MNI EUROPEAN OPEN: BoJ On Hold As Expected

EXECUTIVE SUMMARY

- POWELL LEAVES DOOR AJAR TO SEPTEMBER CUT - MNI FED WATCH

- TRUMP SAYS US WILL SET 15% TARIFF ON SOUTH KOREAN IMPORTS UNDER NEW DEAL - RTRS

- BOJ KEEPS RATE AT 0.50%; STICKS TO GRADUAL HIKE - MNI BRIEF

- BOJ UPS FY25CPI TO 2.7%; PRICE RISK BALANCED - MNI BRIEF

- CHINA JUL MANUFACTURING PMI FALLS WITHIN CONTRACTION - MNI BRIEF

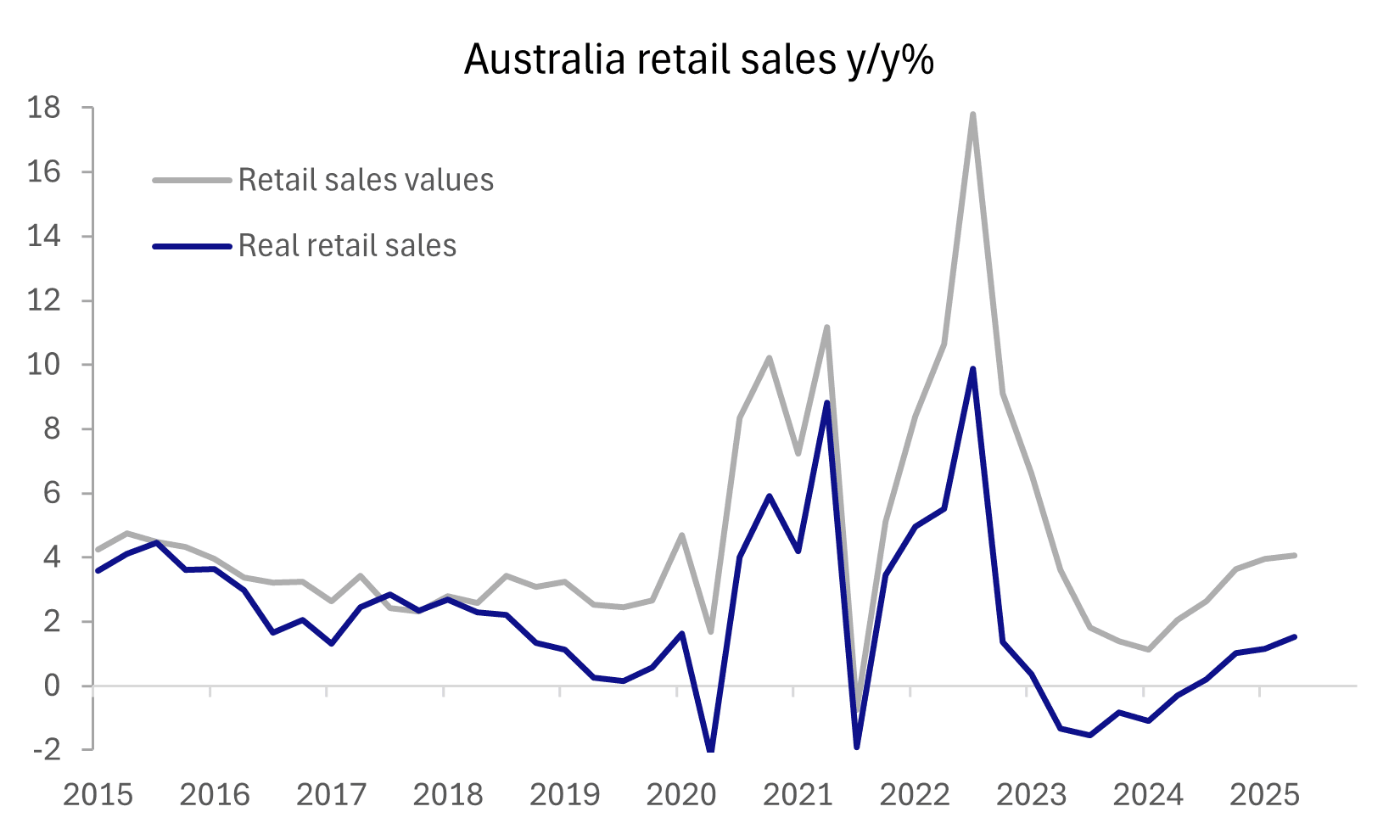

- AUSSIE RETAIL SPENDING RISES IN JUNE - MNI BRIEF

Fig 1: Australian Retail Sales

Source: MNI/ABS

UK

WAGES (BBC): “The British Medical Association and Health Secretary Wes Streeting have agreed to resume talks following the end of the latest strike by resident doctors in England.”

EU

UKRAINE (RADIO FREE EUROPE): “On the streets of multiple Ukrainian cities hundreds of people called on lawmakers to approve a draft bill to strengthen powers of the National Anti-Corruption Bureau of Ukraine (NABU) and the Specialized Anti-Corruption Prosecutor's Office (SAPO). Parliament is due on July 31 to discuss the bill -- which marks a reversal of a law passed with unusual rapidity on July 22.”

UKRAINE (POLITICO): “Tsyvinskyi, a veteran anti-corruption detective, was selected on June 24 by an independent commission to lead Ukraine’s Economic Security Bureau, which probes economic crimes. But two successive government cabinets in Kyiv have refused to confirm his appointment, despite Ukraine’s pledges to both the EU and the International Monetary Fund to comply.”

US

TRADE (RTRS): “President Donald Trump said on Wednesday the U.S. will charge a 15% tariff on imports from South Korea as part of a deal that eases, for now, tension with a top-10 trading partner and key Asian ally.”

