MNI EUROPEAN OPEN: Bessent Comments Weigh On USD/JPY

EXECUTIVE SUMMARY

- FED’S GOOLSBEE SAYS FALL FOMC MEETINGS ARE ‘LIVE’ - MNI BRIEF

- BOSTIC SAYS WEAKER JOBS COULD MEAN LESS PATIENT FED - MNI BRIEF

- BESSENT SAYS BOJ IS FALLING BEHIND THE CURVE, EXPECTS HIKE - BBG

- CHINA PORK PRICES DOWN 1.4%M/M AT THE START OF AUGUST - MNI BRIEF

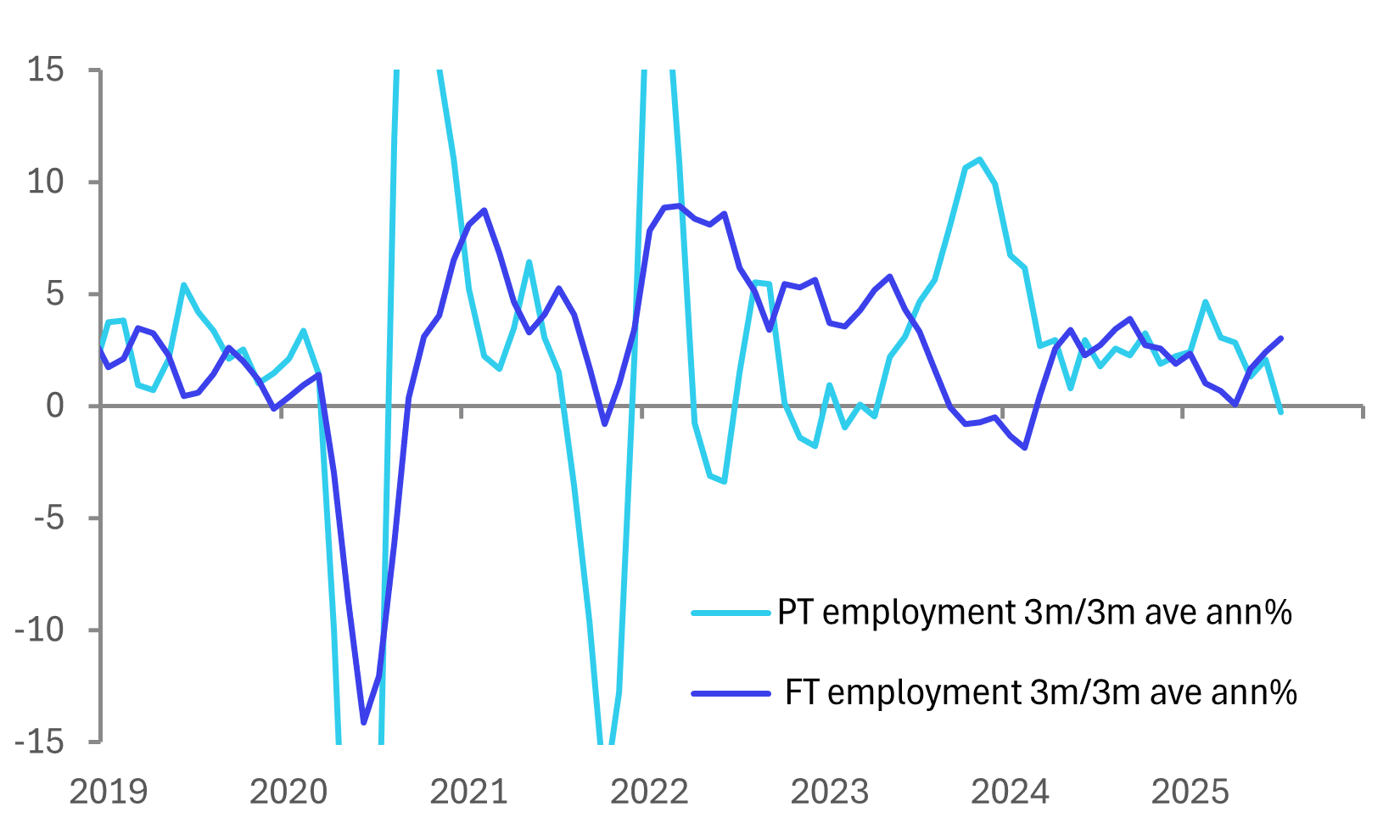

- AUSSIE UNEMPLOYMENT DOWN 10BP TO 4.2% - MNI BRIEF

- FORMER RBNZ STAFFER ON NEXT WEEK'S MPC MEETING - MNI

Fig 1: Australia employment 3-month momentum %

UK

UKRAINE (BBC): “There is a "viable chance" of a ceasefire between Russia and Ukraine, Prime Minister Sir Keir Starmer has said, ahead of Friday's summit between US President Donald Trump and Russian President Vladimir Putin.”

