MNI EUROPEAN OPEN: Japan Core CPI Maintains Firm Trend

EXECUTIVE SUMMARY

- FED’S PERLI SEEING EARLY SIGNS OF SHIFT TO AMPLE RESERVES - MNI

- GERMANY'S MERZ BACKS NORD STREAM BAN - FT

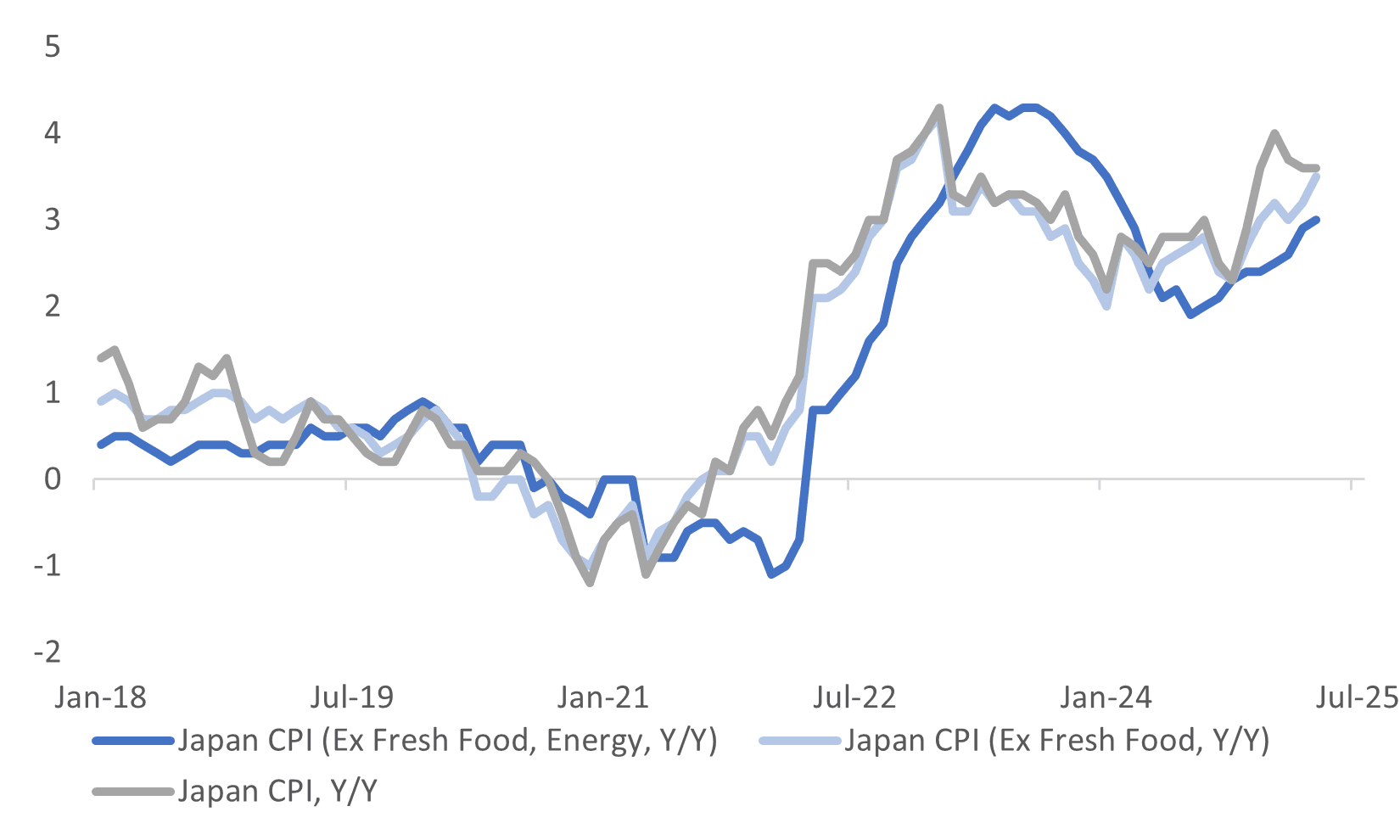

- JAPAN APRIL CORE CPI RISES 3.5% VS. MARCH 3.2% - MNI

- TRUMP INITIATED CALL WITH JAPAN'S ISHIBA, DISCUSSED TARIFFS - BBG

- JAPAN’S AKAZAWA TO VISIT US FOR THIRD ROUND OF US TRADE TALKS - BBG

- FORMER RBA ECONOMISTS DISCUSS THE RBA’S NEXT MOVES - MNI

Fig 1: Japan Core CPI Continuing To Trend Higher

Source: MNI - Market News/Bloomberg/Refinitiv.