TRADE (BBC): “US President Donald Trump signed an executive order ending a global tariff exemption used by shoppers of low-cost goods. The order, signed on Wednesday, comes into force on 29 August and broadens earlier presidential action that specifically targeted cheap products from China and Hong Kong to now cover the rest of the world.”

FED (MNI FED WATCH): Federal Reserve Chair Jerome Powell signaled Wednesday the door to a rate cut at the September FOMC meeting is open, but the Fed leader did not commit to a move, instead emphasizing that the central bank should know a lot more about how the economy is responding to the Trump administration's policies by its next meeting.

FED (MNI): Attached is a rough transcript of Fed Chair Jerome Powell's July 30 press conference.

FED (MNI): The Federal Reserve kept interest rates steady Wednesday for a fifth straight meeting but two governors dissented in favor of lowering rates by a quarter point, against a backdrop of relentless pressure from the White House for the central bank to reduce borrowing costs.

OTHER

CANADA (MNI INTERVIEW): BOC Idle Rest Of Yr Despite Cut Talk- Ex Staffer

JAPAN (MNI BRIEF): Japan's industrial output rose 1.7% m/m in June, marking the first increase in three months after a 0.1% decline in May, data released by the Ministry of Economy, Trade and Industry showed on Thursday, driven by stronger production of electronic parts and devices, as well as general-purpose and business-oriented machinery.

JAPAN (MNI BRIEF): The Bank of Japan, as widely expected, left its policy interest rate unchanged at 0.50% on Thursday, citing continued high uncertainty surrounding the economic and inflation outlook.

JAPAN (MNI BRIEF): The Bank of Japan on Thursday raised its median forecast for core consumer prices in fiscal 2025 to 2.7% from 2.2% in April, citing stronger-than-expected price moves driven by surging rice costs and their spillover to food prices, following the Board's decision to hold the policy rate at 0.5%.

AUSTRALIA (MNI BRIEF): The market had overestimated the chance of a cut at the July meeting due to significant global uncertainty and its impact on the Reserve Bank of Australia Board’s outlook, Deputy Governor Andrew Hauser told an industry forum on Thursday.

AUSTRALIA (MNI): MNI discusses the RBA's cash rate strategy.

AUSTRALIA (MNI BRIEF): Australian retail turnover rose 1.2% in June following May's 0.5% increase, higher than the 0.4% market expectation, according to data released by the Australian Bureau of Statistics on Tuesday.

BRAZIL (RTRS): “U.S. President Donald Trump on Wednesday slapped a 50% tariff on most Brazilian goods to fight what he has called a "witch hunt" against former President Jair Bolsonaro, but softened the blow by excluding sectors such as aircraft, energy and orange juice from heavier levies.”

BRAZIL (MNI EM WATCH): BRASILIA - The Central Bank of Brazil said Wednesday it will maintain its official Selic rate at 15.00% for a "very prolonged period," reiterating an "interruption" that points to the end to the tightening cycle but also attempts to push back on any premature expectations for cuts.

CHINA

MANUFACTURING (MNI BRIEF): China's Manufacturing Purchasing Managers Index fell by 0.4 points to 49.3 in July, staying below the breakeven 50 mark for the fourth month, affected by traditional off-season, high temperatures, heavy rains and floods in some areas, data from the National Bureau of Statistics showed Thursday.

MNI: PBOC Net Drains CNY47.8 Bln via OMO Thursday

MNI (BEIJING) - The People's Bank of China (PBOC) conducted CNY283.2 billion via 7-day reverse repos, with the rate unchanged at 1.40%. The operation led to a net drain of CNY47.8 billion after offsetting maturities of CNY331 billion today, according to Wind Information

- The seven-day weighted average interbank repo rate for depository institutions (DR007) fell to 1.4937% at 09:34 am local time from the close of 1.5176% on Wednesday.

- The CFETS-NEX money-market sentiment index, measuring interbank money-market liquidity, closed at 48 on Wednesday, compared with the close of 46 on Tuesday. A higher reading points to tighter liquidity condition, with 50 representing an equilibrium.

MNI: PBOC Sets Yuan Parity Higher At 7.1494 Thurs; -0.49% Y/Y

MNI (BEIJING) - The People's Bank of China (PBOC) set the dollar-yuan central parity rate higher at 7.1494 on Thursday, compared with 7.1441 set on Wednesday. The fixing was estimated at 7.2065 by Bloomberg survey today.