HOUSE PRICES (BBG): "UK July RICS House Price Index at -13 vs Est. -5"

EU

US/RUSSIA (BBG): “US President Donald Trump warned he would impose “very severe consequences” if Vladimir Putin didn’t agree to a ceasefire agreement later this week, following a call with European leaders ahead of his meeting with the Russian president.”

UKRAINE (BBC): “Trump reportedly told the Europeans that his goal for the summit was to obtain a ceasefire between Moscow and Kyiv. He also agreed that any territorial issues had to be decided with Volodymyr Zelensky's involvement, and that security guarantees had to be part of the deal, according to France's Emmanuel Macron.”

UKRAINE (EURACTIV): “Kyiv is willing to discuss territorial issues with Russia, amid new “hope for movement" towards peace in Ukraine, German Chancellor Friedrich Merz said on Wednesday.”

NETHERLANDS (EURACTIV): “The Netherlands’ competition regulator will meet 12 major online platforms — including TikTok, Facebook and X — on 15 September to discuss disinformation in the run-up to the 29 October elections.”

US

FED (MNI): Federal Reserve Bank of Chicago President Austan Goolsbee said Wednesday he is looking for further signs that tariffs' impact on prices will stay limited before lowering interest rates, adding the U.S. economy is not on the brink of recession.

FED (MNI BRIEF): A persistently weaker-than-expected job market could mean the Federal Reserve might face greater urgency to cut interest rates than it previously thought, Atlanta Fed President Raphael Bostic said Wednesday, following a soft July jobs number and large downward revisions for May and June.

FED (MNI BRIEF): The fall FOMC meetings are "live" as Federal Reserve officials debate whether inflation is headed down or if tariff effects will keep price pressures persistently high, Chicago Fed President Austan Goolsbee said Wednesday.

TARIFFS (RTRS): The announcement by President Donald Trump's administration of the results of a probe into pharmaceutical imports and new sector-specific U.S. tariffs likely remains weeks away, four official and industry sources said, later than initially promised as he focuses on other matters.

OTHER

JAPAN (BBG): “US Treasury Secretary Scott Bessent said the Bank of Japan is falling behind the curve in addressing inflation, in a rare comment admonishing policy decisions by a foreign central bank.”

AUSTRALIA (MNI BRIEF): The unemployment rate fell 10 basis points to 4.2% in July, matching expectations, as the economy added 24,500 jobs, Australian Bureau of Statistics data showed Thursday.

NEW ZEALAND (MNI): A former RBNZ staffer offers his view on next week's MPC meeting.

CHINA

CREDIT (FINANCIAL NEWS): “Observers should not over-speculate on fluctuations in monthly credit growth readings, PBOC-backed Financial News says in a commentary following the release of China’s July credit data.”

LOAN RATES (CSJ): “Chinese consumers with the highest credit are expected to obtain loans with interest rates below 3% after the country’s newly announced subsidy program is formally implemented, China Securities Journal reports Thursday citing a member of the consumer loans business at a branch of China Construction Bank.”

CAPITAL FLOWS (SECURITIES DAILY): “Foreign capital allocation to domestic yuan bonds has accelerated again since the second half of 2024, driven by increasing preference for non-U.S. dollar assets and the attractiveness of the Chinese bond market’s lower correlation with other developed countries, Securities Daily reported citing analysts.”

PRICES (MNI BRIEF): China's pork prices, an important component in the nation’s CPI measure, fell 1.4% m/m during the first 10 days of August, data from the National Bureau of Statistics showed on Thursday.

MNI: PBOC Net Drains CNY32 Bln via OMO Thursday

MNI (BEIJING) - The People's Bank of China (PBOC) conducted CNY128.7 billion via 7-day reverse repos, with the rate unchanged at 1.40%. The operation led to a net drain of CNY32 billion after offsetting maturities of CNY160.7 billion today, according to Wind Information.

- The seven-day weighted average interbank repo rate for depository institutions (DR007) fell to 1.4065% at 09:37 am local time from the close of 1.4522% on Wednesday.

- The CFETS-NEX money-market sentiment index, measuring interbank money-market liquidity, closed at 48 on Wednesday, compared with the close of 47 on Tuesday. A higher reading points to tighter liquidity condition, with 50 representing an equilibrium.