UK

CONSUMER CONFIDENCE (BBG): “UK consumer confidence rebounded slightly in May, a new survey showed, as the Bank of England eased borrowing costs and government officials struck a trade deal with the US.”

EU

TRADE (BBG): “European Central Bank President Christine Lagarde warned that international trade will be changed forever by the tensions over tariffs, even as the world’s leading economies edge toward some compromises.”

GERMANY (FT/BBG): " German chancellor Friedrich Merz is backing a proposed EU ban on the Nord Stream pipelines connecting Russia to Germany in an attempt to stop US and Russian efforts to reactivate the gas links, FT reports, citing three officials it didn’t identify."

ECB (MNI SOURCES): Risks Tilt To Downside As ECB Mulls Path Below 2%

SWEDEN (MNI INTERVIEW): Swedish Household Demand Frail - FI Econ Head

US

FED (MNI): The manager of the Federal Reserve's asset portfolio, Roberto Perli, said Thursday he is seeing "early signs" of a transition to ample bank reserves from abundant levels, with the timeline for QT now dependent in part on the efficiency of the Standing Repo Facility.

FED (MNI): Federal Reserve Bank of New York President John Williams said Thursday the optimal supply of bank reserves varies greatly, depending on central bank jurisdiction, uncertainty, the design of liquidity facilities and preferences over the various goals related to monetary policy implementation.

FED (MNI): The Federal Reserve’s framework review is likely to restore greater symmetry between its employment and inflation objectives, but may still end up being too narrowly focused on changes in terminology to be a truly useful exercise in determining what went wrong in the 2021-2022 inflation surge, former Fed officials told MNI.

EDUCATION (RTRS): “U.S. President Donald Trump's administration revoked Harvard University's ability to enroll international students on Thursday, and is forcing current foreign students to transfer to other schools or lose their legal status, while also threatening to expand the crackdown to other colleges.

OTHER

GLOBAL (BBG): "Finance ministers and central bank governors from the Group of Seven nations pledged to address “excessive imbalances” in the global economy, an effort clearly aimed at China, though the final communique omitted the name of the country."

AUSTRALIA (MNI): Former RBA economists discuss the RBA's next moves

JAPAN (MNI BRIEF): Japan's annual core consumer inflation rate accelerated to 3.5% in April from 3.2% in March, driven by rising food prices excluding perishables and energy, data from the Ministry of Internal Affairs and Communications showed Friday.

JAPAN/US (BBG): 'US President Donald Trump initiated a phone call with Japanese Prime Shigeru Ishiba and discussed tariffs in general terms, just as Tokyo’s top negotiator left for the US for another round of trade talks. Trump didn’t say anything specific about tariffs while Ishiba reiterated Japan’s existing stance over the levies during a 45-minute meeting, the prime minister told reporters on Friday in Tokyo."

JAPAN (BBG): “Japan’s top trade negotiator Ryosei Akazawa will leave Friday for the US for a third round of trade talks with the Trump administration.”

PHILIPPINES (BBG): “ The Philippine central bank is looking at reducing its holdings of US Treasuries after Moody’s Ratings downgraded the US’ credit score, according to Governor Eli Remolona.”

CHINA

US/CHINA (BBG): "Beijing and Washington continued high-level contact with a Thursday call between senior officials, a sign that the two sides are maintaining active communications following their trade truce earlier this month. US Deputy Secretary of State Christopher Landau and China’s Executive Vice Foreign Minister Ma Zhaoxu discussed a wide range of issues of mutual interest, according to a statement from the US State Department.

ASEAN (21ST CENTURY HERALD): "The upcoming China ASEAN Free Trade Area 3.0 agreement introduces a digital economy chapter covering connectivity in hard digital infrastructure, electronic payment systems and personal information protection, as well as network security rules, according to Zhai Kun, deputy director at Peking University, following the announcement negotiations on the deal have been finalised."

CHINA MARKETS

MNI: PBOC Net Injects CNY36 Bln via OMO Friday

MNI (BEIJING) - The People's Bank of China (PBOC) conducted CNY142.5 billion via 7-day reverse repos, with the rate unchanged at 1.40%. The operation led to a net injection of CNY36 billion after offsetting the maturities of CNY106.5 billion today, according to Wind Information.

- The seven-day weighted average interbank repo rate for depository institutions (DR007) fell to 1.5060% at 09:30 am local time from the close of 1.5660% on Thursday.

- The CFETS-NEX money-market sentiment index, measuring interbank money-market liquidity, closed at 48 on Thursday, compared with the close of 45 on Wednesday. A higher reading points to tighter liquidity condition, with 50 representing an equilibrium.