MARKET DATA

AUSTRALIA Q2 RETAIL SALES VOLUMES +0.3% Q/Q; EST. 0.0%; Q1 +0.1%

AUSTRALIA JUNE RETAIL SALES VALUES +1.2% M/M; EST. 0.4%; MAY +0.5%

AUSTRALIA JUNE BUILDING APPROVALS +11.9% M/M; EST. 1.8%; MAY +2.2%

AUSTRALIA JUNE PRIVATE HOUSES -2.0% M/M; MAY -1.0%

AUSTRALIA JUNE PRIVATE CREDIT +0.6% M/M; EST. +0.5%; MAY +0.6%

AUSTRALIA JUNE PRIVATE CREDIT +6.8% Y/Y; MAY +6.9%

AUSTRALIA Q2 EXPORT PRICES -4.5% Q/Q; EST. -3.0%; Q1 +2.1%

AUSTRALIA Q2 IMPORT PRICES -0.8% Q/Q; EST. -0.4%; Q1 +3.3%

JAPAN JUNE P INDUSTRIAL OUTPUT +1.7% M/M; EST. -0.8%; MAY -0.1%

JAPAN JUNE P INDUSTRIAL OUTPUT +4.0% Y/Y; EST. 1.3%; MAY -2.4%

JAPAN JUNE RETAIL SALES +1.0% M/M; EST. 0.5%; MAY -0.6%

JAPAN JUNE RETAIL SALES +2.0% Y/Y; EST. 1.8%; MAY +1.9%

JAPAN JUNE DEPT, SUPERMARKET SALES -0.1% Y/Y; MAY +0.6%

SOUTH KOREA JUNE INDUSTRIAL OUTPUT S/ADJ +1.6% M/M; EST. +2.5%; MAY -3.3%

SOUTH KOREA JUNE INDUSTRIAL OUTPUT +1.6% Y/Y; EST. +2.6%; MAY -0.3%

SOUTH KOREA CYCLICAL LEAD INDEX CHANGE JUNE +0.2; MAY 0.0

CHINA JULY MANUFACTURING PMI 49.3; EST. 49.7; JUNE 49.7

CHINA JULY NON-MANUFACTURING PMI 50.1; EST. 50.2; JUNE 50.5

CHINA JULY COMPOSITE PMI 50.2; JUNE 50.7

MARKETS

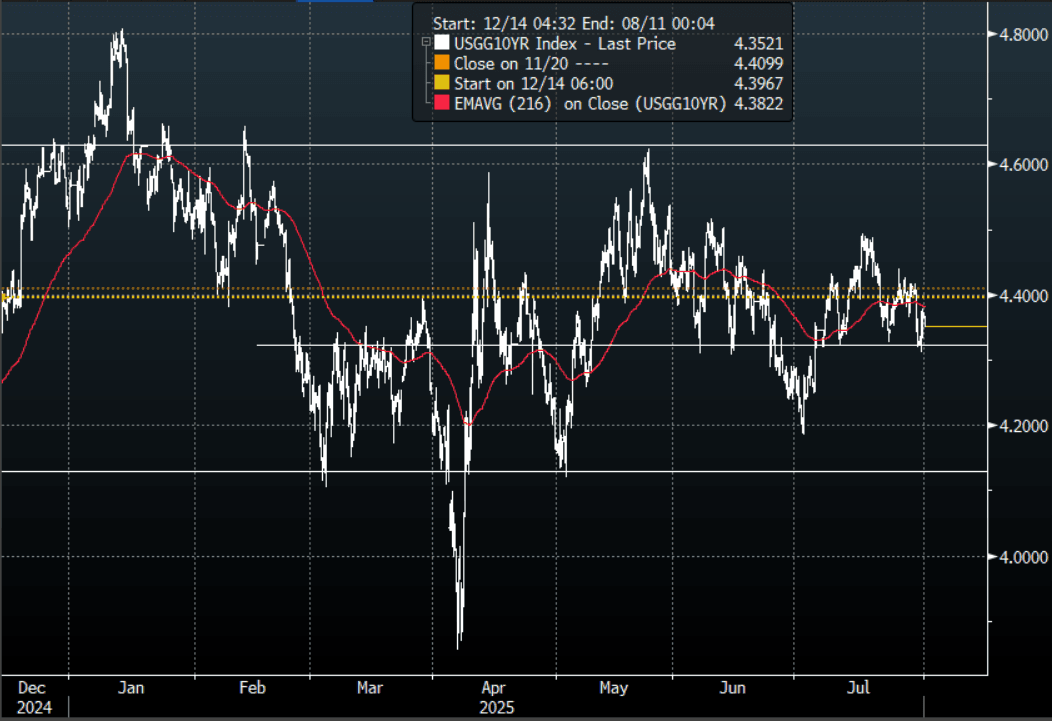

The TYU5 range has been 110-31 to 111-04+ during the Asia-Pacific session. It last changed hands at 111-03+, up 0-03 from the previous close.

- The US 2-year yield has shifted lower trading around 3.92.4%, down 0.01 from its close.

- The US 10-year yield has edged lower trading around 4.352%, down 0.01 from its close.

- The 10-year yield has again held the support around its pivot within the wider range 4.10% - 4.65%, decent supply was seen around the 4.30/35% area once more. This would need to clear above the 4.45% area to potentially regain upward momentum now.

- Nick Timiraos on X: ”September’s Fed decision hinges on data clarity. If the recent muddle persists, that “could make it very tough—if it’s not bad enough to make it a slam dunk to cut, and it is not good enough to declare victory,” says Rich Clarida.”

- “Powell gives the Heisman stiff-arm to any attempt to get pinned down on September. Responding to a leading hypothetical on what would generate a rate cut in September: "I'm not going to say that, no. We're just going to need to see the data. It could go in many different directions." "We're going to make a judgment based on all of the data and based on the balance-of-risks analysis."

- Data/Events: Challenger Job Cuts, Personal Income, PCE, ECI, Initial Jobless Claims, MNI Chicago PMI

Fig 1: 10-Year US Yield 120min Chart

Source: MNI - Market News/Bloomberg Finance L.P

JGBS: Bonds Unwind Initial Post-BoJ Cheapening, Lab Mkt Data Tomorrow

JGB futures are little changed, -2 compared to settlement levels, after reversing initial weakness seen after the release of the BoJ Policy Decision.

- The BoJ held rates steady at 0.50%, as widely expected. The decision by the board was also unanimous. The central bank nudged down the degree of uncertainty surrounding the outlook. It noted: "it remains highly uncertain how trade and other policies in each jurisdiction will evolve and how overseas economic activity and

prices will react to them." In the previous statement, these uncertainties were judged 'extremely' high. - On balance, the statement brings us marginally closer to a further rate hike, given the central bank's degree of uncertainty was slightly softened. Still, the BoJ seems unlikely to act in the near term (the next policy meeting is on Sep 19, followed by Oct 30). It has time to assess key macro trends and obtain greater clarity around the outlook (i.e. move away from high uncertainty around the trade/external outlook).

