg survey today.

MARKET DATA

NEW ZEALAND OCT EXPORTS NZD 6.50BN; PRIOR 5.78BN

NEW ZEALAND OCT IMPORTS NZD 8.04BN; PRIOR 7.17BN

NEW ZEALAND OCT TRADE BALANCE NZD -1542MN; PRIOR -1384MN

AUSTRALIA NOV P S&P GLOBAL AUSTRALIA PMI MANUFACTURING 51.6; PRIOR 49.7

AUSTRALIA NOV P S&P GLOBAL AUSTRALIA PMI SERVICES 52.7; PRIOR 52.5

AUSTRALIA NOV P S&P GLOBAL AUSTRALIA PMI COMPOSITE 52.6; PRIOR 52.1

JAPAN OCT NATL CPI Y/Y 3.0%; MEDIAN 3.0%; PRIOR 2.9%

JAPAN OCT NATL CPI EX FRESH FOOD Y/Y 3.0%; MEDIAN 3.0%; PRIOR 2.9%

JAPAN OCT NATL CPI EX FRESH FOOD, ENERGY Y/Y 3.1%; MEDIAN 3.1%; PRIOR 3.0%

JAPAN OCT TRADE BALANCE ADJUSTED -¥4.2BN; MEDIAN -¥128.9bn; PRIOR -¥302.4BN

JAPAN OCT EXPORTS Y/Y 3.6%; MEDIAN 1.1%; PRIOR 4.2%

JAPAN OCT IMPORTS Y/Y 0.7%; MEDIAN -1.0%; PRIOR 3.0%

JAPAN NOV P S&P GLOBAL PMI MANUFACTURING 48.8; PRIOR 48.2

JAPAN NOV P S&P GLOBAL PMI SERVICES 53.1; PRIOR 53.1

JAPAN NOV P S&P GLOBAL PMI COMPOSITE 52.0; PRIOR 51.5

SOUTH KOREA OCT PPI Y/Y 1.5%; PRIOR 1.2%

SOUTH KOREA NOV EXPORTS 20 DAYS Y/Y 8.2% ; PRIOR -7.8%

SOUTH KOREA NOV IMPORTS 20 DAYS Y/Y 3.7% ; PRIOR -2.3%

MARKETS

US TSYS: Treasury Yields Give Back Some of Overnight Gains

US treasury futures are all up marginally today whilst heading for a weekly gain. The US 10-Yr is at 113-00 today looking at reasonable gains for the week having closed off last Friday at 112-17. TYZ5 is back above all major moving averages, having dipped below for 10 trading days as investors views on potential rate cuts in December whipsaw around.

Cash is weaker today with yields up to +1bps higher in the front end, giving back overnight gains.

- The 2-Yr is up +1.3bps to 3.548% - lower by -6bps for the week.

- The 5-Yr is up +1.0bps at 3.658% - lower by -8bps for the week

- The 10-Yr is up +0.8bps at 4.094% - lower by -5bps for the week.

- The 30-Yr is up +0.1bps at 4.726% - lower by -2bps for the week.

Whilst the flow of government provided data continues tonight with housing starts, building permits and new home sales the reality is that markets are deeming these releases as stale. The November preliminary PMIs however should receive more focus alongside the University of Michigan inflation and sentiment indicators. There are no major auctions scheduled at this stage with bills and 2-Yr notes the focus.

