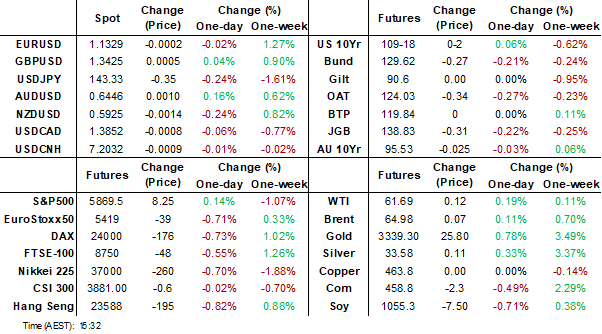

MNI EUROPEAN MARKETS ANALYSIS: USD/JPY Uptick Faded

- USD/JPY bounced early, as headlines crossed that US Tsy Secretary Bessent and Japan FinMin Kato discussed FX markets, with seemingly little shift on current positions that markets should determine FX levels. Still, the USD/JPY bounce was short lived.

- US yields have given back some of Wednesdays' gains, but focus remains on the US fiscal outlook, with a vote on Trump's tax bill scheduled for early Thursday morning US time.

- The NZ government continues to expect the budget to be in surplus in FY29, while the timing is unchanged, the amount has been revised down and is flat as a share of GDP.

- Later the Fed’s Barkin & Williams, ECB’s de Guindos & Elderson and BoE’s Pill, Breeden & Dhingra speak. The ECB’s April meeting accounts are published. US April Chicago Fed, existing home sales, May flash PMIs, Kansas Fed manufacturing and jobless claims print as well as European May PMIs.

MARKETS

US TSYS: Asia Wrap - Yields Give Back Some Overnight Gains

TYM5 has traded higher within a range of 109-13 to 109-19 during the Asia-Pacific session. It last changed hands at 109-18, up 0-02 from the previous close.

- The US 2-year yield has drifted lower, dealing around 4.001%, down 0.02 from its close.

- The US 10-year yield has drifted lower, dealing around 4.5825%, down 0.02 from its close.

- Bloomberg - “Investors are pushing back against President Donald Trump's tax-cut plan, driving yields on benchmark 30-year Treasuries to as high as 5.1% and sparking declines in stocks and the dollar.”

- “The concern is that the tax bill would add trillions of dollars to already bulging budget deficits, which could lead to a surge in borrowing costs and make it difficult for the US to address its fiscal deterioration.”

- “US HOUSE REPUBLICANS SET PRE-DAWN THURSDAY VOTES FOR SWEEPING TRUMP TAX BILL AFTER MARATHON NEGOTIATIONS - [RTRS]"

- “Trump said he’s “giving very serious consideration” to taking Freddie Mac and Fannie Mae public after more than a decade of being under government oversight.”(BBG)

- The 10-year found sellers again going into the 20-Year auction overnight and then extended after weak demand. Should yields hold this break we will then target the 4.75% area. Support seen back towards 4.45%, dips look likely to continue to see supply in the short-term. Data/Events :Chicago Fed Activity Index, Initial Jobless Claims, S&P PMI’s, Existing home Sales, Kansas City Fed Manu. Activity

JGBS: Modest Bear-Steepener, Subdued Session Ahead Of US Tax Bill

JGB futures are weaker, -33 compared to settlement levels.

- "Those JGBs issued by the Japanese government with super-low yields over the past decade were snapped up by one huge price-insensitive investor, the BoJ. Now that the BoJ wants to step back, long term yields are shooting up."

- "Why do "paper losses" on the central bank balance sheet matter? Well, the BoJ arranged a huge fixed-for-floating interest rate swap (1 GDP), paying floating and receiving fixed. If you consolidate the BoJ and the Treasury, that means huge losses for Japan's taxpayers. These "paper losses" measure the costs for Japanese taxpayers of failing to lock in low long rates."(per Hanno Lustig, see the below link) https://x.com/HannoLustig/status/1925215266402943062"

- Cash US tsys are ~1bp richer in today's Asia-Pac session.

- House Republicans have made a series of last-minute changes to their sprawling tax-and-spending bill, searching for a path that placates the party's warring wings just enough to get the bill passed at a pre-dawn vote on Thursday.

- Cash JGBs are showing a modest bear-steepener across benchmarks, with yields flat to 2bps higher.

- Swap rates are flat to 4bps higher, with a steepening bias.Tomorrow, the local calendar will see National CPI and Dept Sales data alongside BoJ Rinban Operations covering 1-25-year JGBs.

