MNI EUROPEAN MARKETS ANALYSIS: USD Mostly Higher As Oil Rises

- Oil benchmarks are up around 3.5%, with news flow continuing to support prices - the US Treasury announcing sanctions on large Russian oil producers and reports that this will mean Indian imports of Russian crude will trend towards zero.

- The USD is higher, particularly against yen, although USD/JPY hasn't breached mid Oct highs. US yields are edging higher, mindful of the correlation with oil prices. As expected the BOK left rates on hold. A number of USD/Asia pairs have broken higher, with the oil move likely helping dollar sentiment.

- Later US September existing home sales and October Kansas Fed manufacturing print as well as August Canadian retail sales and euro area preliminary October consumer confidence. The Euro summit takes place and ECB’s Lane speaks.

MARKETS

US TSYS: Yield Rally Grinds to a Halt, US 10-Yr Consolidates Below 4.00%

The US 10-Yr bond future TYZ5 has done very little in the trading session in Asia, down -01 at 113-24+ as the grind lower in yields appears to take a breather.

Cash bonds had opened with a modest bid tone, which fell away leaving yields largely unchanged from the open.

- The US 2-Yr is unchanged at the open at 3.44%

- The US 5-Yr also fell by -1bp to 3.55%

- The US 10-Yr is at 3.94% with the sub 4.00% range now seemingly in place, as the government shut down drags on. We look now to near term lows of 3Q '24 as potential targets for the 10-Yr of 3.60 - 3.70%

- The US 30-Yr continues to perform down at 4.53%.

Tonight the market will focus on Initial Jobless Claims and Continuing Claims as key data releases, with other data impacted by the government shutdown. Issuance highlights are a 5-Yr US$26bn TIPS auction, upsized by $3bn from the last issue.

Renewed money market strains will prompt the Federal Reserve to end quantitative tightening soon and resume asset purchases within six to 12 months after that, former Fed Board economist Jonathan Wright told MNI. Key short-term borrowing rates spiked about 10 basis points last Wednesday, the same day as a large Treasury coupon settlement, and stayed elevated Thursday as banks tapped the Fed’s standing repo facility, a backstop that provides cash in exchange for U.S. Treasuries and agency bonds. "It looks to me like we’re at about the same place as early 2019, where there are signs of trouble on the horizon but nothing you can call turmoil in money markets yet. But continuing to reduce the amount of bank reserves will at some point get us to a steep part of the demand curve – at least on some days – and run a risk of a repeat of what happened in September 2019," Wright, an economist at Johns Hopkins University, said in an interview.