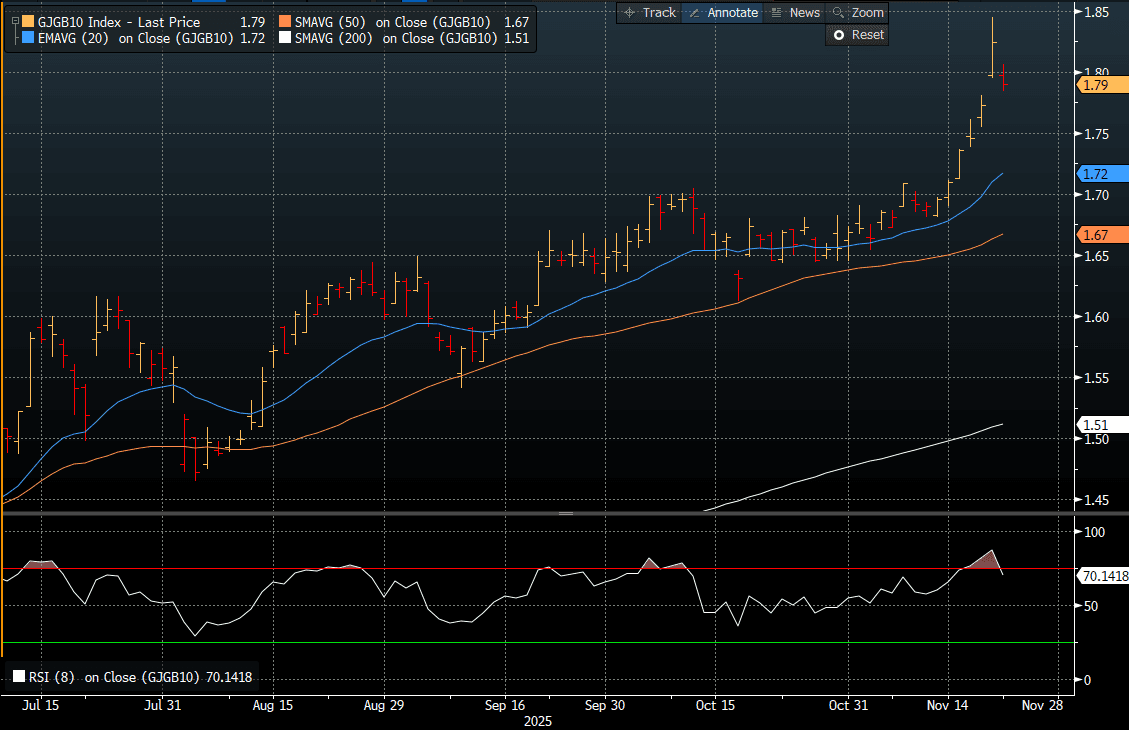

JGBS: Yields Extend Retreat From Yesterday’s Peaks

JGB futures are stronger, +25 compared to settlement levels, albeit off session highs. Nevertheless, the market has managed to unwind yesterday's explosive move to cycle lows.

- Japan's Oct CPI was in line with market forecasts across the three inflation metrics, and a slight tick up from the Sep outcome. Headline printed at 3.0%y/y, as did the core ex fresh food measure (both measures were 2.9% in Sep). The ex fresh food, energy measure edged up to 3.1%y/y from 3.0% prior.

- “Japanese Prime Minister Sanae Takaichi’s cabinet approved a stimulus plan valued at ¥21.3 trillion to address voter frustrations. The plan includes ¥11.7 trillion for price relief, with measures such as subsidies for gas and electricity bills and cash handouts per child. The price relief measures are expected to push down the overall inflation gauge by an average 0.7 percentage points from February to April.” - BBG

- Cash JGBs are flat to 6bps richer across benchmarks, with the curve flatter. The benchmark 10-year yield is 3.4bps lower at 1.790% versus the cycle high of 1.84%, set yesterday. (see chart)

- Swap rates are flat to 4bps lower.

- On Monday, the local market will be closed for a holiday.

Source: Bloomberg Finance LP

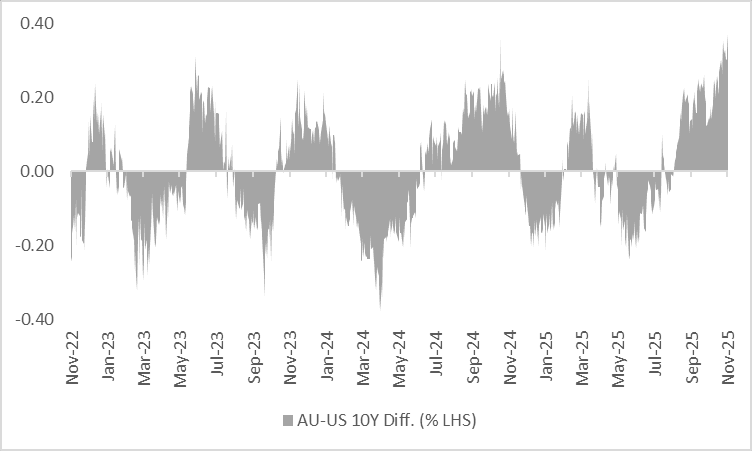

AUSSIE BONDS: Modest Rally But AU-US 10Y Diff At Highest Level Since Late 2022

ACGBs (YM +2.0 & XM +1.0) are marginally stronger but well off session highs.

- Cash US tsys are flat to 1bp cheaper, with a flattening bias, in today's Asia-Pac session after yesterday's risk-off induced rally.

- Cash ACGBs are 1-2bps richer with the AU-US 10-year yield differential at +37bps, the highest since late 2022. (see chart)

- However, a simple regression of the 10-year yield differential against the AU-US 1-year forward 3-month swap rate (1Y3M) differential over the past two years suggests the current spread is +7bps to fair value.

- The latest ACGB May-32 supply achieved a weighted average yield that printed 0.44bp through prevailing mids (per Yieldbroker). Moreover, the cover ratio increased, rising to 3.5171x from 3.3850x.

- The bills strip is little changed.

- RBA-dated OIS pricing is showing a 25bp rate cut in December at a 2% probability, with a cumulative 11bps of easing priced by mid-2026.