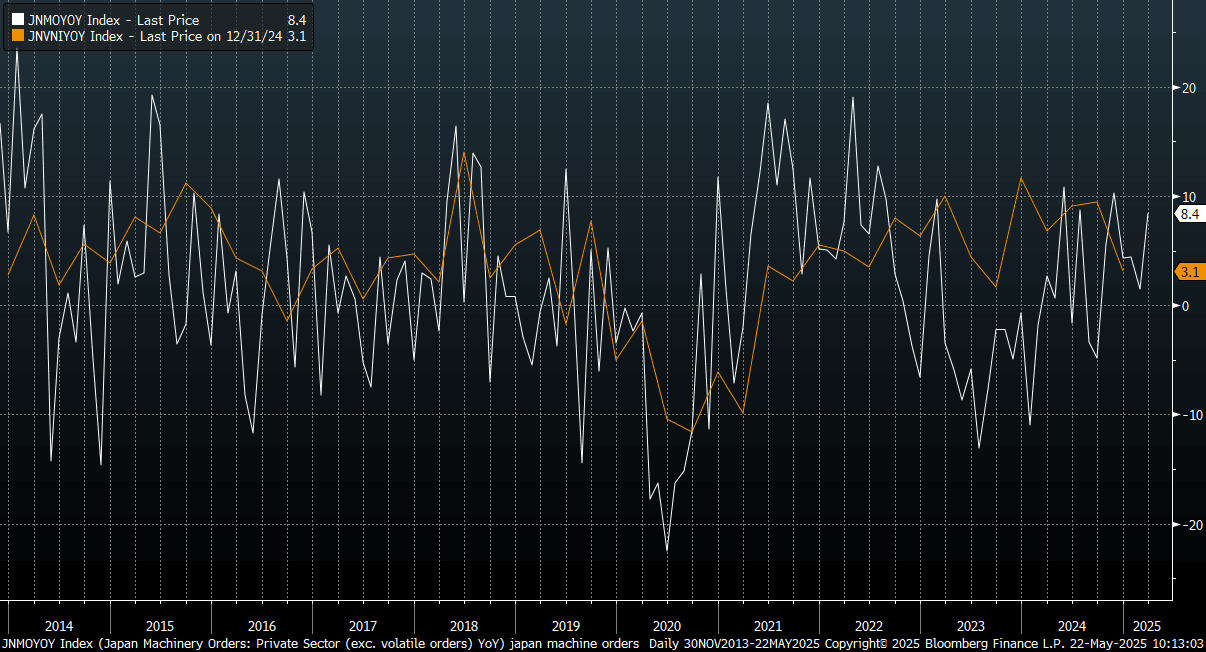

JAPAN DATA: March Core Machine Orders Well Above Estimates

Japan core machine orders for March printed well above market estimates. The m/m outcome was+13% against a -1.6% forecast, while prior was 4.3%. In y/y terms we rose 8.4%, against a -1.8% forecast and 1.5% prior.

- The chart below plots core machine orders (in y/y terms) against Capex in y/y terms from the national accounts. We had the Q1 print for GDP show firmer business spending than forecast, so today's core machine orders print for March reinforces this positive trend for end Q1.

- Still, given the Q2 outlook and beyond is being impacted by tariffs and trade uncertainty, the result is unlikely to shift steady BoJ thinking in the near term.

- The detail showed manufacturing orders up a strong 8.0% in m/m terms.

Fig 1: Japan Core Machine Orders & Capex (Y/Y)

Source: MNI - Market News/Bloomberg

JAPAN DATA: Local Investors Offshore Bond Purchases Surge In Recent Weeks

The standout last week, was the continued rise in Japan buying of offshore bonds. In the past two weeks, we have seen just over ¥4.75trln in net buying in this space. This pushes year to date flows back to positive territory. This pick up comes despite a turn down in global bond returns. This trend has continued this week, given sharp moves higher in back end US Tsy yields. Still global returns are well above earlier 2025 lows.

- Local Japan investors sold offshore equities for the first time since mid March last week, ending a strong run of outflows.

- In terms of inflows into Japan, we saw a continued net buying of local stocks. This marked the seventh straight week of net inflows into this segment.

- In contrast, offshore investors remained net sellers of local bonds for the third straight week. Again, given the surge higher in JGB yields this past week, such trends will be a watch point for the market. Inflows from offshore investors had been quite strong in April for local bonds.

Table 1: Japan Weekly Offshore Investment Flows

| Billion Yen | Week ending May 16 | Prior Week |

| Foreign Buying Japan Stocks | 714.9 | 439.4 |

| Foreign Buying Japan Bonds | -241.4 | -141.3 |

| Japan Buying Foreign Bonds | 2824.6 | 1928.7 |

| Japan Buying Foreign Stocks | -226.3 | 250.8 |

Source: MNI - Market News/Bloomberg

AUSSIE BONDS: Modestly Cheaper With A Slightly Steeper Curve

ACGBs (YM -1.0 & XM -3.0) are cheaper but sit near session bests on a data-light day.

- Cash ACGBs are showing a modest bear-steepener, with benchmark yields 1-3bps higher, with the AU-US 10-year yield differential at -11bps. For context, this differential was around flat at the start of the week.

- Cash US tsys are ~1bp richer in today's Asia-Pac session.

- House Republicans have made a series of last-minute changes to their sprawling tax-and-spending bill, searching for a path that placates the party's warring wings just enough to get the bill passed at a pre-dawn vote on Thursday.

- “Trump said he’s “giving very serious consideration” to taking Freddie Mac and Fannie Mae public after more than a decade of being under government oversight.” (BBG)

- The bills strip is slightly mixed, with a steepener bias, with pricing +1 to -2.

- RBA-dated OIS pricing is slightly firmer across meetings today. A 25bp rate cut in July is given a 66% probability, with a cumulative 68bps of easing priced by year-end.

- RBA Hauser will give a speech at 1830 AEST today. The local calendar will be empty tomorrow apart from AOFM’s planned sale of A$800mn of the 2.75% 21 November 2028 bond.

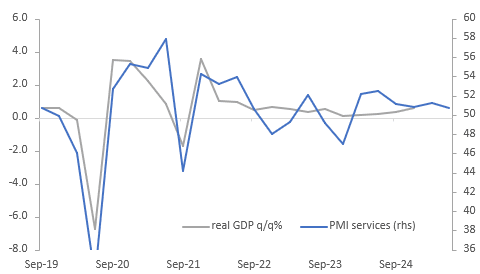

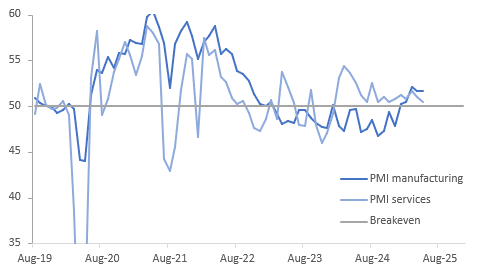

AUSTRALIA DATA: Q2 Slowdown Suggested By PMI Data

The preliminary May S&P Global composite PMI showed a moderation in growth with the index easing to 50.6 from 51, the lowest since February. The quarterly averages are showing that after a slight pickup in private sector growth in Q1 it likely slowed a bit in Q2. The manufacturing PMI was stable at 51.7, while services eased to 0.5 points to 50.5, lowest since November.

