ASIA STOCKS: India Has Large Outflow

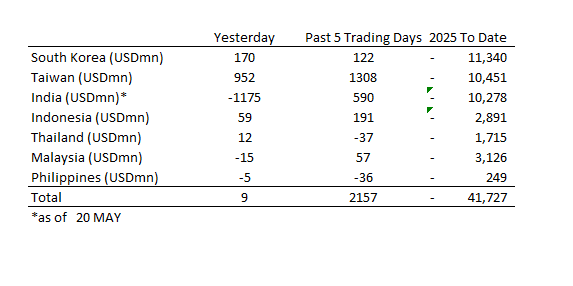

Following five successive days of inflows, India had a substantial outflow on the 20th whilst Taiwan continued to receive inflows.

- South Korea: Recorded inflows of +$170m yesterday, bringing the 5-day total to +$122m. 2025 to date flows are -$11,340. The 5-day average is +$24m, the 20-day average is +$57m and the 100-day average of -$121m.

- Taiwan: Had inflows of +$952m yesterday, with total inflows of +$1,308m over the past 5 days. YTD flows are negative at -$10,451. The 5-day average is +$262m, the 20-day average of +$481m and the 100-day average of -$116m.

- India: Had outflows of -$1,175m as of the 20th, with total inflows of +$590m over the past 5 days. YTD flows are negative -$10,278m. The 5-day average is +$118m, the 20-day average of +$235m and the 100-day average of -$121m.

- Indonesia: Had inflows of +$59m as of yesterday, with total inflows of +$191m over the prior five days. YTD flows are negative -$2,891m. The 5-day average is +$38m, the 20-day average $5m and the 100-day average -$33m

- Thailand: Recorded inflows of +$12m as of yesterday, outflows totaling -$37m over the past 5 days. YTD flows are negative at -$1,715m. The 5-day average is -$7m, the 20-day average of -$15m the 100-day average of -$17m.

- Malaysia: Recorded outflows of -$15m as of yesterday, totaling +$57m over the past 5 days. YTD flows are negative at -$3,126m. The 5-day average is +$2m, the 20-day average of +$41m and the 100-day average of -$22m.

- Philippines: Saw outflows of -$5m as of yesterday, with net outflows of -$36m over the past 5 days. YTD flows are negative at -$249m. The 5-day average is -$7m, the 20-day average of +$2m the 100-day average of -$3m.

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

FOREX: USD Edges Higher, As US Equity Futures Firm

Early G10 FX trends are skewed modestly in favor of the USD, unwinding some of Monday's shifts, albeit only marginally at this stage. The USD BBDXY was last up a little over 0.15%, to be close to 1218.25. A firmer US equity futures backdrop since the open is aiding USD sentiment, particularly against the safe havens.

- The USD BBDXY index is still close to intra-session lows from Monday near 1212, which was fresh lows in the index back to end 2023.

- Eminis and Nasdaq futures are up around 0.30-35% at this stage, but this follows cash losses from Monday trade of more than 2%. Concern around Fed independence weighed notably.

- USD/JPY has risen back above 141.10 in latest dealings, with Monday lows just under 140.50. EUR/USD is down to 1.1490, while USD/CHF is back above 0.8110, these currencies off around 0.20-0.30% versus the USD.

- US yields are mostly lower, with the 10yr back sub 4.40%, after Monday's sharp rise led by the back end of the curve.

- Japan FinMin Kato stated that he is heading to the US today for global meetings, and aims to meet with US Tsy Secretary Bessent and discuss FX.

- Elsewhere Economic Revitalization Minister Akazawa stated that Japan and the US are deciding the scope of trade talks (per BBG). This will remain a key focus point for markets.

- NZD/USD is down around 0.30% as well, last near 0.5980/85, while AUD/USD is back close to 0.6400.

- We had NZ trade data earlier, with another trade surplus recorded, but NZD sentiment wasn't impacted.

- The data calendar is empty for the remainder of today's Asia Pac session.

NEW ZEALAND: NZ Continues To See Strong Export Growth, Outlook Clouded

NZ recorded its third merchandise trade surplus in four months in March at $970mn up from $392mn. The YTD deficit narrowed to $6.13bn from $6.63bn. It has now declined around $11bn since the May 2023 peak. Both export and import growth were robust last month. Trade is a bright spot in NZ’s struggling economy but with a 10% tariff on goods to the US and an escalating US-China trade war the outlook is highly uncertain and likely to be negative.

NZ merchandise trade balance $bn YTD

Source: MNI - Market News/LSEG

- Goods exports rose 0.6% m/m sa and 18.9% y/y with shipments strong to the two largest destinations China (+22.7% y/y) and the US (+21.8% y/y) while they were weak to Australia after a run of solid months (-0.5% y/y).

- Exports to the US have been trending higher since before Covid but they reached a new record level in March, as producers likely wanted to beat the imposition of US tariffs.

- Shipments of milk products, meat and machinery & equipment have driven the strength over the year. There was strong growth in milk products & fruit to China, while to the US it was meat.

- Imports fell 1.9% m/m sa in March but annual growth has been robust rising to 12.4%. The annual strength has been concentrated in consumer goods (+14.7% y/y) and non-transport capex (+8.3% y/y), while transport has been weak down 3% y/y, but does tend to be volatile.

- Q1 merchandise export values rose 11% q/q, while imports were up 4.1% q/q.

NZ goods exports y/y% 3-mth ma

US TSYS: Cash Open - Quiet Start

TYM5 is trading 110.24+, down 0-01 from its close.

- Risk turned lower on Monday with concerns that President Trump will fire Fed Chairman Jerome Powell, adding to a market that is already consumed with uncertainty.

- “The US treasury has $60 Billion of extraordinary measures left, in addition to its cash pile, to help keep paying the government's bills.”(per BBG)

- Global GDP may take a $2 Trillion hit by the end of 2027 from Trump’s tariffs, per Bloomberg Economics estimates.

- Russia - Ukraine: Trump said there’s a good chance of a deal being reached this week. A US delegation led by Marco Rubio, Steve Witkoff and Keith Kellogg are slated to meet Ukrainian and European officials in London on Wednesday.

- China has warned countries against striking deals with the US that could hurt Beijing’s interests, putting countries in a position where they will eventually have to pick a side.

- The US 10-year yield has opened in Asia around 4.40%, after closing at 4.4106%.

- Data: The IMF releases its World Economic Outlook