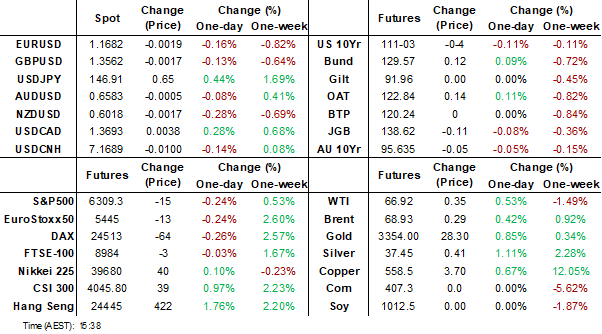

MNI EUROPEAN MARKETS ANALYSIS: USD Supported Amid Tariff Risk

- Early sentiment was dictated by Trump's 35% tariff threat against Canada. USD/CAD spiked higher, while US equity futures fell. We are away from worst levels though as US officials stated that USCMA goods will still be exempt.

- USD/JPY has remained well supported and tested above 147.00. US Tsy yields have edged a little higher, led by the back end. Hong Kong and China equities have outperformed, with multiple support factors in play.

- Looking ahead, focus will be on whether the EU receives its tariff letter from the US later today. On the data front we have UK GDP, along with final French inflation. In the US, the June Federal Budget Balance is out.

MARKETS

US TSYS: Asia Wrap - Yields Edge Higher Led By The Long-End

The TYU5 range has been 111-02+ to 111-08 during the Asia-Pacific session. It last changed hands at 111-03, down 0-04 from the previous close.

- The US 2-year yield has edged higher trading around 3.876%.

- The US 10-year yield has edged higher trading around 4.36%, up 0.01 from its close.

- The 10-year yield has topped out just above the 4.40% area, giving the bulls some reprieve. No clear direction though in the 10-year as it chops around in a wider 4.10% - 4.60% range for most of the year, with the 4.40% area being the pivot. A sustained close back above the 4.45% area could see more of the longs pared back but while this area holds they should be happy to stick with their position looking for a move back to the lower end of the range.

- The Real Fly on X: “FED'S GOOLSBEE SAID HE DOESN’T AGREE WITH CALLS TO CUT RATES JUST TO LOWER GOVERNMENT DEBT COSTS, EMPHASIZING THE FED’S MANDATE IS FOCUSED ON JOBS AND INFLATION. HE ADDED, “THE FED BUILDING IS NOT A LUXURY BUILDING.”

- (Bloomberg) -- “JPMorgan Chase CEO Jamie Dimon said on Thursday he thought the financial market was underestimating the possibility of U.S. interest rates climbing higher, a prospect he described as a “cause for concern.”

- Data/Events: Federal Budget Balance

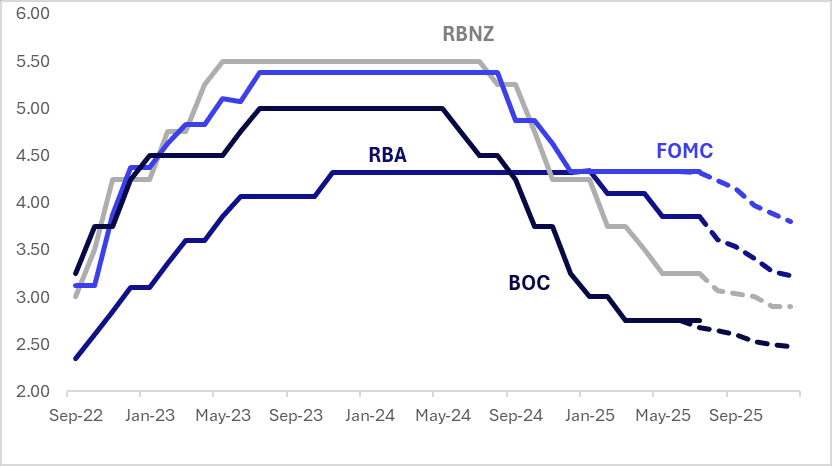

STIR: $-Bloc Markets Little Changed Over Past Week, Except For Australia

Interest rate expectations across dollar-bloc economies were largely unchanged over the past week, except in Australia, where rates firmed by 16bps.

- RBA-dated OIS pricing jumped after the Reserve Bank unexpectedly held the cash rate at 3.85% on Tuesday. The Board judged inflation risks to be more balanced and noted the continued strength of the labour market, but remained cautious due to persistent uncertainty around demand and supply. It opted to wait for further data to confirm that inflation is on track to return to the 2.5% target. The decision was made by a 6–3 majority.

- Markets had assigned a 92% probability to a 25bp cut ahead of the announcement. As of writing, pricing across meetings is 9–19bps firmer than before Tuesday’s decision.

- On Wednesday, the RBNZ held the OCR steady at 3.25%, as widely expected, with just 4bps of easing priced in. The Committee considered two options: a 25bp cut or no change. The case for easing was driven by concerns over weakening economic momentum, but the decision to hold reflected elevated uncertainty. As the RBNZ noted, “Some members emphasised that waiting would allow the Committee to assess whether weakness in the domestic economy persists, and how inflation and inflation expectations evolve.”