MNI: PBOC Sets Yuan Parity Higher At 7.1919 Fri; +0.62% Y/Y

MNI (BEIJING) - The People's Bank of China (PBOC) set the dollar-yuan central parity rate higher at 7.1919 on Friday, compared with 7.1903 set on Thursday. The fixing was estimated at 7.2154 by Bloomberg survey today.

MARKET DATA

NEW ZEALAND Q1 RETAILS SALES EX INFLATION Q/Q 0.8%; MEDIAN 0.0%; PRIOR 1.0%

JAPAN APR NATL CPI Y/Y 3.6%; MEDIAN 3.5%; PRIOR 3.6%

JAPAN APR NATL CPI EX FRESH FOOD Y/Y 3.5%; MEDIAN 3.4%; PRIOR 3.2%

JAPAN APR NATL CPI EX FRESH FOOD, ENERGY Y/Y 3.0%; MEDIAN 3.0%; PRIOR 2.9%

SOUTH KOREA APR PPI Y/Y 0.9%; PRIOR 1.3%

UK MAY GfK CONSUEMR CONFIDENCE -20; MEDIAN -22; PRIOR -23

MARKETS

US TSYS: Asia Wrap - Quiet session

TYM5 has traded higher within a range of 109-29 to 110-02+ during the Asia-Pacific session. It last changed hands at 109-30+, up 0-04 from the previous close.

- The US 2-year yield has drifted lower, dealing around 3.98%, down 0.01 from its close.

- The US 10-year yield is dealing around 4.5270%, unchanged from its close.

- Bloomberg - “Donald Trump’s tax bill faces changes and delays in the Senate after narrowly passing the House. Majority Leader John Thune said senators have questions about tax permanence and are engaged in a “very active discussion” over Medicaid.”

- Bloomberg - “Finance ministers and central bank governors from the G7 nations pledged to address “excessive imbalances" in the global economy, aiming to create a level playing field and increase transparency. The communique called for an analysis of market concentration and international supply chain resilience, and recognised the potential risks of international low-value shipments, often from Chinese retailers.”

- The 10-year found buyers eventually above 4.60% as shorts are pared back into the US long weekend, this demand helped yields back off in the US session. Support seen back towards 4.45/50%, dips look likely to see supply in the short-term. Should yields hold this break higher we will then target the 4.75% area.

- Data/Events : New Home Sales, Kansas City Fed Services Activity

JGBS: Bull-Flattener Partially Reverses Some Of This Week's Carnage

JGB futures are stronger and at Tokyo session highs, +22 compared to settlement levels.

- Outside of the previously outlined National CPI, there haven't been many by way of domestic drivers to flag.

- “US President Donald Trump initiated a phone call with Japanese Prime Minister Shigeru Ishiba to discuss tariffs in general terms. The two leaders discussed various topics, including tariff negotiations, economic security cooperation, and national security.” (per BBG)

- " Workers at companies affiliated with the Japan Business Federation won pay hikes exceeding 5% for a second consecutive year, which will help to keep a floor under domestic inflation"(BBG)

- Cash US tsys are slightly richer in today's Asia-Pac session after yesterday's rally. A light US calendar tonight with New Home Sales and Kansas City Fed Services Activity data due. The US markets will be closed for Memorial Day on Monday.

- Cash JGBs have bull-flattened, with yields 1-6bps lower. The benchmark 30-year yield is 4.5bps lower (2bps lower in the last 10mins) at 3.135% versus the high of 3.204% set this week.

- Swap rates are little changed out to the 7-year range but 1-3bps lower beyond. Swap spreads are mixed.

- On Monday, the local calendar will see Coincident/Leading Index data alongside an Auction for Enhanced-Liquidity 5-15.5 YR.

AUSSIE BONDS: Modestly Mixed, Subdued Session, US Holiday Mon, CPI On Wed

ACGBs (YM -1.0 & XM +1.5) are slightly mixed on a light local-data day.

- Cash US tsys are slightly richer in today's Asia-Pac session after yesterday's rally. US markets will be closed for Memorial Day on Monday.

- Cash ACGBs are 1bp cheaper to 1bp richer with a flatter 3/10 curve.

- The AU-US 10-year yield differential is -8bps, positioned in the bottom half of the +/- 30bps range that has largely held since November 2022.

- The bills strip is -1 to -3 across contracts.

- RBA-dated OIS pricing is little changed across meetings today but 8-17bps softer than Tuesday's pre-RBA levels. A 25bp rate cut in July is given a 64% probability, with a cumulative 67bps of easing priced by year-end.

- As a result, the expected year-end policy rate differential between Australia and New Zealand has narrowed by approximately 16bps over the past week, currently sitting at +30bps.

- The local calendar will be empty on Monday and Tuesday ahead of April's CPI on Wednesday.

