MALAYSIA: CPI In Line with Expectations

- Malaysia's April CPI rose +1.4% YoY in line with estimates and March's result

- Core CPI rose +2% YoY

- Food and non-alcoholic beverages +2.3% YoY; Housing, water and electricity +2% YoY and Transport +0.7% YoY.

- The BNM does not have a specific inflation target but believes above 3% exceeds what is deemed acceptable.

- Clearly at these levels, the BNM has limited concerns as to inflationary pressures, even in a trade war environment.

- The BNM next meets on July 09

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

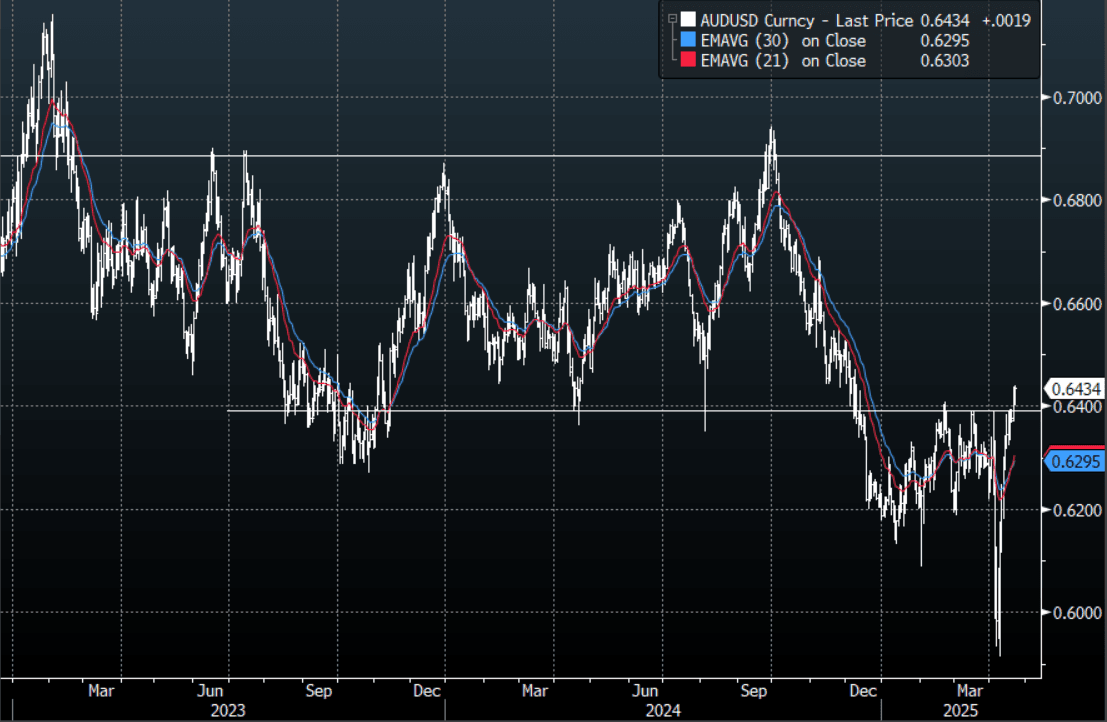

FOREX: Antipodean Wrap - AUD & NZD Making New Highs

With hopes of any early trade deal fading, the market very quickly returned to what is now becoming a consensus trade, sell the USD. USD/CNH is stable but look at EUR/CNH and CNH/JPY to see how the Yuan is being managed lower. “ (Bloomberg) -- New Zealand exporters had a bumper start to the year, buoyed by a lower currency and higher global prices for key commodities such as milk powder and meat. Exports surged to a record NZ$20.6 billion ($12 billion) in the three months through March, Statistics New Zealand said Tuesday in Wellington. That’s a seasonally adjusted 11% jump from the fourth quarter and 19% more than the year-earlier period.”

- AUD/USD - Asian range 0.6402 - 0.6436, AUD has traded better bid for most of the Asian session. After showing some signs of exhaustion at the end of last week the AUD has broken and held above the pivotal 0.6400 area. Dips back to the 0.6300 area should continue to find demand while the market obsesses about a lower USD.

- AUD/JPY - Asian range 90.12 - 90.57. Price goes into the London open towards the lows trading around 90.20, still firmly within last week’s range of 89.50-91.50. Support towards 90.00 continues to hold for now, a break through here and the downward trend could be reinstated.

- NZDUSD - Asian range 0.5981 - 0.6021, NZ exports hit a record on low currency and high commodities. The market is going into London pressing new highs. Thoughts of a reversion were fleeting as upward momentum is reignited. Expect buyers to return first around 0.5920/50, then around 0.5850/80.

