JAPAN DATA: Local Investors Sell Offshore Bonds, Japan Equities Remain In Demand

Japan weekly outbound and inbound investment flows were lower in aggregate compared to recent weeks. Local investors sold both offshore bonds and stocks. This has been a theme evident since late Sep and for much of Oct. In the last 4 weeks, cumulative net selling of offshore bonds has been over ¥1.1trln, although noted this doesn't offset the buying seen from late Aug and in the early part of Sep (close to ¥4trln). Global bond returns remain elevated, supported by the break lower in US Tsy yields. On the equity side, cumulative net selling is evident by local investors but the sums are not large.

- In terms of inflows into Japan assets, offshore investors maintained a firm bias for local stocks, bringing net inflows in the past 3 weeks to over ¥5.1trln. Japan equities have surged in Oct trade to date, with dips well supported. Optimism is elevated around the tech/AI space, while new PM Takaichi also has a pro-growth agenda and is therefore seen supportive of local stocks.

- On the bond side, offshore investor flows were close to flat.

Table 1: Japan Weekly Offshore Investment Flows

| Billion Yen | Week ending Oct 17 | Prior Week |

| Foreign Buying Japan Stocks | 752.6 | 1886.6 |

| Foreign Buying Japan Bonds | -0.7 | 201.2 |

| Japan Buying Foreign Bonds | -669.7 | 601.3 |

| Japan Buying Foreign Stocks | -288.1 | 59.2 |

Source: Bloomberg Finance L.P./MNI

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

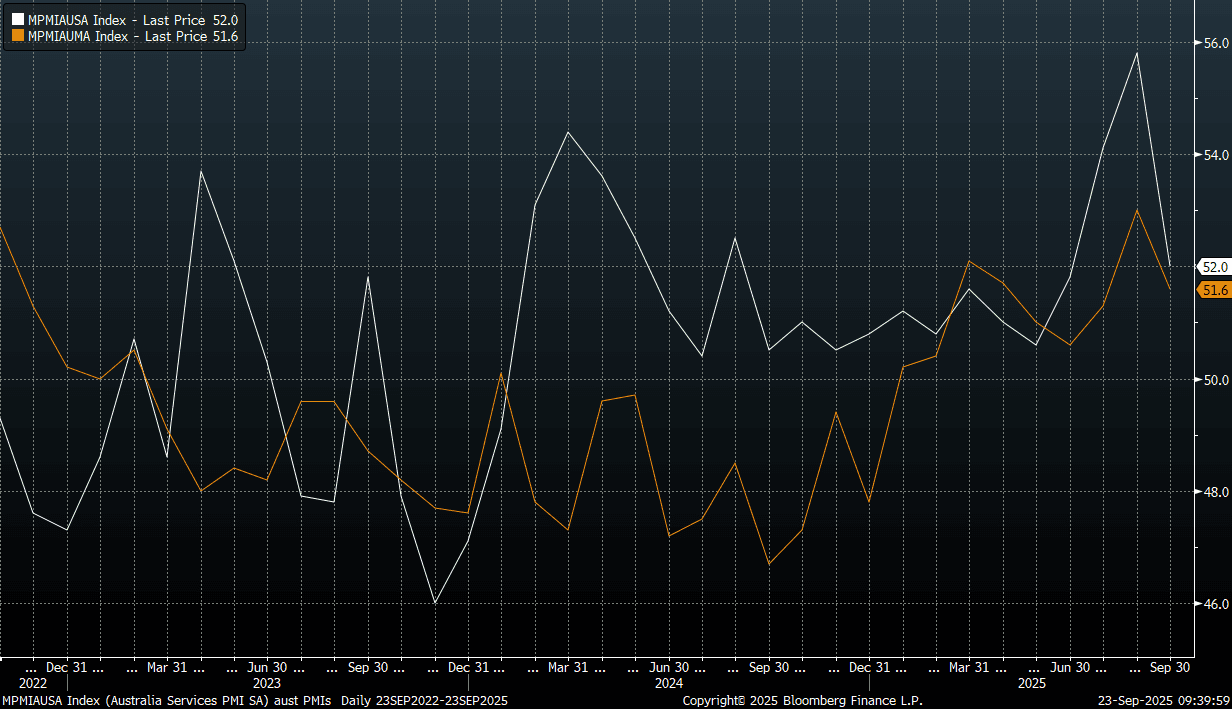

AUSTRALIA DATA: September PMIs Off Recent Highs, But Q3 Average Higher

Australian preliminary PMIs for September fell from their August levels. The manufacturing print came in at 51.6, from 53.0, while services were at 52.0 from 55.8 in August (see the chart below). This saw the composite PMI come in at 52.1 from 55.5.

- Despite the pullback in the Sep PMIs, the average readings for Q3 were still above those seen in both Q2 and Q1 of this year. For manufacturing, the Q3 average was just under 52.0 (Q2 average was 51.1), while for service the Q3 average was 54, against a 51.1 Q2 average.

- In terms of the detail, for manufacturing output fell to 52.9 from 53.8, while new orders were also down for the month. On the services side, employment eased down to 53.3 form 53.7 prior (per BBG).

- These comes come ahead of next week's RBA decision. The RBA Governor appeared before parliament yesterday, noting that data outcomes since the last policy meeting in August had been either as expected or slightly firmer.

- Note tomorrow we get August monthly CPI.