- Next week, the AOFM plans to sell A$400mn of the 4.25% 21 June 2034 bond on Tuesday and A$1200mn of the 4.25% 21 March 2036 bond on Friday.

BONDS: NZGBS: Modest Twist-Flattening To Finish The Week, RBNZ Decision On Wed

NZGBs closed off bests, showing at twist-flattening, with benchmark yields 1bp higher to 2bps lower.

- Today’s supply saw solid demand across the lines with cover ratios ranging from 2.92x (Apr-29) to 3.33x (Apr-33).

- Cash US tsys are slightly richer in today's Asia-Pac session after yesterday's rally. A light US calendar tonight with New Home Sales and Kansas City Fed Services Activity data due. The US markets will be closed for Memorial Day on Monday.

- Swap rates closed little changed.

- The local calendar will be empty for Monday and Tuesday next week ahead of the RBNZ Policy Decision on Wednesday. 25bps of easing is fully priced next week meeting.

- RBNZ-dated OIS pricing has seen little change across meetings compared to this time last week, with rates remaining 2–18bps above levels observed prior to the Q1 CPI release on April 17.

- However, following Tuesday’s RBA easing and dovish tilt, RBA OIS pricing has softened 8-17bps versus pre-RBA levels.

- As a result, the expected year-end policy rate differential between Australia and New Zealand has narrowed by approximately 16bps over the past week, currently sitting at +30bps.

FOREX: Asia FX Wrap - Fresh USD Selling In Asia

The BBDXY has had a range of 1217.67 - 1221.00 in the Asia-Pac session, it is currently trading around 1217. “The PBOC’s net injections of liquidity via one-year medium-lending facility for a third month in May suggests a policy focus to stabilize growth, according to a report by Shanghai Securities News" - BBG. “The White House’s chief economist rejected the notion that a secret currency accord to weaken the dollar is in the works, and instead touted the benefits of a strong greenback.” - BBG

- EUR/USD - Asian range 1.1279 - 1.1319, Asia is currently trading 1.1310. A quiet Asian session with EUR drifting higher. The market is still expected to use dips as a buying opportunity where dips back towards 1.10 should see buyers remerge.

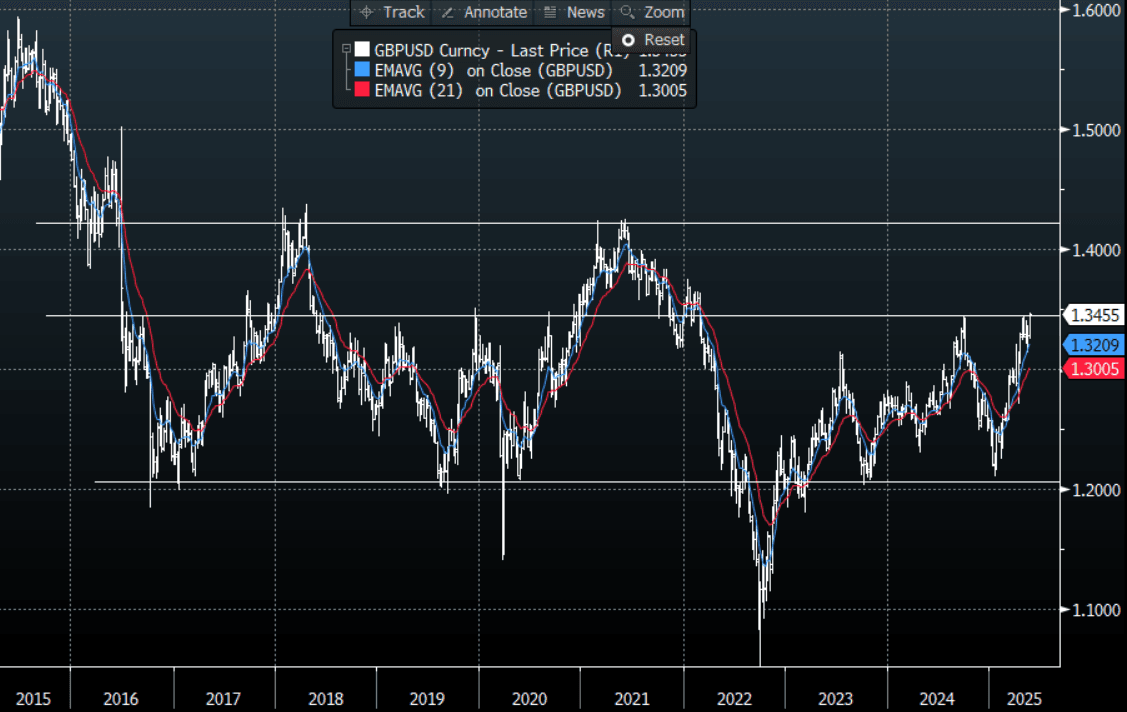

- GBP/USD - Asian range 1.3412 - 1.3451, Asia is currently dealing around 1.3450. A quiet Asian session with GBP drifting higher. The GBP is back to testing Pivotal Weekly Resistance in the 1.3500 area, expect it to do some work here. A sustained break signals a potential acceleration of the trend higher.

