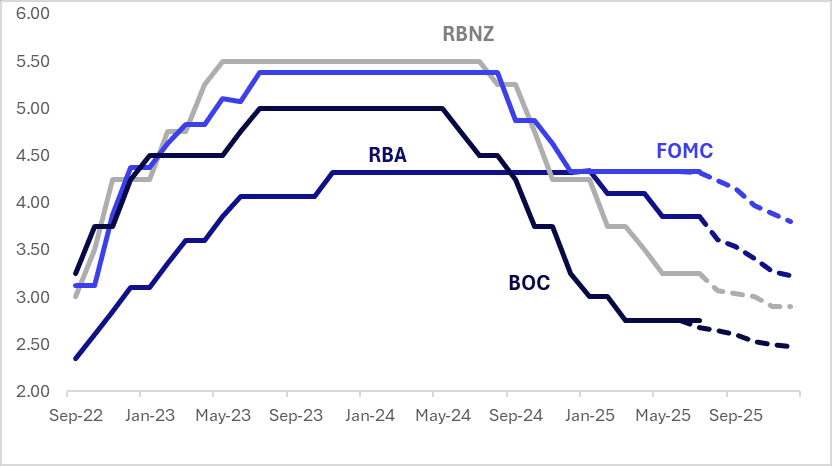

STIR: $-Bloc Markets Little Changed Over Past Week, Except For Australia

Interest rate expectations across dollar-bloc economies were largely unchanged over the past week, except in Australia, where rates firmed by 16bps.

- RBA-dated OIS pricing jumped after the Reserve Bank unexpectedly held the cash rate at 3.85% on Tuesday. The Board judged inflation risks to be more balanced and noted the continued strength of the labour market, but remained cautious due to persistent uncertainty around demand and supply. It opted to wait for further data to confirm that inflation is on track to return to the 2.5% target. The decision was made by a 6–3 majority.

- Markets had assigned a 92% probability to a 25bp cut ahead of the announcement. As of writing, pricing across meetings is 9–19bps firmer than before Tuesday’s decision.

- On Wednesday, the RBNZ held the OCR steady at 3.25%, as widely expected, with just 4bps of easing priced in. The Committee considered two options: a 25bp cut or no change. The case for easing was driven by concerns over weakening economic momentum, but the decision to hold reflected elevated uncertainty. As the RBNZ noted, “Some members emphasised that waiting would allow the Committee to assess whether weakness in the domestic economy persists, and how inflation and inflation expectations evolve.”

- Looking ahead, the next key events for the region are the FOMC and BoC meetings on July 30, with markets pricing just a 5% chance of a 25bp cut.

- Looking ahead to December 2025, current market-implied policy rates and cumulative expected easing are as follows: US (FOMC): 3.80%, -53bps; Canada (BOC): 2.47%, -28bps; Australia (RBA): 3.22%, -63bps; and New Zealand (RBNZ): 2.90%, -35bps.

Figure 1: $-Bloc STIR (%)

Source: Bloomberg Finance LP / MNI

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

AUSSIE BONDS: Bear-Flatter But Narrow Ranges Ahead Of US CPI

ACGBs (YM -4.0 & XM -1.5) are weaker after dealing in narrow ranges on a local-data-light session.

- There has been limited market reaction to the headlines coming from US-China trade talks, with the main takeaway being that the Geneva consensus was also agreed to by both sides. The US side appeared confident that this would see rare earth flows increase from China to the US (leaders from both China and the US still have to agree to implement the outcome of the talks).

- Cash US tsys are ~1bp richer in today’s Asia-Pac session ahead of today’s CPI data. Analyst unrounded estimates see core CPI inflation accelerating mildly to 0.27% M/M (median, 0.28% average) in May after 0.24% M/M in April. (See link)

- Cash ACGBs are 2-4bps cheaper with a flatter curve and the AU-US 10-year yield differential at -20bps.

- Today’s auction of A$1000mn of the Nov-32 bond saw the weighted average yield print 0.65bps below prevailing mid-yields. However, the cover ratio declined to 3.2100x from 3.4786x in the previous auction.

- The bills strip has bear-steepened, with pricing -1 to -3.

- RBA-dated OIS pricing is firmer across meetings today. A 25bp rate cut in July is given a 79% probability, with a cumulative 72bps of easing priced by year-end.

CHINA: Local Equities Recoup Yesterday's Losses, CNH Outperforming USD Uptick

China stocks markets are outperforming the softer US equity futures trend, as the market digests earlier headlines around US-China trade talks. The CSI 300 was last up around 0.70%, putting the index back near 3890/95. Earlier highs were at 3911.61, which was still below recent highs recorded in May for the index.

- Recall late yesterday that China and Hong Kong equities came under pressure, with some chatter around uncertainty of trade talk outcomes weighing on sentiment. The CSI 300 finished down 0.51% yesterday, so catch up today is not surprising, given the trade talks have still delivered positives.

- BBG also notes brokerage and financial stocks outperforming today, ahead of the upcoming Lujiazui forum in Shanghai (held June 18-19), where more support for financial related firms may be announced.

- Rare earth related companies are also outperforming, with the US side expressing confidence that flows of these critical minerals will pick up to the US.

- USD/CNH is little changed through, last near 7.1880, with better onshore equities not seeing positive spill over to CNH at this stage. It is outperforming broader G10 trends through, where the USD has mostly ticked higher. The BBDXY index was last +0.15%.

- The modestly negative reaction for US equity futures may reflect lack of announcements around the broader tariff outlook, with the recent discussions focused on getting what was agreed to in Geneva in may back on track.

JGBS: Cash Bonds Little Chnaged, PPI Below Estimates

In Tokyo morning trade, JGB futures are stronger, +9 compared to settlement levels.

- Japan's May PPI was below market expectations, falling 0.2% m/m (against a +0.2% forecast). April's rise was revised to +0.3% (from 0.2%). In y/y terms, we printed 3.2%, against a 3.5% forecast (prior was 4.1%). In terms of the detail, manufacturing PPI was down 0.4%m/m. Weakness was evident in commodities, particularly petroleum, coal (-4.8%m/m). Iron ore and steel were also down in m/m terms. Import prices for commodities were down 1.1%m/m, continuing a negative trend, now off 10.3% in y/y terms.

- There has been limited market reaction to the headlines coming from US-China trade talks, with the main takeaway being that the Geneva consensus was agreed to by both sides. The US side appeared confident that this would see rare earth flows increase from China to the US (leaders from both China and the US still have to agree to implement the outcome of the talks).

- Cash US tsys are slightly richer in today’s Asia-Pac session ahead of today’s CPI data.

- Cash JGBs are slightly mixed across benchmarks, with a mild steepening bias. The benchmark 10-year yield is 0.6bps lower at 1.472% versus the cycle high of 1.596%.

- Swap rates are flat to 1bp lower. Swap spreads are tighter.