Australia S&P Global services PMI vs GDP q/q%

- While new orders continue to grow, it was at a slower pace in May with services at their lowest in 10 months. Export orders rose for the first time in three months driven by manufacturing but were still soft. S&P Global report that firms noted a decline in new business during the election campaign.

- Both services & manufacturing firms continued hiring although the pace slowed in May from April. Job creation continues due to expectations of better business conditions driving higher orders going forward, but firms are still careful reducing purchasing and inventories.

- Input and output inflation measures slowed to historical averages with the former at a 3-month low but firms are still able to pass them onto customers. The RBA noted this week that some sectors are finding that the “weakness in demand makes it difficult to pass on cost increases”.

- Services firms stated that higher costs were linked to staffing, while for manufacturers it was higher raw material prices.

- Confidence fell to below the historical average and its lowest since October driven by services. Manufacturing rose likely in line with a de-escalation in global trade tensions.

Australia S&P Global PMIs

Source: MNI - Market News/Bloomberg

BONDS: Outperforms $-Bloc Post-Budget Release

NZGBs closed showing a bull-steepener, with benchmark yields flat to 3bps lower.

- NZGBs have outperformed the $-bloc, with the NZ-US and NZ-AU 10-year yield differentials respectively narrow by 8bps and 4bps.

- The NZ government continues to expect the budget to be in surplus in FY29, while the timing is unchanged, the amount has been revised down and is flat as a share of GDP.

- From FY26 deficits were revised higher due to weaker revenue as growth was revised down near-term and unemployment higher.

- The 2025/26 NZGB programme has been set at NZ$38bn, NZ$2bn lower than that published at the Half Year Economic and Fiscal Update 2024 (HYEFU). The forecast NZGB programme for 2026/27 has been reduced by NZ$2bn, while 2027/28 and 2028/29 have been revised higher, by NZ$2bn and NZ$6bn respectively.

- S&P: New Zealand’s fiscal and current account deficits may put downward pressure on its credit rating. S&P Global Ratings says New Zealand’s budget repair efforts are starting to stall. (per BBG)

- Swap rates closed showing a modest twist-steepener.

- Tomorrow, the local calendar will see Retail Sales Ex Inflation data for Q1.

- The NZ Treasury plans to sell tomorrow NZ$250mn of the 3.00% Apr-29 bond, NZ$150mn of the 3.50% Apr-33 bond and NZ$50mn of the 1.75% May-41 bond.

NEW ZEALAND: Growth Environment Drives Weaker Public Finance Outlook

The NZ government continues to expect the budget to be in surplus in FY29, while the timing is unchanged the amount has been revised down and is flat as a share of GDP. From FY26 deficits were revised higher due to weaker revenue as growth was revised down near-term and unemployment higher. A similar pattern is likely in the updated RBNZ staff forecasts released May 28. CPI inflation was revised up this financial year but still around the mid-point of the target band over the forecast horizon.

- FY25 deficit is expected to be at 2.3% of GDP down from 3.0% estimated in December, while FY26 is forecast to be 0.3pp higher at 2.6%. Both the revenue and expenditure shares of GDP have been revised down across the horizon.

- Net debt forecasts are lower near term with FY25 revised down 2.4pp to 42.7% of GDP but the peak remains around 46% in FY28. NZ will increase its bond programme by $3bn in FY25.

- Production-based GDP growth is now forecast to contract 0.8% in FY25 down from +0.5%, while FY26 was revised down 0.4pp to 3.3%. The unemployment rate should still peak at 5.4% and then trend lower to 4.3% by FY29.

- Key policy initiatives announced include a tax incentive to increase capex and in terms of spending there will be increased funding for defence ($1bn 2025 & $1.6bn 2026), infrastructure ($1bn hospitals, $0.7bn schools), cost-of-living support and for frontline public services. There is $1.338bn of new measures net of additional revenue/savings ($4.9bn), while there is $6.8bn of new capital investment.

- The default employee/employer contributions to KiwiSaver will rise 1pp to 4% by April 2028.

- Monthly CPI releases will start in 2027.

FOREX: Asia FX Wrap - USD Struggles To Bounce

The BBDXY has had a range of 1216.80 - 1219.91 in the Asia-Pac session, it is currently trading around 1218. “House Republican leaders released a new version of Donald Trump’s tax bill with a larger SALT cap and other changes in a bid to win support from GOP factions. The House may vote as soon as Thursday”(BBG).”The EU shared a revised proposal with the US which includes gradually reducing tariffs to zero on some goods, people familiar said.(BBG)”

- EUR/USD - Asian range 1.1311 - 1.1345, Asia is currently trading 1.1330. A quiet Asian session with EUR drifting higher. The market is still expected to use dips as a buying opportunity and dips back towards 1.10 should see buyers remerge. Can it find upward momentum again ?

- GBP/USD - Asian range 1.3405 - 1.3441, Asia is currently dealing around 1.3425. A quiet Asian session with GBP drifting higher. The GBP is back to testing Pivotal Weekly Resistance in the 1.3500 area, expect it to do some work here. A break signals a potential acceleration of the trend higher.

