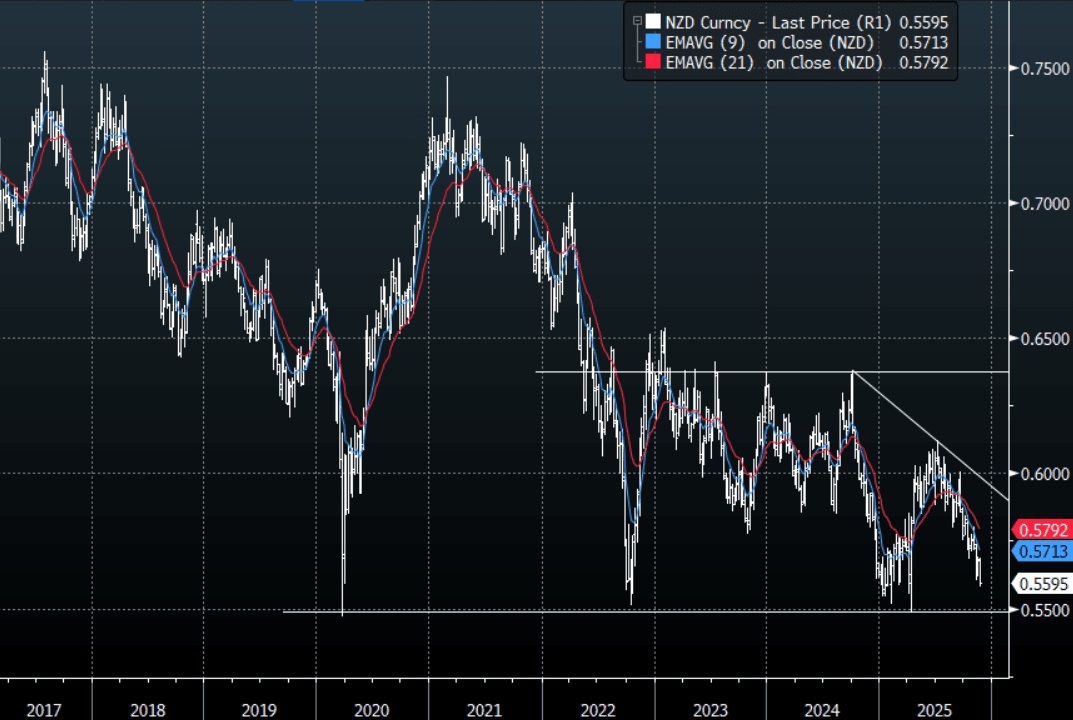

NZD: NZD/USD - Drifts Back Toward 0.5600

The NZD/USD had a range today of 0.5581 - 0.5598 in the Asia-Pac session, going into the London open trading around 0.5595, +0.15%. The NZD/USD drifted a little higher as the market tries to digest the implications of the overnight price action in global risk. This does not have a great smell and we are now sitting on some pivotal levels in global risk that if they give way will potentially signal a deeper pullback. The NZD continues to trade heavy with this backdrop having topped out back toward 0.5640 overnight. The next target is the pivotal 0.5500 area which has been very strong support the last few years. On the day I suspect while the NZD remains under 0.5630-50 the rallies will be faded as the market turns its focus toward that support.

- MNI AU - Trade Deficit Widens In Oct, Not Showing Typical H2 Improvement Yet: New Zealand Oct trade data saw the trade deficit widen slightly to -NZ$1542mn from a revised -NZ$1384mn in Sep. Both exports and imports rose in the month, with imports up by slightly more to drive the wider deficit. This is a NZD negative at the margins, and comes after the further decline in whole milk prices earlier this week. Note the 12 mth YTD deficit was -NZ$2281mn, showing a further trend improvement.

- MNI Interview: Our policy team also highlights a former RBNZ economists' viewpoint on the OCR outlook, see this link for more details. https://www.mnimarkets.com/articles/mni-interview-rbnz-done-easing-after-next-cut-fmr-economist-1763697187886

- Options : Closest significant option expiries for NY cut, based on DTCC data: 0.5480(NZD644m). Upcoming Close Strikes : 0.5670(NZD788m Nov 26), 0.5720(NZD646m Nov 25) - BBG

- The NZD/USD Average True Range for the last 10 Trading days: 42 Points

Fig 1: NZD/USD Spot Weekly Chart

Source: MNI - Market News/Bloomberg Finance L.P

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

US TSYS: Modest Declines in Yields Again Today

Bond futures finished -01 lower today for TYZ5 on low volumes, looking for a catalyst for the next move .