- Cash JGBs are little changed across benchmarks out to the 20-year and 1-2bps cheaper beyond. The benchmark 10-year yield is 0.1bp higher at 1.562% versus the cycle high of 1.616%.

- Swap rates are flat to 1bp lower.

- Tomorrow, the local calendar will see Jobless Rate and Job-To-Applicant Ratio data.

AUSSIE BONDS: Modestly Cheaper, Narrow Ranges Despite Upbeat Data

ACGBs (YM -4.5 & XM -2.5) remain weaker after trading in narrow ranges.

- Q2 retail sales volumes were stronger-than-expected, rising 0.3% q/q after 0.1%, the fourth consecutive rise bringing annual growth to 1.5%, the highest in almost three years. RBA Deputy Governor Hauser noted today that consumption growth has not recovered as expected, given the pickup in real disposable income growth and low unemployment.

- The number of building approvals rose sharply in June, driven by the volatile multi-dwelling component. They were up 11.9% m/m after a downwardly-revised +2.2% in May, with private houses down 2.0% m/m but non-houses jumped 33.1% m/m.

- Cash US tsys are ~2bps richer in today’s Asia-Pac session after yesterday’s post-FOMC sell-off.

- Cash ACGBs are 1-3bps cheaper with the AU-US 10-year yield differential at-8bps.

- The bills strip is weaker, with pricing -3 to -5.

- RBA-dated OIS pricing is firmer across meetings today. A 25bp rate cut in August is given a 97% probability, with a cumulative 60bps of easing priced by year-end (based on an effective cash rate of 3.84%).

- Tomorrow, the local calendar will see Cotality Home Values, S&P Global PMI Mfg and PPI data.

- The AOFM plans to sell A$1200mn of the 2.75% 21 June 2035 bond tomorrow.

BONDS: NZGBS: Closed Mid-Range But Outperformed US Tsys

NZGBs closed mid-range, with yields flat.

- After the negative post-FOMC lead-in from US tsys, NZGBs opened weaker but reversed direction as US tsys rallied ~2bps in today’s Asia-Pac session.

- NZGBs outperformed US tsys on the day, with the NZ-US 10-year yield differential 4bps lower at +16bps.

- Today’s weekly supply drew a powerful bid tone, with cover ratios of 3.72x (May-34) to 4.90x (May-30).

- “Housing and personal consumer lending from registered banks grew to NZ$381.59 billion in June from NZ$379.91 billion in the previous month. Such lending from non-bank lending institutions was broadly flat in the month at NZ$12.09 billion, compared with NZ$12.05 billion in the prior month.” (MTN via BBG)

- Swap rates closed 1-2bps higher, with the 2s10s curve marginally flatter.

- RBNZ dated OIS pricing closed little changed across meetings. 20bps of easing is priced for August, with a cumulative 34bps by November 2025.

- Tomorrow, the local calendar will see ANZ July consumer confidence and June building permits data.

FOREX: USD Gets A Boost From A Hawkish Powell

The BBDXY has had a range of 1217.30 - 1219.06 in the Asia-Pac session, it is currently trading around 1218, -0.05%. The USD’s slide lower finally stalled at the back end of last week and some profit-taking has been seen. Monday’s US-EU trade deal was seen as a big loss for the European Union and this has provided the USD bounce with further tailwinds. A hawkish tone from Powell has added to the USD’s tailwinds and to the shorts woes. A sustained move back above the 1220 area would begin to really pressure the shorts in the short-term, but offer better levels for the market to re-enter shorts possibly back towards the 1240/50 area. The market will now be looking towards NFP on Friday.

- EUR/USD - Asian range 1.1404 - 1.1438, Asia is currently trading 1.1425. The pair saw some heavy selling putting in a top towards 1.1800 for now. The price looked a little stretched in the short term, and with the USD making a recovery the EUR is set for a correction of sorts. It broke the first support around the 1.1550 area and is now testing the more important 1.1300/1.1400 area, where I would expect demand first up.

- GBP/USD - Asian range 1.3234 - 1.3263, Asia is currently dealing around 1.3260. This pair looks like it is now breaking lower indicating a deeper correction. Support seen now back towards 1.3100/1.3200 and look for supply now on bounces back towards 1.3500.

