BONDS: NZGBS: NZ-US 10Y Diff Sharply Wider, RBNZ Next Wednesday

NZGBs closed showing a twist-steepener, with yields 1bp lower to 3bps higher across benchmarks.

- Cash US tsys are 1-2bps cheaper, with a flattening bias, in today's Asia-Pac session after yesterday's risk-off induced rally.

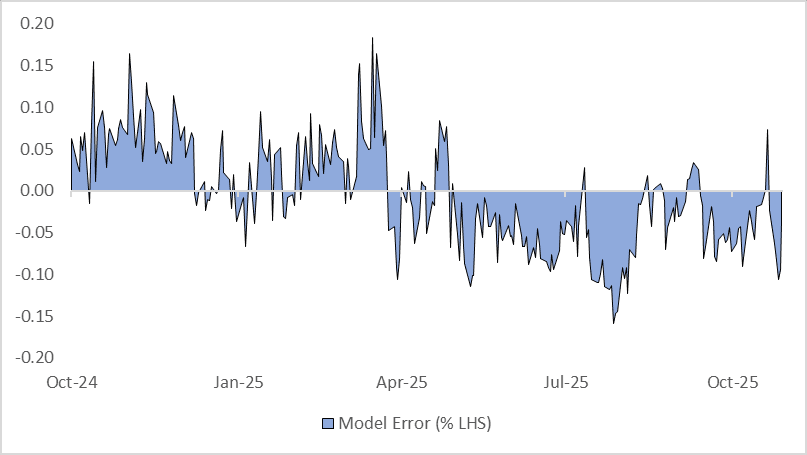

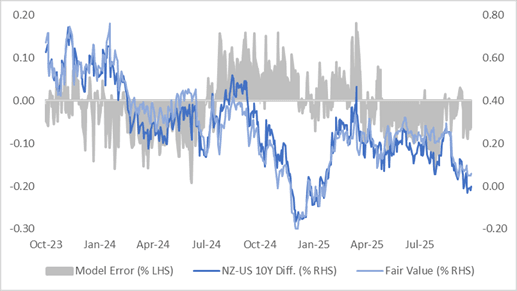

- The NZ-US 10-year yield differential closed 7bps wider at +7bp. Yesterday, a simple regression of the 1Y3M forward swap spread against the 10-year yield differential over the past three years suggested the differential was about 10bps below its estimated fair value. Today, it closed 3bps below fair value. (see chart)

- Swap rates closed flat to 3bps higher, with the 2s10s curve steeper.

- Next week, the local calendar will be empty until the RBNZ Policy Decision on Wednesday.

- RBNZ dated OIS pricing closed slightly softer across meetings. 27bps of easing is priced for November, with a cumulative 35bps by February 2026.

- Our policy team also highlights a former RBNZ economists' viewpoint on the OCR outlook; see this link for more details.

Bloomberg Finance LP

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

ASIA STOCKS: Stocks Pull Back On AI-Related Profit Taking

Bellwether tech stocks declined over 1% today in Asia as a lackluster forecast from Texas Instruments saw it's stock fall, and others follow. After many of the key tech stocks in Asia hitting new highs recently, it is unsurprising to see falls as profit takers step in. Demand remains robust and export data from countries like Korea and Taiwan show that export growth remains strong, suggesting that whilst the outlook remains strong, a re-rating in expectations can occur.

- Major Asian bourses have hit new highs over the last week and have followed each other lower today, with the NIKKEI leading the falls. The NIKKEI is down -0.60% after hitting new highs yesterday as investors seek to understand the outcome of political negotiations to form a new government.