- USD/CNH - Asian range 7.1967 - 7.2058, the USD/CNY fix printed 7.1919. Asia is currently dealing around 7.1985. Sellers should continue to be found on a bounce back towards the 7.2400 area again.

- Cross asset : SPX +0.01%, Gold $3315, US 10-Year 4.53%, BBDXY 1217, Crude oil $60.86

Data/Events : Ger GDP, Fra Consumer Confidence, Fed Governor Lisa Cook, St. Louis Fed President Alberto Musalem and Kansas City Fed chief Jeff Schmid are scheduled to speak later Friday. Chicago Fed President Austan Goolsbee will also be interviewed on CNBC.

Fig 1: GBP/USD Spot Weekly Chart

Source: MNI - Market News/Bloomberg

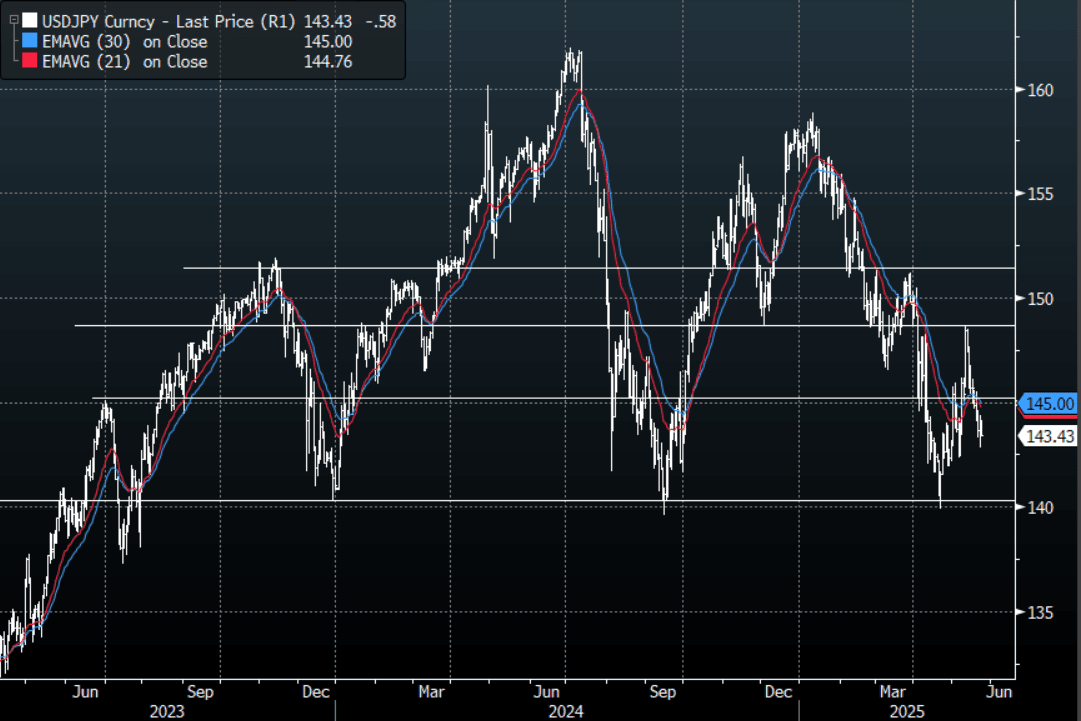

JPY: Asia Wrap - Sellers Cap Move Above 144.00 Again

The Asia-Pac range has been 143.40 - 144.14, Asia is currently trading around 143.45. The relief from USD selling overnight did not last long, USD/ASIA has seen a fresh round of selling in our session as Asia's major markets have another strong week of inflows with almost $2bn recorded to yesterday.

- "Japan's hotter-than-expected core inflation boosts odds of a Bank of Japan rate hike in July, ING's Min Joo Kang says in a research report. Consumer prices excluding fresh food rose 3.5% in April from a year earlier, up from March's 3.2% increase, and exceeded the market consensus of a 3.4% increase, the senior economist for South Korea and Japan notes. Excluding fresh food and energy, core-core CPI rose 3.0% on year in April, which suggests underlying inflation will remain above the BOJ's target of 2.0%, the economist says." (DJ via BBG)

- “ Workers at companies affiliated with the Japan Business Federation won pay hikes exceeding 5% for a second consecutive year, which will help to keep a floor under domestic inflation”(BBG)

- “ISHIBA: FEEL TRUMP AND I SHARED BROAD UNDERSTANDING, CONVEYED HOPE FOR PRODUCTIVE TALKS OVER TRADE; WILL KEEP SEEKING REMOVAL OF ADDITIONAL US TARIFFS" - BBG

- USD/JPY again struggled to hold onto any gains above 144.00, fresh USD/Asia selling has seen the USD broadly lower in our session.