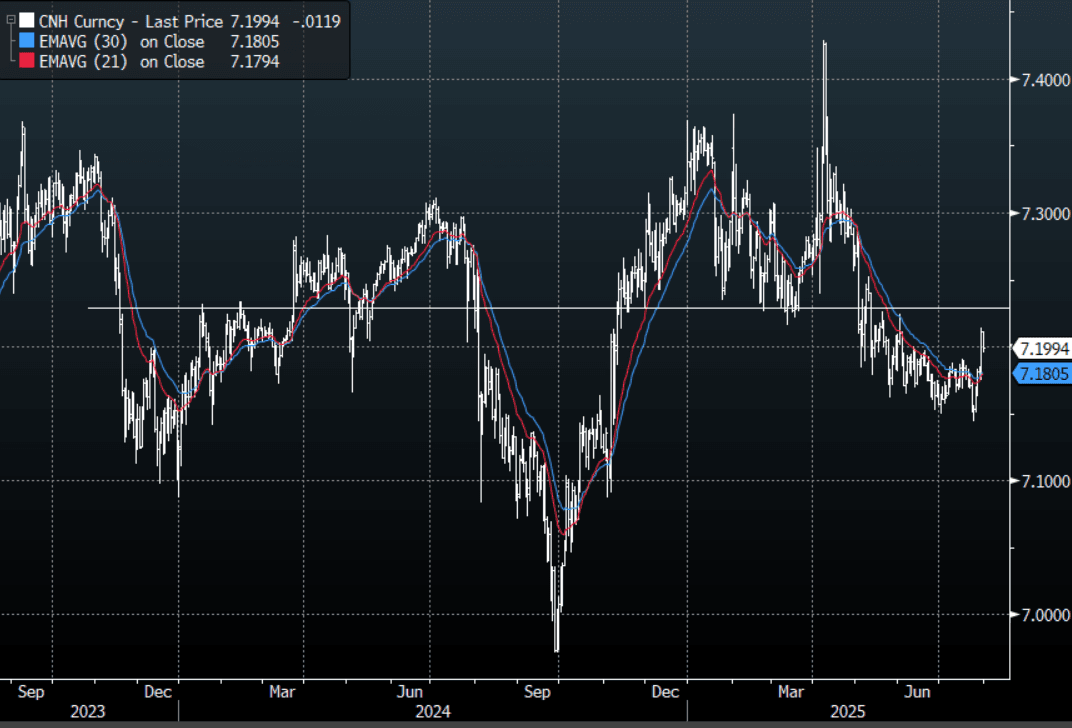

- USD/CNH - Asian range 7.1959 - 7.2113, the USD/CNY fix printed 7.1494, Asia is currently dealing around 7.2000. Sellers should be around on bounces while price holds below the 7.2200/2500 area and the PBOC manages the fix lower. Above 7.2500 and we could see a test of the USD Shorts.

- Cross asset : SPX +0.97%, Gold $3296, US 10-Year 4.354%, BBDXY 1217, Crude Oil $69.87

- Data/Events : Germany Import Prices/Unemployment & CPI, France CPI & PPI, Italy unemployment & CPI, EZ Unemployment

Fig 1: USD/CNH Spot Daily Chart

Source: MNI - Market News/Bloomberg Finance L.P

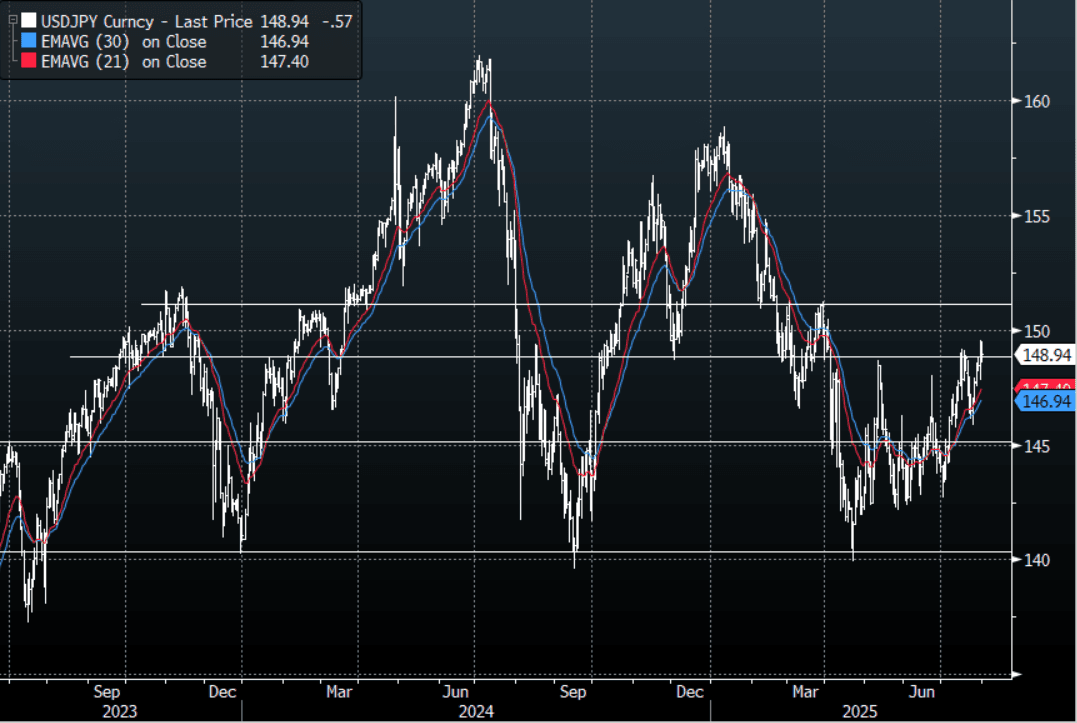

JPY: Asia Wrap - BOJ Raises Inflation Forecast To Help JPY

The Asia-Pac USD/JPY range has been 148.59 - 149.51, Asia is currently trading around 148.80, -0.45%. USD/JPY drifted lower into the BOJ and then took another leg as inflation forecasts were raised. The pair caught between a hawkish Powell and a hawkish BOJ. How the USD trades going into the NFP print tomorrow will probably dictate short-term moves. First support back towards 146/147 and on the topside the pivotal 151/152 area remains key.

- "BOJ Keeps rates unchanged, raises FY2025 inflation forecast to 2.7% from 2.2%" - BBG

- (Bloomberg) - “The BOJ’s hold decision looks at least as hawkish as the Fed’s, meaning that traders should start seriously considering September’s meeting as a live one for a Japanese rate hike.”

- JAPAN DATA Local Investors Sell Offshore Debt, But Recent Trends Still Positive: Offshore flows for Japan bond and equity markets were mixed last week. Local investors sold offshore bonds for the first time since early June. Since mid June we have had cumulative buying for this segment of over 5.6trln, including the modest outflow last week. Hence the trend still remains positive for Japan purchases of offshore debt. Local investors bought overseas equities for the second straight week, but the cumulative trend over recent months remains negative.

- Options : Close significant option expiries for NY cut, based on DTCC data: 146.00($971m).Upcoming Close Strikes : 147.00($1.52b Aug 1), 146.00($1.43b Aug 1) - BBG.