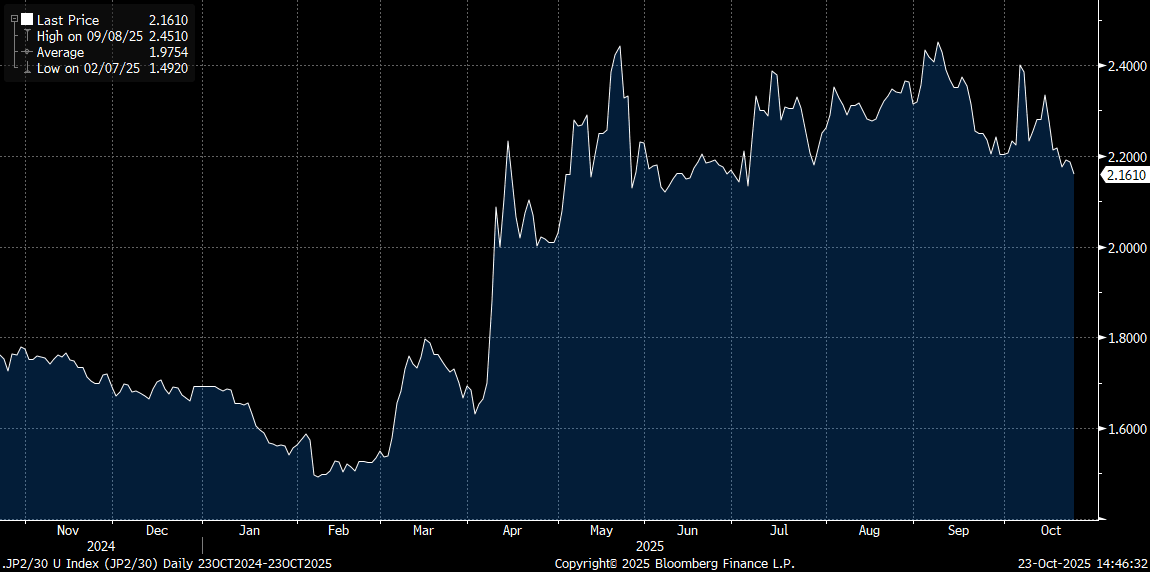

JGBS: 2/30s Curve Flattest Since Early July, Sep CPI Due Tomorrow

JGB futures sit at 136.17, +.01 versus settlement levels in latest dealings, after a 136.11-136.32 range so far today. For JGB futures we are maintaining familiar ranges for now, with US Tsy futures generally biased higher, whilst fiscal concerns in Japan may be limiting the upside (albeit with such fears dissipating somewhat so far this week). The other focus point today has been the oil price spike. We are coming from low levels, but it may slow some of the bullish upside seen in futures.

- Back end JGB yields have softened as the session has progressed today, with the 20-40yr tenors down around 2bps. Steadier trends are evident across other parts of the curve. The 10yr JGB yield unable to sustain +1.66% levels.

- The 2/30s JGB curve is to fresh flats of +216bps, levels last seen in early July, see the chart below. As we noted earlier, markets, at this stage, are taking the prospects of fresh fiscal stimulus from the new Takaichi regime relatively well. Comments from officials that fiscal discipline will still be eyed likely calming market sentiment to a degree. We still await exact details of the fiscal package, which could be launched next month.

- On the BoJ, headlines crossed earlier, "EX-BOJ EXECUTIVE MAEDA: BOJ LIKELY TO RAISE INTEREST RATES EITHER IN DECEMBER THIS YEAR OR JANUARY NEXT YEAR, MAEDA: BOJ MAY ALREADY BE SOMEWHAT BEHIND THE CURVE IN ADDRESSING INFLATION RISK" RTRS.

- Market pricing doesn't have a full hike priced until around March next year.

- Note tomorrow we get Nationwide CPI. The market expects headline measures to tick up, but core core to ease to 3.1%y/y from 3.3%.

Fig 1: JGB 2/30s Curve - Flattening Trend Continues

Source: Bloomberg Finance L.P./MNI

JAPAN DATA: Local Investors Sell Offshore Bonds, Japan Equities Remain In Demand

Japan weekly outbound and inbound investment flows were lower in aggregate compared to recent weeks. Local investors sold both offshore bonds and stocks. This has been a theme evident since late Sep and for much of Oct. In the last 4 weeks, cumulative net selling of offshore bonds has been over ¥1.1trln, although noted this doesn't offset the buying seen from late Aug and in the early part of Sep (close to ¥4trln). Global bond returns remain elevated, supported by the break lower in US Tsy yields. On the equity side, cumulative net selling is evident by local investors but the sums are not large.

- In terms of inflows into Japan assets, offshore investors maintained a firm bias for local stocks, bringing net inflows in the past 3 weeks to over ¥5.1trln. Japan equities have surged in Oct trade to date, with dips well supported. Optimism is elevated around the tech/AI space, while new PM Takaichi also has a pro-growth agenda and is therefore seen supportive of local stocks.

- On the bond side, offshore investor flows were close to flat.