- The price action for the week shows the market is still much more comfortable selling rallies, resistance is now back towards 145.00/146.00. The longer we stay down here the focus will turn once more to the pivotal 140.00 area.

Options : Closest significant option expiries for NY cut, based on DTCC data: 145.00($2.1b May 23),144.00($2.09b May 23), 140.00(1.67b May 23). Upcoming Strikes : 143.00($1.36b May 28), 145.00($1.39b May 28).(BBG)

Fig 1 : USD/JPY Spot Daily Chart

Source: MNI - Market News/Bloomberg

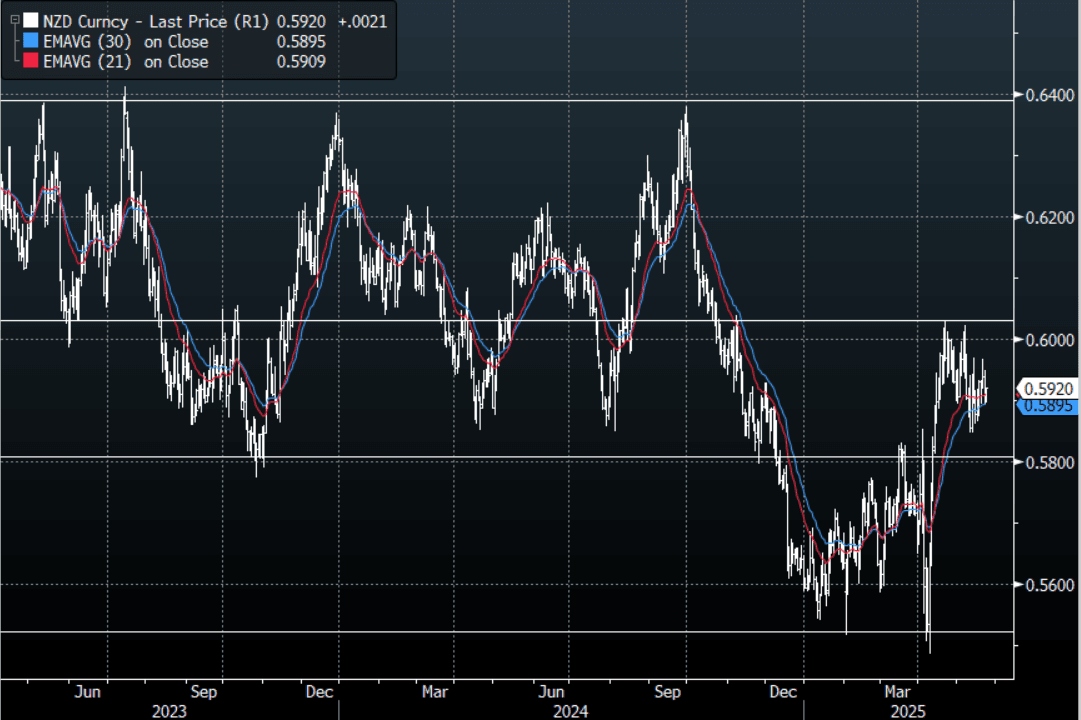

NZD: Asia Wrap - NZD/USD Bounces Off 0.5900

The NZD/USD had a range of 0.5896 - 0.5921 in the Asia-Pac session, going into the London open trading around 0.5920. The USD found some good demand overnight as some positions were pared back heading into the US long weekend. This price action has not followed into our session as fresh selling in USD/ASIA has seen the USD struggle across the board today, Asia's major stock markets had another strong week of inflows with almost $2bn recorded to yesterday.

- Q1 Retail Volumes Up More Than Forecast, Y/Y Pace Edges Higher : New Zealand Q1 retail sales volumes rose 0.8%q/q, versus a flat market forecast. The Q4 rise was also nudged a little higher to +1.0% (against an originally reported 0.9% gain). Today's print is a positive in the sense that other retail/consumer spend indicators have suggested a more adverse backdrop.

- “The Treasury cut projections for bond issuance by NZ$2 billion each of two fiscal years starting in July, The reduction in issuance projections was “tangible positive news,” ANZ senior strategist David Croy writes in a note.”(BBG)

- The NZD/USD has traded quietly bid in Asia today bouncing off the support it found around the 0.5900 area overnight.