MNI: PBOC Sets Yuan Parity Lower At 7.1337 Thurs; -0.47% Y/Y

MNI (BEIJING) - The People's Bank of China (PBOC) set the dollar-yuan central parity rate lower at 7.1337 on Thursday, compared with 7.1350 set on Wednesday. The fixing was estimated at 7.1753 by Bloomberg survey today.

MARKET DATA

UK JULY RICS HOUSE PRICE BALANCE -13; EST. -5; JUNE -7

AUSTRALIA JULY EMPLOYMENT +24.5K M/M; EST. 25K; JUNE +1K

AUSTRALIA JULY FULL-TIME EMPLOYMENT +60.5K M/M; JUNE -36.6K

AUSTRALIA JULY PART-TIME EMPLOYMENT -35.9K M/M; JUNE +37.6K

AUSTRALIA JULY JOBLESS RATE 4.2%; EST. 4.2%; JUNE 4.3%

AUSTRALIA JULY PARTICIPATION RATE 67.0%; EST. 67.1%; JUNE 67.0%

MARKETS

US TSYS: Asia Wrap - Yields Relatively Unchanged In A Quiet Session

The TYU5 range has been 112-05 to 112-09 during the Asia-Pacific session. It last changed hands at 112-07, up 0-01+ from the previous close.

- The US 2-year yield is trading around 3.672%.

- The US 10-year yield is trading around 4.232%.

- Good demand towards the 10-Year 4.30/35%% pivot saw yields move lower. That area should continue to see demand cap yields, longs will be looking to target the 4.10% area initially.

- "A block of 4,000 contracts in five-year bond September futures traded at a price of 109-02 1/4 on CBOT. A total of 44,981 contracts traded so far in this session." - BBG

- Liz Ann Sonders on X: “Supercore CPI increased by 0.48% m/m in July … one of largest gains this year and a break from prior months’ tame prints.” See Fig.1 Below

- Ben Hunt on X: “They’re gonna run it hot like you can’t even believe.”

- Paulo Macro on X: “Hard to believe Powell is gonna talk up Sept rate cuts at Jackson Hole next week after that core print yesterday but I guess the music is still playing and they wanna dance right up until until the record scratch.”

- Data/Events: PPI, Initial Jobless Claims

Fig 1: Supercore CPI

Source: MNI - Market News/Bloomberg Finance L.P/@LizAnnSonders

JGBS: Sharp Bear Flattener, Q2 GDP Tomorrow

JGB futures are sharply weaker and near session lows, -39 compared to settlement levels.

- “Rakuten Bank, the online banking arm of Rakuten Group, will refrain from actively buying Japanese government bonds (JGBs), Bloomberg News reported on Thursday, citing a top official. CEO Tomotaka Tori said the group will hold its purchase until the Bank of Japan implements further interest rate hikes, citing market volatility and policy uncertainty.” (MTN via BBG)

- "They're behind the curve," Bessent told Bloomberg TV on Wednesday, noting that he discussed Japan's inflation problem with BOJ Governor Kazuo Ueda. "So they're going to be hiking and they need to get their inflation problem under control," he added." BBG

- JGBs are showing a bear-flattener across benchmarks, with yields flat to 5bps higher. The benchmark 5-year yield is 4.2bps higher at 1.106% after yesterday's poor auction.

- Swap rates are 3-5bps higher.

- Tomorrow, the local calendar will see Q2 GDP(P), IP(F), Capacity Utilisation and Weekly International Investment Flow data.

AUSSIE BONDS: Slightly Cheaper After Jobs Report

ACGBs (YM +1.5 & XM +1.0) are slightly weaker after today’s Employment Report.

- The July labour market data printed in line with consensus but also showed some normalisation in key data after June’s deterioration. There was also a clear trend to more full-time jobs and hours signalling that demand was robust in the month. While “labour market conditions remain a little tight”, as the RBA said in its August statement, they didn’t appear to ease further in July.

- The unemployment rate dropped 0.1pp to 4.2%. The RBA expects it to peak at 4.3% in H2 and then remain there.

- Cash US tsys are slightly richer in today's Asia-Pac session after yesterday's solid rally.

- Cash ACGBs are 1-2bps richer with the AU-US 10-year yield differential at -3bps.

- The bills strip is -1 to +2, with a flattening bias.

- RBA-dated OIS pricing is 2-4bps firmer across meetings after the data release. A 25bp rate cut in September is given a 31% probability, with a cumulative 38bps of easing priced by year-end (based on an effective cash rate of 3.59%).

- Tomorrow, the local calendar will be empty apart from the AOFM planned sale of A$1000mn of the 2.75% 2 1 November 2029 bond.