- Looking ahead, the next key events for the region are the FOMC and BoC meetings on July 30, with markets pricing just a 5% chance of a 25bp cut.

- Looking ahead to December 2025, current market-implied policy rates and cumulative expected easing are as follows: US (FOMC): 3.80%, -53bps; Canada (BOC): 2.47%, -28bps; Australia (RBA): 3.22%, -63bps; and New Zealand (RBNZ): 2.90%, -35bps.

Figure 1: $-Bloc STIR (%)

Source: Bloomberg Finance LP / MNI

JGBS: Bull-Flattener To End The Week, Tariffs Remain In Focus

JGB futures are slightly weaker, -7 compared to the settlement levels.

- The local calendar has been empty today.

- MNI Policy: BOJ to Reaffirm Downside Risks, Up FY25 Inflation - The BOJ's board is set to reaffirm downside risks to the economy and prices outlined in May 1 Outlook Report at its July 30-31 meeting, though officials may increase their median CPI forecast for FY25 from 2.2% partly due to a temporary surge in rice prices, MNI understands.

- (Bloomberg) Japan's top tariff negotiator Ryosei Akazawa may face pressure as US Treasury Secretary Scott Bessent and Commerce Secretary Howard Lutnick visit Osaka, but it's unclear if they will meet with him for trade talks.

- Cash US tsys are slightly cheaper, with a steepening bias, in today's Asia-Pac session. This morning US equity futures gave back all their overnight gains as Trump set a 35% tariff rate for Canada starting on the 1st of August. That said, risk sentiment has since stabilised to a degree. Today's US calendar will see the Federal Budget Balance.

- The cash JGB curve has twist-flattened, with yields 1bp higher to 2bps lower.

- Swap rates are flat to 2bps lower.

- On Monday, the local calendar will see Core Machine Orders, Industrial Production, Capacity Utilisation and Tertiary Industry Index.

AUSSIE BONDS: Cheaper On A Subdued Data Light Session

ACGBs (YM -4.0 & XM -4.5) are weaker on a subdued data-light session.

- Cash US tsys are slightly cheaper, with a steepening bias, in today's Asia-Pac session.

- This morning US equity futures gave back all their overnight gains as Trump sets a 35% tariff rate for Canada starting on the 1st of August. That said, risk sentiment has since stabilised to a degree. Today’s US calendar will see the Federal Budget Balance.

- Cash ACGBs are 3-4bps cheaper with the AU-US 10-year yield differential at -4bps.

- The bills strip is -1 to -3 across contracts, with a steepening bias.

- RBA-dated OIS pricing is little changed across meetings today. A 25bp rate cut in August is given an 89% probability, with a cumulative 61bps of easing priced by year-end.

- As of writing, pricing across meetings is 9–19bps firmer than prior to Tuesday’s RBA decision.

- On Monday, the local calendar will be empty, ahead of Westpac Consumer Confidence on Tuesday.

- Next week, the AOFM plans to sell A$300mn of the 4.75% 21 June 2054 bond on Tuesday, A$800mn of the 4.25% 21 March 2036 bond on Wednesday and A$1100mn of the 1.00% 21 November 2031 bond on Friday.

BONDS: NZGBS: Closed Little Changed, 10Y Outperforms $-Bloc

NZGBs closed little changed after a subdued session of trading. Ranges across benchmarks were restricted to 2-3bps.

- The NZGB 10-year did, however, outperform its $-bloc counterparts, with the NZ-US and NZ-AU yield differentials tighter by 2bps and 4bps respectively.

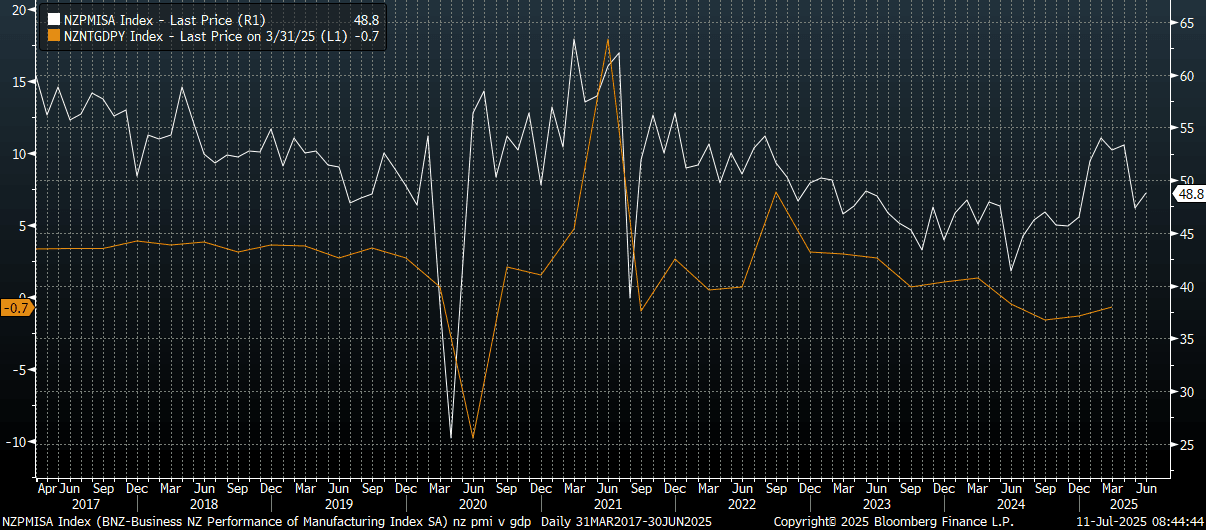

- The New Zealand BusinessNZ manufacturing PMI pushed higher in June to 48.8, after a revised 47.4 read in May. The improvement is welcome, but we still sit below the 50.0 expansion/contraction line, while Feb highs of 54.0 for the index are also some distance away.

