JGBS: 2/30s Curve Flattest Since Early July, Sep CPI Due Tomorrow

JGB futures sit at 136.17, +.01 versus settlement levels in latest dealings, after a 136.11-136.32 range so far today. For JGB futures we are maintaining familiar ranges for now, with US Tsy futures generally biased higher, whilst fiscal concerns in Japan may be limiting the upside (albeit with such fears dissipating somewhat so far this week). The other focus point today has been the oil price spike. We are coming from low levels, but it may slow some of the bullish upside seen in futures.

- Back end JGB yields have softened as the session has progressed today, with the 20-40yr tenors down around 2bps. Steadier trends are evident across other parts of the curve. The 10yr JGB yield unable to sustain +1.66% levels.

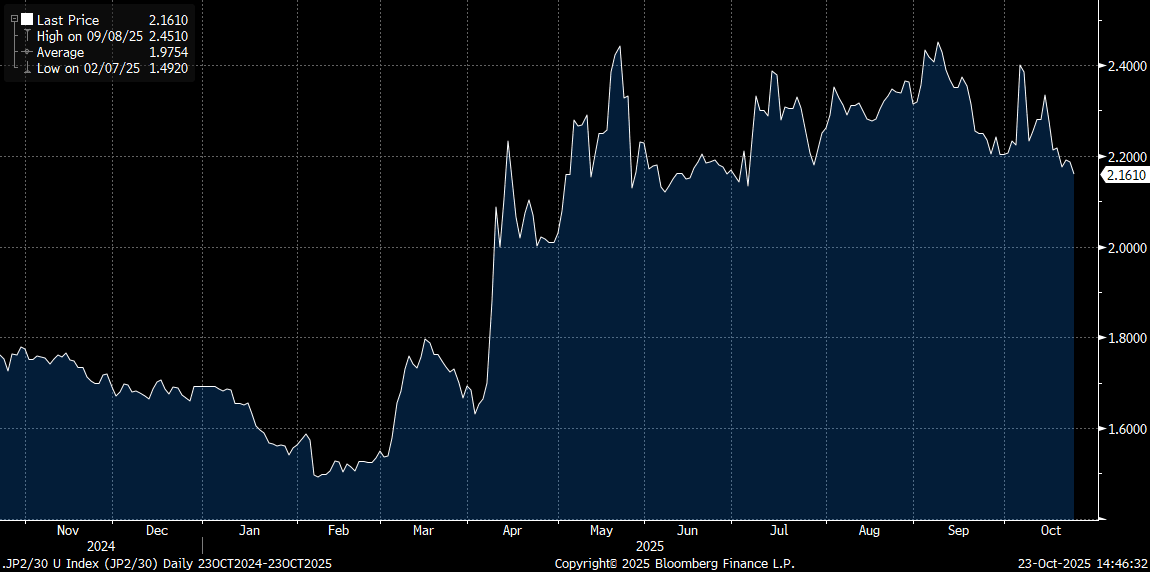

- The 2/30s JGB curve is to fresh flats of +216bps, levels last seen in early July, see the chart below. As we noted earlier, markets, at this stage, are taking the prospects of fresh fiscal stimulus from the new Takaichi regime relatively well. Comments from officials that fiscal discipline will still be eyed likely calming market sentiment to a degree. We still await exact details of the fiscal package, which could be launched next month.

- On the BoJ, headlines crossed earlier, "EX-BOJ EXECUTIVE MAEDA: BOJ LIKELY TO RAISE INTEREST RATES EITHER IN DECEMBER THIS YEAR OR JANUARY NEXT YEAR, MAEDA: BOJ MAY ALREADY BE SOMEWHAT BEHIND THE CURVE IN ADDRESSING INFLATION RISK" RTRS.

- Market pricing doesn't have a full hike priced until around March next year.

- Note tomorrow we get Nationwide CPI. The market expects headline measures to tick up, but core core to ease to 3.1%y/y from 3.3%.

Fig 1: JGB 2/30s Curve - Flattening Trend Continues

Source: Bloomberg Finance L.P./MNI

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

ASIA STOCKS: China Stocks Decline Following No Announcements

A press conference Monday by Chinese financial regulators — including the PBOC governor and banking and stock market supervisors — drew attention from investors as it is about one year ago when a similar meeting saw a broad package of policy easing measures including RRR and interest rate cuts announced. With no such announcements forthcoming, China's equity bourses are all down today whilst other regional bourses delivered gains.

- The Hang Seng fell yesterday on BYD news and is lower again today by -0.96%. The CSI 300 is down -1.19%, the Shanghai Comp down -1.23% and the Shenzhen Comp down -2.27% .

- The KOSPI is up +0.51% today as Samsung makes new all time highs.

- The TAIEX in Taiwan is up strongly by +1.1% reaching another new high for the index.

- The FTSE Malay KLCI remains stuck at present and is where it started the day at 1,603.

- The Jakarta Comp is hitting new highs of 8,087 today, to be up +0.55%.

- The FTSE Straits Times is up +0.36% and the PSEi in the Philippines +0.30%.

- The NIFTY 50 is lower by -0.23% and continues to underperform regional peers, down for a third successive day.

BUND TECHS: (Z5) Trading Closer To Its Recent Lows

- RES 4: 129.50 High Aug 5

- RES 3: 129.44 High Sep 10 and key short-term resistance

- RES 2: 129.13 High Sep 17

- RES 1: 128.60 20-day EMA

- PRICE: 128.25 @ 05:27 BST Sep 23

- SUP 1: 128.01 Low Sep 23

- SUP 2: 127.61 Low Sep 3 and the bear trigger

- SUP 3: 127.46 1.00 proj of the Aug 14 - 15 - 28 price swing

- SUP 4: 127.13 1.236 proj of the Aug 14 - 15 - 28 price swing

Bund futures remain below their latest highs and are trading closer to their recent lows. Key support and the bear trigger lies at 127.61, the Sep 3 low. A break if this level would cancel a recent bullish theme and confirm a continuation of the medium-term bear cycle. For bulls, a reversal higher would refocus attention on key resistance at 129.44, the Sep 10 high. First resistance is at 128.60, the 20-day EMA.

AUSSIE BONDS: Little Changed, August CPI Tomorrow

ACGBs (YM -1.0 & XM -0.5) are modestly weaker on a data-light session.

- There was no cash US tsy trading in today's Asia-Pac session, with Japan closed for a holiday.

- Cash ACGBs are 2bps cheaper.

- The bills strip is -1 to -2 across contracts.

- RBA-dated OIS pricing is giving a 25bp rate cut in September a 4% probability, with a cumulative 25bps of easing priced by year-end (based on an effective cash rate of 3.60%).

- The AOFM plans to sell A$1000mn of the 3.00%21 November 2033 bond on Wednesday and A$900mn of the 2.75% 21 November 2029 bond on Friday.

- Tomorrow, the local calendar will see August CPI data.

- (Bloomberg Economics) “Australia’s August CPI report is likely to show inflation holding firm near the top of the Reserve Bank of Australia’s 2%-3% target band. We estimate annual CPI growth stayed at 2.8%, unchanged from July. The annual electricity price increase boosted the July reading, but this will be partially unwound by the federal government’s subsidy in August.”