CFTC data shows Asset managers surprisingly added slightly to their JPY longs +72326( Last +71610), while leveraged funds have slightly reduced their newly built short JPY position -11571(Last -12606).

Fig 1 : USD/JPY Spot Daily Chart

Source: MNI - Market News/Bloomberg Finance L.P

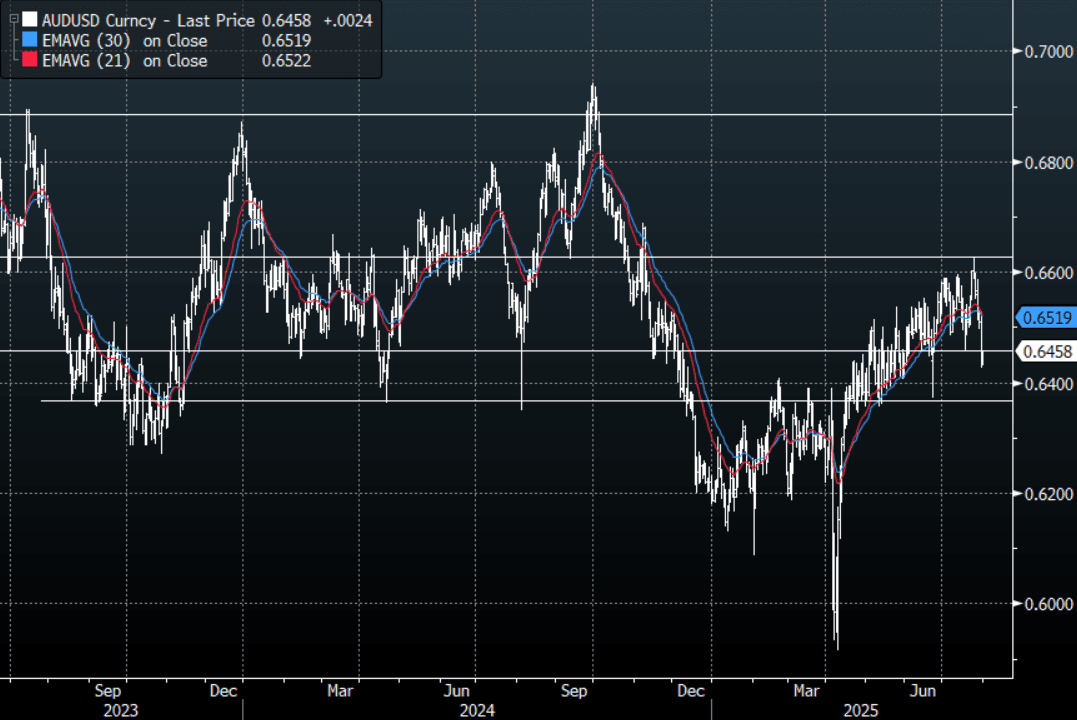

AUD: Asia Wrap - AUD/USD Gets A Boost From Retail and US Tech

The AUD/USD has had a range of 0.6433 - 0.6460 in the Asia- Pac session, it is currently trading around 0.6460, +0.40%. A stellar earning report from Metta and Microsoft saw US stocks surge back into the close. This morning has seen US futures take another leg higher as the market digests the late earnings reports as well a trade deal with South Korea, ESU5 +0.95%, NQU5 +1.35%. Upward momentum now looks to be clearly breaking down and the pivotal support back towards 0.6350 will now be key to hold the bears in check. A better retail print added to the tailwinds, lets see how far the AUD can bounce while stocks keep moving higher.

- AUSTRALIA DATA: Discounting Boosts Q2 Spending But Still Down Per Person. Q2 retail sales volumes were stronger-than-expected, rising 0.3% q/q after 0.1%, the fourth consecutive rise bringing annual growth to 1.5%, the highest in almost three years. RBA Deputy Governor Hauser noted today that consumption growth has not recovered as expected given the pickup in real disposable income growth and low unemployment. The ABS noted that per capita volumes fell again signalling that spending remains soft.

- AUSTRALIA: “Misery Index” Suggest Consumer Confidence Should Have Improved More. RBA Deputy Governor Hauser talked today about how consumer confidence has not improved as much as the “misery index”, combination of inflation and unemployment, implied. He wondered if this was due to a “scarring effect” from high inflation driving real disposable incomes lower in recent years, but noted that the RBA has been unable to model it suggesting that there may be “something special now compared with the past”

- Options : Closest significant option expiries for NY cut, based on DTCC data: 0.6600(AUD1.38b), 0.6500(AUD710m), 0.6465(AUD1.01b). Upcoming Close Strikes : 0.6600(AUD847m Aug 5), 0.6550(AUD831m Aug 5) - BBG

- AUD/JPY - Asia-Pac range 95.87 - 96.28, Asia is trading around 96.15. The pair could not hold above 97.00 on Monday and drifted lower overnight into the FOMC, but has not really bounced back as would be expected considering the move higher in stocks. The support between 95.00 - 96.00 held very well last week and the pair is looking to regain its momentum for a move higher but this price action does not look great. A close back below 95.00 would be problematic for bulls.