- The local calendar will be empty until Wednesday’s October CPI data.

- Next week, the AOFM plans to sell A$400mn of the 4.25% 21 June 2034 bond on Tuesday, A$700mn of the 2.75% 21 November 2029 bond on Wednesday and A$900mn of the 3.75% 21 April 2037 bond on Friday.

Bloomberg Finance LP

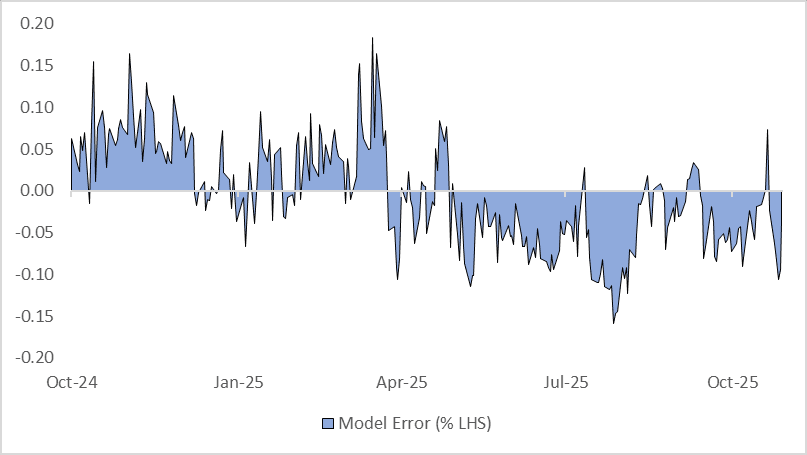

NZGBS: NZ-US 10Y Diff Sharply Wider, RBNZ Next Wednesday

NZGBs closed showing a twist-steepener, with yields 1bp lower to 3bps higher across benchmarks.

- Cash US tsys are 1-2bps cheaper, with a flattening bias, in today's Asia-Pac session after yesterday's risk-off induced rally.

- The NZ-US 10-year yield differential closed 7bps wider at +7bp. Yesterday, a simple regression of the 1Y3M forward swap spread against the 10-year yield differential over the past three years suggested the differential was about 10bps below its estimated fair value. Today, it closed 3bps below fair value. (see chart)

- Swap rates closed flat to 3bps higher, with the 2s10s curve steeper.

- Next week, the local calendar will be empty until the RBNZ Policy Decision on Wednesday.

- RBNZ dated OIS pricing closed slightly softer across meetings. 27bps of easing is priced for November, with a cumulative 35bps by February 2026.

- Our policy team also highlights a former RBNZ economists' viewpoint on the OCR outlook; see this link for more details.