- The NZD continues to look comfortable in a 0.5850/0.6050 range and awaits a catalyst to provide the impetus to break-out.

- The support back towards 0.5800 has held very well, and while this continues to hold expect buyers to be around on dips. The first target is the highs just above 0.6000, a break here is needed to regain momentum.

- Options : Closest significant option expiries for NY cut, based on DTCC data: none, Upcoming Strikes : 0.5705(NZD805m May 23), 0.5980(NZD513m May26)

AUD/NZD range for the session has been 1.0862 - 1.0884, currently trading 1.0875. A sustained break above 1.0930 is needed to turn the focus higher, until then expect supply on bounces.

Fig 1: NZD/USD Spot Daily Chart

Source: MNI - Market News/Bloomberg

AUD: Asia Wrap - AUD/USD Benefits From USD/Asia Selling

The AUD/USD has had a range of 0.6408 - 0.6438 in the Asia- Pac session, it is currently trading around 0.6435. The USD found some good demand overnight as some positions were pared back heading into the US long weekend. This price action has not followed into our session as fresh selling in USD/ASIA has seen the USD struggle across the board today, Asia's major stock markets are staring at another strong week of inflows with almost $2bn recorded to yesterday.

- Bloomberg - “Donald Trump’s tax bill faces changes and delays in the Senate after narrowly passing the House. Majority Leader John Thune said senators have questions about tax permanence and are engaged in a “very active discussion” over Medicaid.”

- “The path lower for dollar-yuan is being endorsed by a trickle down of PBOC daily fixings and its directional relationship with the forwards curve.”(BBG)

- The AUD has been quietly bid for most of the Asian session benefitting from fresh selling across the board in USD/ASIA.

- The AUD/USD is looking comfortable in a 0.6350 - 0.6550 range. The AUD continues to hold up pretty well against the USD so If you want to express a short it looks best to do that in the crosses for now.

- Expect buyers to be around on dips while the support in the AUD holds, a close back below 0.6300/50 would start to challenge the newly formed uptrend.

- Options : Closest significant option expiries for NY cut, based on DTCC data: 0.6375(AUD683m May 23),0.6475(AUD500m May 23) 0.6550(AUD529m May 23), Upcoming Strikes : 0.6510(AUD1.4b May 27)

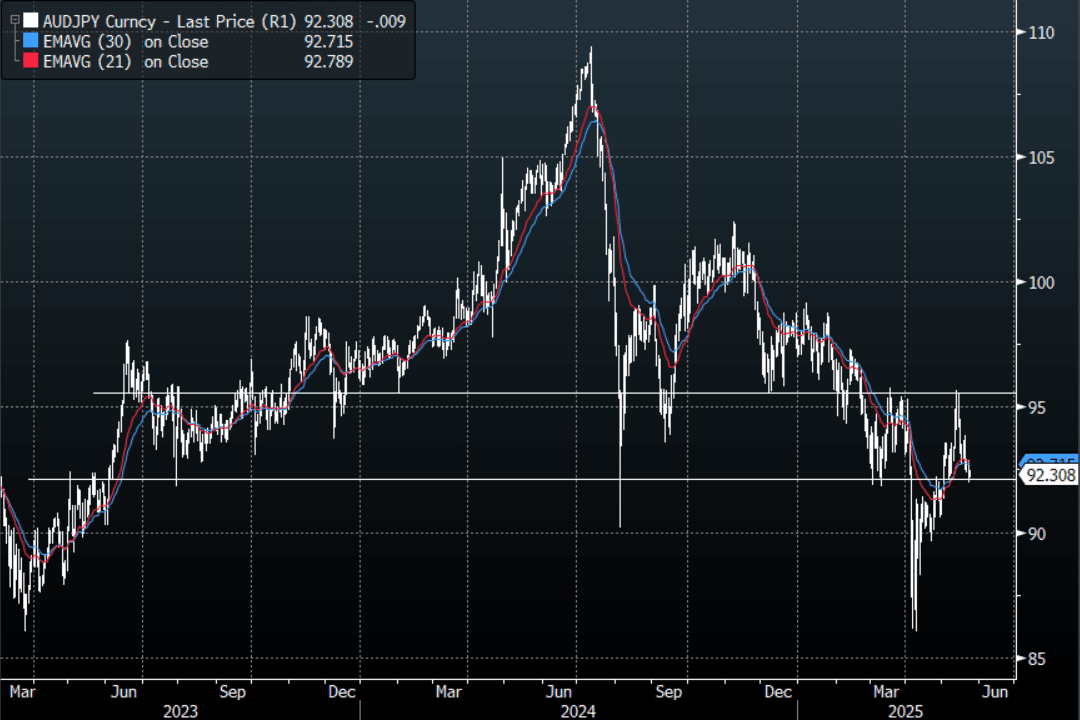

AUD/JPY - Today's range 92.16 - 92.48, it is trading currently around 92.30. Decent demand again seen towards the 92.00 area as it holds overnight. A sustained close back below 91.50/92.00 is needed to turn the focus back towards the lows again. With stocks looking like they could have more to go in this retracement it could provide further headwinds for this pair.