- USD/CNH - Asian range 7.1939 - 7.2061, the USD/CNY fix printed 7.1903. Asia is currently dealing around 7.2025. Sellers should be found on a bounce back towards the 7.2400 area again.

- Cross asset : SPX +0.06%, Gold $3335, US 10-Year 4.58%, BBDXY 1218, Crude oil $61.64

- Data/Events : France Business Confidence, France PMI’s, German PMI’s & IFO, EZ PMI’s

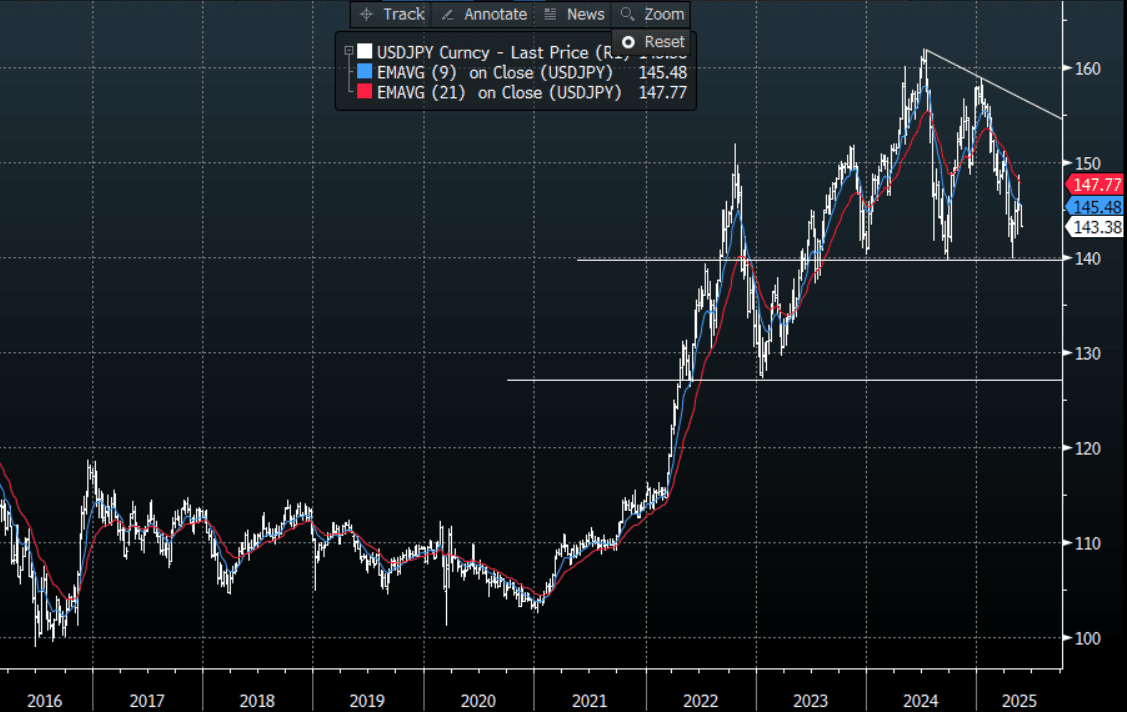

JPY: Asia Wrap - Sellers Cap An Early Bounce

The Asia-Pac range has been 143.15 - 144.40, Asia is currently trading around 143.35. USD/JPY was under pressure all through the overnight session but bounced higher in early morning trading, the pair printed a high of 144.40 on headlines related to the meeting between US Tsy Secretary Bessent and Japan FinMin Kato on the sidelines of the G7 in Canada. It could not hold these gains and spent the rest of the session back under pressure to eventually break the overnight lows.

- Scott Bessent on X - “Great to meet again with Japanese Minister of Finance @KatsunobuKato1 on the margins of the @G7 meetings in Banff. We addressed important issues in the U.S.-Japan economic relationship, including global security, bilateral trade between our nations, and our shared belief that exchange rates should be market determined. https://x.com/SecScottBessent/status/1925313086799630633"

- At face value, this suggests a maintenance of the status quo in terms of FX policy (rather than a potential shift towards a change that would push for greater balance in the trade position, which would argue for stronger yen levels versus the USD, all else equal).

- BoJ board member Noguchi's earlier remarks didn't hint at any major concern around the recent sharp rise in JGB yields : He noted - via Rtrs: "BOJ'S NOGUCHI: PERSONALLY DON'T SEE NEED TO MAKE BIG CHANGES TO EXISTING BOJ TAPER PLAN, whilst adding "BOJ'S NOGUCHI: AS FOR TAPER PLAN FOR APRIL 2026 ONWARD, WE NEED TO EXAMINE WITH A LONGER-TERM PERSPECTIVE", and "*NOGUCHI: MARKET SHOULD DECIDE LONG-TERM INTEREST RATES" - BBG.

- The price action shows the market is still much more comfortable selling rallies, resistance is now back towards 146.00. The longer we stay down here the focus will turn once more to the pivotal 140.00 area.

