MNI EUROPEAN OPEN: Australian Jobs Growth Stalls, U/E Rate Up

EXECUTIVE SUMMARY

- TRUMP EYES TARIFF RATE OF 10% OR 15% FOR MORE THAN 150 COUNTRIES - BBG

- MNI INTERVIEWS US SENATOR ON BANKING COMMITTEE ON FED CHAIR POWELL’S FATE - MNI POLICY

- FED’S WILLIAMS SUPPORTS MAINTAINING RESTRICTIVE STANCE - MNI

- JAPAN JUNE EXPORTS FALL FOR THE SECOND MONTH - MNI BRIEF

- AUSTRALIA'S JOBLESS RATE HITS 3-1/2 YEAR HIGH, RAMPS UP EASING BETS FOR AUGUST - RTRS

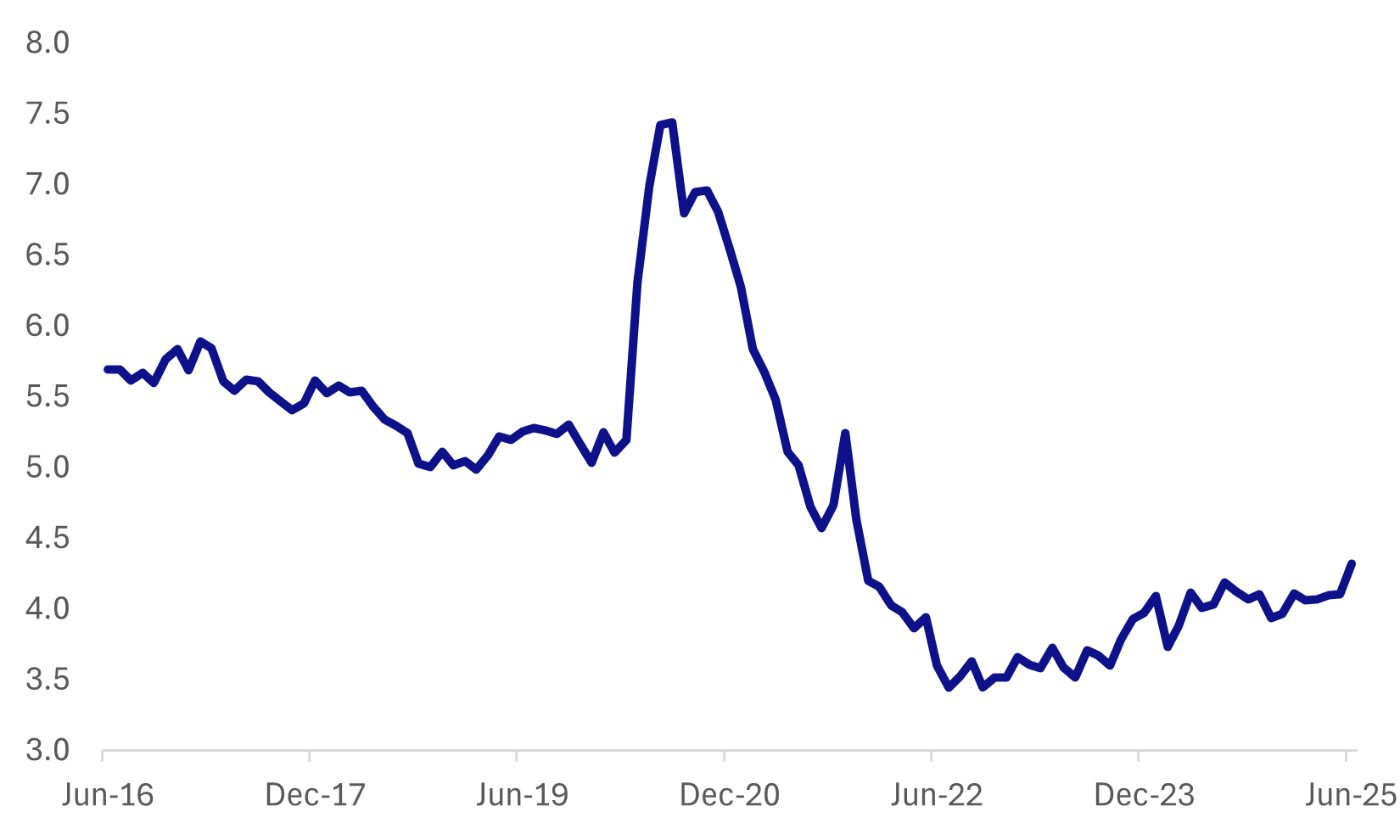

Fig 1: Australian Unemployment Rate Ticks Up In June

Source: MNI - Market News/Bloomberg/Refinitiv.

UK

POLITICS (BBG): "Labour suspended four of its Members of Parliament for breaking party discipline following a large-scale rebellion over welfare cuts earlier this month.

TRADE (BBG): "UK officials are optimistic that the Trump administration will soon agree to modify the domestic-production requirements that are holding up a trade agreement to lower US tariffs on British steel."

EU

FUNDING (MNI BRIEF): The European Commission has proposed a EUR400 billion crisis mechanism facility to provide funding for countries facing unexpected crises, EC President Ursula von der Leyen said on Wednesday.

FISCAL (BBG): “Germany has rejected the European Commission’s €2 trillion ($2.3 trillion) budget proposal, hours after it was announced by European Commission President Ursula von der Leyen in Brussels.”

US

TARIFFS (BBG): "President Donald Trump said he would send letters to more than 150 countries notifying them their tariff rates could be 10% or 15% as he forges ahead with his trade agenda."

FED (MNI INTERVIEW): MNI interviews U.S. Senator on Banking Committee on Fed Chair Powell's fate -- On MNI Policy MainWire now, for more details please contact sales@marketnews.com.