BONDS: NZGBS: Slight Bull-Steepener On A Data-Light Day

NZGBs closed 1-2bps richer, with the 2/10 curve steeper, on a data-light day.

- The local market did underperform in the $-bloc, with the NZ-US and NZ-AU 10-year yield differentials 5bps and 2bps wider, respectively.

- “New Zealand households' perception of current inflation for the September quarter rose to a mean of 8.1% from 6.9% in the June quarter, but was slightly down from 8.2% a year earlier.” (MTN via BBG)

- Today’s supply saw good demand, with cover ratios ranging from 3.15x (Apr-37) to 4.95x (Apr-29).

- Cash US tsys are slightly richer in today's Asia-Pac session after yesterday's solid rally. Thursday's US data includes weekly jobless claims and PPI, eyed for both price pressures in their own right and helping hone July PCE estimates (after the CPI data, MNI's survey of estimates points to 0.25% M/M for core PCE). Fed speakers include Musalem and Barkin.

- Swap rates closed 1bp lower.

- RBNZ dated OIS pricing closed slightly softer across meetings. 23bps of easing is priced for August, with a cumulative 42bps by November 2025.

- Tomorrow, the local calendar will see the July BNZ manufacturing PMI Index, Net Migration and July monthly price series.

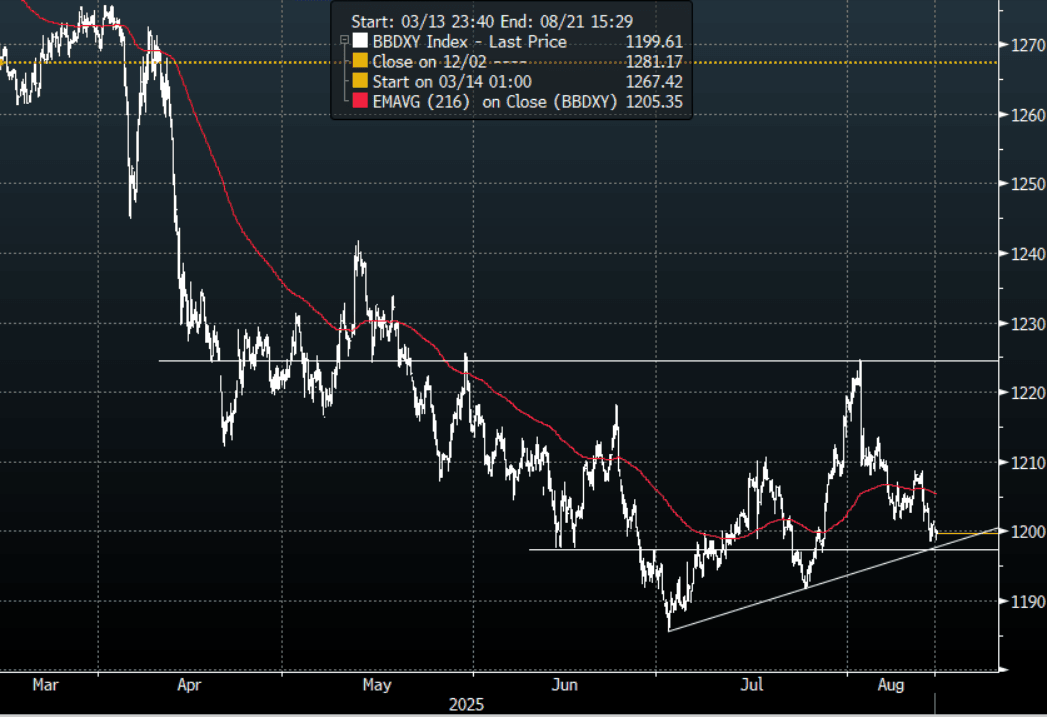

FOREX: Asia FX Wrap - BBDXY Is Probing Below 1200

The BBDXY has had a range of 1198.65 - 1200.56 in the Asia-Pac session, it is currently trading around 1199, -0.12%. The USD had another leg lower but found some demand again towards its support just below 1200. This is clearly the side the market is more comfortable trading and a sustained break below 1197/1195 could see the move lower regain momentum and a retest of the year's lows.

- EUR/USD - Asian range 1.1699 - 1.1715, Asia is currently trading 1.1705. The market moved very quickly back to 1.1700 where it stalled on its first attempt to challenge this area. Will this second attempt have the impetus to break through.

- GBP/USD - Asian range 1.3571 - 1.3592, Asia is currently dealing around 1.3575. The pair bounced nicely off the 1.3100/1.3200 support area. GBP extended above 1.3500 overnight and should continue to find support on dips while the USD remains under pressure. First support seen now back towards 1.3450.