Options : Closest significant option expiries for NY cut, based on DTCC data: 143.50($600m), Upcoming Strikes : 145.00($2.12b May 23),144.00($1.85b May 23)

Fig 1 : USD/JPY Spot Weekly Chart

Source: MNI - Market News/Bloomberg

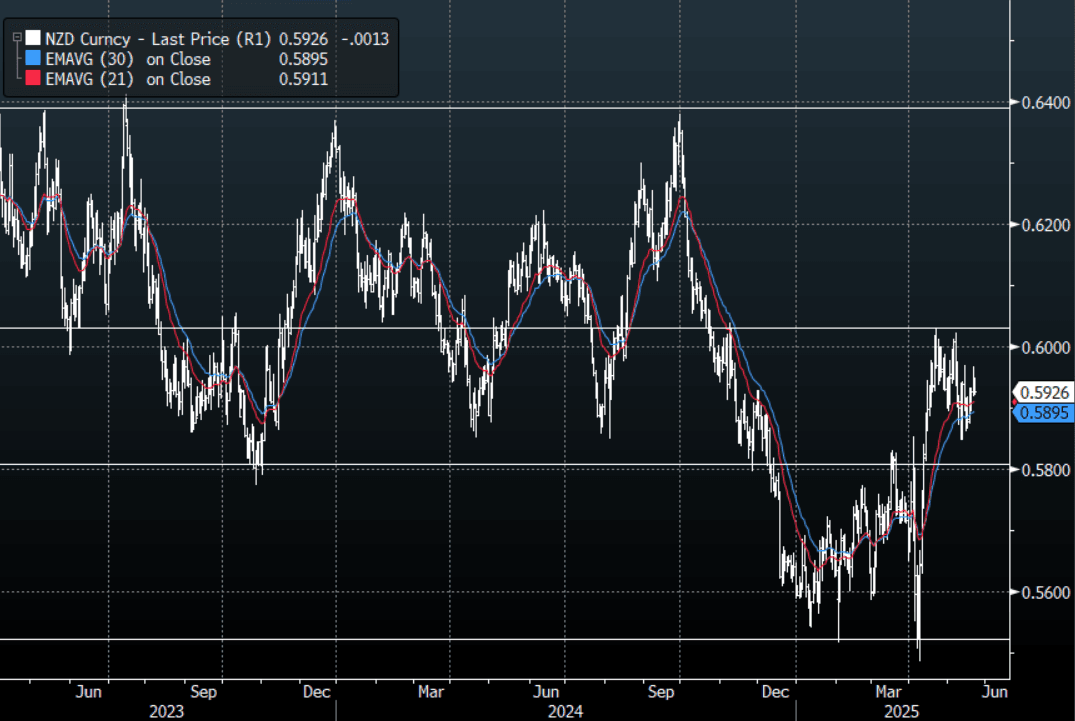

NZD: Asia Wrap - Trades Softer As NZ Sees Slower Growth

The NZD/USD had a range of 0.5921 - 0.5948 in the Asia-Pac session, going into the London open trading around 0.5925. US stocks stabilised in the Asian session but the NZD has traded softer on the NZ Budget showing a weaker economy with less tax revenue.

- The NZ government continues to expect the budget to be in surplus in FY29, while the timing is unchanged the amount has been revised down and is flat as a share of GDP. From FY26 deficits were revised higher due to weaker revenue as growth was revised down near-term and unemployment higher.

- *NEW ZEALAND BUDGET SHOWS WEAKER ECONOMY, LESS TAX REVENUE

- *NEW ZEALAND SEES BUDGET DEFICIT OF NZ$12.1B IN 2026”

- The NZD/USD has traded softer for most of our session albeit not running away.

- The NZD continues to look comfortable in a 0.5850/0.6050 range and awaits a catalyst to provide the impetus to break-out.

- The support back towards 0.5800 has held very well, and while this continues to hold expect buyers to be around on dips. The first target is the highs just above 0.6000, a break here is needed to regain momentum.

- Options : Closest significant option expiries for NY cut, based on DTCC data: none, Upcoming Strikes : 0.5705(NZD805m May 23), 0.5980(NZD513m May26)

AUD/NZD range for the session has been 1.0822 - 1.0877, currently trading 1.0875. The Cross has bounced in our session as the NZD trades softly after the Budget. A sustained break above 1.0920 is needed to turn the focus higher, until then expect supply on bounces.