FED (MNI INTERVIEW): Federal Reserve Chair Jerome Powell could fight a potential firing by President Donald Trump in court by arguing that he is being pushed out unfairly, setting off a tough and public legal battle that would quickly make its way to the Supreme Court, Columbia University's Lev Menand told MNI.

FED (MNI): New York Federal Reserve President John Williams said Wednesday he supports holding interest rates steady and pointed to recent inflation data that he said are only beginning to show increased price pressures.

INFLATION (MNI BRIEF): Tariff-related price increases are starting to percolate through the U.S. economy and firms warned consumer prices could climb faster by late summer, according to the Federal Reserve's latest Beige Book report published Wednesday.

OTHER

MIDDLE EAST (RTRS): “Israel launched powerful airstrikes in Damascus on Wednesday, blowing up part of the defence ministry and hitting near the presidential palace as it vowed to destroy government forces attacking Druze in southern Syria and demanded they withdraw.”

CANADA (MNI): Justin Trudeau's massive deficit spending to shield the economy through the pandemic was the major cause of the following inflation burst rather than laxity from BOC Governor Tiff Macklem, according to a forthcoming paper by former central bank adviser David Andolfatto and St. Louis Fed senior economic policy Advisor Fernando Martin that MNI obtained.

CANADA (MNI BRIEF): Canada's debt management plan for the fiscal year that began April 1 was released Wednesday after delays linked to a federal election and Prime Minister Mark Carney's decision to withhold a budget until the fall, and the document shows CAD623 billion in expected borrowing with a focus on bonds over treasury bills.

CANADA (MNI BRIEF): Canadian Prime Minister Mark Carney told reporters Wednesday he hasn't yet seen the U.S. present a suitable trade agreement ahead of President Donald Trump's Aug. 1 tariff deadline, and for a second day suggested the best case scenario is securing the lowest tariffs among global competitors.

JAPAN (MNI BRIEF): Demand for bank financing from Japanese corporations declined compared to three months ago, as customers increased internally generated funds and found easier access to alternative sources, according to the Bank of Japan’s Senior Loan Officer Opinion Survey on Bank Lending Practices, released Thursday.

JAPAN (MNI BRIEF): Japan’s exports declined for the second consecutive month in June, falling 0.5% year-on-year following a 1.7% drop in May, as shipments of automobiles and iron and steel products weakened under the impact of U.S. tariffs, according to data released Thursday by the Ministry of Finance.

AUSTRALIA (RTRS): "Australian employment rose only marginally in June as the jobless rate jumped to the highest since late 2021, showing perhaps the first crack in what had been an unusually resilient labour market and adding to the case for a rate cut next month."

CHINA

ENERGY (YICAI): “China’s national daily power load reached 1.506 billion kilowatts on July 16, breaking above 1.5 billion for the first time, according to the National Energy Administration, citing higher-than-average temperatures and positive economic growth.”

CONSUMPTION (CSJ): “Authorities should remove unreasonable restrictions that constrain consumption, work to optimise the consumer goods trade-in scheme and increase diversified supply to match consumers’ needs, according to the State Council executive meeting, presided over by Premier Li Qiang on Wednesday.”

MNI: PBOC Net Injects CNY360.5 Bln via OMO Thursday

MNI (BEIJING) - The People's Bank of China (PBOC) conducted CNY450.5 billion via 7-day reverse repos, with the rate unchanged at 1.40%. The operation led to a net injection of CNY360.5 billion after offsetting the maturity of CNY90 reverse repo today, according to Wind Information.

- The seven-day weighted average interbank repo rate for depository institutions (DR007) fell to 1.4167% at 09:28 am local time from the close of 1.5291% on Wednesday.

- The CFETS-NEX money-market sentiment index, measuring interbank money-market liquidity, closed at 52 on Wednesday, compared with the close of 47 on Tuesday. A higher reading points to tighter liquidity condition, with 50 representing an equilibrium.

MNI: PBOC Sets Yuan Parity Lower At 7.1461 Thurs; +1.34% Y/Y

MNI (BEIJING) - The People's Bank of China (PBOC) set the dollar-yuan central parity rate lower at 7.1461 on Thursday, compared with 7.1526 set on Wednesday. The fixing was estimated at 7.1712 by Bloomberg survey today.

MARKET DATA

NEW ZEALAND JUNE FOOD PRICES M/M 1.2%; PRIOR 0.5%

AUSTRALIA JUL CONSUMER INFLATION EXPECTATION 4.7%; PRIOR 5.0%

AUSTRALIA JUNE EMPLOYMENT CHANGE 2.0K; MEDIAN 20.0K; PRIOR -1.1K

AUSTRALIA JUNE FULL TIME EMPLOYMENT CHANGE -38.2K; PRIOR 41.9K

AUSTRALIA JUNE PART TIME EMPLOYMENT CHANGE 40.2K; PRIOR -43K

AUSTRALIA JUNE UNEMPLOYMENT RATE 4.3%; MEDIAN 4.1%; PRIOR 4.1%

AUSTRALIA JUNE PARTICIPATION RATE 67.1%; MEDIAN 67.0%; PRIOR 67.0%

JAPAN JUNE TRADE BALANCE ¥153.1BN; MEDIAN ¥353.9BN; PRIOR -¥638.6BN

JAPAN JUNE EXPORTS Y/Y -0.5%; MEDIAN 0.5%; PRIOR -1.7%

JAPAN JUNE IMPORTS Y/Y 0.2%; MEDIAN -1.1%; PRIOR -7.7%

MARKETS

The TYU5 range has been 110-13+ to 110-20 during the Asia-Pacific session. It last changed hands at 110-14, down 0-06 from the previous close.