Table 1: Japan Weekly Offshore Investment Flows

| Billion Yen | Week ending Oct 17 | Prior Week |

| Foreign Buying Japan Stocks | 752.6 | 1886.6 |

| Foreign Buying Japan Bonds | -0.7 | 201.2 |

| Japan Buying Foreign Bonds | -669.7 | 601.3 |

| Japan Buying Foreign Stocks | -288.1 | 59.2 |

Source: Bloomberg Finance L.P./MNI

AUSSIE BONDS: 10yr Futures Still Threatening Recent Highs, RBA's Bullock Friday

Aussie bond futures have had relatively tight ranges so far today, with 3yr underperforming relative to the 10yr. The 10yr got highs of 95.895, but sits slightly lower now, the 95.90 resistance level intact. The 3yr was last at 96.645. The bias for US Tsy futures is for dips to be supported, with the oil price bounce (post US sanctions news on Russia) not enough to shift sentiment lower so far today.

- Cash ACGB yields are a touch higher, but gains are less than 1bps at this stage, 3yr around 3.35%, while the 10yr is tracking at 4.11%. The 3/10s curve is little changed at +76bps.

- The AU-US 10yr spread is slightly firmer to +16.5bps, but remains well short of recent highs above +30bps.

- The BBG economist survey sees the consensus for the RBA cash rate at 3.35% to end Q1 next year, against a current rate of 3.60%. Market pricing has a cash rate around 3.20% for the March 2026 RBA meeting.

- Note tomorrow we get RBA Bullock speak, while preliminary Oct PMIs are due on the data front.

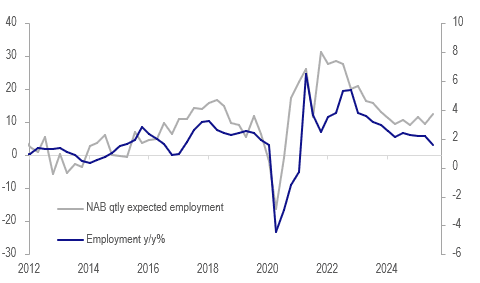

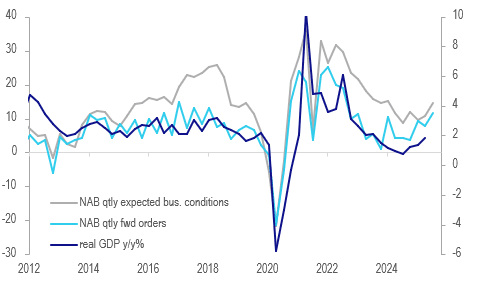

AUSTRALIA DATA: Quarterly NAB Survey Positive On Economic & Jobs Outlook

The Q3 NAB quarterly survey showed that the recovery in the economy continued and the slowdown seen in the labour market may stabilise in Q4 in line with recent SEEK job ad data. NAB employees over the next 12 months rose to its highest since Q1 2024 and labour shortages to its highest since Q4 2024, an indicator monitored by the RBA. This is consistent with a more positive view on the outlook for the economy.

Australia employment outlook

Source: MNI - Market News/LSEG

- Actual business conditions improved 5 points in Q3 to +6.1, while expected conditions rose almost 4 points to 14.6, highest since Q1 2024. In terms of the outlook, expected business confidence printed at +2.2 in Q3 up from -0.4 and the highest in 3 years.

- Suitable labour being a constraint rose to 30.0 from 27.3, expected employment was up 3 points to 12.5 (highest since Q4 2023) and change in employees over next year +2 points to 18.6. At the same time, expected labour costs moderated to 0.6% from Q2’s 1.3%, slightly below the series average.

- Other inflation indicators were back in line with Q1 after rising in Q2 with costs 0.5% and final product prices 0.4%.

- Q3 forward orders were 4 points stronger at 11.8, highest since Q3 2022. However, the export outlook weakened a further 2 points to 2.8, the lowest in a year and likely pressured by fears of weaker demand given increased US protectionism.