Bloomberg Finance LP

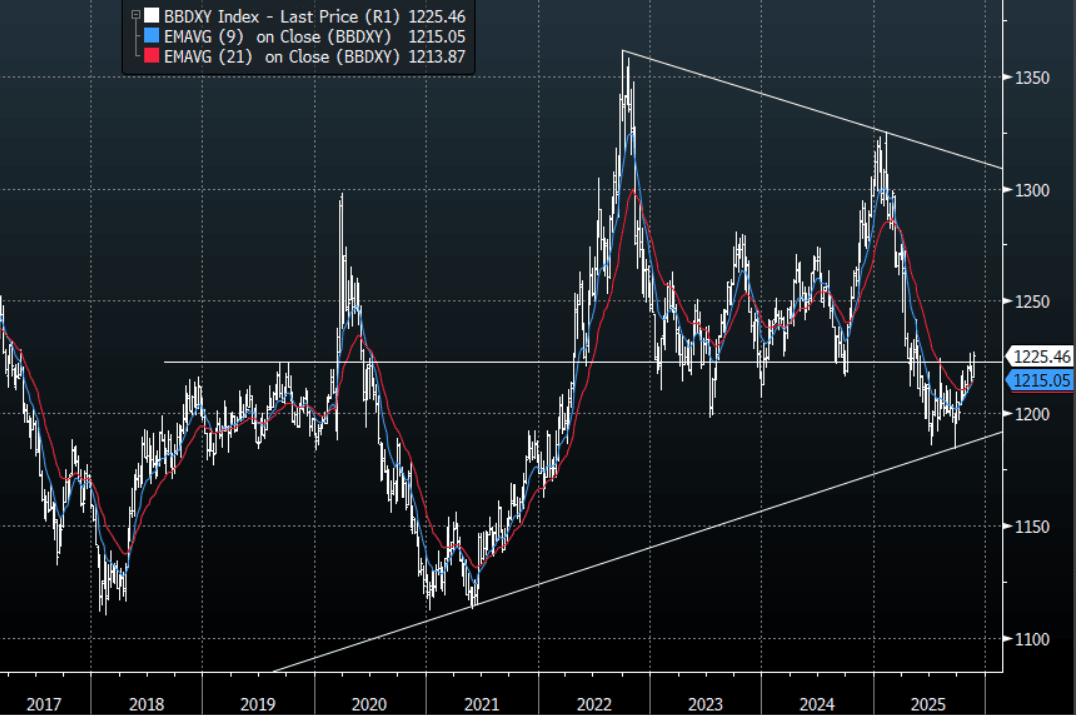

FOREX: USD - BBDXY Is Consolidating Around 1225

The BBDXY has had a range today of 1225.56 - 1226.95 in the Asia-Pac session; it is currently trading around 1225, -0.10%. The USD has drifted lower in our session albeit still close to its recent highs. While the price remains above 1218-1220 I would be skewed toward expressing a long, looking for a retest of the 1230-1240 area at some point. On the day I suspect dips toward 1222-1224 could continue to be supported as the market tries to build a base from which to extend higher.

- EUR/USD - Asian range 1.1524 - 1.1539, Asia is currently trading 1.1540. The pair consolidated just above the 1.1500 area yesterday. On the day I still prefer to be skewed short while below the 1.1545-65 area, as the market turns its focus toward the 1.1400 support.

- GBP/USD - Asian range 1.3053 - 1.3087, Asia is currently dealing around 1.3090. I continue to favor fading rallies, as GBP looks to have put in a medium term top. I suspect rallies will continue to be faded on the day while we stay below the 1.3100-1.3150 area as the market looks to challenge the 1.3000 support.

- Cross asset : SPX +0.30%, Gold $4055, US 10-Year 4.092%, BBDXY 1226, Crude Oil $59.15

- Data/Events : EZ HCOB Eurozone PMI’s/Negotiated Wages, Germany HCOB Germany PMI’s, France Business Confidence/Manufacturing Confidence/HCOB France PMI’s

Fig 1: BBDXY Spot Weekly Chart

Source: MNI - Market News/Bloomberg Finance L.P

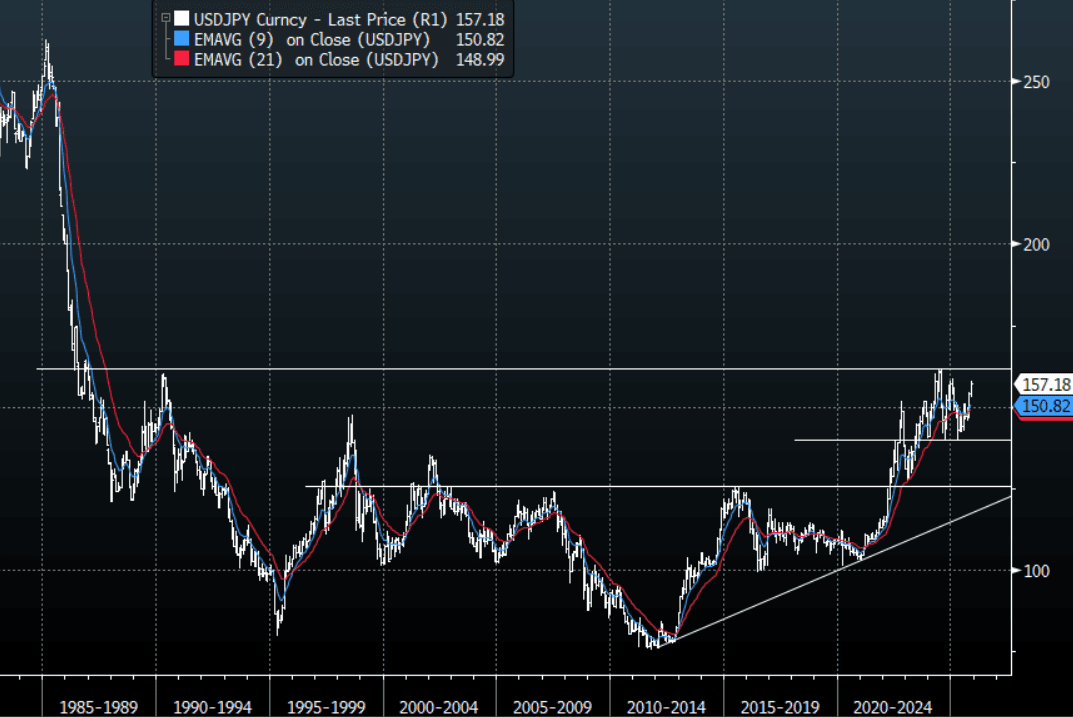

JPY: USD/JPY - Consolidates Above 157.00

The USD/JPY range today has been 157.09 - 157.59 in the Asia-Pac session, it is currently trading around 157.10, -0.20%. The pair continues to consolidate its recent gains above 157.00. The horse looks like it has bolted now though and Japanese officials would have to do something extraordinary to change the narrative. The path of least resistance is now a higher USD/JPY and I suspect any dips back toward the 154-155 area would be used as buying opportunities. I feel they will have to show some sign of fighting this toward or above 160, but given the current inputs this could potentially go a lot higher than that. It will be interesting when we get the CFTC data back as I suspect real money would only just be starting to turn back to a short Yen position.