- The US 2-year yield has edged higher trading around 3.906%, up 0.01 from its close.

- The US 10-year yield has edged higher trading around 4.477%, up 0.02 from its close.

- The 10-year yield has broken above 4.45% in response to the CPI Data, this implies price is likely to turn its focus back to 4.65% and could see further paring back of longs. Support is now back towards the 4.35/40% area which has been the pivot in the larger 4.10% - 4.65% range.

- Nick Timiraos on X: “Removing Powell as Fed chair could lead to a messy, drawn-out standoff. The Fed owns its buildings and controls its security. If Trump attempts removal, Powell could try to stay until the courts uphold it or the Senate confirms a replacement.”

- FED'S WILLIAMS: IT'S NOT SURPRISING THAT TARIFF IMPACTS HAVE BEEN GROWING, NOT SURPRISED TARIFF IMPACTS MODEST SO FAR THERE'S BEEN GOOD NEWS ON SERVICE SECTOR INFLATION, UNDERLYING DISINFLATION PROCESS STILL UNDERWAY" - BBG

- "FED'S WILLIAMS: WITHOUT TARIFFS INFLATION WOULD BE CLOSING IN ON 2% - [RTRS]"

- (Bloomberg) -- “JPM stops out of 10s/30s flatteners on the extent of the recent move and lingering headline risk, though the strategists still say the long-end of the curve appears too steep at current levels.”

JGBS: Twist-Steepener, US Tariff Impact In Trade Data, Natl CPI Tomorrow

JGB futures are little changed but near session highs, +2 compared to settlement levels.

- (Dow Jones) “Japan's exports fell for a second straight month in June, fueling fears that U.S. tariffs will halt the nation's economic recovery and complicate the central bank's policy plans. Exports fell 0.5% compared with the same period a year earlier, according to the Ministry of Finance on Thursday. That was an improvement from May's 1.7% drop but well short of an LSEG-compiled forecast for a 0.5% increase.”

- Cash US tsys are 1-2bps cheaper in today's Asia-Pac session after yesterday's modest rally.

- Cash JGBs have twist-steepened across benchmarks, with yields 2.3bps lower (10-year) to 2.2bps higher (30-year). The benchmark 10-year yield is at 1.562% versus the cycle high of 1.60%.

- (Bloomberg) -- Japan's mounting debt burden and an election that risks making it worse are fuelling debate on whether the nation's sovereign credit rating may be cut sooner rather than later.

- Swap rates are 1bp higher to 2bps lower, with a flatter curve.

- Tomorrow, the local calendar will see Natl CPI data.

AUSSIE BONDS: Holding Post-Jobs Gains, Nov-31 Supply Tomorrow

ACGBs (YM +8.0 & XM +5.0) are holding +4-7bps after a weaker-than-expected June Employment Report.

- The Australian June jobs report was below market expectations. Jobs growth was just +2k, versus +20k forecast, after a revised -1.1k fall in May (originally reported as a -2.5k fall). The unemployment rate rose to 4.3% against a 4.1% forecast and 4.1% May outcome.

- (AFR) But it’s the momentum in the jobs market that should worry Bullock and the RBA board. The underemployment rate rose from 5.9 per cent to 6.0 per cent. The underutilisation rate jumped from 10.1 per cent to 10.3 per cent. And hours worked dropped by 0.9 per cent month-on-month in June. (via BBG)

- Cash ACGBs are 5-8bps richer on the day, 3-6bps richer post-data, with the AU-US 10-year yield differential at -12bps (-3bps pre-data).

- The bills strip has extended its bull-flattener after the data, with pricing +6 to +9.

- RBA-dated OIS pricing is 2-10bps softer across meetings today. A 25bp rate cut in August is given a 98% probability, with a cumulative 63bps of easing priced by year-end.

- Tomorrow, the local calendar will be empty apart from the AOFM’s planned sale of A$1100mn of the 1.00% 21 November 2031 bond.

BONDS: NZGBS: Modestly Richer, NZ-AU 10Y Diff Wider After AU Jobs

NZGBs closed mid-range, with benchmark yields flat to 2bps lower.

- Today’s supply was well received with cover ratios ranging from 2.83x (May-36) to 3.68x (May-30).

- The NZ-US 10-year yield differential was little changed, with the US 10-year 2bps cheaper in today’s Asia-Pac session. The NZ-AU 10-year differential was 4bps wider after a solid post-employment rally for ACGBs.

- June food prices rose 1.2%m/m, versus a 0.52% gain in May. This saw the y/y pace for food prices rise 4.6%, which was the strongest annual pace since late 2023. Stats NZ noted: "Higher prices for the grocery food group and the meat, poultry, and fish group contributed most to the annual increase in food prices, up 4.7 per cent and 6.4 per cent, respectively." Note, we get Q2 inflation next Monday.

- Swap rates closed little changed.

- RBNZ dated OIS pricing closed mostly slightly softer across meetings. 17bps of easing is priced for August, with a cumulative 33bps by November 2025.

- Tomorrow, the local calendar will be empty.

FOREX: Asia FX Wrap - Is The Powell Sacking Rumour Enough To Turn The USD Lower?

The BBDXY has had a range of 1203.66 - 1206.99 in the Asia-Pac session, it is currently trading around 1206, +0.20%. What is clear from the price action is the market is very quick to sell USD’s again if given the excuse, is the mere threat of Powell being dismissed enough to turn the USD lower again. (Bloomberg) - 'The narrative around a long-term decline in the dollar has found fresh fuel from renewed concern about political interference in US monetary policy. The mere revival of discussions - however implausible legally - around firing Federal Reserve Chair Jerome Powell has reintroduced a key bearish catalyst for the dollar.'