Fig 1: NZD/USD Spot Daily Chart

Source: MNI - Market News/Bloomberg

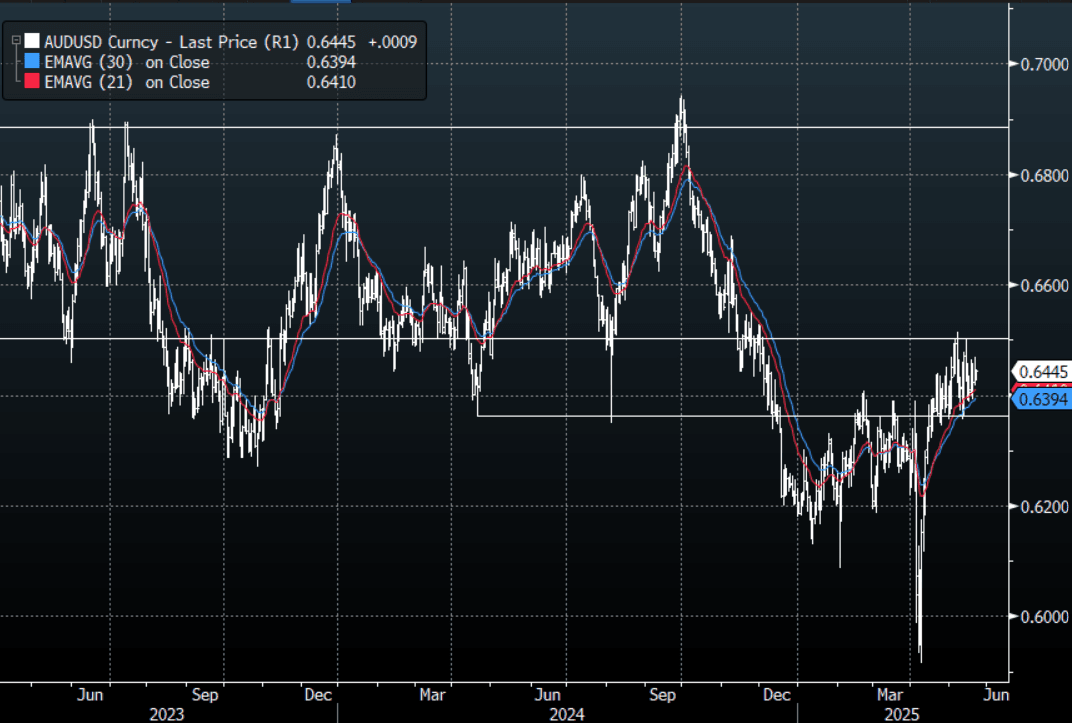

AUD: Asia Wrap - Quiet Session, Trades Steady

The AUD/USD has had a tight range of 0.6427 - 0.6447 in the Asia- Pac session, it is currently trading around 0.6445. US stocks stabilised in the Asian session and the AUD has traded sideways in a pretty quiet session.

- MNI Data - The preliminary May S&P Global composite PMI showed a moderation in growth with the index easing to 50.6 from 51, the lowest since February. The quarterly averages are showing that after a slight pickup in private sector growth in Q1 it likely slowed a bit in Q2. The manufacturing PMI was stable at 51.7, while services eased to 0.5 points to 50.5, lowest since November.

- “Nomura has added another RBA rate cut to its outlook and now forecasts a 25bp reduction in November in addition to August, which would take the cash rate to 3.35%.”(BBG)

- The AUD/USD is looking comfortable in a 0.6350 - 0.6550 range. The AUD continues to hold up pretty well against the USD so If you want to express a short it looks best to do that in the crosses for now.

- Expect buyers to be around on dips while the support in the AUD holds, a close back below 0.6300/50 would start to challenge the newly formed uptrend.

- Options : Closest significant option expiries for NY cut, based on DTCC data: none, Upcoming Strikes : 0.6375(AUD683m May 23), 0.6550(AUD529m May 23), 0.6510(AUD1.4b May 27)

AUD/JPY - Today's range 92.14 - 92.84, it is trading currently around 92.25. Decent demand again seen towards the 92.00 area as it holds overnight. A sustained close back below 91.50/92.00 is needed to turn the focus back towards the lows again. With stocks looking like they have more to go in this retracement it could provide further headwinds for this pair.

Fig 1: AUD/USD spot Daily Chart

Source: MNI - Market News/Bloomberg

ASIA STOCKS: Korea's KOSPI Leads Regional Falls

Plans in the US to seek to pass a bill focused on tax cuts drove bond yields higher and volatility throughout Asia's major bourses. Fears as to the sustainability of the already perilous US fiscal position created a risk off day with the KOSPI one of the biggest fallers. In what was a good day for most Asia FX, major bourses couldn't say the same as falls were experienced throughout the region.

- China's Hang Seng fell -0.55% today following over 2% gains in the prior two trading days as sentiment slipped. The CSI 300 eked out some minor gains of +0.13% whilst the Shanghai Composite was flat and Shenzhen fell -0.45%

- The KOSPI was down -1.20% and could present its first weekly loss since mid-April if there is no improvement tomorrow.

- The FTSE Bursa Malaysia's poor run continues, down for its sixth consecutive day, falling -0.87%.

- The Jakarta Composite's star continues to shine as it rallied again today by +0.56%. It has only recorded four down days in the last 27 trading days.

- In Singapore, the FTSE Straits Times fell -0.33% and the PSEi in the Philippines dropped -1.33%

- India's NIFTY 50 could not hide from the risk aversion and is down -0.80%, to be down over -1.5% so far this week.

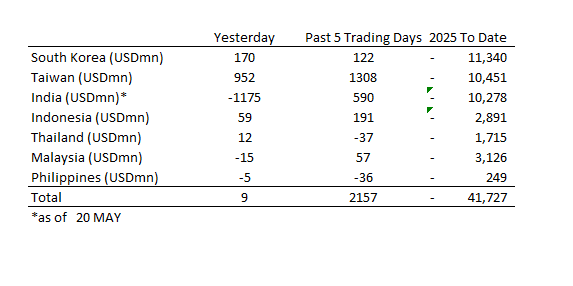

ASIA STOCKS: India Has Large Outflow

Following five successive days of inflows, India had a substantial outflow on the 20th whilst Taiwan continued to receive inflows.

- South Korea: Recorded inflows of +$170m yesterday, bringing the 5-day total to +$122m. 2025 to date flows are -$11,340. The 5-day average is +$24m, the 20-day average is +$57m and the 100-day average of -$121m.

- Taiwan: Had inflows of +$952m yesterday, with total inflows of +$1,308m over the past 5 days. YTD flows are negative at -$10,451. The 5-day average is +$262m, the 20-day average of +$481m and the 100-day average of -$116m.

- India: Had outflows of -$1,175m as of the 20th, with total inflows of +$590m over the past 5 days. YTD flows are negative -$10,278m. The 5-day average is +$118m, the 20-day average of +$235m and the 100-day average of -$121m.

- Indonesia: Had inflows of +$59m as of yesterday, with total inflows of +$191m over the prior five days. YTD flows are negative -$2,891m. The 5-day average is +$38m, the 20-day average $5m and the 100-day average -$33m

- Thailand: Recorded inflows of +$12m as of yesterday, outflows totaling -$37m over the past 5 days. YTD flows are negative at -$1,715m. The 5-day average is -$7m, the 20-day average of -$15m the 100-day average of -$17m.