- Cash US tsys are slightly cheaper, with a steepening bias, in today's Asia-Pac session.

- “Risk sentiment has stabilised to a degree post the earlier Trump headlines around a 35% tariff on Canada. Subsequent headlines from US officials noted that Trump will keep the tariff exemption for USMCA goods.” (per BBG)

- Swap rates closed showing a modest twits-steepener, with rates 1bp lower to 1bp higher.

- RBNZ dated OIS pricing closed little changed across meetings. 18bps of easing is priced for August, with a cumulative 33bps by November 2025.

- On Monday, the local calendar will see the Performance Services Index and Card Spending data.

NEW ZEALAND: PMI Up, But Still Well Off Recent Highs, New Orders Bounce

The New Zealand BusinessNZ manufacturing PMI pushed higher in June to 48.8, after a revised 47.4 read in May. The improvement is welcome, but we still sit sub the 50.0 expansion/contraction line, while Feb highs of 54.0 for the index are also some distance away.

- In terms of the detail, the sub index trends were mixed. Production rose to 48.6, from 47.9, while employment edged up to 47.9 from 45.5. Both these indices are well off recent highs though.

- More encouraging was the bounce in new orders too 51.2 from 45.4 in May. This may hint at better momentum going forward. Finished stocks fell to 46.9.

- Still, BNZ noted: "All sub indexes are well below historic averages and overall PMI “adds to the swathe of data that is suggesting the New Zealand economy stalled in 2q”: BNZ senior economist Doug Steel. (via BBG)

- The chart below plots the headline PMI versus NZ GDP y/y growth. The RBNZ held rates steady earlier this week, but maintained an easier bias (and considered cutting rates by 25bps due to the weaker growth backdrop in recent months).

- Note next Monday we get the services PMI for June, along card spending, which can also help inform the end Q2 growth picture.

Fig 1: NZ Manufacturing PMI Versus NZ GDP Y/Y

Source: Bloomberg Finance L.P./BNZ/MNI

FOREX: Asia FX Wrap - BBDXY Probing The 1200 Area Again

The BBDXY has had a range of 1195.93 - 1199.76 in the Asia-Pac session, it is currently trading around 1199, +0.22%. Price action is interesting though in that it is not violently moving lower from these bouts of strength as it did in the past. The price does look stretched and the market is short so a correction is not out of the question. "CHINA'S WANG YI: US ABUSES TARIFF, UNDERMINES FREE TRADE SYSTEM" BBG

- EUR/USD - Asian range 1.1665 - 1.1707, Asia is currently trading 1.1675. The pair has again seen solid demand again just below the 1.1700 area in our session, can this hold overnight ? The price is still starting to look a little stretched in the short term and is vulnerable to any correction in the USD, first support is back towards 1.1600 then more importantly the 1.1450 area.