- EUR/USD - Asian range 1.1614 - 1.1641, Asia is currently trading 1.1620. The pair is testing its first support around the 1.1600 area. The price still looks a little stretched in the short term and is vulnerable to any correction in the USD, first support around 1.1600 then more importantly the 1.1450 area.

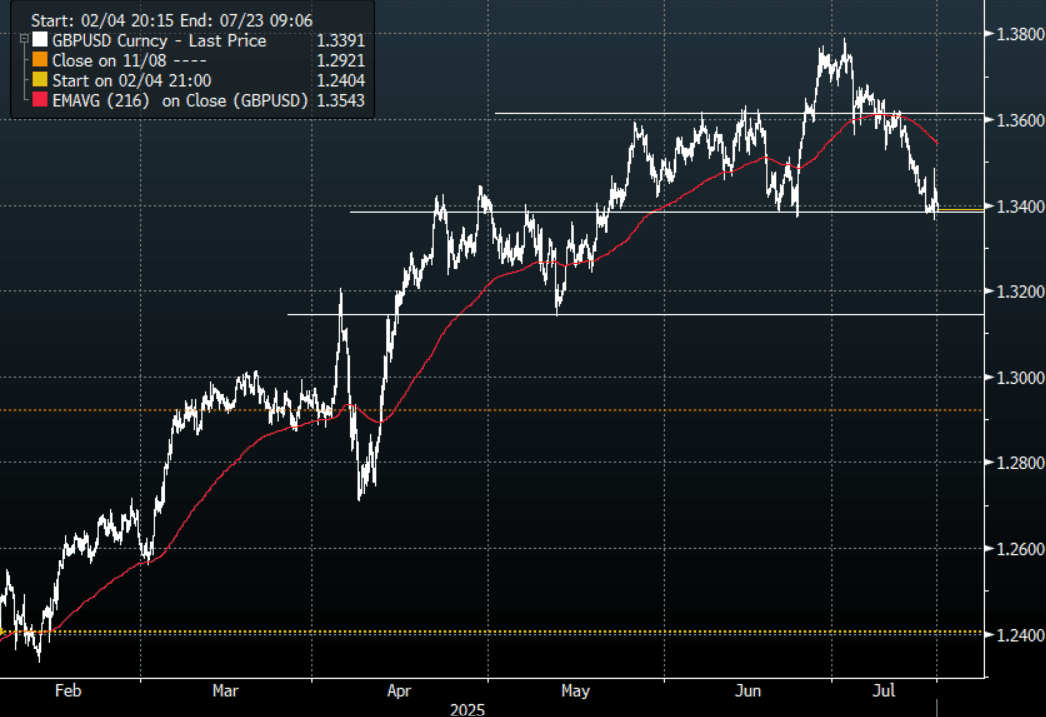

- GBP/USD - Asian range 1.3384 - 1.3430, Asia is currently dealing around 1.3390. Price has rejected the move higher and Bailey’s hint that bigger rate cuts are on their way if the job market deteriorates further will have all eyes on the data out today. The pair has moved very quickly to test important support around 1.3350/1.3400. We have seen some demand initially around this support but a sustained break below and a deeper pullback towards 1.3000/1.3200 could be on the cards. Bounces back towards 1.3500 should now see offers first up.

- USD/CNH - Asian range 7.1781 - 7.1845, the USD/CNY fix printed 7.1461, Asia is currently dealing around 7.1820. Sellers should be around on bounces while price holds below the 7.2000 area and the PBOC manages the fix lower. Above 7.2000 and we could see a test of the USD Shorts.

- Cross asset : SPX -0.25%, Gold $3355, US 10-Year 4.47%, BBDXY 1207, Crude oil $65.67