- USD/CNH - Asian range 7.1681-7.1817, the USD/CNY fix printed 7.1337, Asia is currently dealing around 7.1740. Sellers should be around on bounces while price holds below the 7.2200/2500 area and the PBOC manages the fix lower. Above 7.2500 and we could see a test of the USD Shorts.

- Cross asset : SPX -0.05%, Gold $3360, US 10-Year 4.235%, BBDXY 1199, Crude Oil $62.90

- Data/Events : France CPI, Ital General Government Debt, EZ Industrial Production/Employment

Fig 1: BBDXY 2H Chart

Source: MNI - Market News/Bloomberg Finance L.P

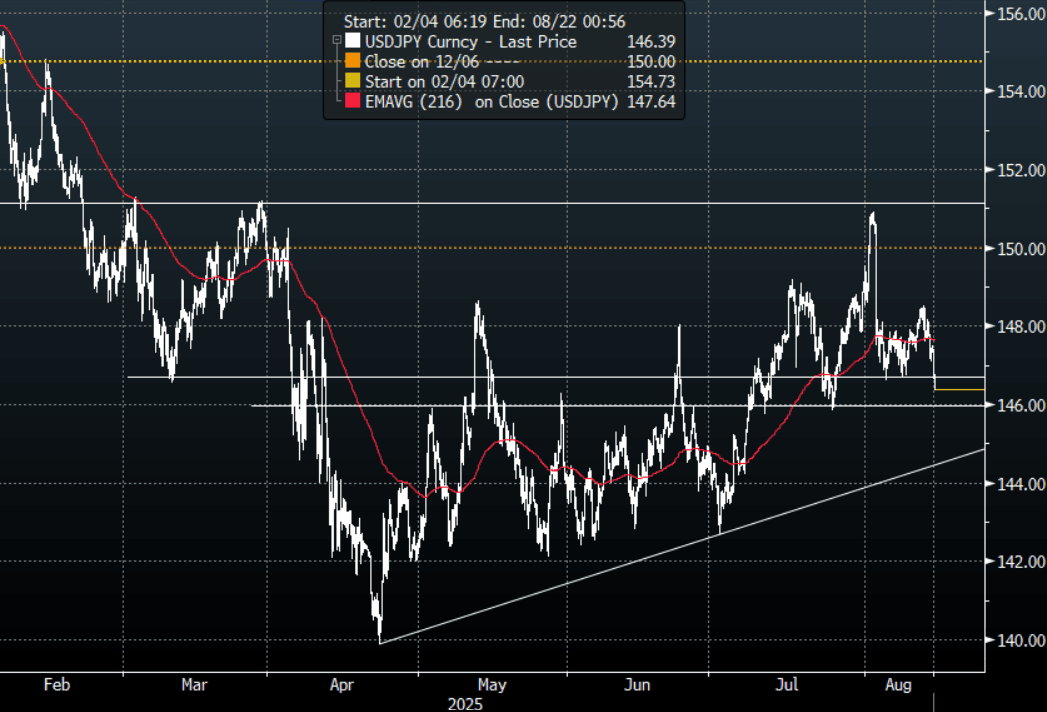

JPY: Asia Wrap - USD/JPY Breaks Below 147.00 On Bessent Comments

The Asia-Pac USD/JPY range has been 146.38-147.42, Asia is currently trading around 146.40, -0.68%. USD/JPY traded heavy for most of the overnight session eventually finding some demand back toward the 147.00 area. Comments from Scott Bessent in a Bloomberg interview then gave it the nudge it needed to break through this demand and extend lower. Price is currently probing the support area between 146.00/147.00, a sustained move below this support is needed to turn the momentum potentially lower again.

- “They’re behind the curve,” Bessent told Bloomberg TV on Wednesday, noting that he discussed Japan’s inflation problem with BOJ Governor Kazuo Ueda. “So they’re going to be hiking and they need to get their inflation problem under control,” he added." BBG

- "Hideo Kumano, executive economist at Dai-Ichi Life Research Institute, said "Bessent may be trying to weaken the dollar through his comments on US and Japanese monetary policy," and that by commenting on another country's policy, "he's breaking the rules."

- The most notable underperformer in Asian stocks today are the Japan benchmark indices, with the Topix and the NKY 225 off a little over 1%.

- Options : Close significant option expiries for NY cut, based on DTCC data: 145.00($1.01b), 149.00($1.15b).Upcoming Close Strikes : 145.00($920m Aug 15), 150.00($685m Aug 15), 150.00($846m Aug 19) - BBG.