Australia growth outlook

Source: MNI - Market News/LSE

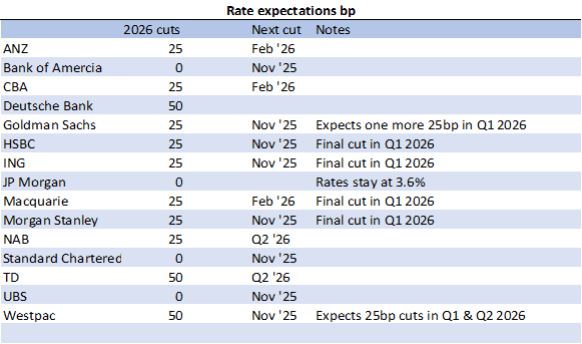

AUSTRALIA: Bloomberg Consensus Expects Q4 24bp Cut & 3.1% Trough

Bloomberg released its October survey of economists and while there was no change in the median cash rate forecast for Q4 2025, forecasts are split between 3.1% and 3.35% for where it will settle and there are even some who believe that the RBA is already done. Q3 CPI on 29 October will be a key input into the 4 November RBA decision.

- Consensus has a 25bp rate cut to 3.35% in Q4, likely in November to coincide with the update staff forecasts, with it staying there in Q1 2026, an upward revision from the September survey’s 3.1%. 25bp of easing to 3.1% is now forecast for Q2.

- The rate outlook is far from unanimous with Westpac forecasting 25bp rate cuts in November, February and Q2 2026, while JP Morgan believes rates will stay where they are now at 3.6%.

- 2025 CPI projections have been revised up 0.1pp to 2.6%, likely reflecting higher monthly prints in Q3. 2026 remains at 2.7%, above the mid-point of the band.

- Q3 GDP is forecast to rise 0.5% q/q on 3 December after Q2’s 0.6%. Q4 is expected to be 0.6%.

RBA rate expectations bp

Source: MNI - Market News/Bloomberg Finance L.P.

BONDS: NZGBS: NZ-US 10yr Back Closer To Fair Value Estimate, As Local Yields Up

NZGB yields have firmed as Thursday's Asia Pac session unfolded, outperforming a still soft US Tsy yield backdrop. The NZ-US 10yr spread is back to +3bps, up from flat levels and getting back closer to our fair value estimate around +6bps. The 2yr NZGB yield is near 2.52%, little changed today, with more shifts in the back end, the 10yr back to 3.96%, up almost 2bps. The NZ 2/10s curve is a touch steeper at +144.5bps, but off earlier Oct highs (+154bps).

- Spillover from the oil price bounce may a factor for higher NZGB yields today, although there isn't impacting US or Aust markets as much. As we noted the NZ-US spread widening is consistent with our fair value analysis.

- As we noted in our earlier update, since Monday's Q3 CPI update, NZ yields have struggled for further downside, as we await a fresh catalyst (technicals still point to lower yield levels). The 2yr swap rate is little changed today, last at 2.30%, just up from recent lows.

- BBG noted, as part of its consensus survey for NZ: "Economists expected New Zealand 3Q 2025 GDP at +1.0% y/y, the lowest forecast since survey’s inception;", although arguably this is already in the price from a rates perspective. The same survey noted economists cash rate to trough at 2.25% into 2026.

- Current market pricing has a tough around 2.09% for the Sep meeting next year (per OIS pricing).

FOREX: USD Index To Fresh Weekly Highs As Oil Spikes On Sanction News

The USD BBDXY index has climbed to fresh highs for the week (last 1214.3), reversing Wednesday's modest pull back. Earlier Oct highs around 1220 are still intact. The main macro focus point today has been higher oil prices, with crude benchmarks up around 3%, following US sanctions news on Russian producers. Insofar as the US terms of trade are positively correlated with energy prices, this has arguably lent USD support today. Yen has been the weakest performer. Cross asset trends elsewhere have been steadier, US equity futures are higher, but only marginally, while Tsy yields are close to flat (albeit up from earlier lows).

- USD/JPY is looking to consolidate its break above 152.00 (session highs rest at 152.57, last near 152.45/50). Citi's Japan terms of trade proxy is weaker, but still close to recent highs (-21.1 so remaining in negative territory). We haven't heard from the Japanese authorities following this recent round of FX weakness.