- MNI AU - Market BoJ Pricing Outlook & USD/JPY Gains Diverging: The weaker yen trend remains a key focus point for Japan policy makers. Earlier the FinMin stated that FX intervention was an option, a clear step up in rhetoric around yen weakness. BoJ Governor Ueda was also before parliament and warned that the weak yen could raise import costs and domestic prices, ultimately putting upward pressure on consumer prices. All else being equal if USD/JPY continues to track higher risks are likely to build around the markets pricing in higher rates.

- "JAPAN FINANCE MINISTER KATAYAMA: OUR PLANNED STIMULUS PACKAGE IS NOT NECESSARILY EXPANSIONARY, WE ARE MINDFUL OF NEED FOR WISE SPENDING - [RTRS]"

- Options : Close significant option expiries for NY cut, based on DTCC data: 155.00($933m),156.00($880m), 157.00($495m) . Upcoming Close Strikes : 153.00($1.17b Nov 26), 154.00{$1.94b Nov 26), 155.00($1.46b Nov 26) - BBG.

- The USD/JPY Average True Range(ATR) for the last 10 Trading days: 113 Points

Fig 1 : USD/JPY Spot Weekly Chart

Source: MNI - Market News/Bloomberg Finance L.P

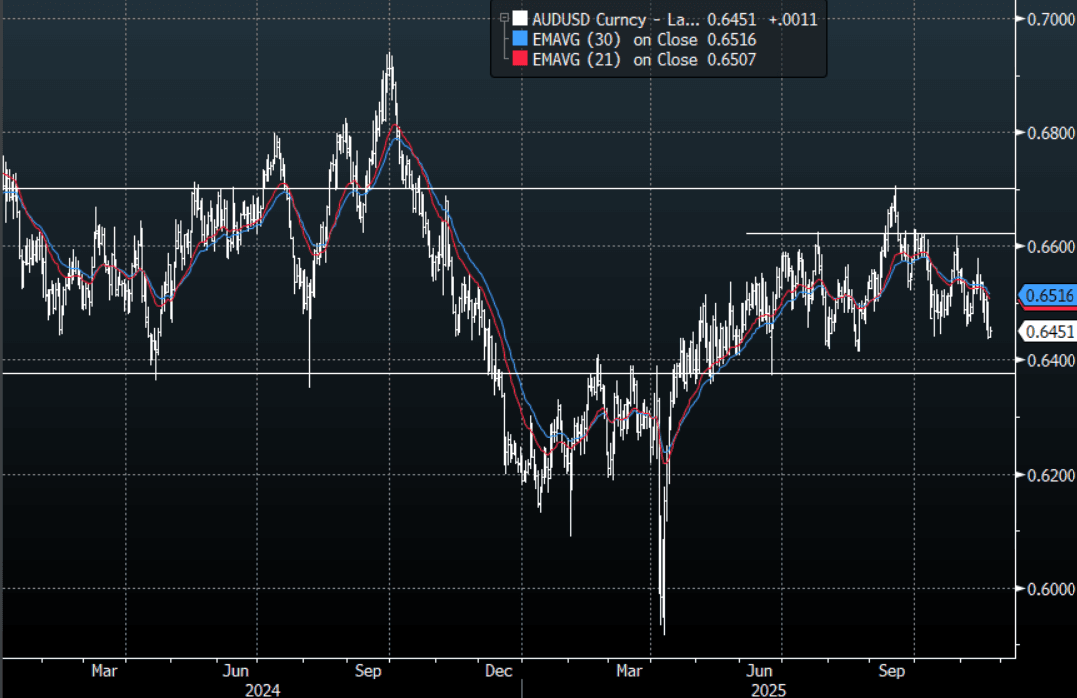

AUD/USD - Support Around 0.6440-0.6450 Holds for Now

The AUD/USD has had a range today of 0.6438 - 0.6458 in the Asia- Pac session, it is currently trading around 0.6450, +0.15%. The AUD/USD has a little higher in a quiet Asian session as the market tries to digest the implications of the overnight price action in risk. This does not have a great smell and we are now sitting on some pivotal levels in global risk that if they give way will potentially signal a deeper pullback. The AUD/USD traded heavy overnight in sympathy to this backdrop and should risk actually break lower it would become vulnerable. The pair is probing its first support right here around the 0.6440-0.6450 area which has been pretty solid the last couple of months, through here and the focus will then turn to the pivotal 0.6350 support. On the day while risk remains under pressure and the AUD is capped below 0.6500-0.6525 I suspect rallies will be faded and the market will be looking to see if it can break this 0.6440-50 support properly to build for a move lower.