Fig 1: AUD/JPY spot Daily Chart

Source: MNI - Market News/Bloomberg

ASIA STOCKS: Major Bourses Mixed as US Fiscal Concerns Remain

Asia's major indexes have had a mixed week this week as deep concerns as to the US fiscal position impacted markets with China being the exception. Asian shares had a better day Friday as bond yield's climb higher stalled.

- China's major bourses all gained today with the Hang Seng up +0.58% and +1.43% for the week. The CSI 300 rose +.30% and is up +0.94% for the week; Shanghai is up a mere +0.08% and +0.46% for the week and Shenzhen gained +0.55% today and +0.77% for the week.

- The KOSPI was down marginally today by -0.05% and is off by -1.33% for the week.

- The FTSE Malay KLCI bounced higher today by +0.48% yet is down by -2.38% for the week.

- The Jakarta Composite is up +0.36% and is one of the best performers in the region up +1.22% for the week.

- The FTSE Straits Times in Singapore is lower by -0.18% and down by -0.63% for the week and the PSEi in the Philippines bounced strongly today by +0.89% yet remains -1.6% lower for the week.

- India's NIFTY 50 is up +0.80% whilst remaining down by -0.85% for the week.

Oil Heading for Large Weekly Fall

- As OPEC+ continues to discuss yet another increase in production, oil prices have delivered large losses for the week.

- OPEC+ are discussing another rise in oil production for July with the final decision to be made next month.

- WTI has steadied today at US$60.84 bbl today and is on track to be lower by over -2.5% for the week.

- The falls this week sees WTI now trading below all major moving averages.

- Brent steadied in the Asia trading day to stem the overnight falls, yet remains on track to be lower by -2.00% for the week and is below all major moving averages.

- The EU is economy chief said it would be 'appropriate to lower the price cap on Russian oil to $50 bbl' to toughen Moscow's ability to fund the war in Ukraine. The current cap is set at $60, operators can buy oil from Russia only when it's purchased below the cap.

GOLD: Yesterday's Losses Forgotten

- Gold all but erased last night's losses to gain +0.54% in the Asian trading session to reach US$3312.33.

- The rally today puts gold on track to deliver gains over 3% for the week as fear over the US fiscal position saw a flight to bullion.

- Gold sits above all major moving averages; the nearest being the 20-day EMA of $3,272.06 with all moving averages sloping upwards, a sign that the bullish momentum remains.

- Gold has only failed to deliver a weekly gain in five of the twenty two weeks of the year so far.

China’s onshore, gold-backed exchange-traded funds saw inflows resume as prices rebounded, according to a report by China Securities Journal. Some 20 gold ETFs listed on Chinese bourses received inflows of about 370m yuan on May 21, report said, citing data from Wind (source BBG)

UP TODAY (TIMES GMT/LOCAL)

| Date | GMT/Local | Impact | Country | Event |

| 23/05/2025 | 0600/0800 | ** | Unemployment | |

| 23/05/2025 | 0600/0700 | *** | Retail Sales | |

| 23/05/2025 | 0600/0800 | *** | GDP (f) | |

| 23/05/2025 | 0645/0845 | ** | Consumer Sentiment | |

| 23/05/2025 | 0830/1030 | ECB's Lane Inflation Lecture in Florence | ||

| 23/05/2025 | 1230/0830 | * | Quarterly financial statistics for enterprises | |

| 23/05/2025 | 1230/0830 | ** | Retail Trade | |

| 23/05/2025 | 1230/0830 | ** | Retail Trade | |

| 23/05/2025 | 1335/0935 | Kansas City Fed's Jeff Schmid | ||

| 23/05/2025 | 1400/1000 | *** | New Home Sales | |

| 23/05/2025 | 1400/1000 | *** | New Home Sales | |

| 23/05/2025 | 1600/1800 | ECB's Schnabel Speech on Financial Education and Monpol | ||

| 23/05/2025 | 1600/1200 | Fed Governor Lisa Cook | ||

| 23/05/2025 | 1700/1300 | ** | Baker Hughes Rig Count Overview - Weekly | |

| 23/05/2025 | 1700/1300 | ** | Baker Hughes Rig Count Overview - Weekly |