- Technically, USD/JPY is close to Oct 14 highs (152.61), while beyond that lies the 153.27 level, highs from Oct 10 and also the bull trigger level.

- Elsewhere AUD and NZD are drifting lower, but remain within recent ranges. AUD/USD is near 0.6480, while NZD/USD is under 0.5730, with this pair still finding selling interest on moves to 0.5760.

- There is weakness in tech related equities today, with nervousness around potential further US curbs on software exports to China. Only the NKY 225 has seen losses beyond 1% though.

- The AUD and NZD are still up against yen as well, with AUD/JPY closing in near 99.00.

- Later US September existing home sales and October Kansas Fed manufacturing print as well as August Canadian retail sales and euro area preliminary October consumer confidence. The Euro summit takes place and ECB’s Lane speaks.

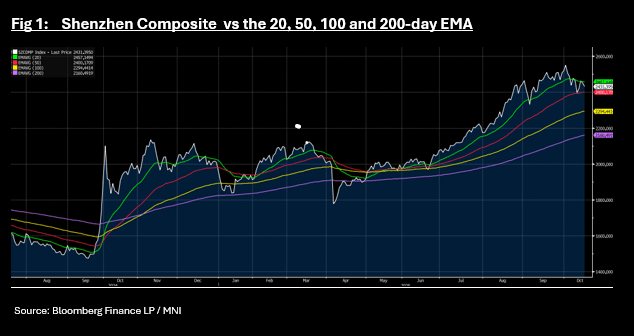

ASIA STOCKS: White House Rumours Roil Tech, Shenzhen Bounces of Key Tech Level

News that the White House is considering export restrictions on critical software to China was enough to push on a tech sector already reaching new highs and investors seemingly willing to take profit (as per Reuters). Samsung lead the KOSPI down just as TSMC did in Taiwan, whilst Softbank was key contributor to the NIKKEI's decline. The news adds to the already heightened level of concern around US China tensions and with many bourses in the region at new highs, profit taking appears a key driver of risk appetite at present.

- The NIKKEI has retreated off its new highs, down -1.4% today with a -690pt decline. The NIKKEI maintains its position above all major moving averages, all of which remain upward sloping, an indication that the positive momentum could continue.

- The KOSPI is lower by -0.55% after closing Wednesday at new highs of 3,883 yet remains up over 3% for the week.

- The Hang Seng has done very little all day as it trends around the 50-day EMA of 25,851 as the fall of -0.5% by the CSI 300 sees it near to the 20-day EMA of 4,561. The Shanghai Comp is down -0.6% and Shenzhen the largest faller, down -0.8%, bouncing off the 20-day EMA of 2,457 it trended below this week. Below the 50-day EMA is at 2,400.

- The NIFTY 50 is trending higher again on suggestions that a US trade deal is closer, and is up +0.50% in morning trade to reach a new high of 26,002 pushing further above all major moving averages.

OIL: Crude Continues Rally, US Russia Sanctions Make Indian Refining Difficult

The news flow continues to be supportive for oil prices with the US Treasury announcing sanctions on large Russian oil producers and reports they will mean Indian imports of Russian crude will trend towards zero. As a result, it will compete for supplies from other producers supporting global prices. WTI is up 3.2% to $60.38/bbl, close to the intraday high of $60.42 but below the 50-day EMA at $61.76. Brent is 3.0% higher at $64.46/bbl, close to today’s peak but below resistance at $65.19, and up 5% this week.

- Following the UK, US restrictions will be imposed against Lukoil and state-run Rosneft, two of the largest producers, aimed at reducing revenues for Russia’s war. They may have more impact than previous sanctions. Lukoil and Rosneft accounted for 2.2mbd in H1, according to Bloomberg.

- Indian refiners have said that the US measures against Rosneft and Lukoil will make it extremely difficult for them to continue using Russian crude. India is the second largest importer of Russian oil after China. President Trump said he would probably discuss China’s consumption at next week’s meeting with President Xi.