- MNI AU - Nov PMIs Up, Particularly Manufacturing, Services Jobs Moderates: Australian Nov preliminary PMIs saw improvement across the board, most notably for manufacturing. The manufacturing index rose to 51.6 from 49.7. We are still short of earlier 2025 highs around 53.0, but the turn around from Oct levels under 50.0 is notable. On the services side, we edged up to 52.7, from 52.5 prior. Again we remain off recent cycle highs, but it broadly suggests reasonably economic momentum for Q4. The composite index was at 52.6 from 52.1 in Oct. The data is second tier, but reinforces the RBA's on hold backdrop in the near term.

- Options : Closest significant option expiries for NY cut, based on DTCC data: 0.6500(AUD2.28b). Upcoming Close Strikes : 0.6450(AUD991m Nov 26), 0.6500(AUD1.07b Nov 26), 0.6535(AUD1.69b Nov 26) - BBG

- The AUD/USD Average True Range for the last 10 Trading days: 47 Points

Fig 1: AUD/USD spot Daily Chart

Source: MNI - Market News/Bloomberg Finance L.P

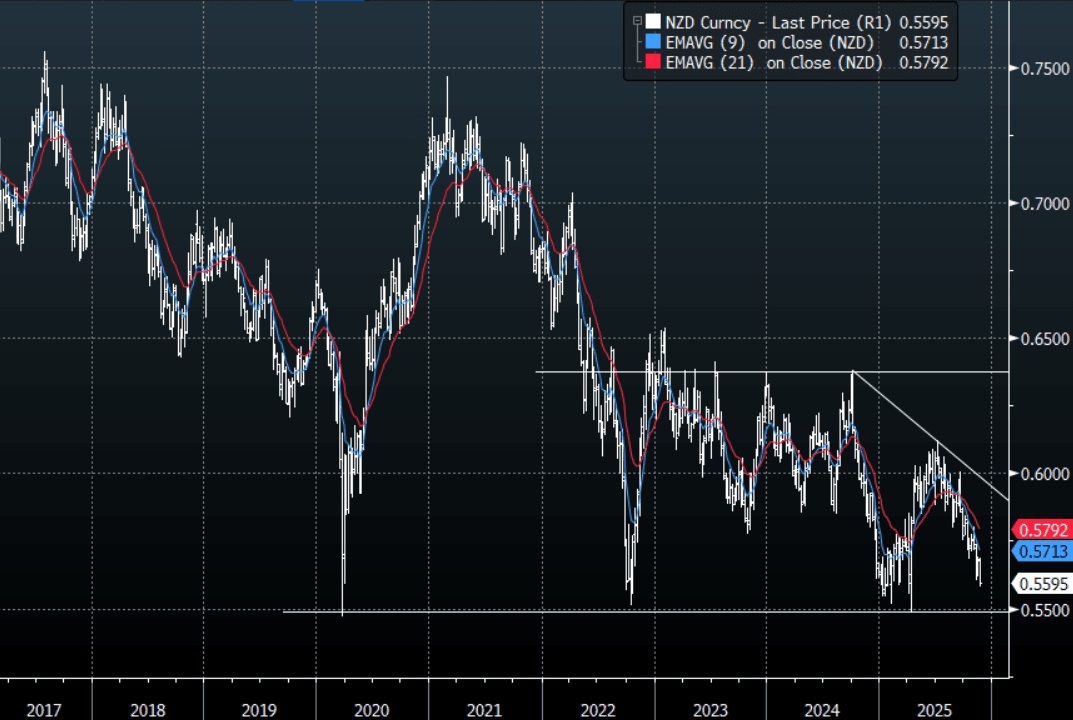

NZD/USD - Drifts Back Toward 0.5600

The NZD/USD had a range today of 0.5581 - 0.5598 in the Asia-Pac session, going into the London open trading around 0.5595, +0.15%. The NZD/USD drifted a little higher as the market tries to digest the implications of the overnight price action in global risk. This does not have a great smell and we are now sitting on some pivotal levels in global risk that if they give way will potentially signal a deeper pullback. The NZD continues to trade heavy with this backdrop having topped out back toward 0.5640 overnight. The next target is the pivotal 0.5500 area which has been very strong support the last few years. On the day I suspect while the NZD remains under 0.5630-50 the rallies will be faded as the market turns its focus toward that support.

- MNI AU - Trade Deficit Widens In Oct, Not Showing Typical H2 Improvement Yet: New Zealand Oct trade data saw the trade deficit widen slightly to -NZ$1542mn from a revised -NZ$1384mn in Sep. Both exports and imports rose in the month, with imports up by slightly more to drive the wider deficit. This is a NZD negative at the margins, and comes after the further decline in whole milk prices earlier this week. Note the 12 mth YTD deficit was -NZ$2281mn, showing a further trend improvement.

