ASIA STOCKS: Major Bourses Mixed as US Fiscal Concerns Remain

Asia's major indexes have had a mixed week this week as deep concerns as to the US fiscal position impacted markets with China being the exception. Asian shares had a better day Friday as bond yield's climb higher stalled.

- China's major bourses all gained today with the Hang Seng up +0.58% and +1.43% for the week. The CSI 300 rose +.30% and is up +0.94% for the week; Shanghai is up a mere +0.08% and +0.46% for the week and Shenzhen gained +0.55% today and +0.77% for the week.

- The KOSPI was down marginally today by -0.05% and is off by -1.33% for the week.

- The FTSE Malay KLCI bounced higher today by +0.48% yet is down by -2.38% for the week.

- The Jakarta Composite is up +0.36% and is one of the best performers in the region up +1.22% for the week.

- The FTSE Straits Times in Singapore is lower by -0.18% and down by -0.63% for the week and the PSEi in the Philippines bounced strongly today by +0.89% yet remains -1.6% lower for the week.

- India's NIFTY 50 is up +0.80% whilst remaining down by -0.85% for the week.

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

BUND TECHS: (M5) Bullish Trend Structure Intact

- RES 4: 133.90 1.236 proj of the Mar 25 - Apr 7- 9 price swing

- RES 3: 133.00 round number resistance

- RES 2: 132.56 High Feb 28 and a key resistance

- RES 1: 132.03 High Apr 7 and the bull trigger

- PRICE: 131.82 @ 05:45 BST Apr 23

- SUP 1: 130.87/130.31 Low Apr 17 / 20-day EMA

- SUP 2: 129.02 Low Apr 10

- SUP 3: 128.60 Low Apr 9 and a key support

- SUP 4: 128.47 Low Mar 28

Bund futures continue to trade closer to their recent highs. A bull cycle remains in play and the pullback between Apr 7 - 9 is considered corrective. A fresh short-term cycle high on Apr 7 reinforces a bullish theme. The contract has recently cleared 131.14, 76.4% of the Feb 28 - Mar 11 bear leg. This opens 132.56 next, the Feb 28 high. Firm support lies at 128.60, the Apr 9 low. A break below this level would alter the picture.