- The EU is meeting today to discuss and probably agree to another package of sanctions on Russia including export bans on items its military uses, blacklisting another 100 tankers, restrictions on Russian/Central Asian banks and trade limitations on India and China, according to Bloomberg.

- Later US September existing home sales and October Kansas Fed manufacturing print as well as August Canadian retail sales and euro area preliminary October consumer confidence. The Euro summit takes place and ECB’s Lane speaks.

Gold Holding Onto Losses, Remains Overbought

Gold prices are little changed ahead of Friday’s US September CPI data but they have held onto this week’s losses of around 3.7%. They fell to $4066.30/oz but have recovered to be down 0.2% to $4091.0. Bullion is being pressured by a stronger US dollar (BBDXY +0.2%) and the prospect of a US-China trade deal with Presidents Trump and Xi due to meet next week. Bloomberg is also reporting large ETF outflows.

- Gold should continue to receive medium-term support from central bank and ETF buying as well as concern over large G7 government deficits, global uncertainty especially around tariffs and their impact which could include monetary easing. Lower rates benefit non-yield bearing gold. Also there seems little progress towards ending the US government shutdown, anyway publicly.

- Silver is little changed at around $48.50 but still below the 20-day EMA at $49.053. It fell to $47.925 early in the session and then recovered to $48.715. It remains pressured by profit taking given it also continues to be overbought.

- Equities are mixed with the S&P e-mini up 0.1%, Hang Seng down 0.1% and Nikkei -1.4%. Oil prices are higher with WTI +3.0% to $60.24/bbl. Copper is up 0.2%.

- Later US September existing home sales and October Kansas Fed manufacturing print as well as August Canadian retail sales and euro area preliminary October consumer confidence. The Euro summit takes place and ECB’s Lane speaks.

SOUTH KOREA: BOK Press Release Key Points

- The Monetary Policy Board of the Bank of Korea decided today to leave the Base Rate unchanged at 2.50% today describing inflation as stable and economic growth in an upward trend thanks to improving consumption and exports (driven by semi conductor demand).

- The board felt that it is necessary to further monitor financial stability conditions, such as the effects of real estate market stabilization measures on housing markets in Seoul and its surrounding areas and on household debt, as well as exchange rate volatility given trade negotiations remaining outstanding. .

- They currently suggest that the global economy is expected to slow modestly in growth and experience a divergence in inflation trajectories across countries as the impact of U.S. tariff increases starts to materialize.

- The BOK sees the growth rate as generally consistent with the August forecast of 0.9% for this year and of 1.6% for next year, noting that both upside and downside uncertainties have increased, stemming from factors such as trade negotiations between Korea and the U.S. and between the U.S. and China, developments in the semiconductor industry, and the pace of recovery in domestic demand.

- The BOK next meets November 27.