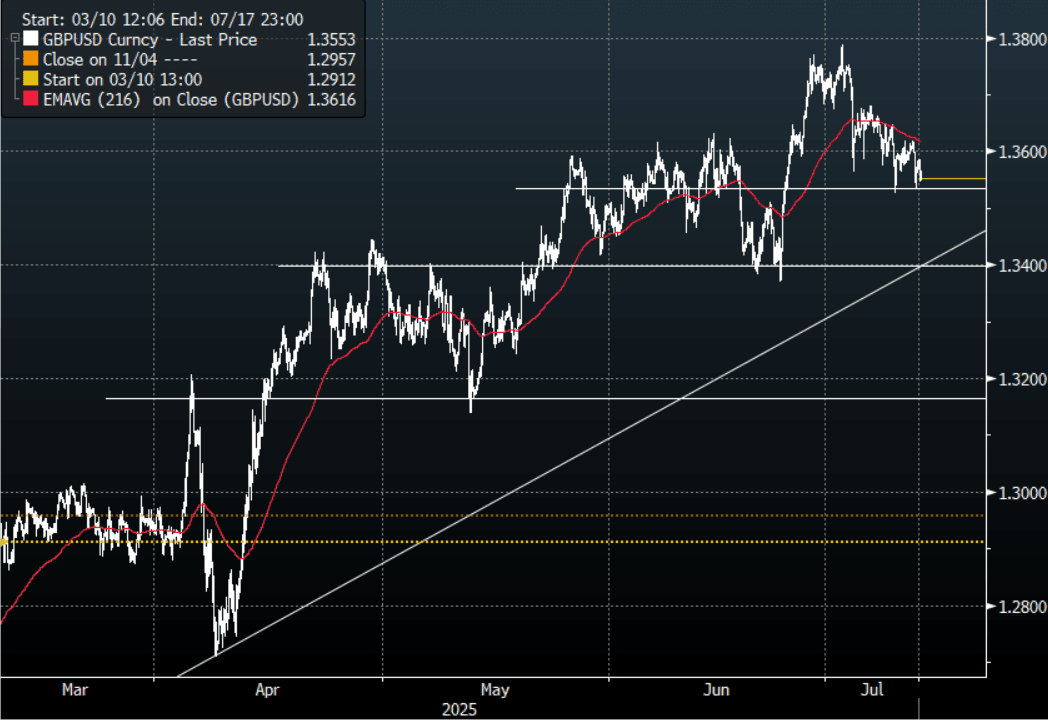

- GBP/USD - Asian range 1.3545 - 1.3586, Asia is currently dealing around 1.3555. Decent demand continues to be seen back towards the 1.3500 area. Price has rejected the move higher but the USD would need to gain momentum higher for GBP/USD to extend lower in the short-term. First support around 1.3500 a break below here would signal a deeper pullback to the more important 1.3350/1.3400 area.

- USD/CNH - Asian range 7.1679 - 7.1834, the USD/CNY fix printed 7.1475, Asia is currently dealing around 7.1700. Sellers should be around on bounces while price holds below the 7.2500 area and the PBOC manages the fix lower.

- Cross asset : SPX -0.25%, Gold $3330, US 10-Year 4.36%, BBDXY 1199, Crude oil $66.75

- Data/Events : Germany wholesale Price Index, France CPI

Fig 1: GBP/USD Spot Hourly Chart

Source: MNI - Market News/Bloomberg Finance L.P

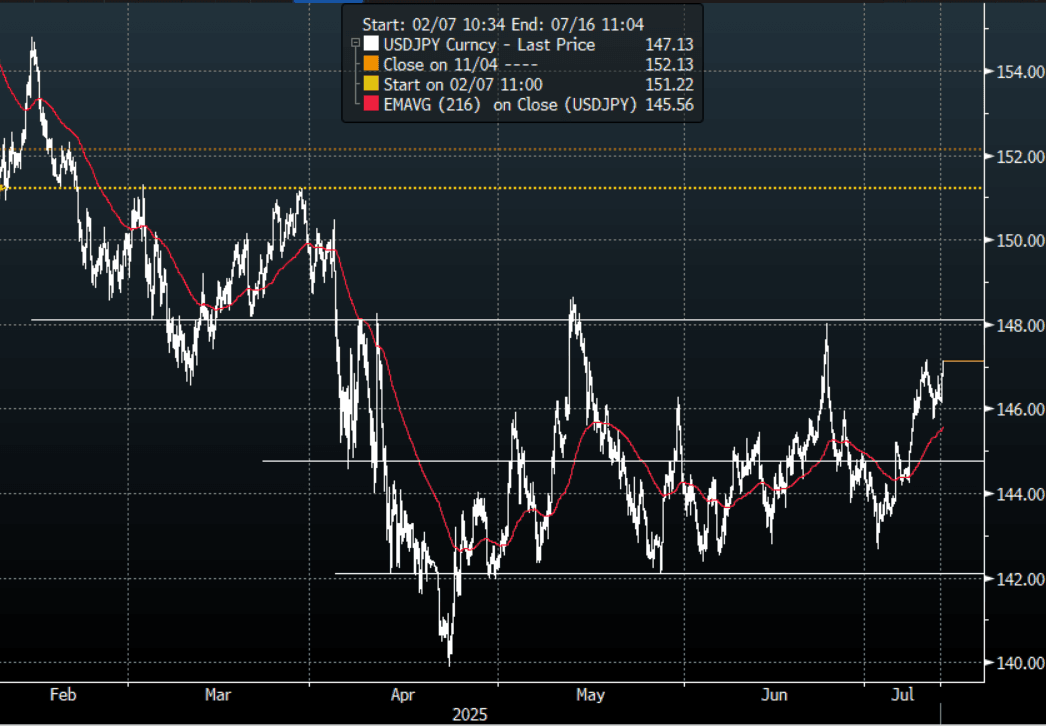

JPY: Asia Wrap - USD/JPY Finds Demand, Back Challenging JPY longs Above 147.00

The Asia-Pac USD/JPY range has been 146.14 - 147.15, Asia is currently trading around 147.15, +0.60%. The pair has traded better bid for most of our session and is back to testing above the 147.00 area . The USD/JPY relentless march higher has been pretty telling, challenging a market positioned the wrong way. Price is now consolidating some of those recent gains, dips back towards 144.50/145.00 should now find support first up. The previous 2 forays towards the top of the range were both rejected very quickly; this time it seems to be hanging around for now implying it might have more to play out. The JPY crosses are breaking higher as well adding to the headwinds for JPY longs.

- MNI Policy: BOJ to Reaffirm Downside Risks, Up FY25 Inflation - The BOJ’s board is set to reaffirm downside risks to the economy and prices outlined in May 1 Outlook Report at its July 30-31 meeting, though officials may increase their median CPI forecast for FY25 from 2.2% partly due to a temporary surge in rice prices, MNI understands.