- AUD/NZD - Asian range 1.0682 - 1.0706, the cross has drifted sideways in the Asian session.

Fig 1 : AUD/USD Spot Daily Chart

Source: MNI - Market News/Bloomberg

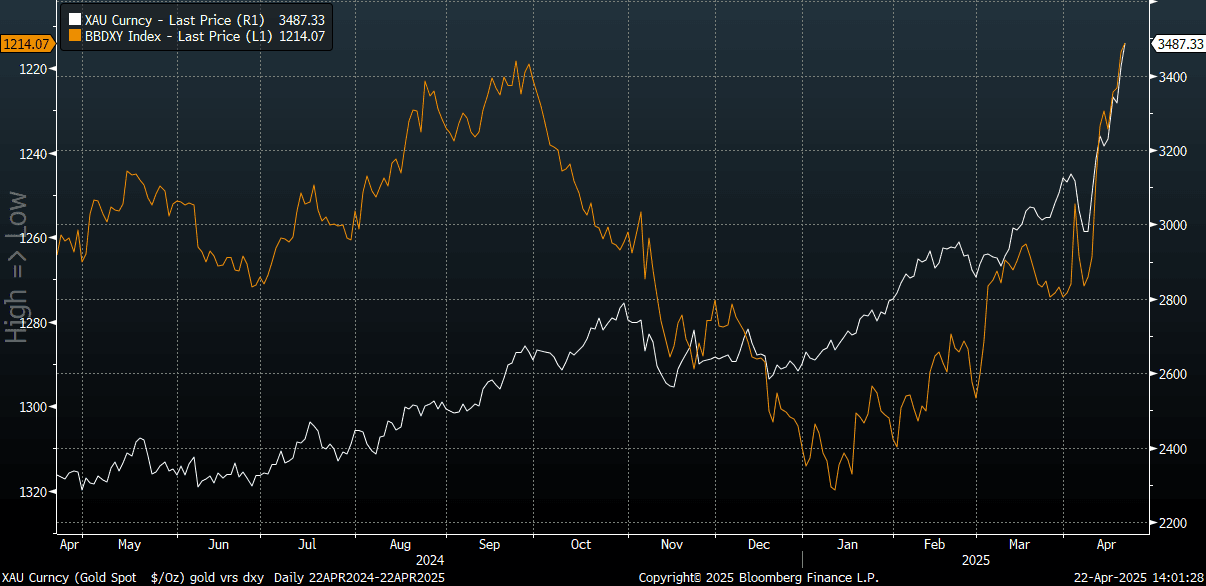

GOLD: Close To $3500, Moving In Line With USD Weakness

Gold is fast approaching the $3500 level. Session highs rest at $3494.8, while we were last near $3486/87, still up 1.8% for the session so far. Monday's gain for bullion was 2.92%.

- Gold is moving in lockstep with USD weakness, the chart below shows bullion plotted against the BBDXY index, which is inverted on the chart.

- The inability of the USD to sustain the earlier modest rebound has likely only added to gold's current bullish momentum. The USD remains firmly under pressure, with continued unwinding of US exceptionalism in focus.

- As we noted earlier, the RSI (14) on gold is comfortably into overbought territory, not at 79.6, but we are still under 2024 extremes for this metric.

Fig 1: Gold Spot Price & USD BBDXY Index (Inverse)

Source: MNI - Market News/Bloomberg

JGBS: Weaker & At Session Lows At Lunch

At the Tokyo lunch break, JGB futures are sharply weaker and at session lows, -41 compared to the settlement levels.

- "Bank of Japan officials see no need to change their stance on gradually raising interest rates despite US tariffs, as they wait for more data to analyse the impact. The BOJ is likely to hold its policy settings steady at its May 1 meeting and may cut its price forecast due to a stronger yen, cheaper oil, and economic weakness." (per BBG)

- “The impact of Donald Trump’s tariff campaign has already filtered through to Japanese companies, with about 10% saying the measures have affected their businesses and more voicing concern on the future jolt, according to a MoF survey.” (per BBG)

- Cash US tsys are slightly cheaper, with a flattening bias, in today's Asia-Pac session after yesterday's long-end sell-off.

- Cash JGBs are 1- 5 bps cheaper across benchmarks, with the belly leading. The benchmark 10-year yield is 4.5bps higher at 1.330% versus the cycle high of 1.596%.

- Swap rates are 2-6 bps higher. Swap spreads are mixed.

- Today, the local calendar will be empty apart from an Enhanced Liquidity Auction for 15.5-39-year JGBs.