Fig 1: AUD/USD spot Daily Chart

Source: MNI - Market News/Bloomberg Finance L.P

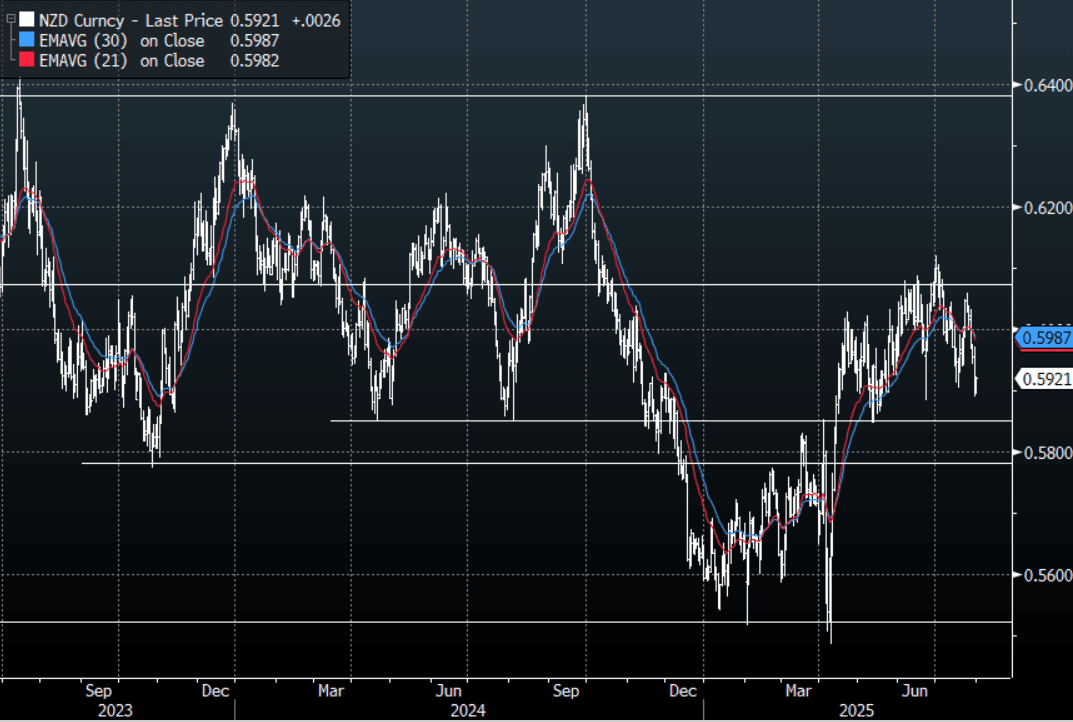

NZD: Asia Wrap - NZD/USD Gets Relief From US Tech Earnings

The NZD/USD had a range of 0.5894 - 0.5917 in the Asia-Pac session, going into the London open trading around 0.5915, +0.37%. The pair broke through 0.5950 and traded very poorly overnight with momentum lower being added by Powell’s hawkish tone. The support towards 0.5800/50 will now become pivotal, a sustained close back below there would start to look very bearish. Strong Tech Earnings has seen risk open better bid, this could provide the NZD/USD with some respite in our session to slow the recent slide, E-Minis +0.95%, NQU5 - +1.35%.

- Bloomberg - “Meta surged after a stronger-than-expected third-quarter revenue forecast signaled its core advertising business is still growing quickly enough to support aggressive AI spending. Microsoft also jumped as sales from its Azure cloud-computing unit grew 39%, faster than analysts anticipated.”

- CHINA Official PMIs Continue to Moderate: China's National PMIs continued to moderate in July. Ongoing weakness in domestic consumption and volatility in exports is exacerbating the concerns. Despite this, at China's Politburo on Wednesday, the nation's economic strength was saluted. That came after the country registered a record trade surplus in the first half of the year on soaring shipments to southeast Asia and stabilizing exports to the US.

- Options : Closest significant option expiries for NY cut, based on DTCC data: 0.5965(NZD504m). Upcoming Close Strikes : none. - BBG

- CFTC Data shows Asset Managers again reduced their newly built longs in NZD +5034(Last +8192), the Leveraged community added slightly to their shorts last week -7328(Last -6744).

AUD/NZD range for the session has been 1.0905 - 1.0924, currently trading 1.0915. The Cross continues to trade sideways as the pair tries to build some momentum to move higher.

Fig 1: NZD/USD Spot Daily Chart

Source: MNI - Market News/Bloomberg Finance L.P

ASIA STOCKS: Japan Outperforms, Softer Trends Elsewhere

Asian equities are mostly weaker, outside of Japan market gains. This comes despite a much better US futures backdrop, although this is largely focused on the tech side, following late positive earnings/outlook news from both Meta and Microsoft in the US on Wednesday. Nasdaq futures were last up +1.35%, while Eminis were around +0.95% higher.

- Japan markets are seeing the Topix up close to 0.80%, while the NKY 225 is around 0.90% higher. Some positive spillover from US futures moves may be in play, while earlier the BoJ held rates steady, as widely expected. The level of uncertainty surrounding the trade outlook was described as high, but this was down from the previous meeting's description of 'extremely high'.

- The Taiex is also tracking slightly firmer, last up around 0.25%. The Kospi is struggling though, down close to 0.45%. This comes despite a positive trade deal outcome, at least at face value, with the US, where the reciprocal tariff rate will be 15%.

- China and Hong Kong markets are both down a little over 1% at the lunch time break. In Wednesday US trade the Golden Dragon index continued to decline, down a further 1.82% (marking the fifth straight session decline). Earlier data showed slightly softer than expected official PMI reads for China in terms of July. Manufacturing remains in contraction territory.

- In South East Asia, markets are weaker, although losses are not beyond 1% at this stage. Thailand and Malaysia await tariff level announcements from the US. US President Trump has doubled down on criticism of Indian tariffs and their business with Russia. Benchmark Indian markets are off a little over 0.60%.

OIL: Crude Slightly Lower, Watching Developments Against Russian Crude Buyers

Oil prices are only slightly lower today holding onto the significant gains made this week in the face of US President Trump’s threats against Russia and those who buy its fossil fuels. WTI reached a high of $70.41/bbl early in the APAC session but has trended lower since to be down 0.2% to $69.87. Brent is 0.3% lower at $73.05/bbl after a peak of $73.53. The USD index is down 0.2%.