- "S.KOREA, US, JAPAN HOLD JOINT DRILLS, INVOLVING BOMBER: YONHAP" - BBG

- "TACHIBANA: SPEEDING UP PROCESS FOR RESUMING CHINA BEEF EXPORTS” - BBG

- USD/JPY has lost all downside momentum for now and is back in its wider 142.00 - 148.00 range. The Market is long JPY and should the USD manage to continue to correct higher the risk is a move back to the top end of the range to further challenge the conviction of the shorts.

- Options : Close significant option expiries for NY cut, based on DTCC data: 146.30($648m).Upcoming Close Strikes : 146.50($1.25b July 16).

Fig 1 : USD/JPY Spot Hourly Chart

Source: MNI - Market News/Bloomberg Finance L.P

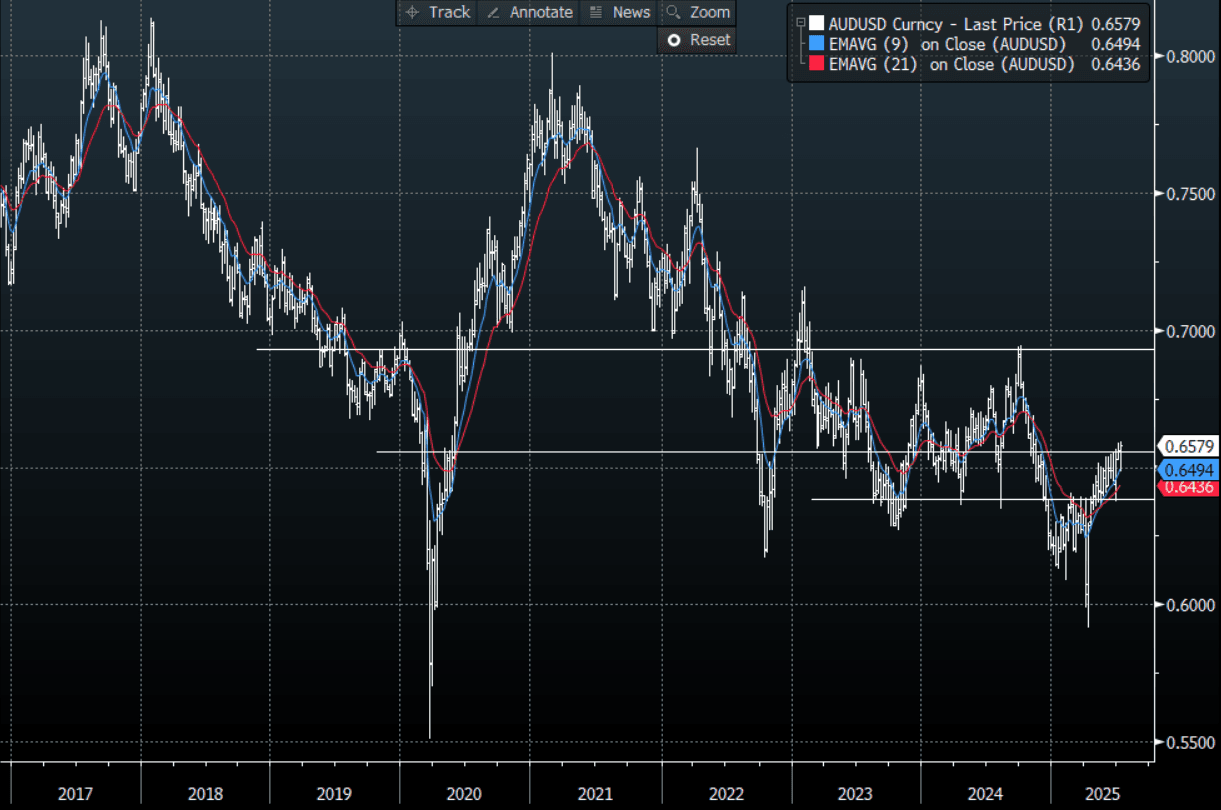

AUD: Asia Wrap - AUD/USD Finds Demand On Canada Tariff Dip

The AUD/USD has had a range of 0.6556 - 0.6595 in the Asia- Pac session, it is currently trading around 0.6580, -0.12%. The pair dropped quickly on Trump's announcement of a 35% tariff on Canada, risk later stabilised as new headlines expanded that Trump will keep tariff exemption on USMCA goods and AUD clawed back nearly all of its losses. The AUD outperformed across the board overnight and might point to some reduction of the market shorts it has been running, the CFTC data next week should offer a clue. Can the AUD/USD now break above 0.6600 and gain the momentum it needs to build for a bigger move higher back towards 0.6900/0.7000.

- (Bloomberg) -- “Risk Stabilizes, Trump Will Keep Tariff Exemption On USMCA Goods: Risk sentiment has stabilized to a degree post the earlier Trump headlines around a 35% tariff on Canada. Subsequent headlines from US officials noted that Trump will keep the tariff exemption for USMCA goods.”

- 'PRICED: IFC A$300 Million Tap of May 2030 Kangaroo Social Bond' -BBG

- The AUD/USD continues to hold above its support around 0.6500, looks like it's back to the 0.6500 - 0.6600 range and it should now take its cues from the USD. Watching to see if the market can build on this outperformance and break above 0.6600.