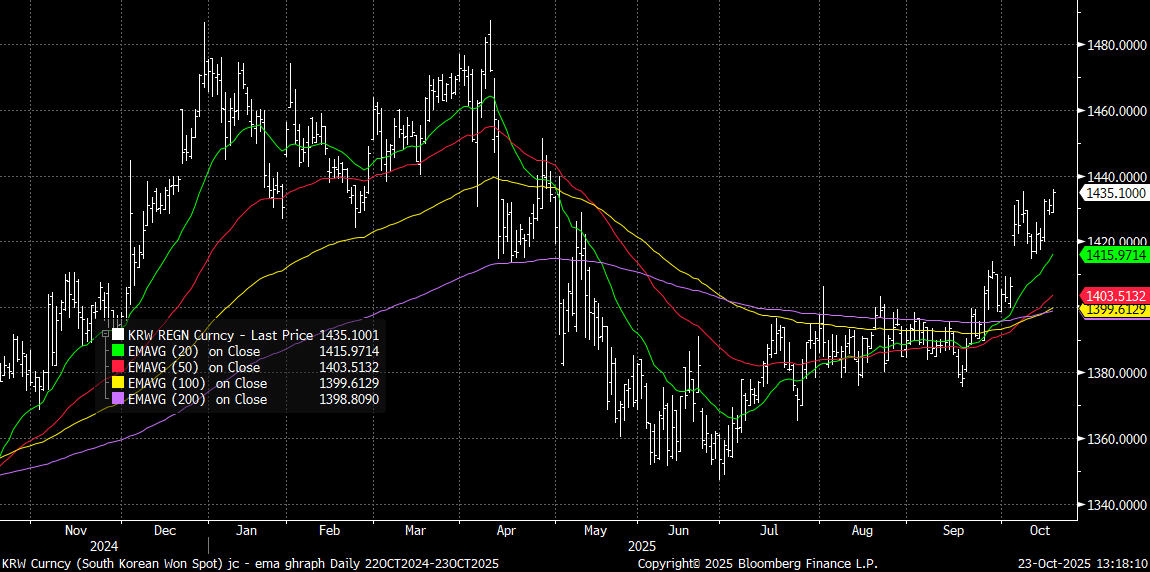

KRW: USD/KRW Eyeing Break Higher, Amid Firmer USD, BoK Mindful Of Vol

USD/KRW is probing earlier Oct highs, as the market digests the BOK on hold outcome from earlier. Spill over from higher USD/JPY levels is evident (last near 152.50).For USD/KRW we sit just under earlier highs (1435.85), which were levels last seen in early May. A clean break higher could see the 1440/1450 region targeted, see the chart below.

- The BoK kept an easing bias, with 4 out of 6 board members seeing scope to lower rates within 3 months, while one member called for a cut today. Governor Rhee noted the majority of the board were focused on financial stability, and wanted time to assess government measures to cool the housing market. High FX volatility was a both a cautious point and something the central bank needed to monitor.

- This suggests any fresh move higher in USD/KRW may be gradual rather than dramatic. Implied vols support such a bias, as we are back under 8%, well off earlier 2025 highs.

- The won remains a laggard in terms of the lower US-SK rate differentials and still elevated equities (both globally and local), although sentiment looks a little more cautious in this space.

- However, until broader USD sentiment looks softer (particularly from a USD/JPY standpoint, as JPY/KRW levels are watched from a competitiveness standpoint), it may be difficult to call a top in USD/KRW.

Fig 1: USD/KRW Spot At Risk Of Breaking Higher, But Implied Vols Contained

Source: Bloomberg Finance L.P./MNI

INDONESIA: October Pause As BI Leaves Door Open To Further Easing

Again Bank Indonesia (BI) surprised by doing the opposite of consensus expectations. On Wednesday it held rates at 4.75% when it had been forecast to cut 25bp. This pause followed three consecutive monthly rate cuts. BI’s assessment of the economy and the need to support growth was broadly unchanged from last month when it eased, so another rate cut in November or December remains likely. It maintained its willingness to support government measures to boost the economy.

- The reasons for the hold were in line with those given for September’s rate cut – the decision was consistent with inflation within the target band, with FX stability and cooperation to boost growth. However, it has added the transmission mechanism to the monitoring list in the first paragraph.

- In September BI voiced its concern that lending rates were only marginally lower despite 125bp of easing in 2025 and now this month it is “monitoring the transmission effectiveness of accommodative monetary policy”.

- It continues to see the global economy moderating, domestic growth as solid but below capacity, IDR stable, inflation within the corridor and BoP “sound”.

- It no longer seemed concerned about the impact of softer consumer confidence on consumption even though it moderated in September to 115.0 from 117.2, the lowest since April 2022. It did state that “there remains a further opportunity to strengthen domestic demand”. It noted that core inflation was being pressured by spare capacity.

- It kept its 2025 growth forecast unchanged at “above the midpoint of the 4.6-5.4% range” and that 2026 will be stronger. Q3 growth was driven by exports and government spending.