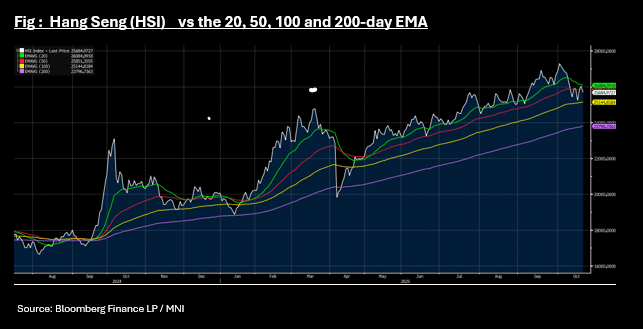

- China's major bourses are down also with the Hang Seng falling -1.3% and back below the 50-day EMA it trended above only yesterday. Other onshore bourses are down with the CSI 300 has pulled back -0.705 and near to the 20-day EMA again, whilst Shanghai and Shenzhen are down -0.45% and -0.55% respectively.

- The KOSPI is an outlier today, reaching yet another new high of 3,835 to be up +0.29%.

- Ahead of the BI decision later, the JCI is down -0.6% as markets await what appears to be an imminent rate cut.

- Headlines have crossed from Indian news source Mint, that a US-India trade deal will soon see tariff rates fall sharply. Some key quotes are outlined below, but notably the article states tariff rates may come down form 50% to 15-16%. Market optimism around a trade deal has been growing, given recent Trump remarks that India would curb Russian oil imports. The NIFTY 50 has reached a new high of 25,866, up +0.10% in morning trade.

GOLD: Gold & Silver’s Early Wednesday Decline Short-Lived, USD Slightly Softer

Profit taking in gold and silver begun on Tuesday continued early in Wednesday’s APAC trading but the declines have been more than unwound and both are now slightly higher on the day. The moderate decline in the US dollar, unchanged US yields and weaker equities appear to have driven the recovery. Traders have been long, with the extent unclear due to the lack of CFTC positioning data because of the US government shutdown, and Tuesday’s sell off appears to have been driven by repositioning as both metals are in overbought territory.

- Gold reached a low of $4004.26, below the 20-day EMA at $4021.6, but has recovered to be 0.2% higher at $4131.2, just below support at $4140.8 and off today’s peak at $4143.28. It remains overbought.

- Silver fell to $47.550 earlier but is now up 0.5% to $48.94, still below the 20-day EMA at $49.089. The 50-day EMA at $44.996 is a level to watch.

- Equities are generally weaker with the Hang Seng down 1.3%, Nikkei -0.5% but S&P e-mini close to flat. Oil prices are stronger with WTI +1.7% to $58.20/bbl. Copper is down 0.1%.

- Later UK September CPI data print and ECB President Lagarde and Board members Buch and de Guindos speak.

BONDS: Closed With A Bear-Flattener, NZ-US 10Y Diff Looks Too Low

NZGBs closed showing a bear-flattener, with benchmark yields flat to 2bps higher.

- On a relative basis, the NZGB 10-year has underperformed its US tsy counterpart, with the NZ-US yield differential 2bps higher at flat. (see chart)

- A simple regression of the 1Y3M forward swap spread against the 10-year yield differential over the past 18 months suggests the current differential is 6bps below its estimated fair value of +6bp

- “NZ's central bank considered Hayley Gourley as a potential board member and recommended that option to the government before she was appointed to the MPC.” – BBG

- “NZ is relaxing climate reporting rules due to concerns over the cost to businesses, with companies listed on the NZX only having to provide disclosures if their market capitalisation is NZ$1 billion or more.” - BBG

- Swap rates closed little changed.

- RBNZ dated OIS pricing closed little changed across meetings. 25bps of easing is priced for November, with a cumulative 39bps by February 2026.

- The local calendar will be empty until next Tuesday's release of Filled Jobs data for September.

- On Thursday, the NZ Treasury plans to sell NZ$225mn of the 4.50% May-30 bond, NZ$175mn of the 4.25% May-36 bond and NZ$50mn of the 5.00% May-54 bond.

Figure 1: NZ-US 10-Year Yield Differential

Source: Bloomberg Finance LP / MNI