- Options : Closest significant option expiries for NY cut, based on DTCC data: 0.6650(AUD599m), 0.6700(AUD 315m). Upcoming Close Strikes : 0.6560(AUD631m July 15), 0.6495(AUD611m July15), 0.6700(AUD611m July 16).

- CFTC Data shows last week Asset managers pared back their shorts slightly -35992, the Leveraged community maintained their shorts -22903.

- AUD/JPY - Today's range 95.98 - 96.81, it is trading currently around 96.70, +0.40%. The pair has again tested above 96.00 and this time looks to be building real momentum to extend higher. The market has been caught wrong-footed in both legs of this pair and price action suggests a potential move back to 99.00/100.00.

Fig 1: AUD/USD spot Weekly Chart

Source: MNI - Market News/Bloomberg Finance L.P

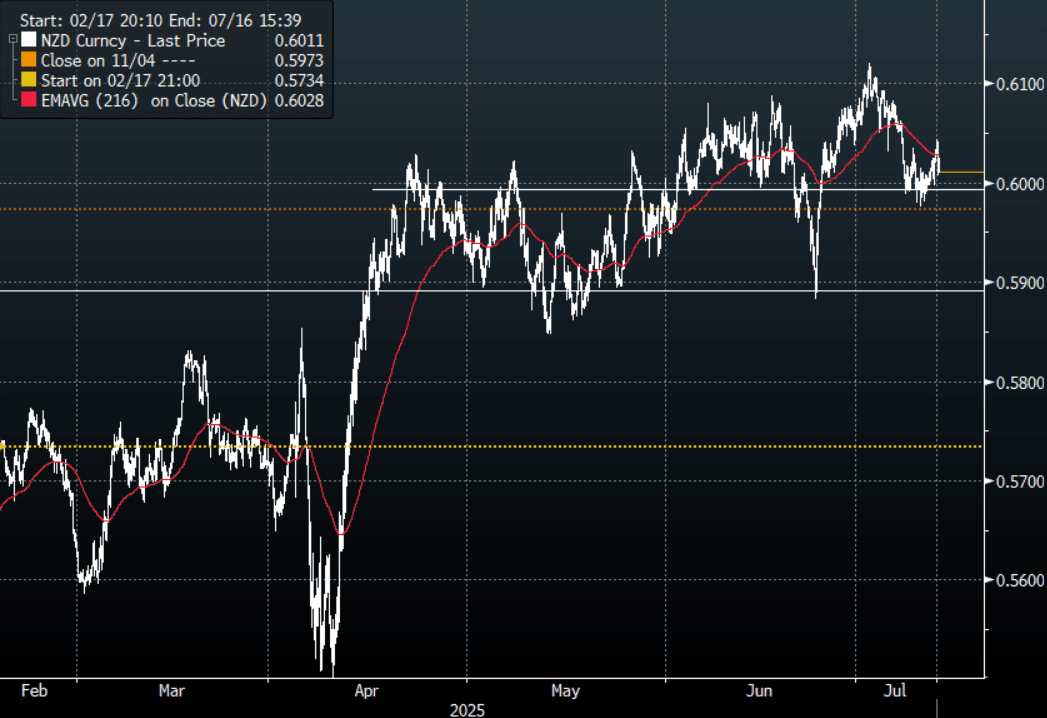

NZD: Asia Wrap - NZD/USD Edges Lower On Canada Tariff, Testing 0.6000 Support

The NZD/USD had a range of 0.6008 - 0.6044 in the Asia-Pac session, going into the London open trading around 0.6015, -0.38%. The pair dropped lower on the Canada tariff headlines but unlike the AUD has not regained all its losses subsequent to clarification that USMCA goods will be exempt. The NZD/USD continues to find good demand towards the 0.6000 area and will need to hold above this support for the Bulls to gain confidence the NZD can build some momentum to push higher once more.

- (Bloomberg) -- “Risk Stabilizes, Trump Will Keep Tariff Exemption On USMCA Goods: Risk sentiment has stabilized to a degree post the earlier Trump headlines around a 35% tariff on Canada. Subsequent headlines from US officials noted that Trump will keep the tariff exemption for USMCA goods.”

- NZ PMI Up, But Still Well Off Recent Highs, New Orders Bounce: The New Zealand BusinessNZ manufacturing PMI pushed higher in June to 48.8, after a revised 47.4 read in May. The improvement is welcome, but we still sit sub the 50.0 expansion/contraction line, while Feb highs of 54.0 for the index are also some distance away.

- Options : Closest significant option expiries for NY cut, based on DTCC data: none. Upcoming Close Strikes : none.

- CFTC Data showed last Asset Managers have reduced their newly built longs in NZD +8515, the Leveraged community reduced their short last week -8424.

- AUD/NZD range for the session has been 1.0908 - 1.0938, currently trading 1.0935. The cross has broken out of its recent range and focus will now turn to the more pivotal 1.0900/50 area.

Fig 1: NZD/USD Spot Hourly Chart

Source: MNI - Market News/Bloomberg Finance L.P

ASIA STOCKS: Little Spill Over From Canada Tariff Threat, China & HK Outperform

Fallout from Trump's 35% tariff threat on Canada has been negligible so far in Asia Pac markets. Markets seemingly happy to take increased tariff risks in its stride. Earlier reports (from an NBC interview) with US President Trump indicated a baseline reciprocal tariff in the 15-20% region (so higher than the paused 10% amount) US equity futures fell as these headlines crossed, but are up from lows. Eminis were last down by around 0.20% (we were off over 0.50% at one stage). In the region continued gains for Hong Kong and China markets have been the standout.