- CFTC data shows asset managers reduced their JPY longs +60532( Last +75119), leveraged funds slightly reduced their newly built short JPY position -29308(Last -31280).

Fig 1 : USD/JPY Spot 2H Chart

Source: MNI - Market News/Bloomberg Finance L.P

AUD: Asia Wrap - AUD/USD Tries Higher On Employment, No Follow Through

The AUD/USD has had a range of 0.6543 - 0.6569 in the Asia- Pac session, it is currently trading around 0.6550, +0.10%. US equities continue to grind higher making new all-time highs. The more US cuts get priced in, the more pressure it puts on an already bearish USD market. I felt the bounce back towards 0.6550 offered a good risk/reward to fade initially but if the US starts pricing in more aggressive cuts can the AUD ignore it? The Price remains firmly in the 0.6350-0.6650 range, a sustained break back above 0.6650 is needed to potentially regain upward momentum. The AUD attempted to move higher on the employment data but could not hold onto those gains and has quickly settled back to where it started prior to the print.

- AUSTRALIA DATA: July Sees Some Normalisation In Labour Indicators. The July labour market data printed in line with consensus but also showed some normalisation in key data after June’s deterioration. There was also a clear trend to more full-time jobs and hours signalling that demand was robust in the month. While “labour market conditions remain a little tight”, as the RBA said in its August statement, they didn’t appear to ease further in July.

- CBA Expects One More Cut As More Optimistic On Growth. The RBA unanimously cut rates 25bp to 3.6% on Tuesday as was widely expected bringing total easing this cycle to 75bp. CBA expects one more rate cut in November and notes that its growth forecasts are more optimistic than the RBA’s. However, the risks are skewed that there will be more in 2026 depending on the data.

- Options : Closest significant option expiries for NY cut, based on DTCC data: 0.6600(AUD1.33bm), 0.6690(AUD583m). Upcoming Close Strikes : 0.6523(AUD562m Aug 15), 0.6515(AUD673m Aug 19) - BBG

- CFTC Data shows Asset managers added to their shorts -60729(Last -49183), the Leveraged community added very slightly to their own shorts -13997(Last -13823).

- AUD/JPY - Asia-Pac range 95.96 - 96.51, Asia is trading around 96.00. The pair has bounced and tested its first resistance around the 96.50/97.00 area where momentum stalled. The sellers have capped the move for now, price is firmly back into the 94.50-97.50 range.