UP TODAY (TIMES GMT/LOCAL)

| Date | GMT/Local | Impact | Country | Event |

| 23/10/2025 | 0645/0845 | ** | Manufacturing Sentiment | |

| 23/10/2025 | 0730/0930 | SNB Minutes | ||

| 23/10/2025 | 0900/1000 | ** | Gilt Outright Auction Result | |

| 23/10/2025 | 1000/1100 | ** | CBI Industrial Trends | |

| 23/10/2025 | 1100/0700 | *** | Turkey Benchmark Rate | |

| 23/10/2025 | - | ECB Lagarde at Euro Summit in Brussels | ||

| 23/10/2025 | 1230/0830 | *** | Jobless Claims | |

| 23/10/2025 | 1230/0830 | ** | WASDE Weekly Import/Export | |

| 23/10/2025 | 1230/0830 | ** | Retail Trade | |

| 23/10/2025 | 1230/0830 | ** | Retail Trade | |

| 23/10/2025 | 1330/1530 | ECB Lane Award Acceptance Speech | ||

| 23/10/2025 | 1400/1000 | *** | NAR existing home sales | |

| 23/10/2025 | 1400/1600 | ** | Consumer Confidence Indicator (p) | |

| 23/10/2025 | 1400/1000 | Fed Vice Chair Michelle Bowman | ||

| 23/10/2025 | 1425/1025 | Fed Governor Michael Barr | ||

| 23/10/2025 | 1430/1030 | ** | Natural Gas Stocks | |

| 23/10/2025 | 1500/1100 | ** | Kansas City Fed Manufacturing Index | |

| 23/10/2025 | 1530/1130 | * | US Bill 08 Week Treasury Auction Result | |

| 23/10/2025 | 1530/1130 | ** | US Bill 04 Week Treasury Auction Result | |

| 23/10/2025 | 1700/1300 | ** | US Treasury Auction Result for TIPS 5 Year Note | |

| 24/10/2025 | 2200/0900 | *** | Judo Bank Flash Australia PMI | |

| 24/10/2025 | 2301/0001 | ** | Gfk Monthly Consumer Confidence | |

| 24/10/2025 | 2330/0830 | *** | CPI | |

| 24/10/2025 | 0030/0930 | ** | Jibun Bank Flash Japan PMI | |

| 24/10/2025 | 0600/0800 | ** | PPI | |

| 24/10/2025 | 0600/0700 | *** | Retail Sales | |

| 24/10/2025 | 0645/0845 | ** | Consumer Sentiment | |

| 24/10/2025 | 0700/0900 | ** | PPI | |

| 24/10/2025 | 0715/0915 | ** | S&P Global Services PMI (p) | |

| 24/10/2025 | 0715/0915 | ** | S&P Global Manufacturing PMI (p) | |

| 24/10/2025 | 0730/0930 | ** | S&P Global Services PMI (p) | |

| 24/10/2025 | 0730/0930 | ** | S&P Global Manufacturing PMI (p) | |

| 24/10/2025 | 0800/1000 | ** | S&P Global Services PMI (p) | |

| 24/10/2025 | 0800/1000 | ** | S&P Global Manufacturing PMI (p) | |

| 24/10/2025 | 0800/1000 | ** | S&P Global Composite PMI (p) | |

| 24/10/2025 | 0800/1000 | ECB Cipollone Fireside Chat on International Finance | ||

| 24/10/2025 | 0830/0930 | *** | S&P Global Manufacturing PMI flash | |

| 24/10/2025 | 0830/0930 | *** | S&P Global Services PMI flash | |

| 24/10/2025 | 0830/0930 | *** | S&P Global Composite PMI flash | |

| 24/10/2025 | 1200/0800 | ** | Brazil Preliminary CPI | |

| 24/10/2025 | 1230/0830 | *** | CPI | |

| 24/10/2025 | 1230/0830 | *** | CPI | |

| 24/10/2025 | 1230/0830 | *** | CPI | |

| 24/10/2025 | 1300/1500 | ** | BNB Business Confidence | |

| 24/10/2025 | 1345/0945 | *** | S&P Global Manufacturing Index (Flash) | |

| 24/10/2025 | 1345/0945 | *** | S&P Global Services Index (flash) |