- There look to be a number of factors driving the China/HK equity market rebound. Potential US-China talks cited as one positive, with US Secretary of State Rubio to meet with China's Wang Yi in Malaysia today cited as one factor (this could lead to a Trump-XI meeting later this year). Attractive valuations for China stocks relative to HK could also be in play. Goldman Sachs also raised Hong Kong stocks to market weight, and raised the outlook for the MSCI Asia Pac ex Japan index (via BBG).

- At the break, HK's HSI is up 1.9%, while the CSI 300 is up +1.1%, putting the index above 4050, which is fresh highs back to Dec last year.

- Elsewhere, Japan markets are mixed, the Topix +0.60%, but NKY 225 down slightly. The recent rally in South Korean and Taiwan stocks has slowed, but these bourses are still in the green at this stage.

- In South East Asia, the standout is Thailand markets, up over 1%, but after being out yesterday this could reflect some catch up.

- Other markets in the region are tracking higher, except for India.

ASIA STOCKS: Inflow Momentum Positive For South Korea & Taiwan, Tech Gains Help

Yesterday still saw decent inflow momentum for the likes of South Korea and Taiwan, see the table below. South Korea's Kospi continues to rally, amid further reform hopes, with broader global gains in the tech space, also a positive. For Taiwan's market, similar global drivers are in play, while bellwether TSMC continues to post firm sales momentum, aiding hopes AI related chip demand will remain strong.

- Both of these markets have more than offset outflows seen in other parts of the region. A risk remains from the escalation in trade tensions, with Trump's 35% tariff threat against Canada weighing on sentiment today (US equity futures are down, while offshore inflows into South Korea markets have been pared).

- Outside of South Korea and Taiwan (along with modestly positive into momentum into India), the rest of the region hasn't seen positive inflow over the past 5 trading days.

Table 1: EM Asia Equity Flows

| Yesterday | Past 5 Trading Days | 2025 To Date | |

| South Korea (USDmn) | 454 | 320 | -8871 |

| Taiwan (USDmn) | 371 | 408 | -2557 |

| India (USDmn)* | 78 | 210 | -7903 |

| Indonesia (USDmn) | -24 | -172 | -3530 |

| Thailand (USDmn)* | 0 | -51 | -2433 |

| Malaysia (USDmn) | -10 | -99 | -2769 |

| Philippines (USDmn) | -10 | -10 | -563 |

| Total (USDmn) | 859 | 605 | -28626 |

| * Data Up To July 9 |

Source: Bloomberg Finance L.P./MNI

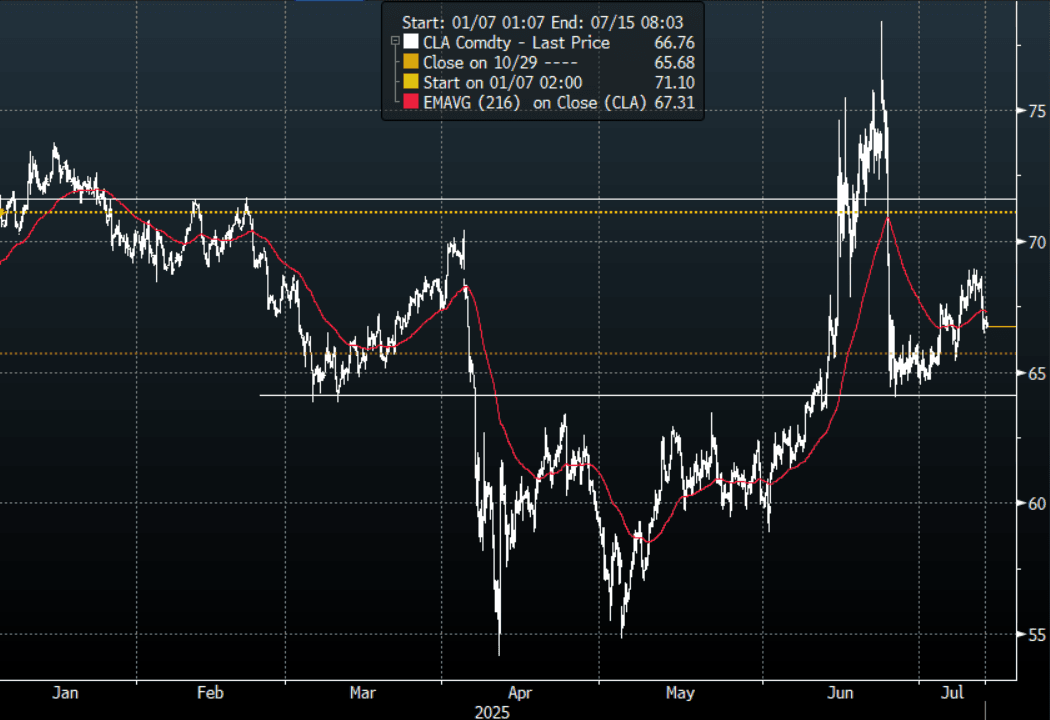

OIL: Consolidates In Asia After Overnight Move Lower

The overnight range for the CLQ5(WTI) contract was $66.45 - $68.65, it is currently trading around $66.76 in the Asia-Pac session. Oil had a decent move lower as Opec discussed a potential pause to further production increases, potentially pointing to lower energy demands.