- More US trade deals have been announced with India to face 25% tariffs plus an unspecified “penalty” for buying Russian oil and weapons, Brazil 50% for policies that threaten US security, while South Korea’s will be 15% in line with Japan and the EU. President Trump said today that India’s 25% was too high and so that doesn’t seem the final rate.

- With India to currently be penalised for buying Russian oil, the market is nervous that US restrictions particularly on third parties could materially impact global supplies. OPEC meets on August 3 to decide its production target for September and while another increase is widely expected, it has limited capacity to make up for any loss of Russian output.

- The US also increased restrictions on Iran targeting the shipping network and companies of Hossein Shamkhani. The EU sanctioned his business interests last week. His vessels are said to transport goods and oil from Russia and Iran around the world.

- Later US June PCE spending/prices, July Challenger job cuts, Q2 employment cost index, jobless claims and MNI July Chicago PMI are released. Also, July France/Germany CPI and June euro area unemployment print.

Gold Higher Today With Attention On US Data & Trade Deals

After falling 1.6% on Wednesday, gold is up 0.7% to $3296.7/oz today as it finds support from two FOMC members voting for a July rate cut and some punitive trade measures from the US against India and Brazil. It reached a high of $3298.61 earlier. US Treasury yields and the US dollar are lower today (BBDXY USD -0.1%) which will also be supporting the rally in bullion.

- More US trade deals have been announced with India to face 25% tariffs plus an unspecified “penalty” for buying Russian oil and weapons, Brazil 50% for policies that threaten US security, while South Korea’s will be 15% in line with Japan and the EU. President Trump said today that India’s 25% was too high and so that doesn’t seem the final rate.

- Trade deals will continue to be a focus with the clear possibility that negotiations will continue past the August 1 deadline. Today’s US PCE prices and Friday’s July payrolls will also be monitored closely.

- Silver is up 0.3% to $37.24, close to the intraday high which followed a low of $36.979.

- Equities are mixed with the S&P e-mini up 0.9% and Nikkei +0.9% but Hang Seng down 1.1% and KOSPI -0.7%. Oil prices are down with WTI -0.2% to $69.89/bbl. Copper has continued sinking and is -20.5%.

- Later US June PCE spending/prices, July Challenger job cuts, Q2 employment cost index, jobless claims and MNI July Chicago PMI are released. Also, July France/Germany CPI and June euro area unemployment print.

UP TODAY (TIMES GMT/LOCAL)

| Date | GMT/Local | Impact | Country | Event |

| 31/07/2025 | 0600/0800 | ** | Import/Export Prices | |

| 31/07/2025 | 0630/0830 | ** | Retail Sales | |

| 31/07/2025 | 0645/0845 | *** | HICP (p) | |

| 31/07/2025 | 0645/0845 | ** | PPI | |

| 31/07/2025 | 0755/0955 | ** | Unemployment | |

| 31/07/2025 | 0800/1000 | *** | Bavaria CPI | |

| 31/07/2025 | 0800/1000 | *** | North Rhine Westphalia CPI | |

| 31/07/2025 | 0800/1000 | *** | Baden Wuerttemberg CPI | |

| 31/07/2025 | 0900/1100 | ** | Unemployment | |

| 31/07/2025 | 0900/1100 | *** | HICP (p) | |

| 31/07/2025 | 1000/1200 | ** | PPI | |

| 31/07/2025 | 1200/1400 | *** | HICP (p) | |

| 31/07/2025 | 1230/0830 | *** | Jobless Claims | |

| 31/07/2025 | 1230/0830 | ** | WASDE Weekly Import/Export | |

| 31/07/2025 | 1230/0830 | * | Payroll employment | |

| 31/07/2025 | 1230/0830 | *** | Personal Income and Consumption | |

| 31/07/2025 | 1230/0830 | *** | Employment Cost Index | |

| 31/07/2025 | 1230/0830 | *** | Gross Domestic Product by Industry | |

| 31/07/2025 | 1342/0942 | *** | MNI Chicago PMI | |

| 31/07/2025 | 1430/1030 | ** | Natural Gas Stocks | |

| 31/07/2025 | 1530/1130 | ** | US Bill 04 Week Treasury Auction Result | |

| 31/07/2025 | 1530/1130 | * | US Bill 08 Week Treasury Auction Result | |

| 01/08/2025 | 2300/0900 | ** | S&P Global Manufacturing PMI (f) | |

| 01/08/2025 | 2330/0830 | * | Labor Force Survey | |

| 01/08/2025 | 0030/0930 | ** | S&P Global Final Japan Manufacturing PMI | |

| 01/08/2025 | 0130/1130 | * | Producer price index q/q | |

| 01/08/2025 | 0145/0945 | ** | S&P Global Final China Manufacturing PMI | |

| 01/08/2025 | 0715/0915 | ** | S&P Global Manufacturing PMI (f) | |

| 01/08/2025 | 0745/0945 | ** | S&P Global Manufacturing PMI (f) | |

| 01/08/2025 | 0750/0950 | ** | S&P Global Manufacturing PMI (f) | |

| 01/08/2025 | 0755/0955 | ** | S&P Global Manufacturing PMI (f) | |

| 01/08/2025 | 0800/1000 | * | Retail Sales | |

| 01/08/2025 | 0800/1000 | ** | S&P Global Manufacturing PMI (f) | |

| 01/08/2025 | 0830/0930 | ** | S&P Global Manufacturing PMI (Final) | |

| 01/08/2025 | 0900/1100 | *** | HICP (p) | |

| 01/08/2025 | - | *** | Domestic-Made Vehicle Sales | |

| 01/08/2025 | 1230/0830 | *** | Employment Report | |

| 01/08/2025 | 1345/0945 | *** | S&P Global Manufacturing Index (final) |