- MNI Interview: Our policy team also highlights a former RBNZ economists' viewpoint on the OCR outlook, see this link for more details. https://www.mnimarkets.com/articles/mni-interview-rbnz-done-easing-after-next-cut-fmr-economist-1763697187886

- Options : Closest significant option expiries for NY cut, based on DTCC data: 0.5480(NZD644m). Upcoming Close Strikes : 0.5670(NZD788m Nov 26), 0.5720(NZD646m Nov 25) - BBG

- The NZD/USD Average True Range for the last 10 Trading days: 42 Points

Fig 1: NZD/USD Spot Weekly Chart

Source: MNI - Market News/Bloomberg Finance L.P

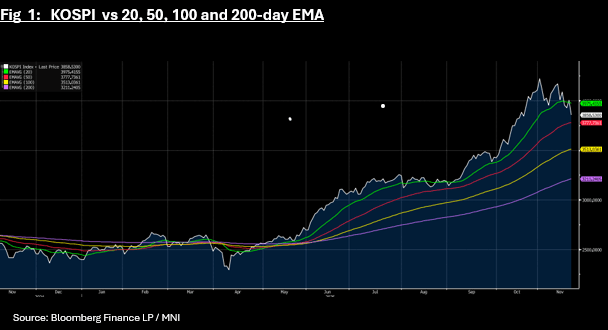

Asia Stocks Looking at Worst Week Since April

Major bourses were down today with the tech heavy NIKKEI and KOSPI leading the falls. The falls have seen the weakest week for major bourses since the volatility of April. With clarity on a rate cut not forthcoming in the data overnight, Asia's investors appear to be resetting their expectations for rates, weighing heavy on equities, with yields ignoring overnight leads to push higher in the Asia trading day. Despite the better than expected Nvidia results, some forecasters are now saying that the tech led rally is on shaky grounds and fundamentals are likely to reassert in the near term. With several key bourses recently at highs and P/Es at top end of estimates, a modest change in sentiment has the potential for a sizeable change in momentum.

- The NIKKEI fell -2.4% today and is down -3.5% for the week, whilst the KOSPI is down -3.7% today and -3.9% for the week. The losses for the KOSPI sees it back below the 20-day EMA for the first time since the beginning of September and at 3,854, has the 100-day EMA of 3,777 below it.

- China's major bourses have had a very week Friday with the Hang Seng down -2% and -4.7% for the week whilst the CSI 300 is down -1.9% and -3.2% for the week.

- SE Asia's bourses are mixed with the Jakarta Composite holding onto a weekly gain of +0.35% despite falling -0.25% today whilst Malaysia is down for the week by -0.50% following falls of -0.15% today and the SE Thai down -1.15% today to slip to a loss of -0.6%

- India's NIFTY 50 is weak at the outset of the trading day in India, down -0.45% whilst retaining gains of +0.5% for the week as hopes hang on the announcement of a trade deal with the US soon.

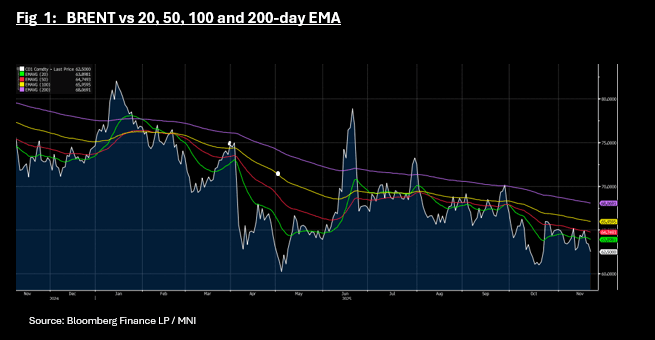

Oil Set for Weekly Fall on Ukraine Peace Plan

- Oil is set for moderate losses for the week as news of a Ukraine / Russia peace plan drives prices lower Friday.

- WTI is down -1.8% today at US$58.06 bbl and currently down -3.3% for the week. WTI has delivered weekly gains on twice out of the last eight trading weeks, primarily on supply concerns.

- The IEA forecasts increased estimated surpluses in 2026 of up to 4 million barrels a day, with global growth prospects modest at best. Were a peace deal to be reached and Russian oil allowed to flow, this would add further pressure to oil prices.

- Brent is down -1.40% today at US$62.49 bbl and down -2.9% for the week. The losses this week sees Brent back below all major moving averages, having dipped below the 20-day EMA of $63.89.