Fig 1: Australian PMIs Off Q3 Highs (Manufacturing Orange, Services White)

Source: Bloomberg Finance L.P./MNI

AUSSIE BONDS: Modestly Cheaper With US Tsys

ACGBs (YM -2.0 & XM -1.5) are modestly weaker after US tsys finished 2-3bps cheaper.

- MNI FED: Cleveland's Hammack: Policy Very Mildly Restrictive, Concerns On More Cuts. Cleveland Fed President Hammack (hawk, 2026 FOMC voter) sounds extremely cautious about making further cuts: "I am laser focused on inflation. And that's why to me, I think that we should be very cautious in removing monetary policy restriction, because I think it's important that we stay restrictive to bring inflation back down to target.

- There will be no cash US tsy trading in Asia-Pac today with Japan out.

- S&P Global Sept. Flash PMIs have printed: Mfg PMI 51.6 vs 53 Prior; Composite 52.1 vs 55.5 Prior; and Services 52.0 vs 55.8 Prior".

- Cash ACGBs are 3bps cheaper with the AU-US 10-year yield differential +13bps.

- The bills strip is -2 to -3 across contracts.

- RBA-dated OIS pricing is giving a 25bp rate cut in September a 4% probability, with a cumulative 25bps of easing priced by year-end (based on an effective cash rate of 3.60%).

- This week, the AOFM plans to sell A$300mn of the 4.75% 21 June 2054 bond today, A$1000mn of the 3.00% 21 November 2033 bond on Wednesday and A$900mn of the 2.75% 21 November 2029 bond on Friday.

BONDS: NZGBS: Little Changed, New RBNZ Gov. Announced Tomorrow

In local morning trade, NZGBs are unchanged despite US tsys finishing yesterday’s session with moderate losses.

- Headlines have crossed from BBG that the new RBNZ Governor could be announced tomorrow. BBG note: "New Zealand is set to appoint a woman to head its central bank for the first time as it seeks to refresh an institution damaged by leadership turmoil.", while also noting the new Governor was expected to come from offshore (i.e. was not a New Zealander).

- The appointment comes at a time after recent upheaval for the RBNZ. Governor Orr left the post abruptly in March, while Chair of RBNZ board, Neil Quiqley also left recently. Last week's Q2 GDP data was weaker than market and RBNZ forecasts, driving further easing expectations in terms of the market outlook.

- Swap rates are little changed.

- RBNZ dated OIS pricing is little changed across meetings. 33bps of easing is priced for October, with a cumulative 59bps by November 2025.

- The local calendar will be empty until Friday's Consumer Confidence data.

- On Thursday, the NZ Treasury plans to sell NZ$250mn of the 4.50% May-30 bond and NZ$200mn of the 3.50% Apr-33 bond.