- Data/Events : EZ CPI

Fig 1: GBP/USD Spot 120min Chart

Source: MNI - Market News/Bloomberg Finance L.P

JPY: Asia Wrap - USD/JPY Finds Demand On The Dip

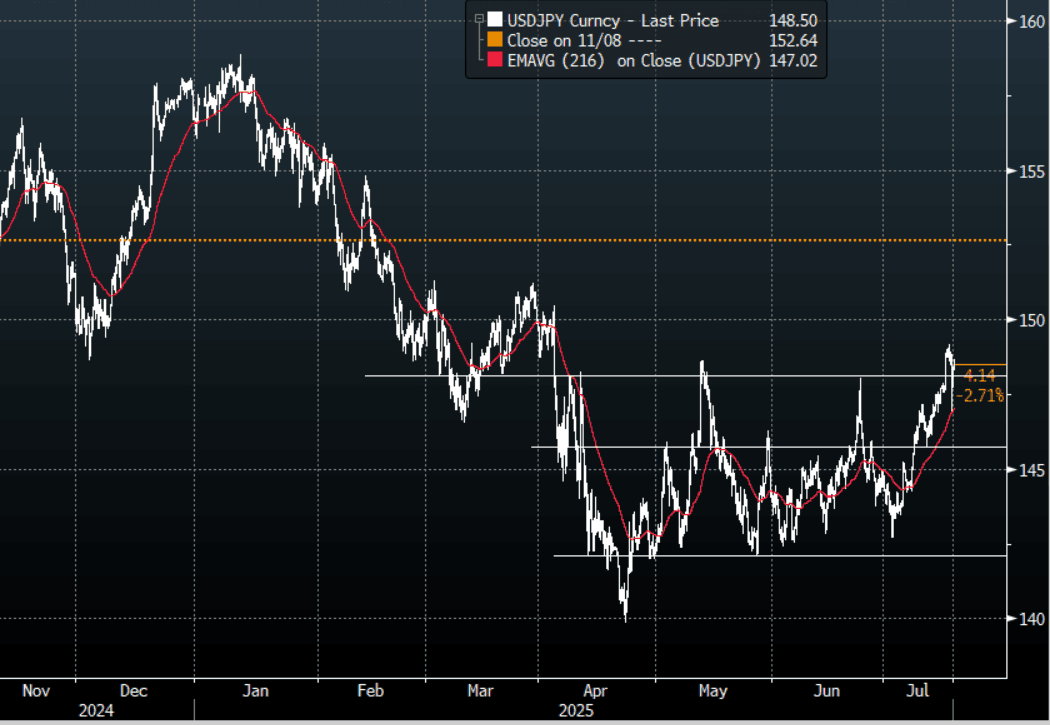

The Asia-Pac USD/JPY range has been 147.73 - 148.66, Asia is currently trading around 148.50, +0.45%. The USD had a bit of a roller coaster of a ride yesterday as rumours of a potential Powell sacking gained traction, this was later denied by Trump, though he also left the door open to Powell being dismissed for fraud. What is clear from the price action is the market is very quick to sell USD’s again if given the excuse, the last couple of weeks has been painful for the JPY longs but the market still strongly believes the USD will ultimately end lower and does not want to miss out. Decent demand was seen towards the 147.00 area overnight and would think unless there is confirmation of Powell being dismissed dips lower should be supported initially.

- (Bloomberg) - USD/JPY is seeing a short squeeze as algo systems react to headlines from Fed’s Williams which sound supportive of the US dollar. There was also likely dollar buying going into the Tokyo yen fixing as it was set at 148.51. “WILLIAMS: FACTORS SUPPORTING STRENGTH OF DOLLAR STILL IN PLACE.”

- JAPAN DATA Exports Fall Y/Y For Second Straight Month, Below Forecasts.

- Earlier we saw some verbal jawboning on FX comments from Japan officials. Aoki is the Deputy Chief Cabinet Secretary Via BBG: "AOKI: CONCERNED ABOUT MOVES IN FX MARKET INCL. SPECULATIVE ONES, KEY FOR FX RATE TO MOVE STABLY, REFLECT FUNDAMENTALS"

- Personally I don’t feel the BOJ would consider intervention again unless USD/JPY is back above 155.00 and looking to challenge 160.00 again.

- The USD/JPY market did not hold above its breakout very long, is the mere threat of Powell being dismissed enough to turn around the fortunes of USD/JPY ?

- Options : Close significant option expiries for NY cut, based on DTCC data: 147.00($1.25b).Upcoming Close Strikes : 147.00($1.29b July 22), 145.50($1.29b July 21) - BBG.

- CFTC data shows Asset managers reduced their JPY longs slightly +89331, while leveraged funds have almost squared their newly built JPY longs +5224.

Fig 1 : USD/JPY Spot 120min Chart

Source: MNI - Market News/Bloomberg Finance L.P

AUD: Asia Wrap - AUD/USD Testing Support Below 0.6500 On Poor Employment Data

The AUD/USD has had a range of 0.6473 - 0.6533 in the Asia- Pac session, it is currently trading around 0.6485, -0.67%. The USD had a bit of a roller coaster of a ride yesterday as rumours of a potential Powell sacking gained traction, this was later denied by Trump, though he also left the door open to Powell being dismissed for fraud. The price action was very clear though, if Powell is removed the USD will be swiftly sold. Australian unemployment climbed to a 4-Year high and this saw the AUD tumble across the board. The AUD/USD is attempting to break through its support just below 0.6500, one would think we would need the USD to catch a bid into the London session if this is to follow through. A break below here signals a deeper correction back towards the 0.6350 area.

- (Bloomberg) -- Australian unemployment unexpectedly climbed to a four-year high in June as hiring almost stalled, suggesting a loosening of the labor market and bolstering the case for the Reserve Bank to reduce interest rates next month.

- (Bloomberg) -- The RBA will likely cut rates by a quarter point at their August, November and February meetings, according to Nomura Singapore Ltd. “With cracks now appearing — particularly the drop in full-time workers — this opens the door wider for RBA cuts.” “The fall in AUD/USD makes sense as a solid job market has been a key reason why the RBA has been patient thus far in cutting rates.”

- Options : Closest significant option expiries for NY cut, based on DTCC data: 0.6540(AUD556m), 0.6500(AUD473m). Upcoming Close Strikes : 0.6480(AUD886m July18), 0.6500(AUD739m July 21), 0.6600(AUD725m July 21)

- CFTC Data shows Asset managers added to their shorts slightly -38252, the Leveraged community pared back their shorts to -19061.

- AUD/JPY - Today's range 96.11 - 96.77, it is trading currently around 96.35, +0.20%. The pair collapsed lower with risk but has not really recovered its losses as well as the broader market. Demand was seen again this morning toward the initial breakout area of 95.50/96.00 and this will need to hold to build a platform from which to probe higher again. A Deeper correction in risk though would clearly provide strong headwinds to further gains.