- In further potential increases to supply, President Trump is looking to expand drilling access for US firms to increase US output with over 30 possible new leases proposed. Leases are being explored in areas in California, Florida and Alaska and could open up more than 1 bn acres of coastal zones to drilling.

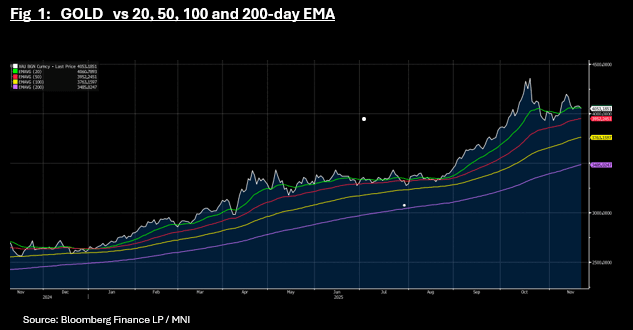

- As the probability of a rate cut by the FED continues to diminish, gold's fortunes have turned down and on course for a weekly fall.

- Gold is losing ground by -0.59% today to be at US$4,053.28 and lower by -0.77% for the week.

- Since it's high on October 20, gold is now over 7% lower with key drivers being diminished rate cut expectations and the calming of the trade war.

- The falls today sees bullion slip below the 20-day EMA of US$4,060.73. Below is the 50-day EMA of $3,952.24.

UP TODAY (TIMES GMT/LOCAL)

| Date | GMT/Local | Impact | Country | Event |

| 21/11/2025 | 0700/0700 | *** | Public Sector Finances | |

| 21/11/2025 | 0700/0700 | *** | Retail Sales | |

| 21/11/2025 | 0745/0845 | ** | Manufacturing Sentiment | |

| 21/11/2025 | 0800/0900 | ECB de Guindos Remarks/Q&A at Foro Gran Via | ||

| 21/11/2025 | 0815/0915 | ** | S&P Global Services PMI (p) | |

| 21/11/2025 | 0815/0915 | ** | S&P Global Manufacturing PMI (p) | |

| 21/11/2025 | 0830/0930 | ** | S&P Global Services PMI (p) | |

| 21/11/2025 | 0830/0930 | ** | S&P Global Manufacturing PMI (p) | |

| 21/11/2025 | 0830/0930 | ECB Lagarde Speech at European Banking Congress | ||

| 21/11/2025 | 0900/1000 | ** | S&P Global Services PMI (p) | |

| 21/11/2025 | 0900/1000 | ** | S&P Global Manufacturing PMI (p) | |

| 21/11/2025 | 0900/1000 | ** | S&P Global Composite PMI (p) | |

| 21/11/2025 | 0930/0930 | *** | S&P Global Manufacturing PMI flash | |

| 21/11/2025 | 0930/0930 | *** | S&P Global Services PMI flash | |

| 21/11/2025 | 0930/0930 | *** | S&P Global Composite PMI flash | |

| 21/11/2025 | 1000/1100 | Negotiated Wage Growth | ||

| 21/11/2025 | 1130/1230 | ECB de Guindos Remarks/Q&A at Deusto Business School | ||

| 21/11/2025 | 1230/0730 | New York Fed's John Williams | ||

| 21/11/2025 | 1330/0830 | ** | Retail Trade | |

| 21/11/2025 | 1330/0830 | Fed Governor Michael Barr | ||

| 21/11/2025 | 1345/0845 | Fed Vice Chair Philip Jefferson | ||

| 21/11/2025 | 1400/0900 | Dallas Fed's Lorie Logan | ||

| 21/11/2025 | 1400/0900 | Boston Fed's Susan Collins | ||

| 21/11/2025 | 1445/0945 | *** | S&P Global Manufacturing Index (Flash) | |

| 21/11/2025 | 1445/0945 | *** | S&P Global Services Index (flash) | |

| 21/11/2025 | 1500/1000 | *** | U. Mich. Survey of Consumers | |

| 21/11/2025 | 1500/1000 | ** | University of Michigan Surveys of Consumers Inflation Expectation | |

| 21/11/2025 | 1500/1000 | ** | Wholesale Trade | |

| 21/11/2025 | 1500/1000 | ** | Wholesale Trade | |

| 21/11/2025 | 1540/1540 | BOE Pill in Panel at Swiss National Bank | ||

| 21/11/2025 | 1800/1300 | ** | Baker Hughes Rig Count Overview - Weekly | |

| 21/11/2025 | 1800/1300 | ** | Baker Hughes Rig Count Overview - Weekly | |

| 21/11/2025 | 1800/1300 | ** | Baker Hughes Rig Count Overview - Weekly | |

| 22/11/2025 | 0800/0900 | ECB Lagarde in Roundtable at Austrian National Bank | ||

| 22/11/2025 | 1100/1200 | ECB Lagarde Keynote on Fiscal and MonPol |