Fig 1: AUD/JPY spot Daily Chart

Source: MNI - Market News/Bloomberg Finance L.P

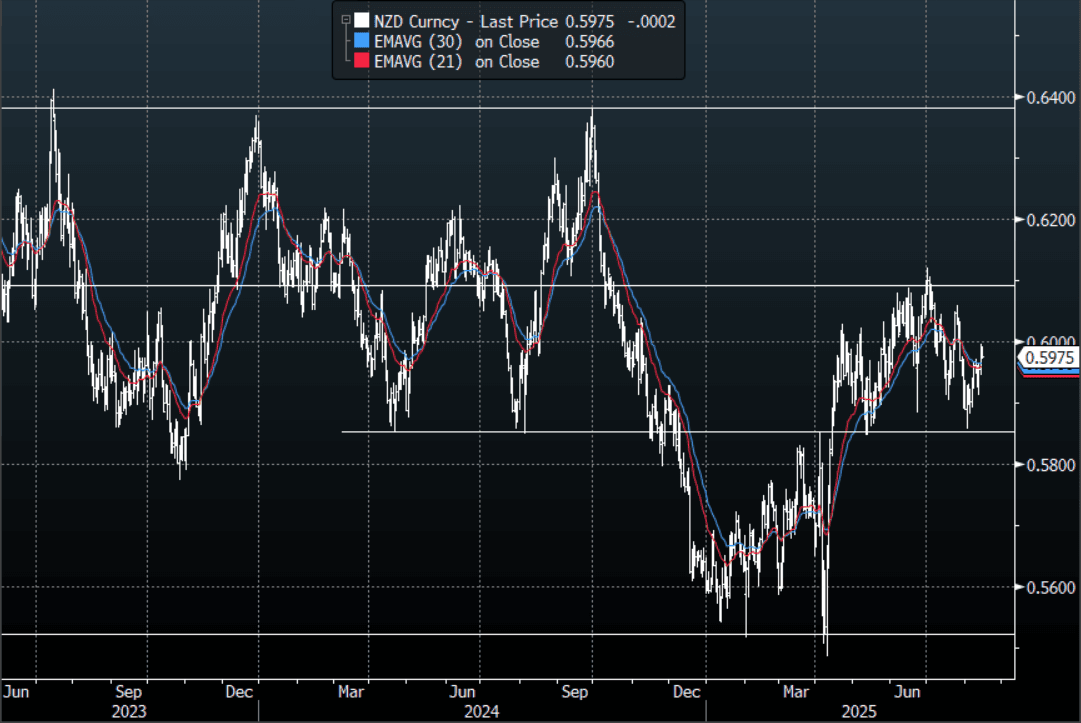

NZD: Asia Wrap - NZD/USD Drifting On A 0.59 Handle

The NZD/USD had a range of 0.5972 - 0.5991 in the Asia-Pac session, going into the London open trading around 0.5980, +0.04%. US equities continue to grind higher making new all-time highs. The more US cuts get priced in, the more pressure it puts on an already bearish USD market. Risk has opened a little lower this morning, E-minis -0.10%, NQU5 -0.10%. The NZD/USD is still firmly within its 0.5850-0.6150 range, the USD will need to break lower to test the top-end.

- "NZ Mean Household 2-Year Inflation Expectation 4.6%: RBNZ Survey. RBNZ publishes 3q Tara-ā-Whare Household expectations survey results, on website. Mean expected inflation in two years is 4.6% down from 4.7% in 2q. Median expected inflation rate in two years is 3%. Unchanged for sixth straight quarter.Mean expected inflation in one year is 6% up from 5.6% in 2q" - BBG

- Options : Closest significant option expiries for NY cut, based on DTCC data: 0.6000(NZD340m), 0.5825(NZD300m). Upcoming Close Strikes : 0.5500(NZD300m Aug 19). - BBG

- CFTC Data shows Asset Managers have cut their longs completely and started to rebuild a short in the NZD -1811(Last +3903), the Leveraged community added to their shorts slightly -6778(Last -6250).

- AUD/NZD range for the session has been 1.0943 - 1.0970, currently trading 1.0955. The Cross continues to trade sideways after stalling towards the 1.1000 area once more. The range looks to be 1.0850-1.1000 for now.

Fig 1: NZD/USD Spot Daily Chart

Source: MNI - Market News/Bloomberg Finance L.P

ASIA STOCKS: Japan Weighed By Stronger Yen, Australia & Indonesia Outperform

Asian stock markets are showing mixed trends in Thursday trade. The most notable underperformer is Japan benchmark indices, with the Topix and the NKY 225 off over 1%. Trends elsewhere are mixed, with aggregate moves under 1% at this stage. In terms of US futures we sit a little weaker, but trends have been relatively steady so far today

- A stronger yen (USD/JPY is down sub 146.50, +0.65% in yen terms) in the aftermath of comments from US Tsy Secretary that the BoJ is behind the curve in addressing inflation, is a headwind for Japan stocks. The Topix transportation index is down close to 1.85%, so slightly underperforming the headline index. This index is often sensitive to exchange rate shifts.

- Australia's ASX 200 is up around 0.55%, outperforming at the margins. Earlier jobs data painted a resilient backdrop, particularly in terms of the surge in full time jobs growth and the slight dip in the unemployment rate.

- South Korea's Kospi is down around 0.20%, HSBC downgraded local stocks to underweight (from neutral) citing valuations in certain sectors (per BBG). Some concerns around potential tax changes reportedly being considered by the government has been a headwind for stocks of late. Taiwan's Taiex is off around 0.40% at this stage, after closing near record highs yesterday.

- In China and Hong Kong, markets are mixed. Hong Kong was higher earlier, but is now down a touch, while the CSI 300 is up a little over 0.50%, last close to 4200.

- In South East Asia, Singapore is down around 0.4%, while Malaysia and Thailand are also down modestly. Indonesia is up, last +0.80%, to put the JCI at fresh record highs. Offshore inflows have returned of late, while a tailwind from likely easier Fed policy settings is another positive.

OIL: Crude Stabilises Thursday Ahead Of US-Russia Meeting

Oil prices have stabilised during today’s APAC session. They have trended down for almost all of August on excess supply worries. On Wednesday US crude inventories rose more than expected and the IEA forecast a record market surplus for 2026. WTI is up 0.4% to $62.90/bbl but off its intraday peak of $63.00, while Brent is 0.4% higher at $65.90/bbl after reaching $65.98. The USD index is down 0.1%.

- The market is watching Ukraine developments closely with Presidents Trump and Putin meeting in Alaska on Friday.

- While Trump appears to see this event as the start of a process, any indication that a ceasefire is possible may weigh on oil prices as it increases the chance of an easing of sanctions on Russia. However, Trump has warned that there could be “very severe consequences” if Putin doesn’t agree to a truce. An extra 25% tariff will be imposed on India if there is no peace deal and India continues to buy Russian oil.