- Malaysia: Recorded outflows of -$15m as of yesterday, totaling +$57m over the past 5 days. YTD flows are negative at -$3,126m. The 5-day average is +$2m, the 20-day average of +$41m and the 100-day average of -$22m.

- Philippines: Saw outflows of -$5m as of yesterday, with net outflows of -$36m over the past 5 days. YTD flows are negative at -$249m. The 5-day average is -$7m, the 20-day average of +$2m the 100-day average of -$3m.

OIL: Crude Stabilises After Yesterday’s Losses, Monitoring Range Of Issues

After falling over a percent on Wednesday, oil prices are slightly higher during today’s APAC session. WTI is up 0.2% to $61.68/bbl, close to the intraday high, while Brent is up 0.1% to $64.95/bbl. Markets continue to worry about and monitor Russia & Iran developments, OPEC production plans, US demand and trade negotiations.

- The USD index is down 0.1% today to be down 1.2% this week which has likely supported dollar-denominated crude in a weaker risk sentiment environment. Markets are concerned by the US’ fiscal outlook.

- US Secretary of State Rubio said that licences to export oil from Venezuela would expire on May 27 as planned when a 60-day extension had been expected. This will impact Chevron significantly as it has produced around 20% of Venezuela’s oil recently, according to Bloomberg.

- Europe increased sanctions this week on Russian financial intermediaries and tankers headed to China and the UK now wants the price cap on Russian crude reduced. The US is currently hesitant to follow with Trump saying that tighter restrictions will be counterproductive but a WSJ report is suggesting that he did tell European leaders after his call with Putin that he believed that Russia is not yet ready for peace.

- Later the Fed’s Barkin & Williams, ECB’s de Guindos & Elderson and BoE’s Pill, Breeden & Dhingra speak. The ECB’s April meeting accounts are published. US April Chicago Fed, existing home sales, May flash PMIs, Kansas Fed manufacturing and jobless claims print as well as European May PMIs.

GOLD: Bullion Continues Trend Higher As US Deficit Worries Persist

Gold prices continue to trend higher during the APAC session rising around 0.7% to $3338.15/oz after rising 0.8% on Wednesday as the metal benefits from safe-haven flows as risk sentiment deteriorates on worries over the US budget. It is up 4.2% this week. They reached a high of $3345.38 earlier, approaching initial resistance of $3347.50, 9 May high.

- Negotiations continued with Republicans who won’t support US President Trump’s tax cut bill unless further spending cuts are included. A vote is hoped to take place this week. The expected increase in the deficit has troubled markets with US yields rising sharply yesterday but are slightly lower today.

- The USD index is down 0.1% today to be down 1.2% this week which has contributed to buying of dollar-denominated gold.

- Medium-term signals for gold remain bullish with the corrective phase finished. Moving average studies highlight a bull-mode position. Initial resistance is at $3347.5, 9 May high, while support is at $3176.4, 20-day EMA.

- Equities are lacklustre with the Hang Seng down 0.6% and Nikkei -1.0% and S&P e-mini up only 0.06%. Oil prices are up slightly with WTI +0.2% to $61.67/bbl. Copper is 1.2% higher and silver 0.9% to $33.69.

- Later the Fed’s Barkin & Williams, ECB’s de Guindos & Elderson and BoE’s Pill, Breeden & Dhingra speak. The ECB’s April meeting accounts are published. US April Chicago Fed, existing home sales, May flash PMIs, Kansas Fed manufacturing and jobless claims print as well as European May PMIs.

INDIA: Preliminary PMI's Show Ongoing Resilience

- India's preliminary PMI's confirmed that the economy remains resilient in spite of the global uncertainties.

- The PMI Manufacturing (preliminary) rose to +58.3, from +58.2 prior and marking the best result since the middle of 2024.

- Despite the rise output declined to +61.4 from +61.9 and new orders fell also.

- The PMI Services (prelim) jumped to +61.2 from +58.7 prior to the highest it has been since Q1 2024

- The PMI services saw employment rise to +57.9 from +53.9 to market its highest ever reading; and prices charged rose for its highest reading since November 2024.

MALAYSIA: CPI In Line with Expectations

- Malaysia's April CPI rose +1.4% YoY in line with estimates and March's result

- Core CPI rose +2% YoY

- Food and non-alcoholic beverages +2.3% YoY; Housing, water and electricity +2% YoY and Transport +0.7% YoY.

- The BNM does not have a specific inflation target but believes above 3% exceeds what is deemed acceptable.

- Clearly at these levels, the BNM has limited concerns as to inflationary pressures, even in a trade war environment.

- The BNM next meets on July 09

CHINA: Country Wrap: Signs of Life in China Property Sales

- China Securities Journal reports that sales of second hand and new homes in major cities in China have been showing signs of recovery. Property viewings are on the increase in Beijing with some signs of price increases and some new developments selling out (source China Securities)

- Chinese Premier Li Qiang will meet President Prabowo Subianto during the visit, says Foreign Ministry spokesperson. The trip will include a business banquet, a meeting with parliament leaders and MoU signings on health, tourism and export protocols, he says in a press briefing on Wednesday (source BBG)

- China's Hang Seng fell -0.55% today following over 2% gains in the prior two trading days as sentiment slipped. The CSI 300 eked out some minor gains of +0.13% whilst the Shanghai Composite was flat and Shenzhen fell -0.45%

- Yuan Reference Rate at 7.1903 Per USD; Estimate 7.2035

- Bonds were a touch softer today with the CGB 10YR at 1.68% (+0.5bp)

ASIA FX: Mixed Trends In NEA, USD/KRW Rebounds, USD/TWD Dips Towards 30.00

In North East Asia FX, trends have been mixed. USD/CNH couldn't sustain an earlier dip, while USD/KRW has rebounded after strong won gains on Wednesday. USD/TWD is lower.

