MNI: Ex-RBA Economists Tip Two Cuts On Tight Labour Outlook

The Reserve Bank of Australia is likely to deliver two more 25-basis-point cuts this year coinciding with updated forecast publications, former staffers told MNI, arguing that the RBA’s concerns over labour market tightness means that the market’s expectation for the cash rate to reach 3.1% by December is likely overblown.

“3.1% would be a slightly expansionary setting rather than a neutral one and would only be needed if the labour market weakens,” said Mark Wooden, professorial fellow at the Melbourne Institute and former Fair Work Commission panel member. “That might happen if the trade war seriously affects demand from key partners like China. But otherwise, two more cuts seem most likely.”

The RBA’s dovish tilt this week as it cut by 25bp to 3.85% prompted markets to lower year-end cash rate expectations by about 15bp. (See chart)

Blair Chapman, senior economist at Seek and former RBA research economist, said future rates moves will likely align with the release of updated Statement on Monetary Policy forecasts – next due Aug 7-8 and Nov 3-4. While some see a potential July cut, Chapman said the board’s relatively optimistic inflation and employment outlook suggests a more cautious path unless major shocks emerge.

“The labour market has already surprised them on the upside, and during the press conference [Governor Michele Bullock] was dismissive of the monthly CPI indicator,” Chapman said. “They’ll likely wait for the quarterly CPI on July 30 and the next forecast round before cutting again in August.”

Markets currently assign a 64.7% probability of a July cut, with August attracting a 96% chance.

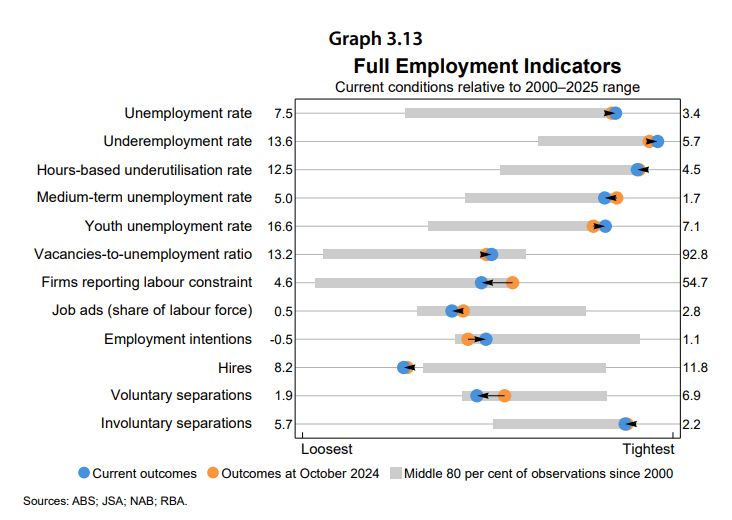

LABOUR OF LOVE

The RBA’s employment outlook, described with a high degree of uncertainty in May’s SOMP, factored in two more cuts, said Tim Robinson, senior research fellow at the Melbourne Institute and former RBA economist, noting subtle changes to how the Reserve presented labour slack.

“For the unemployment and underemployment gaps, as well a range of central estimates from various models, they now also have a measure of the confidence intervals. These do include positive values,” he said.

“It’s not clear that this constitutes a change in thinking, but it does convey the large amount of uncertainty that surrounds these estimates. That is typical but they are making it more obvious.” However, direct data still suggested a tight labour market, he argued. (See chart)

Bullock’s comment at the press event following this week's decision that the RBA may need to reevaluate its view of full employment is not likely to lead to a major shift in the estimated NAIRU (non-accelerating inflation rate of unemployment), Wooden noted. (See MNI RBA WATCH: Board's Dovish Turn Included Debate Of 50bp Cut) “Most indicators have been stable for some time – the employment-to-population ratio has hovered near record highs for over a year – so they have had ample time to reach this revised assessment,” he said.

With unemployment around 4.1%, Wooden said a sub-4% jobless rate would likely be inflationary. “There’s no strong reason to believe NAIRU has recently shifted. It’s likely still around 4%.” Still, Wooden stressed that the RBA should focus on broader indicators, such as the employment-to-population ratio and hours worked, when judging labour market slack and its inflationary impact.

Chapman pointed to declining average hours worked as indicating hidden slack not captured by unemployment rates. “Also, recent state government EBAs [enterprise bargaining agreements] and [Fair Work Commission] decisions may see the RBA's NAIRU estimate remain higher than some commentators think, unless the RBA controls for these recent backward-looking and policy-induced changes in wage growth in their wage Phillips curve models,” he said.

Chapman added that the RBA’s May 14 forecast cutoff meant it missed some of the latest jobs data within the latest SOMP. “Their June forecast assumes a 100,000 drop in employment over two months," he continued, adding that any errors would throw off unemployment and inflation forecasts.