Fig 1: AUD/USD spot 120min Chart

Source: MNI - Market News/Bloomberg Finance L.P

NZD: Asia Wrap - NZD/USD Trades Heavy Rallies Should Be Capped For Now

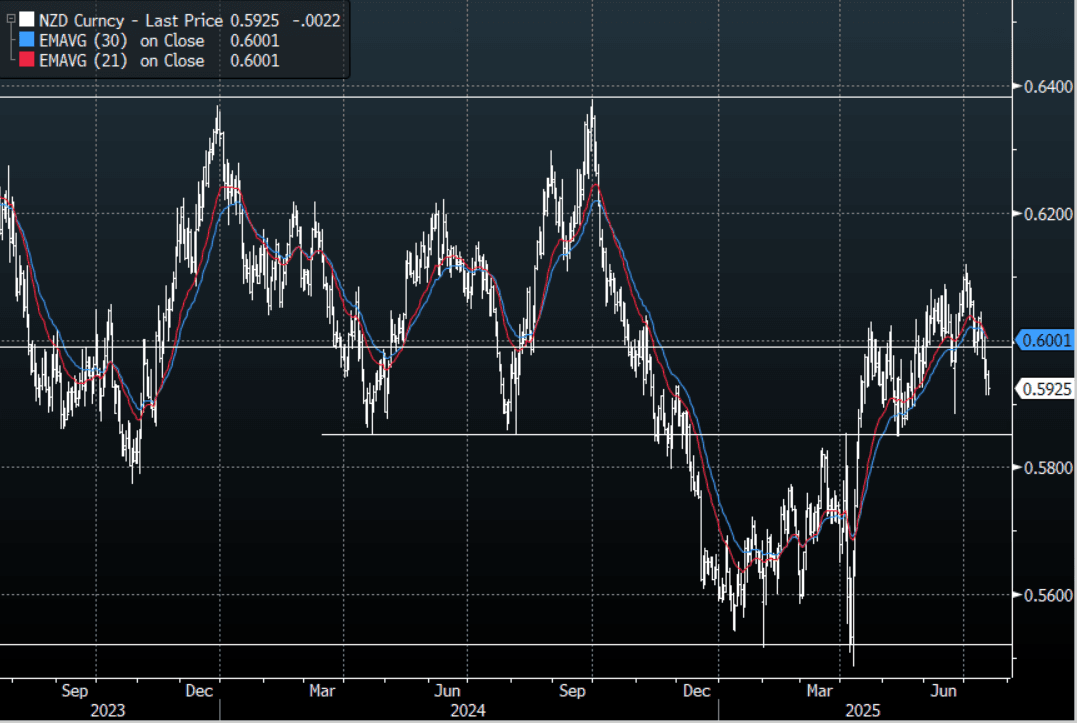

The NZD/USD had a range of 0.5912 - 0.5953 in the Asia-Pac session, going into the London open trading around 0.5925, -0.40%. The USD had a bit of a roller coaster of a ride yesterday as rumours of a potential Powell sacking gained traction, this was later denied by Trump, though he also left the door open to Powell being dismissed for fraud. The price action was very clear though, if Powell is removed the USD will be swiftly sold. NZD/USD has broken below its recent support just under 0.6000 and the price action now suggests we could have a look back towards the important 0.5850 support area. Look for supply now on bounces back towards 0.6000 to cap initially. Any hint of Powell being removed though would clearly see the NZD surge higher once more.

- NEW ZEALAND June Sees Higher Food/Utility Prices, Q2 CPI Out Next Monday

- "NZ Westpac Sees Q2 Inflation Up 0.6%q/q, 2.8% y/y : The local bank weighs in on expectations for next week's Q2 CPI outcome. It expects y/y at 2.8%, which is above RBNZ projections." - BBG

- “ANZ Bank raises Q2 inflation pick to 2.9% from 2.8% previously. “The RBNZ will find the details of the CPI a little more uncomfortable than they hoped back in May.” - BBG

- Options : Closest significant option expiries for NY cut, based on DTCC data: none. Upcoming Close Strikes : 0.5932(NZD317m July 18), 0.6000(NZD300m July 22). - BBG

- CFTC Data shows Asset Managers added slightly to their newly built longs in NZD +9229, the Leveraged community added slightly to their shorts last week -8654

- AUD/NZD range for the session has been 1.0939 - 1.0981, currently trading 1.0950. The cross has moved lower in response to the AU Employment data. Dips back to 1.0850/1.0900 should still find support as the pair tries to build momentum to move higher.

Fig 1: NZD/USD Spot Daily Chart

Source: MNI - Market News/Bloomberg Finance L.P

ASIA STOCKS: Most Regional Bourses Higher, Thailand Up Over 2%

Regional Asia Pac equity indices are mostly higher in the first part of Thursday trade. Firmer trends are evident in South East Asia (SEA) at the moment, with Thailand the standout, up close to 2.4% at this stage. US equity futures are down modestly, while EU futures are faring better. US cash trade on Wednesday saw sentiment whipped around by headlines/stories on Trump firing Fed Chair Powell (which was later denied, but is still a possibility).

- Hong Kong markets sit up a touch at the break, the HSI near 24535, still close to recent highs. The CSI 300 is up 0.31%, near 4020, so within recent ranges.

- Japan markets are modestly higher at this stage, the Topix +0.50%. USD/JPY is recovering from Wednesday's dip, while the authorities issued fresh verbal jawboning on FX markets. June trade data showed export growth stayed negative as shipments to the US fell.

- The Kospi and Taiex are little changed so far. TSMC earnings will be in focus for Taiwan and the broader AI/tech space.

- In SEA, Thailand stocks are up strongly, the SET around 1185, which is fresh highs back to May. A move above 1200 could be targeted. THB is outperforming in the FX space as well. Direct catalysts don't appear apparent. Less offshore selling pressures have been evident in Thailand markets so far in July, a potential positive.

- Indonesian stocks are up as well, last +1.20%, putting the JCI at fresh highs since January of this year. Australia's market is up around 0.65%, with earlier jobs data firmed RBA easing odds for August.

- The Philippines benchmark is down 0.65%, bucking positive trends seen elsewhere in SEA.