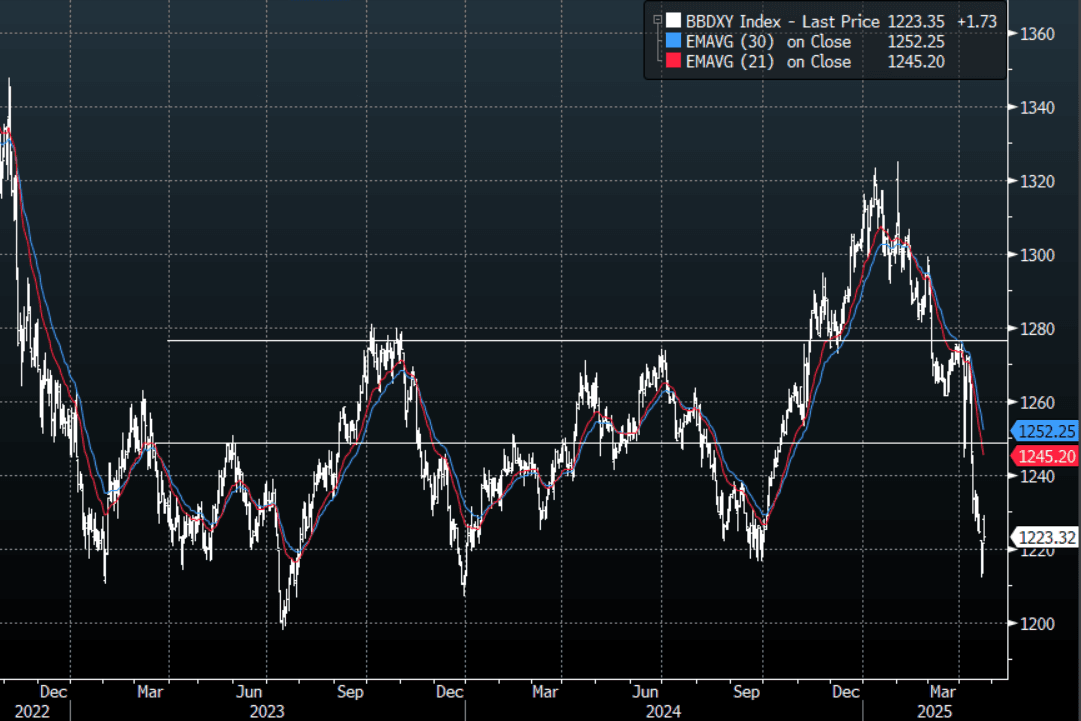

FOREX: FX Wrap - USD Rebounds

The BBDXY had an Asian range of 1221.87 - 1229.02. With risk turning around on Trump’s U-turn on Powell and China, as well as Tesla soaring on Elon Musk saying he would be pulling back significantly from DOGE, the USD has had a decent bounce. Is this move sustainable ? Should risk continue to rally we could see some relief from short-term oversold levels but the market will see a decent bounce as an opportunity to once again fade. Bloomberg reports Emmanuel Macron is exploring the possibility of dissolving parliament and holding snap elections as soon as this fall.

- EUR/USD - Asian range 1.1308 - 1.1429, has given back all of Mondays gains and more. The EUR comes off from levels that are overbought, it's been a huge move when you consider it was trading sub 1.0400 the beginning of March. The consensus trade is now to be short USD, a short term rally would be healthy. Demand should remerge on dips back to 1.1100.

- GBP/USD - Asian range 1.3234 - 1.3338, like the EUR Asia looked to be stopping out weaker hands. Dips should be supported, first around 1.3200 then the big support towards 1.3000.

- USD/JPY - Asian range 141.49 - 143.22, large gap higher in the Asian open in what looked to be stops being executed as risk rallied. Supply returned above 143.00 and we have drifted lower for the session from then onwards. USD/JPY’s fate is tied to whether risk is able to hold onto these gains and begin a sustained rally or if this is just another bounce to be faded.

- AUD/USD - Asian Range 0.6349 - 0.6405, The initial leg higher in risk saw the AUD move lower as the USD got bought. Decent buyers emerged around 0.6350 and the AUD has moved back towards 0.6400 going into London.

- USD/CNH - Asian range 7.2922 - 7.3156, the USD/CNY fix printed at 7.2116. USD/CNH continues to trade sideways and find support towards 7.2800.

- Cross asset : SPX +1.58%, Gold 3340, US 10yr 4.35%, BBDXY 1223, Crude oil 64.22.

- Data/Events : US S&P Global Services & Manufacturing PMI, FRA PMI’s, GER PMI’s, EC PMI’s, EC Trade Balance

Fig 1 : BBDXY Daily Chart

Source: MNI - Market News/Bloomberg

BONDS: NZGBS: Closed Slightly Cheaper, Focus Abroad As Risk-On Extends

NZGBs closed slightly cheaper, with benchmark yields 1-2bps cheaper. With the local calendar light today, the domestic market has focused its attention abroad.

- Risk-on sentiment extended into today's Asia-Pac session after US President Trump stated that he had no intention of firing Fed Chair Powell.

- Trump also stated that the final tariff number for China wouldn't be near the current 145%. He also expressed optimism around trade deals with lots of countries and spoke of the large investment agreements reached for flows into the US.

- Cash US tsys have twist-flattened in today's Asia-Pac session, with yields 2bps higher to 8bps lower.

- The NZ–US 10-year yield differential widened by 6bps to +14bps. This places the spread roughly where it was in early March, though it's about 20bps narrower than its levels in early April.

- Swap rates closed flat to 3bps higher, with the 2s10s curve flatter.

- RBNZ dated OIS pricing closed flat to 3bps firmer across meetings, with late 2025 leading. 27bps of easing is priced for May, with a cumulative 80bps by November 2025.

- Tomorrow, the local calendar will see ANZ Consumer Confidence.

- The NZ Treasury plans to sell NZ$250mn of the 4.50% May-30 bond and NZ$250mn of the 4.25% May-36 bond tomorrow.