- The US 2-Yr did very little all morning before rising modestly to 3.465 in the afternoon trading session.

- The US 5-Yr ground was flat at 3.56%

- The 10-Yr has consolidated below 4.00%, rallying again modestly by -0.5bps to reach 3.96% in line with October 24 yield levels.

- The 30-Yr continues to outperform rallying -0.5bps overnight to reach 4.53%. Likely next inflection point could be the April lows of 4.40%.

- Yield moves are appearing disjointed relative to current interest rate pricing as the government shutdown continues as bond traders agonize over the potential impact on the economy. New ranges are being defined and as markets await the release of the September CPI, markets appeared skewed towards lower yields for now.

- There is limited Tier 1 data releases for markets to follow tonight, only MBG mortgage applications. Equity weakness in Asia will be watched for any follow through particularly as many bourses reach new highs.

AUSSIE BONDS: Subdued Session, Market Scales Back Chances Of A Nov Cut

ACGBs (YM -0.5 & XM +1.0) are slightly mixed.

- Cash ACGBs are little changed with the AU-US 10-year yield differential at +15bps.

- The bills strip is -1 to -2 across contracts.

- A 25bp rate cut in November is assigned a 64% probability, with a cumulative 23bps of easing priced by year-end.

- Compared with previous instances in this easing cycle, the market appears less confident than usual about a November 4 cut.

- This caution aligns with the RBA’s pattern over the past year of easing less than what six-month forward expectations had implied. Those expectations currently sit around 3.20%, compared with the cash rate of 3.60%. (see chart)

- The local data calendar remains fairly quiet throughout the week.

- Today’s auction of the Jun-35 showed solid pricing for ACGBs, with the weighted average yield coming in 0.43bps below prevailing mid-yield. However, the cover ratio nudged lower to 2.9056x from 3.2958x at the previous auction.

- The AOFM plans to sell A$800mn of the 2.75% 21 November 2029 bond on Friday.

- QTC has priced a A$2 billion increase to its 4.50% August 22, 2035 A$ fixed rate benchmark bond, according to BofA Securities. - BBG

Figure 1: RBA Cash Rate Vs. OIS 6M1M (6M Ago)

Source: Bloomberg Finance LP / MNI

ASIA STOCKS: Stocks Pull Back On AI-Related Profit Taking

Bellwether tech stocks declined over 1% today in Asia as a lackluster forecast from Texas Instruments saw it's stock fall, and others follow. After many of the key tech stocks in Asia hitting new highs recently, it is unsurprising to see falls as profit takers step in. Demand remains robust and export data from countries like Korea and Taiwan show that export growth remains strong, suggesting that whilst the outlook remains strong, a re-rating in expectations can occur.

- Major Asian bourses have hit new highs over the last week and have followed each other lower today, with the NIKKEI leading the falls. The NIKKEI is down -0.60% after hitting new highs yesterday as investors seek to understand the outcome of political negotiations to form a new government.

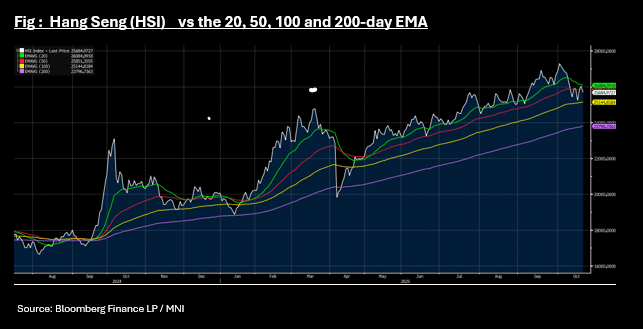

- China's major bourses are down also with the Hang Seng falling -1.3% and back below the 50-day EMA it trended above only yesterday. Other onshore bourses are down with the CSI 300 has pulled back -0.705 and near to the 20-day EMA again, whilst Shanghai and Shenzhen are down -0.45% and -0.55% respectively.

- The KOSPI is an outlier today, reaching yet another new high of 3,835 to be up +0.29%.

- Ahead of the BI decision later, the JCI is down -0.6% as markets await what appears to be an imminent rate cut.

- Headlines have crossed from Indian news source Mint, that a US-India trade deal will soon see tariff rates fall sharply. Some key quotes are outlined below, but notably the article states tariff rates may come down form 50% to 15-16%. Market optimism around a trade deal has been growing, given recent Trump remarks that India would curb Russian oil imports. The NIFTY 50 has reached a new high of 25,866, up +0.10% in morning trade.