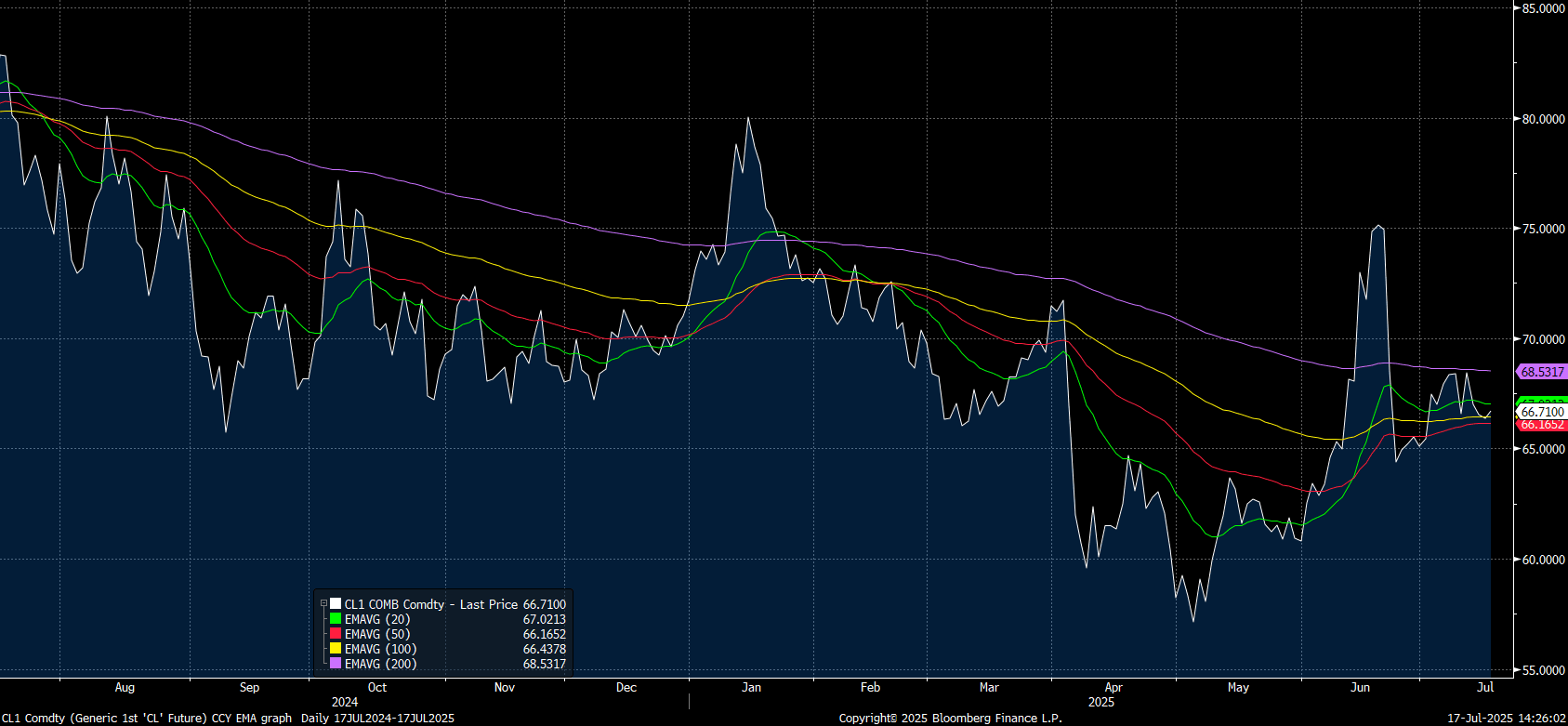

Oil Snaps Three Down Days with Modest Gains

- Oil broke three days of losses to eke out some minor gains in the Asia trading day today.

- WTI is up +34c to US$66.72 bbl. Having traded briefly below the 100-day EMA of $66.43, it has moved back above. The 20-day EMA is above at $67.02

Source: Bloomberg Finance L.P./MNI

- Brent is up also to snap three down days, rising 25c to US$68.77 bbl.

- Oils fortunes continue to ebb and flow between OPEC+ supply headlines and tariff headlines. President Donald Trump said he would send letters to more than 150 countries notifying them of tariff rates, and that the levies imposed could be 10% or 15%..

- Crude oil put spreads and other bearish strategies were active as weekly EIA oil inventory data showed signs of a softening physical market.

- Iranian authorities seized an unidentified foreign oil tanker on charges of smuggling 2 million liters of fuel in the Sea of Oman, semi-official Mehr agency reports.

- Multiple oil fields in the Kurdistan region in northern Iraq were attacked by drones on Wednesday, adding to a spate of hits on energy installations in the area this week. A majority of oil companies in the region suspended production after the attacks, resulting in the loss of nearly 200,000 barrels of oil production, according to an official.