- Later the Fed’s Musalem (voter) and Barkin speak. July US PPI & jobless claims, UK Q2 GDP & June IP/trade, Q2 euro area/employment & June IP are released.

GOLD: Bullion Range Trading Ahead Of Friday's Ukraine Meeting, Fed Speak Later

Gold prices have been in a narrow range again reaching an intraday high of $3374.78/oz and then falling to $3355.67 but still 0.2% up on the day at $3361.7. US yields are little changed and the BBDXY USD index is down 0.1%. Gold has been supported by growing expectations of a September Fed 25bp rate cut, which is now more than priced in. It will also be watching Friday’s Trump-Putin talks for any change in geopolitical risks.

- US Treasury Secretary Bessent has called for the Fed to cut rates 50bp in September and noted that they should be around 1.5pp lower than the current level. Also, there is yet to be official confirmation that gold imports will be exempt from duties after President Trump posted that they would be.

- Silver reached $38.739 earlier but has moderated since and is now up 0.2% to $38.587. It has been unable to break initial resistance at $39.655.

- Equities are mixed with the S&P e-mini down 0.1% and Nikkei -1.4% but CSI 300 up 0.5% and ASX +0.6%. Oil prices are higher with WTI +0.4% to $62.88/bbl. Copper is up 0.1%.

- Later the Fed’s Musalem (voter) and Barkin speak. July US PPI & jobless claims, UK Q2 GDP & June IP/trade, Q2 euro area/employment & June IP are released.

UP TODAY (TIMES GMT/LOCAL)

| Date | GMT/Local | Impact | Country | Event |

| 14/08/2025 | 0600/0700 | *** | UK Monthly GDP | |

| 14/08/2025 | 0600/0800 | *** | Final Inflation Report | |

| 14/08/2025 | 0600/0700 | ** | Trade Balance | |

| 14/08/2025 | 0600/0700 | ** | Index of Services | |

| 14/08/2025 | 0600/0700 | ** | Index of Production | |

| 14/08/2025 | 0600/0700 | ** | Output in the Construction Industry | |

| 14/08/2025 | 0600/0700 | *** | GDP First Estimate | |

| 14/08/2025 | 0600/0800 | *** | Final Inflation Report | |

| 14/08/2025 | 0645/0845 | *** | HICP (f) | |

| 14/08/2025 | 0800/1000 | *** | Norges Bank Rate Decision | |

| 14/08/2025 | 0900/1100 | ** | Industrial Production | |

| 14/08/2025 | 0900/1100 | *** | GDP (p) | |

| 14/08/2025 | 0900/1100 | * | Employment | |

| 14/08/2025 | 1230/0830 | *** | Jobless Claims | |

| 14/08/2025 | 1230/0830 | ** | WASDE Weekly Import/Export | |

| 14/08/2025 | 1230/0830 | *** | PPI | |

| 14/08/2025 | 1230/0830 | *** | PPI | |

| 14/08/2025 | 1430/1030 | ** | Natural Gas Stocks | |

| 14/08/2025 | 1530/1130 | ** | US Bill 04 Week Treasury Auction Result | |

| 14/08/2025 | 1530/1130 | * | US Bill 08 Week Treasury Auction Result | |

| 14/08/2025 | 1800/1400 | Richmond Fed's Tom Barkin | ||

| 15/08/2025 | 2350/0850 | *** | GDP | |

| 15/08/2025 | 0200/1000 | *** | Fixed-Asset Investment | |

| 15/08/2025 | 0200/1000 | *** | Retail Sales | |

| 15/08/2025 | 0200/1000 | *** | Industrial Output | |

| 15/08/2025 | 0200/1000 | ** | Surveyed Unemployment Rate M/M | |

| 15/08/2025 | 0430/1330 | ** | Industrial Production | |

| 15/08/2025 | 0700/0900 | * | CH Flash GDP | |

| 15/08/2025 | 1230/0830 | ** | Monthly Survey of Manufacturing | |

| 15/08/2025 | 1230/0830 | ** | Wholesale Trade | |

| 15/08/2025 | 1230/0830 | *** | Retail Sales | |

| 15/08/2025 | 1230/0830 | ** | Import/Export Price Index | |

| 15/08/2025 | 1230/0830 | ** | Empire State Manufacturing Survey | |

| 15/08/2025 | 1230/0830 | *** | Retail Sales | |

| 15/08/2025 | 1300/0900 | * | CREA Existing Home Sales | |

| 15/08/2025 | 1315/0915 | *** | Industrial Production |