MNI: RBA To Cut In August, Jobs Market To Guide Further Easing

The Reserve Bank of Australia is likely to cut the cash rate by 25 basis points to 3.6% at its August meeting, though further easing will depend on the performance of the labour market as officials cautiously edge toward a neutral stance, former RBA staffers told MNI.

While the RBA has focused heavily on inflation, the lower-than-expected Q2 trimmed mean reading of 2.7% likely opened the door to an August cut, said Blair Chapman, senior economist at Seek and former RBA research economist.

However, Chapman noted that the trajectory beyond August would be guided by labour market data, with the current cash rate not far above neutral. “It’s whether they think they need to go from restrictive to expansionary,” he said, highlighting the Reserve’s estimated non-accelerating inflation rate of unemployment (NAIRU) of 4.5% as a benchmark for gauging slack in the labour market.

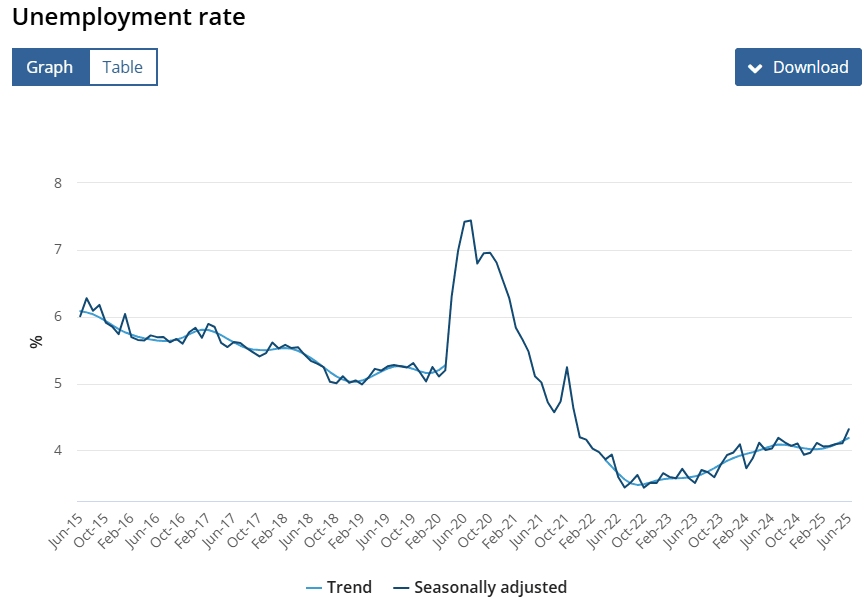

June’s unemployment rate rose 20bp to 4.3%, prompting markets to aggressively price in a cut at the Aug 11–12 meeting. Following Wednesday’s inflation data, traders fully priced in a 25bp cut, with expectations that the rate will fall to 3% by February.

However, Chapman flagged uncertainty around that path, pointing to Governor Michele Bullock’s recent warnings about wage-price pressures. “The Bank will continue to act patiently and watch for further deterioration in the labour market to really lock in further cuts,” Chapman said. “Although market pricing and their forecasts mean that there is another one or two to come.”

James Morley, professor of macroeconomics at the University of Sydney, said the RBA would look beyond the headline unemployment rate, weighing broader indicators to assess labour market strength. Referring to Bullock’s recent speech, he said the Reserve likely still views conditions as relatively tight.

“That would be a reason not to cut as much,” Morley said. “But if the labour market indicators do get worse, which I suspect they will, then they would no longer be thinking about feeling their way to neutral – they might have to think about actually cutting beyond neutral. The gradualism is probably less about exactly what the level of neutral is; it’s more about uncertainty.”

Sean Langcake, head of macroeconomic forecasting at Oxford Economics Australia and a former RBA economist, said the Bank would closely monitor soft indicators such as business confidence in the coming months to assess the domestic impact of global trade tensions. Langcake expects the Board to cut in August and again in November, and sees the neutral rate at about 3.25%.

“Another two cuts this year makes sense,” he said. “It’s not aggressive, but it is kind of stepping into the breach a little bit.” Should unemployment rise sharply toward 5%, the RBA could cut twice in Q4, though Langcake cautioned that uncertainty around the labour market signal would keep the Bank cautious in its approach.

JULY PAUSE

Morley said the RBA’s decision to hold in July, surprising markets, allowed Governor Bullock to reinforce the importance of the quarterly CPI over the monthly indicator, and signal the Bank would not be pressured by market expectations. (See MNI RBA WATCH: Board Shocks With Hold As Trade Fears Ease)

However, he argued that based on domestic data and broad Board agreement on the rate direction, the Bank should have moved in July. “I don't think the old line of ‘keeping your powder dry’ made sense,” he said, adding that uncertainty about the global outlook and the RBA’s natural tendency toward caution likely motivated the pause, along with a view that worst-case scenarios had been avoided.

While the RBA published its voting breakdown for the first time in July, Morley noted that the Governor’s view would continue to carry significant weight, despite the potential for more visible dissent.