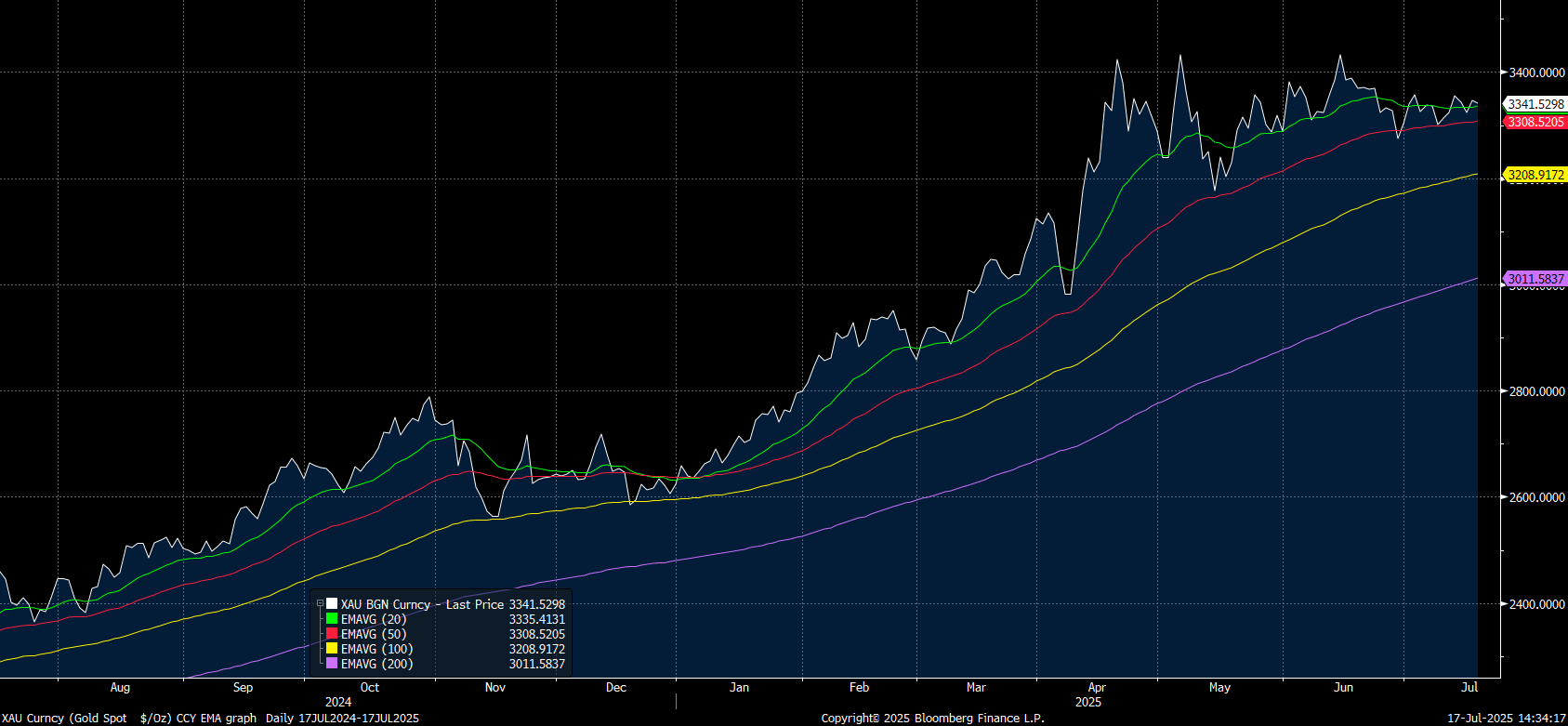

Gold Tests Key Technical Level

- Gold softened marginally today and if that continues through the European trading day, a key technical level will be tested.

- Gold is re-acting to the headlines out of the US as the President continues his attack on the Fed Chairman Powell.

- Gold is responsive to interest rate cuts as it does not earn or pay interest and lower interest rates flow through to lower costs of funding gold purchases. President Trump's main issue with Powell is he wants lower rates.

- Gold is lower today in the Asia trading day by -0.16% to be US$3,341.65 and sits just above the 20-day EMA of $3,335.45. A breach below sees the next technical level at $3,308.54 for the 50-day EMA.

Source: Bloomberg Finance L.P./MNI

UP TODAY (TIMES GMT/LOCAL)

| Date | GMT/Local | Impact | Country | Event |

| 17/07/2025 | 0600/0700 | *** | Labour Market Survey | |

| 17/07/2025 | 0600/0700 | *** | Labour Market Survey | |

| 17/07/2025 | 0900/1100 | *** | HICP (f) | |

| 17/07/2025 | 0900/1000 | ** | Gilt Outright Auction Result | |

| 17/07/2025 | - | ECB Cipollone At G20 Meeting | ||

| 17/07/2025 | 1230/0830 | *** | Jobless Claims | |

| 17/07/2025 | 1230/0830 | ** | WASDE Weekly Import/Export | |

| 17/07/2025 | 1230/0830 | * | International Canadian Transaction in Securities | |

| 17/07/2025 | 1230/0830 | *** | Retail Sales | |

| 17/07/2025 | 1230/0830 | ** | Import/Export Price Index | |

| 17/07/2025 | 1230/0830 | ** | Philadelphia Fed Manufacturing Index | |

| 17/07/2025 | 1230/0830 | *** | Retail Sales | |

| 17/07/2025 | 1315/0915 | Fed Governor Adriana Kugler | ||

| 17/07/2025 | 1400/1000 | * | Business Inventories | |

| 17/07/2025 | 1400/1000 | ** | NAHB Home Builder Index | |

| 17/07/2025 | 1400/1000 | * | Business Inventories | |

| 17/07/2025 | 1430/1030 | ** | Natural Gas Stocks | |

| 17/07/2025 | 1530/1130 | ** | US Bill 04 Week Treasury Auction Result | |

| 17/07/2025 | 1530/1130 | * | US Bill 08 Week Treasury Auction Result | |

| 17/07/2025 | 1645/1245 | San Francisco Fed's Mary Daly | ||

| 17/07/2025 | 1730/1330 | Fed Governor Lisa Cook | ||

| 17/07/2025 | 2000/1600 | ** | TICS | |

| 17/07/2025 | 2230/1830 | Fed Governor Christopher Waller | ||

| 18/07/2025 | 2330/0830 | *** | CPI | |

| 18/07/2025 | 0600/0800 | ** | PPI | |

| 18/07/2025 | 0800/1000 | ** | EZ Current Account | |

| 18/07/2025 | 0900/1100 | ** | Construction Production | |

| 18/07/2025 | - | ECB Cipollone At G20 Meeting | ||

| 18/07/2025 | 1230/0830 | *** | Housing Starts | |

| 18/07/2025 | 1230/0830 | *** | Housing Starts |