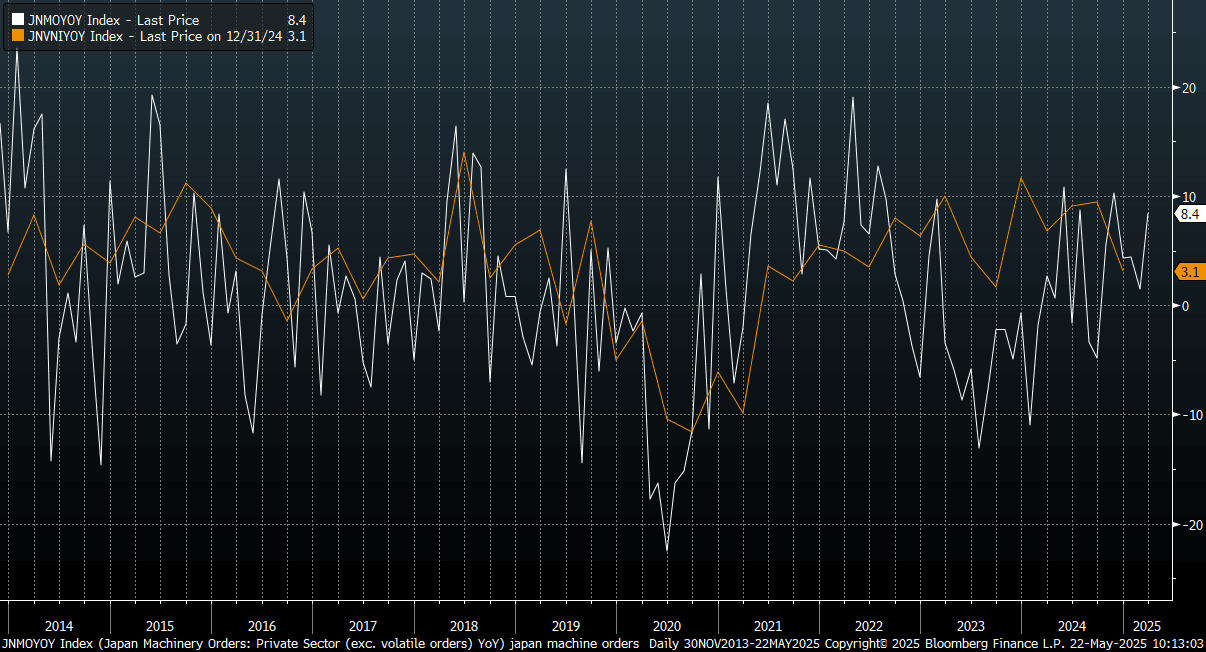

JAPAN DATA: March Core Machine Orders Well Above Estimates

Japan core machine orders for March printed well above market estimates. The m/m outcome was+13% against a -1.6% forecast, while prior was 4.3%. In y/y terms we rose 8.4%, against a -1.8% forecast and 1.5% prior.

- The chart below plots core machine orders (in y/y terms) against Capex in y/y terms from the national accounts. We had the Q1 print for GDP show firmer business spending than forecast, so today's core machine orders print for March reinforces this positive trend for end Q1.

- Still, given the Q2 outlook and beyond is being impacted by tariffs and trade uncertainty, the result is unlikely to shift steady BoJ thinking in the near term.

- The detail showed manufacturing orders up a strong 8.0% in m/m terms.

Fig 1: Japan Core Machine Orders & Capex (Y/Y)

Source: MNI - Market News/Bloomberg

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

US TSYS: Cash Open - Quiet Start

TYM5 is trading 110.24+, down 0-01 from its close.

- Risk turned lower on Monday with concerns that President Trump will fire Fed Chairman Jerome Powell, adding to a market that is already consumed with uncertainty.

- “The US treasury has $60 Billion of extraordinary measures left, in addition to its cash pile, to help keep paying the government's bills.”(per BBG)

- Global GDP may take a $2 Trillion hit by the end of 2027 from Trump’s tariffs, per Bloomberg Economics estimates.

- Russia - Ukraine: Trump said there’s a good chance of a deal being reached this week. A US delegation led by Marco Rubio, Steve Witkoff and Keith Kellogg are slated to meet Ukrainian and European officials in London on Wednesday.

- China has warned countries against striking deals with the US that could hurt Beijing’s interests, putting countries in a position where they will eventually have to pick a side.

- The US 10-year yield has opened in Asia around 4.40%, after closing at 4.4106%.

- Data: The IMF releases its World Economic Outlook

AUSSIE BONDS: Twist-Steepening As Trading Resumes, Trump v Powell In Focus

ACGBs (YM +6.0 & XM -3.0) have twist-steepened after US tsys finished mixed on Monday. The US 2-year yield was down 4bps to 3.76%. The long end was underwater, with the 30-year rate rising 10bps to 4.90% amid inflation angst and fiscal worries. The US 10-year yield ranged between 4.3287% - 4.4185%, closing near the high around 4.41%, 8 bps higher.

- US markets were impacted by ongoing uncertainty over tariffs and rising concerns over Fed independence. President Trump's further verbal attacks on Fed Chair Powell appeared to heighten concerns over the soundness of US assets and unnerved investors.

- Cash ACGBs are 7 bps lower to 1 bp higher with the AU-US 10-year yield differential at -12 bps.

- Swap rates are 6bps lower to 1bp higher, with the 3s10s curve steeper.

- The bills strip has bear-flattened, with pricing +2 to +6.

- RBA-dated OIS pricing is 1-8 bps softer across meetings today. A 50bp rate cut in May is given a 25% probability, with a cumulative 122bps of easing priced by year-end (based on an effective cash rate of 4.09%).

- Today, the local calendar will be empty.

- This week, the AOFM plans to sell A$1000mn of the 3.25% 21 April 2029 bond on Wednesday.

JPY: Eyes Pivotal 140.00 Area

The range on Monday was 142.14 - 140.48, price opens in Asia near the lows around 140.70/80. Price action is very clear, any move back towards risk aversion will see the purchase of JPY accelerate.

- Concerns President Trump will fire Fed Chairman Jerome Powell added to a market that is already consumed with uncertainty.

- “BOJ Officials see little need to change their gradual rate hike stance despite US trade uncertainties, " people familiar said. They are considering cutting inflation forecasts due to a stronger yen and cheaper oil.” (per BBG)

- Prime minister Ishiba Shigeru stated the government will do everything in its power to provide support to small and medium sized businesses affected by the US tariffs.

- Regarding tariff negotiations, he expressed the view that US President Trump places the highest priority on eliminating trade deficits with countries around the world, including Japan.

- Regarding non-tariff barriers on automobiles, about which the US side has expressed dissatisfaction, he said, “ we will work things out properly so that they are not described as unfair,” indicating his intention to consider how to respond. (per BBG)

- The perception of the US is changing and the belief in its exceptionalism is being challenged. If this view pervades, expect the move lower in the USD to intensify and USD/JPY the favourite vehicle to express this in currencies.

- On the day expect sellers back towards 142/143, traders will be watching the long term pivotal area around 140.00 a break would really see this move accelerate opening up a bigger move back to 125/130.

- CFTC data shows Asset managers continuing to add to longs, while leveraged are only just starting to get long.

- USD/JPY: upcoming notable strikes, 140.00($1.61b), 145.00($1.38b) Exp Apr 24 NY cut (Source DTCC).

- Data : The IMF releases its World Economic Outlook tonight.

Fig 1 : USD/JPY CFTC Weekly Data

Source: MNI - Market News/Bloomberg