- (Bloomberg) -- “President Donald Trump said he planned to make a “major statement” on Russia, as the US prepares to send more weapons to Ukraine. In addition, Trump said he expected the Senate to pass a tougher Russia sanctions bill sponsored by Senator Lindsey Graham of South Carolina. ”

- “OPEC+ is discussing a pause in further supply rises from October after its next monthly hike, according to delegates familiar with the matter.”

- “In futures, oil steadied after falling more than 2% on Thursday as investors weighed the fallout from President Donald Trump’s tariffs and OPEC+ supply.” - BBG

- Brent front-month futures fell 2.2% to $68.64 a barrel on the ICE Futures Europe exchange. It is currently trading $68.80 as we head into the London session.

Fig 1: WTI Crude Future Hourly Chart

Source: MNI - Market News/Bloomberg Finance L.P

GOLD: Slightly Higher As Market Weighs New Tariffs Due On Aug 1

Gold is 0.3% higher in today’s Asia-Pac session, after closing 0.3% higher at $3324.05 on Thursday.

- Gold has struggled for direction as traders focused on tariff threats from President Donald Trump and the outlook for US monetary policy. The president proposed a slew of country-specific tariffs this week, including moves against Canada and Brazil, while pushing the overall deadline for implementation to Aug. 1. In addition, he’s planning a substantial levy on imports of copper.

- Elsewhere, investors were considering the outlook for US interest rates. Fed Bank of San Francisco President Mary Daly said she still views two reductions as likely, with a greater chance that the price effects from tariffs may be more muted than anticipated.

- Lower rates are typically positive for gold, which doesn’t pay interest.

- According to MNI’s technicals team, support to watch is the bear trigger at $3,248.7, the June 30 low. On the upside, a resumption of gains would refocus attention on $3,451.3, the June 16 high.

ASIA FX: Mixed Session, CNH Supported By Equities, THB Rebounds, MYR Lags

Asian currencies have traded in a mixed fashion in the first part of Friday trade. In NEA trends are mixed, with CNH firmer but KRW down slightly. In SEA, Thailand markets have returned, with THB rebounding, while in other parts of the region the USD has been modestly firmer. Early focus was on USD gains against the majors, as US President Trump threatened Canada with 35% tariffs, but spill over to USD/Asia pairs was fairly limited.

- USD/CNH has tested sub 7.1700 in the first part of Friday trade. We continue to see the USD/CNY fixing trend lower, which is biasing the pair lower and/or driving outperformance on key crosses. Mostly notable this past week has been CNH/JPY, with the pair break above 20.51 today. The better global equity tone, with China markets rallying strongly today (amid multiple supports) is aiding gains in this cross. For USD/CNH we are still within recent ranges.

- Spot USD/KRW has drifted a little higher last around the 1375 level, so still sub recent highs. USD/JPY gains have likely spilled over to the won, while the onshore equity rally has cooled. Early July trade data pointed to positive export growth trends.

- USD/TWD is little changed, last near 29.20, while USD/HKD is still near 7.8500, despite further HKMA intervention and rising Hibor rates.

- USD/THB has fallen by around 0.40%, putting the pair last near 32.55. This is still up from recent lows close to 32.30.

- USD/MYR has firmed, last close to 4.2580, maintaining a recent uptrend. May IP in Malaysia was below expectations at +0.35y/y, versus +2.1% forecast and 2.7% prior.

- USD/IDR is little changed, holding close to 16220 in latest dealings.

UP TODAY (TIMES GMT/LOCAL)

| Date | GMT/Local | Impact | Country | Event |

| 11/07/2025 | 0600/0700 | *** | UK Monthly GDP | |

| 11/07/2025 | 0600/0700 | ** | Trade Balance | |

| 11/07/2025 | 0600/0700 | ** | Index of Services | |

| 11/07/2025 | 0600/0700 | ** | Index of Production | |

| 11/07/2025 | 0600/0700 | ** | Output in the Construction Industry | |

| 11/07/2025 | 0645/0845 | *** | HICP (f) | |

| 11/07/2025 | 1130/1330 | ECB Cipollone At Ukraine Recovery Conference | ||

| 11/07/2025 | - | *** | Money Supply | |

| 11/07/2025 | - | *** | New Loans | |

| 11/07/2025 | - | *** | Social Financing | |

| 11/07/2025 | 1230/0830 | *** | Labour Force Survey | |

| 11/07/2025 | 1230/0830 | * | Building Permits | |

| 11/07/2025 | 1230/0830 | *** | Labour Force Survey | |

| 11/07/2025 | 1600/1200 | *** | USDA Crop Estimates - WASDE | |

| 11/07/2025 | 1700/1300 | ** | Baker Hughes Rig Count Overview - Weekly | |

| 11/07/2025 | 1700/1300 | ** | Baker Hughes Rig Count Overview - Weekly | |

| 11/07/2025 | 1800/1400 | ** | Treasury Budget |