- USD/CNH saw a brief dip under 7.1950 not long after the USD/CNY fixing, which was a fresh low back to early Apr of this year. However, we steadily climbed from there and are back above the 7.2030 level now. CNH's beta with respect to USD moves remains low, particularly in terms of fresh USD downside. This is leaving CNH underperforming on key crosses. CNH/JPY is back under 19.90.

- Spot USD/KRW has rebounded, following Wednesday's strong won gains, which reflected reports that US-South Korea officials are discussing FX markets, with US officials reportedly stating that the weaker won trend is driving the country's trade surplus. From the low 1370 region, USD/KRW now sits back above 1380, around 0.65% weaker in won terms. Today's move higher in the pair feels like a consolidation though after Wednesday's sharp dip. Sellers might emerge between current levels and 1390.

- USD/TWD has fallen close to 30.00, but hasn't been able to test below the figure level yet. Late yesterday, the CBC Governor stated that the authorities allowed the FX to strengthen to reset market dynamics around continued appreciation speculation. It was added that the central bank doesn't have a line in the sand when it comes to FX levels. If we can break sub 30.00, the earlier May low near 29.60 could be in focus.

UP TODAY (TIMES GMT/LOCAL)

| Date | GMT/Local | Impact | Country | Event |

| 22/05/2025 | 0600/0700 | *** | Public Sector Finances | |

| 22/05/2025 | 0645/0845 | ** | Manufacturing Sentiment | |

| 22/05/2025 | 0715/0915 | ** | S&P Global Services PMI (p) | |

| 22/05/2025 | 0715/0915 | ** | S&P Global Manufacturing PMI (p) | |

| 22/05/2025 | 0730/0930 | ** | S&P Global Services PMI (p) | |

| 22/05/2025 | 0730/0930 | ** | S&P Global Manufacturing PMI (p) | |

| 22/05/2025 | 0800/1000 | *** | IFO Business Climate Index | |

| 22/05/2025 | 0800/1000 | ** | S&P Global Services PMI (p) | |

| 22/05/2025 | 0800/1000 | ** | S&P Global Manufacturing PMI (p) | |

| 22/05/2025 | 0800/1000 | ** | S&P Global Composite PMI (p) | |

| 22/05/2025 | 0830/0930 | *** | S&P Global Manufacturing PMI flash | |

| 22/05/2025 | 0830/0930 | *** | S&P Global Services PMI flash | |

| 22/05/2025 | 0830/0930 | *** | S&P Global Composite PMI flash | |

| 22/05/2025 | 1000/1100 | ** | CBI Industrial Trends | |

| 22/05/2025 | 1050/1150 | BOE's Breeden On Climate Panel | ||

| 22/05/2025 | 1100/1200 | BOE's Dhingra On UK Productivity Panel | ||

| 22/05/2025 | 1130/1330 | ECB April Minutes Released | ||

| 22/05/2025 | 1200/0800 | Richmond Fed's Tom Barkin | ||

| 22/05/2025 | 1230/0830 | *** | Jobless Claims | |

| 22/05/2025 | 1230/0830 | ** | WASDE Weekly Import/Export | |

| 22/05/2025 | 1230/0830 | * | Industrial Product and Raw Material Price Index | |

| 22/05/2025 | 1230/1330 | BOE's Pill At MonPol Conference (Text 16:30BST) | ||

| 22/05/2025 | 1300/1500 | ** | BNB Business Confidence | |

| 22/05/2025 | 1345/0945 | *** | S&P Global Manufacturing Index (Flash) | |

| 22/05/2025 | 1345/0945 | *** | S&P Global Services Index (flash) | |

| 22/05/2025 | 1400/1000 | *** | NAR existing home sales | |

| 22/05/2025 | 1400/1000 | * | Services Revenues | |

| 22/05/2025 | 1430/1030 | ** | Natural Gas Stocks | |

| 22/05/2025 | 1500/1100 | ** | Kansas City Fed Manufacturing Index | |

| 22/05/2025 | 1500/1700 | ECB's Elderson Dinner Speech at Biodiversity Day | ||

| 22/05/2025 | 1530/1130 | ** | US Bill 04 Week Treasury Auction Result | |

| 22/05/2025 | 1530/1130 | * | US Bill 08 Week Treasury Auction Result | |

| 22/05/2025 | 1535/1735 | ECB's de Guindos Speech in Madrid | ||

| 22/05/2025 | 1700/1300 | ** | US Treasury Auction Result for TIPS 10 Year Note | |

| 22/05/2025 | 1800/1400 | New York Fed's John Williams | ||

| 22/05/2025 | 1900/1500 | New York Fed's Roberto Perli | ||

| 23/05/2025 | 2301/0001 | ** | Gfk Monthly Consumer Confidence | |

| 23/05/2025 | 2330/0830 | *** | CPI | |

| 23/05/2025 | 0600/0800 | ** | Unemployment | |

| 23/05/2025 | 0600/0700 | *** | Retail Sales | |

| 23/05/2025 | 0600/0800 | *** | GDP (f) | |

| 23/05/2025 | 0645/0845 | ** | Consumer Sentiment | |

| 23/05/2025 | 0830/1030 | ECB's Lane Inflation Lecture in Florence | ||

| 23/05/2025 | 1230/0830 | * | Quarterly financial statistics for enterprises | |

| 23/05/2025 | 1230/0830 | ** | Retail Trade | |

| 23/05/2025 | 1230/0830 | ** | Retail Trade | |

| 23/05/2025 | 1335/0935 | Kansas City Fed's Jeff Schmid |